Oct

31

What the Spec List Is, from DailySpeculations

October 31, 2016 | 2 Comments

Welcome to the Speculators list. We are a group of about 250 who bring various approaches to investing and trading in the markets ranging from quantitative/empirical to highly qualitative. Our group contains individuals from a wide variety of backgrounds including academia (both professors and students), journalism, portfolio management and trading, science, coaching, psychology, medical research, technology, and software development. Some of our members are active in several of the above. We encourage contributions on topics that link almost any field (biology, psychology, or sports to name a few) to speculation in the markets.

Welcome to the Speculators list. We are a group of about 250 who bring various approaches to investing and trading in the markets ranging from quantitative/empirical to highly qualitative. Our group contains individuals from a wide variety of backgrounds including academia (both professors and students), journalism, portfolio management and trading, science, coaching, psychology, medical research, technology, and software development. Some of our members are active in several of the above. We encourage contributions on topics that link almost any field (biology, psychology, or sports to name a few) to speculation in the markets.

We try to foster an ambiance of an extended dinner party and in support of this objective one of our few rules are to refrain from personal attacks on other members (while vigorous debates on the merit of topics are encouraged ) upon punishment of buying a round of drinks to all members (Ben Franklin style ) . In addition, some periodic participation is expected ("lurking" is discouraged and occasionally inactive members are removed ). Along these lines, part of the requirements for new members is to send a brief bio to the list shortly after joining so the members can get to know you (a brief bio being mandatory for participation).

We also ask that members try to keep their posts market related as we find this helps keep our many busy professionals interested and active in the discussions. Members are expected to respect the privacy of others in the group in general, and specifically ask that members do not forward posts by other members to third parties outside the group.

If a member wants to refer other members to an outside source (a web page link for example) they should provide a brief abstract to help others decide if its something that interests them. Original thoughts and analysis of members is generally preferred over news found in the typical sources. For a more complete list of our general content and posting guidelines we ask that you please read the section below labeled "General Spec-List Guidlines".

As part of membership on the spec list you will also be subscribed to a separate list for a wider range of topics (called the Open-SpecList) that would generally be deemed off topic or inappropriate for the spec-list. If after some time you feel that your posts are mainly on markets and speculation, and you would prefer not to receive the open list post, please let us know and you will be unsubscribed. Many members find this list useful for postings on current events, politics, cultural issues, etc.

On the issue of what's significant enough to send to the various lists, one of our stalwart members offers the following:

"Is this post be worth reading a day, week or month from now? If yes, send to Spec-List. Otherwise, is this post worth reading right now? If yes, send to Open-List. If no, send to your email buddies "

Finally, perhaps the list can best be understood by the words of William Haynes, one of our most esteemed members in a letter to Victor and Laurel.

The List.

What is "The List"? It is often a window on the souls of its members. And a window on our own souls is often opened when we read what others write here. It is lessons on life. Chess strategies. Investment in markets, life, family, nation and the future. It can be and often is profound and superficial; deep and shallow and always enlightening, even when a writer may not be. It sends out tendrils seeking answers and finds them, coiled about ideas we would never have found alone. The List lives and throbs with the insights, prejudices, wants and experiences of the members. There is a selection process at work here, as some find an intellectual home … others move in for a while and then move on. Those who remain don't always agree and contention boils up, simmers and fades, sometimes leaving a residue of hostility but never, never boredom. The List is ephemeral. Although there are rumors that somewhere everything ever posted on the web is archived, the sheer quantity of material generated makes that less than credible. So our moving fingers write, and having writ move on, leaving little more than fading memories, but building new ideas and broadening the thinking of we who read, and answer, and ponder, blending what is read into a tapestry that, but for the List would never have been woven. Surely we, the weavers are much the better for it, and must acknowledge the debt each of us owes to each other, and to the two who first spread the warp and the woof.

Oct

31

Rational Decision-Making Under Uncertainty, from Patrick Boyle

October 31, 2016 | 1 Comment

This is a paper by Victor Haghani of LTCM fame on bet sizing observing and analysing how people place bets on a coin flip that is biased to come up heads 60% of the time.

This is a paper by Victor Haghani of LTCM fame on bet sizing observing and analysing how people place bets on a coin flip that is biased to come up heads 60% of the time.

Ralph Vince writes:

It's a very interesting paper, and to many might be surprising. A couple of comments:

1. It assumes someone's criterion in wagering on this is to maximize what someone makes. This is certainly not the case in capital markets, where (the rather nebulous) risk-adjusted return is king, specfically: "Optimal F: Calculating the Expected Growth-Optimal Fraction for Discretely-Distributed Outcomes"

2. Even what the authors and Thorp himself claim are the amounts to wager so as to maximize expected gain, their answer is not quite aggressive enough! The amounts the refer to are asymptotic, as the number of trials ever-increases. The author himself points to a horizon of 300 plays in half an hour, and the actual optimal wager (which would, int hat time period, yield a greater return than the authors or Thorp point to) is slightly more aggressive, and can be determined from the above paper.

Not trying to toot my own horn (it needs no tooting, and besides, my horn will do a lot, but tooting it won't do) but the paper is inaccurate on these two points.

Jim Sogi writes:

Thank you for the interesting article. The other night at our band practice, the bass player's wife, who works at a public school, asked me if I was taking my money out of the market. She had heard a number of people were worried about the election and a market drop if either candidate was elected. I told her the market would probably go up, though it might jump around a bit. I thought that was interesting. Its an example of the public doing the wrong thing, for the wrong reasons. It reflects peoples fear about uncertainty about the election. It helps explain some of the market action recently.

Rocky Humbert writes:

Mr. Sogi's anecdote and conclusion is a textbook example of Confirmation Bias — which is the tendency to search for, interpret, favor and recall information in a way that confirms one's preexisting beliefs or hypotheses.

To wit: On what basis does Mr. Sogi conclude that the bass player's wife represents the "public" — as distinct from Mr. Sogi himself being the "public" ??!!

How the stock market will perform over the next 30 or 60 days has very little to do with the study of a coin that is heavily loaded to land on heads. At best, the stock market's performance over the next 30 days is only slightly better than 50:50.

Alston Mabry writes:

Just had to do a quick sim of their betting game.

{kind=link}

Oct

31

Swifts and the Aerial Lifestyle, from Pitt T. Maner III

October 31, 2016 | Leave a Comment

Swifts have an amazing ability to stay aloft.

Swifts have an amazing ability to stay aloft.

1) 'Lead researcher Anders Hendenstrom, professor of biology at Lund University, said: "It's mind-boggling that they can stair airborne for 10 months without needing to come down. "Most of the time there is a trade-off between energy use and life: live hard and die young. "But these birds live quite long, up to 20 years, so somehow they have beaten this rule."

and

2) Why come down when it is safer to stay aloft? "So, what are the main selective forces leading to such an extreme aerial lifestyle as found in swifts? One factor could be that specializing in high-altitude aerial insects as a main food source requires the suite of adaptations for efficient flight shown by swifts which compromises terrestrial locomotion and make swifts vulnerable to predators and parasites had they been landing more often. Our data suggest that even if common swifts settle to roost occasionally, which has been observed also in young swifts if the weather is bad their predominant element during the 10-month non-breeding period is up in the air."

Oct

31

Fracking, from Pitt T. Maner III

October 31, 2016 | Leave a Comment

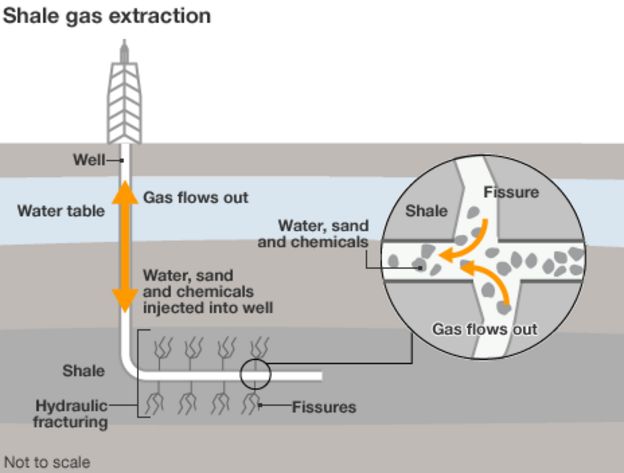

I find it interesting the difference in public and private thoughts on fracking by the cattle trader. And also the price trajectories of the proppant companies. Sand companies (increased amounts now being used per well) have rebounded. On the other hand a leading ceramic (more useful in higher pressure/deeper wells) proppant producer hitting rock bottom. A tough business to be in.

I find it interesting the difference in public and private thoughts on fracking by the cattle trader. And also the price trajectories of the proppant companies. Sand companies (increased amounts now being used per well) have rebounded. On the other hand a leading ceramic (more useful in higher pressure/deeper wells) proppant producer hitting rock bottom. A tough business to be in.

"Chesapeake Energy Declares ‘Propageddon’ With Record Frack":

'The super-sized dose of sand — known as "proppant" — is able to prop open bigger and more numerous cracks in the rock for oil and gas to flow. Output from the well increased 70 percent over traditional fracking techniques, Jason Pigott, vice president of operations, said during a presentation.

"What we're doing is unleashing hell on every gas molecule downhole," Pigott said.'

Oct

31

Post Human Investing, from Stefan Martinek

October 31, 2016 | Leave a Comment

The idea of systematic trading was not generally accepted 10-15 years ago. Markets were mostly viewed as efficient at that point. Or mostly efficient and any excess returns were just a compensation for risk taking – still efficient in a loose definition of efficiency. Today, trading systems are everywhere. Systems are now called "indexes" or "smart beta". Different strategies are now called "factors". Is 2/20 fee structure going the way CD, Dodo, floor broker, etc. If outperformance can be replicated by some "factors", who needs an expensive trader/manager?

Peter Pinkhaven writes:

"Strategies that have reasonable sharpe ratios are usually cyclical" - Asness

I believe AQR were one of the pioneers of the recent systematic factor investing.

Bill Rafter writes:

The automatic trading systems make the markets more efficient and more liquid. They are not predictive but extremely efficient in their reactivity. What the spec should do is view that as an advantage rather than a problem. It would only be a problem if he were a scalper. There is a very good solution to this for the spec (professional or near-pro), and it revolves around knowing which games to play and which to pass.

There will certainly be some professional specs who outperform, and they will be worth the fee. However that fee may continue to be 2&20 on the basis of value, or it may work lower for any number of reasons. Full disclosure: "someone we know" charges 1&10, as they want to keep clients forever rather than have the fee level be an issue in the future.

Oct

31

Israel, from Victor Niederhoffer

October 31, 2016 | Leave a Comment

One likes to use Israel open to close for prediction of US markets the next day over the weekend. This must be counted out. Strange to see it down 7% year to date versus our S&P up 4% year to date.

One likes to use Israel open to close for prediction of US markets the next day over the weekend. This must be counted out. Strange to see it down 7% year to date versus our S&P up 4% year to date.

Anatoly Veltman writes:

A few considerations:

1. A short term indicator - intraday trend Sunday morning as predictor of the intraday trend Sunday evening - may well be valid. One better know make-up of participation "over there". Are foreign "actively trading funds" significant participants?

The above notwithstanding, and to address the second observed anomaly

2. Longer term trends may be cyclical, and they may also be lagging. Being "surprised" with 11% discrepancy is not everything (yet). What was the delta in FX for the same period? (I'm assuming their index is in shekels). Maybe shekel also depreciated 11%, and under-performance is actually 22%…Interest rate differentials and trends are another variable. Finally, U.S. aid and geopolitical threats loom huge over any Israel forecast.

I wonder if anyone can weigh in on "Dem vs. Rep" impact on Israel's future.

Rocky Humbert writes:

Please. Two stocks, Teva Pharma and Perrigo Pharma account for 20% of the TA-100 index. Both stocks have declined massively over the past 12 months and can account for the index underperformance.

As anyone who is sentient should know, the bio, pharma, and generic drug stocks have performed horribly over the past twelve months — beginning with Valiant and Shkreli and Hilliary's tweet — and more recently on bad R&D and earnings news and speculation about the end of price-hike-led earnings growth. When I was buying the drug stocks during the last Hillary-scare, the pe multiples were 9x to 12x. The multiples today are 15x to 23x — even after the declines.

Someone should tell the "public" …

TA-100 Index: The TA-100 Index, typically referred to as the Tel Aviv 100, is a stock market index of the 100 most highly capitalised companies listed on the Tel Aviv Stock Exchange…

David Lillienfeld writes:

It seems likely to me that the generic manufacturers are going to come under a lot of pricing pressure moving forward. The ethicals? I'm not so sure. Yes, there's looking to be a potential product failure on Regeneron's cholesterol drug, likely partly because of price, but almost half of all drug development today is for orphan drugs—and I haven't seen much in the way of push back from the market with regard to them. Lots of kvetching, no changes in purchases.

One of the "wake-up calls" for the industry has been what happened with Gilead's Hep C franchise. (When Gilead bought Parmassett, from whom it got this franchise, everyone thought they grossly overpaid—not unlike Pfizer and Wyeth for Lipitor. It was the deal of the century thus far—for Gilead.) It made a lot of money—short term. There was lots of grousing about the high cost, never mind that it was curative in ways that existing treatments were not, i.e., it was cost-effective even if insurers didn't appreciate the fact immediately. What few understood was that most of that revenue—and profits—resulted from a backlog of patients, now emptied, through which Gilead had to recover its costs and pays the piper for past failed efforts. Did it overcharge beyond that? Depends whom you ask.

There were other viral diseases (Gilead's specialty) it was supposed to have turned its attentions to, as well as (finally) some performance from its oncology unit. About 6-7 weeks ago, though, I noticed that construction on the Gilead campus had slowed. Not stopped, though. I tried speaking with people that I know there, make that knew there, and heard that a couple of retired and have fallen off the grid. One was pretty disgusted and turned up at Genentech—and was unwilling to talk except to say that he was still detoxing.

Look at pharma companies like BioMarin and Ultragenyx and you might find companies with lots of pricing power. Also lots of waiting-to-be acquired power. Will they be hauled in front of a Congressional committee? Perhaps, but I doubt it. That's the nature of an orphan drug—and I don't see that changing anytime soon. The costs of development (fixed costs) are almost as high as for those intended for more common conditions. Yes, there are fewer patients, but they may also be harder to find (= expense). And there are the drug failures. Go ask Bristol-Myers Squibb about the impact of those—BMS is in the process of hacking off a good portion of its R&D department after a major failed trial/program.

Two thoughts: First, stay away from cancer immunotherapy. Yes, someone will win big there—maybe. No one has any clue as to whom/if. In 5 years, probably a different story, but at the moment, not ready for prime-time. (If you like to gamble, go to Vegas or Macau.) Think of this area as the equal of NASH. Maybe Intercept will be a big winner. I'm not so sure. One thing is clear—there's an increasing amount of roadkill on that highway.

So yes, Rocky, the generic manufacturers are challenged—and given the size of the generics marketplace and some of the price hikes that have taken place, I don't see that ending any time soon.

But the pharma space still offers opportunities, just not with the larger companies.

Oct

31

Poll Numbers, from Andy Aiken

October 31, 2016 | Leave a Comment

"I have noticed that 538 are quite incompetent (and aggressively so)– they don't grasp something basic about an election probability as an estimator of a future binary outcome. The more uncertainty, the closer the estimator to 50%. But let us 'price' it as an arbitrage-free option."

"I have noticed that 538 are quite incompetent (and aggressively so)– they don't grasp something basic about an election probability as an estimator of a future binary outcome. The more uncertainty, the closer the estimator to 50%. But let us 'price' it as an arbitrage-free option."

I think that Taleb is correct here. The point estimate of an election probability is far more unstable than the 538 model portrays. Also, on the betting markets, the uncertainty should be reflected in wide bid-ask spreads, which is not the case in these markets either.

{kind=link}

Stefan Jovanovich comments:

The poll numbers are not trades that must be cleared; they are, at best, applied social science research. There is no penalty for getting the estimate wrong; no one ever gets fired for having missed the spread. When you all lay on a single trade, there is actual money at stake - far more serious money than anything these D List celebrities on the tube ever put at risk. (Reminder: "Politics is show business for ugly people.") The stuff fascinates me because it is the random walk of actual history, but why do any of you serious punters pay attention to it as anything other than a minor sports bet - like wagering on Columbia basketball in Casino (the movie)?

For all the supposed money at stake in politics and the outcomes of political elections, the actual net expenditures - the money spent that goes outside the bubble of the campaign organization itself - are trivial. There is more money spent by GEIGO and its rivals on pitching auto liability coverage than all the net payments to television for Presidential campaign ads for both parties.

The poll numbers being reported, even this morning, are for samples taken before Friday's revelation about the Danger Man's laptop. They "changed" because the pollsters decided to use a sample that was a statistical probability rather than one that was completely bent in favor of Mrs. Clinton. ABC News had a headline that says it all "Shift in the Electorate's Makeup Tightens the Presidential Contest". Yeah, right. The makeup of the electorate over an entire campaign season does not change. If it did, the Democrats would not be so passionate about enacting same day registration and voting.

A week ago ABC News had a poll that showed Mrs. Clinton up by 12 points and at the magic number of 50. The poll with the headline had her at 47 and Trump at 45. What "changed" was the weighting of the sample. The earlier poll divided the electorate as 36% Democrat, 27% Republican and 31% Independent. The more recent one splits it 37, 29, 29.

So, Stefan, how does this prove your thesis? Easy. The folks at ABC decided that 81% of the registered Republicans are now going to vote, as opposed to only 75% a week ago. They also decided that 5% fewer registered Democrats were actually going to vote.

Who is in the electorate does not change. Who is going to be foolish enough to waste their time to actually vote is always the question.

The enduring paradox of representative government is the fact that there is no statistically valid reason for any individual to bother with voting. Your individual vote NEVER counts. It is a pure act of faith. That is the reason that the countries that are actual democracies are wise enough to make voting have a real cost; it is only in autocracies that voting is free, easy and compulsory.

As for who will win next week, I still favor the Harold Macmillan prediction. When asked by a journalist (who else?) what will determine the coming Parliamentary election, he replied: "Events, dear boy, events."

Oct

25

I Am Reading, from Victor Niederhoffer

October 25, 2016 | Leave a Comment

I am reading here Ripley's Believe It or Not: Book of Chance and find it amazingly accurate and interesting. It gives ideas for inventions that are very useful and came to be, and has a million interesting things about luck and skill, and gambling.

Oct

25

I’ll Give You a Symbolic Indicator, from Anatoly Veltman

October 25, 2016 | Leave a Comment

This weekend, the BTC/USD has traded back up to equal its precise level of July 31, 2016–the day that the most outrageous hack in crypto-currency history started to filter through to global news domain…What an unbelievable recovery, and what an unmistakable indicator that even the worst known fears of man today are not feared as much as the unknown, or the ones that may be quietly swept under the rug. Might this be one illustration of what precarious world we are living in today, and an indication of how conventional personal property is becoming deemed less and less organically "secure"?

Oct

25

The Price of Success, from anonymous

October 25, 2016 | 1 Comment

What it cost to see the cubbies play:

Standing room only ticket prices at Wrigley = 2.5K

Standing room prices at Progressive Field (really?) is 650

Cubs behind home plate = 18K each

Progressive field = 3K

Oct

24

A Symptom of What’s Wrong, from Victor Niederhoffer

October 24, 2016 | 3 Comments

A symptom of what's wrong with America, economics, and the cattle trader's economics is this sentence in Robert Gordon The Rise and Fall of American Growth. If the stock market continues to advance, we know that inequality will increase, for capital gains on equities accrue disproportionately to the top income brackets". The book predicts that "the outlook for future growth in the standard of living is not promising" because of this predicted inequality (and slowing innovation, the baby boom, increased debt, and poor education). "We face headwinds that are stronger barriers to continued growth than were faced by our ancestors a century or two ago". Yes, the barriers are economists like Gordon and policies like those of the cattle trader. A totally flawed book suffering from the English and Pickety disease that could have been great if not suffused by collectivist fallacies.

A symptom of what's wrong with America, economics, and the cattle trader's economics is this sentence in Robert Gordon The Rise and Fall of American Growth. If the stock market continues to advance, we know that inequality will increase, for capital gains on equities accrue disproportionately to the top income brackets". The book predicts that "the outlook for future growth in the standard of living is not promising" because of this predicted inequality (and slowing innovation, the baby boom, increased debt, and poor education). "We face headwinds that are stronger barriers to continued growth than were faced by our ancestors a century or two ago". Yes, the barriers are economists like Gordon and policies like those of the cattle trader. A totally flawed book suffering from the English and Pickety disease that could have been great if not suffused by collectivist fallacies.

Jim Sogi writes:

Take a look at the Nikkei chart for the last 50 years. They had decades of tremendous growth. In 1989 it peaked, and crashed. Then for the next 25 years until now, its been in a range. Their population is declining. Young Japanese people, increasingly, are not attracted to the opposite sex. When you go to Japan, you really notice a lot of 60 year olds. There is a big population bulge at that age. Those are their boomers. There are no immigrants. There is no diversity. Diversity causes innovation.

Technology has a hard time increasing productivity in the face of large demographic shifts. The cell phone brought huge increases in productivity, but there is a plateauing zombie effect going on with increasing screen addiction.

Both the above are presented in support of my theory about long term market ranges.

Alex Castaldo writes:

Sogi-san's idea about the importance of demographic trends finds some support in a recent paper by Fed economists:

The United States, like other advanced economies, is undergoing a dramatic demographic transition related to the unfolding of the post-war baby boom. As a consequence, the growth rate of the labor force has declined and should remain low for the foreseeable future. In this paper, we investigate the extent to which demographic changes, especially those related to the baby boom, can explain the currently low levels of real interest rates and GDP growth.

We build an overlapping generation (OG) model that is consistent with observed and projected changes in fertility, labor supply, life expectancy, family composition, and international migration. The model allows us to explore the extent to which demographic changes, in and of themselves, can explain the timing and magnitude of movements in real interest rates and real GDP growth during the post-war period and beyond. […].

We find that demographic factors alone can account for a 1.25 percentage-point decline in the equilibrium real interest rate in the model since 1980 - much, if not all, of the permanent decline in real interest rates over that period according to some recent time-series estimates, such as Johannsen and Mertens (2016b) and Holston et al. (2016). The model is also consistent with demographics having lowered real GDP growth 1.25 percentage points since 1980, primarily through lower growth in the labor supply; this decline is in line with changes in estimates of the trend of GDP growth over that period. Interestingly, the model also implies that these declines have been most pronounced since the early 2000s, so that downward pressures on interest rates and GDP growth due to demographics could be easily misinterpreted as persistent but ultimately temporary influences of the global financial crisis.

Larry Williams comments:

Amen! Especially now that everyone owns stocks in one form (retirement programs,etc) or another.

Like JFK said, "a rising tide lifts all ships".

John Floyd comments:

I first arrived in Japan in 1985 in the midst of the boom. Reservations were necessary well in advance to have a sit down lunch anywhere and the likes of Maiko Kawakami were more than willing to pay me $40 an hour to teach them, English. But after many years of a palpable buzz that included the Plaza Accord, expanding money supply, real estate price increases, etc. came the arrival of a new BOJ Governor Mieno in December 1989. Mieno believed the gains in asset prices was a bubble and "undermined the stability…of Japanese society by weakening the ethos of labor…" and immediately began tightening monetary policy. Equity markets began a decline and with a lag of a year or so did real estate prices.

In thinking about Japan I would consider some of the following, Further I would consider how it relates to what is happening in Europe, US, and China at the moment, to name a few.

Why has the "great hedge fund trade" that began in the mid 1990's of shorting Japanese bonds not worked?

Is there something inherent in Japanese culture that has prevented the open restructuring of debt that is more prevalent in Western societies? Why can you drop $1,000 of your English teaching money in a restaurant and have someone return it to you the next day gift wrapped?

Does an aging population save or spend more and what might that influence be on the economy and markets?

How does the rise in China debt levels over the past few years compare to both the Japanese(circa 1980 area) and US debt (circa 2000 area) expansions?

Do you believe the Japanese will stick on the path of the 3 arrows which have been partially successful? Might they expand their arsenal?

What is happening to the stock of JGB's and the ownership there of and thus the subsequent interest rates demanded?

What about this new 10 year yield target and how does it square with inflation and the Yen?

Is there a debt write off as that is the ultimate solution? General government gross debt has gone from about 50% of GDP in the late 80's to about 250% now.

What happens to the JPY, stocks, and bonds if debt is restructured given the impact on growth, inflation, etc.? I was last in Japan a few years ago and remarkably the prices had not changed much since the 1980's for hotels, noodles, beer, coffee, etc. But, alas I did not price out the demand for young English teachers.

Oct

24

The Cast of Characters, from Victor Niederhoffer

October 24, 2016 | Leave a Comment

The cast of characters that goes along with the Zacharian "your own man" and the proverbial "useful idiot" is large in our field. I see "the captain", "the pessimist" (perhaps the bearometer), "the cheat" (perhaps a bio executive from Boston), "the complainer" (perhaps Steve Jobs), "the sanctimonious scoundrel" (from Nebraska). I am seeing the boy (market) who plays "lady I did it" with a big spike overnight then a return to unchanged at the open. What other characters from the playground do you see? Do you feel this is a useful type of thinking?

The cast of characters that goes along with the Zacharian "your own man" and the proverbial "useful idiot" is large in our field. I see "the captain", "the pessimist" (perhaps the bearometer), "the cheat" (perhaps a bio executive from Boston), "the complainer" (perhaps Steve Jobs), "the sanctimonious scoundrel" (from Nebraska). I am seeing the boy (market) who plays "lady I did it" with a big spike overnight then a return to unchanged at the open. What other characters from the playground do you see? Do you feel this is a useful type of thinking?

Oct

24

The Election and the Market, from Ralph Vince

October 24, 2016 | 1 Comment

I am quite certain stocks lift off here, immediately, and the beneficiaries are those who are long before the election should she win. It's going to be very hard to step into it once it goes for most who aren't in beforehand. We're on the long road to 1% long rates and similar numbers for unemployment according to my calculations.

I am quite certain stocks lift off here, immediately, and the beneficiaries are those who are long before the election should she win. It's going to be very hard to step into it once it goes for most who aren't in beforehand. We're on the long road to 1% long rates and similar numbers for unemployment according to my calculations.

As for the election, Trump lived to fight another day when everyone reacted in seeming horror to what he said about accepting the election results. He was so pathetic at the last debate, and the spotlight shifted, to his fortune, as a result of his "horrifying(?)" statement. As Pat Buchanan, who bears the furrowed brow I recognize and expect of all those who have tortured by Jesuits, puts so poignantly in his most recent column:

"The establishment is horrified at the Donald's defiance because, deep within its soul, it fears that the people for whom Trump speaks no longer accept its political legitimacy or moral authority."

I don't think this election is a foregone conclusion or can be measured anymore than we can know what a jury's verdict will be at this point. As difficult to predict as the market may be, it is a much simpler calculus than this election.

Oct

24

Free at Last, from Stefan Jovanovich

October 24, 2016 | Leave a Comment

You all will be saved from any future lectures about Ulysses Grant next week. That is when Ron White's biography becomes available on Amazon. It is, by far, the best ever written.

You all will be saved from any future lectures about Ulysses Grant next week. That is when Ron White's biography becomes available on Amazon. It is, by far, the best ever written.

Apologies for not adding the appropriate "but". White comes closest among all the biographers to understanding who Grant was, but he still falls far short of understanding what he thought. The biography's treatment of Grant's economic ideas avoids repeating Henry Adams' lies; but it falls far short of understanding why Grant's pushing through Resumption was the key to the United States' extraordinary rise to wealth and power after for the last century and a half. That part of the story still remains to be written.

P.S. The best single modern volume on Grant, though not a full biography, is Mark Perry's book on Mark Twain and the man he admired more than any other.

Oct

24

Fighting Over Property, from Stefan Jovanovich

October 24, 2016 | Leave a Comment

On this date in 1775 the Second Continental Congress adopted, with modification, the motion that Edward Rutledge had first proposed in July. Rutledge had been appalled that the Continental Army and its predecessor the New England Army had black-skinned soldiers. (Under the Crown "blacks" had been excluded from all formally-established state militias, but the rebellious colonists in Massachusetts had accepted all comers.) Rutledge moved that all negroes be immediately discharged from the Army; the Congress, with its usual talent for Paul Ryan spreadsheet logic, decided that it would not discharge serving soldiers who were black-skinned but would not recruit any new "blacks".

The British responded immediately by publishing what became known as Dunmore's Proclamation, offering freedom to slaves who agreed to fight for the British. On November 12, 1775 General Washington had entered in the Army's Orderly Book Congress' formal instruction that negroes no longer be enlisted in the army. He then wrote to Congress to tell them what they had done: "the free negroes who have served in this army are very much dissatisfied at being discarded . . . it is to be apprehended that they may seek employ in the Ministerial [British] Army."

Simon Schama, who hates Americans almost as much as he despises Israelis, claims that as many as 100,000 slaves ran away from plantations as the result of Dunmore's Proclamation. (General query: What is it about this particular number that makes it a source of rhetorical magic? One is reminded of the first President Clinton's 100,000 cops, for example.)

The number was, according to the one scholar who has tried to do the actual counting, somewhere between 800 and 2,000. Roughly 250 of these became members of the Ethiopian Regiment. Another 300 embarked with Dunmore in 1776 when he fled Williamsburg. There is, with all of this, the usual irony. Like every man of property in the colonies, except for Quakers and the odd free-thinker, Dunmore himself was a slave owner.

People with extra melanin did continue to fight in the War for Independence. As the war dragged on, the "manpower shortage" (lovely phrase that only perfumed princes can use without gagging) forced even Virginia to accept negroes and mulattoes, when necessary.

The best summary of the full story is here.

Its author, Noel Poirier, now runs the National Watch and Clock Museum, which a wonderful antidote to all the worship of the dead at Gettysburg, if you find yourself in that part of the world.

Oct

24

Omaha, Omaha, from Stefan Jovanovich

October 24, 2016 | Leave a Comment

The greatest single demographic change of the last 20 years among people born in the United States has been the collapse in the relative rate of growth of the "black" and Asian populations. (The growth rate for Hispanics born in the United States has not changed from what it has been for the last 50 years; what catches people's attention are the numbers that come from steady compounding.)

Sometime in the 1990s the production of new "white" people who do not have Hispanic surnames and new "black" and became the same; and the birth rate for new "Asian" people fell below that of non-Hispanic whites. The nomination of Barack Obama in 2008 did a great deal to hide this fact because registration and voting - turnout - by black people surged; that higher level of participation continued in 2012, even though there was no further increase.

The best evidence for this is the shameless weighting of the current political polls. No public pollster offers racial breakdowns of their party weightings. They tell you how many Democrats and Republicans and Independents they have but not how many members of each Census racial category make up the partisan groupings. If, as the networks clearly do, you want Mrs. Clinton's numbers to be up, you can do what I explained in my piece about ESPN polling: you can overweight Democrats slightly in relation to Republicans and then dramatically underweight Independents. You can then double down by overweighting the number of black and Asian Democrats and underweighting Hispanic and non-Hispanic white ones. (Note: Asians have replaced Jews as the second most reliable Census category of Democratic voters; it is the historical gift of Earl Warren that keeps on giving.)

Those of us who still profit shamelessly from selling services to "the media" are amused by the hand-wringing over the decline in the NFL's ratings. Your most popular player retires, and his famous rival is suspended and you wonder that your ratings go DOWN? Yet, the grieving and lamentation in network TV land may also be the recognition of the fact that, in terms of present and future ratings, neither blacks nor Asians now offer the prospect of more and more eyeballs. Soccer - i.e. the "real" football - anyone?

Oct

24

Are You Concerned About a Rate Hike? My Response, from Ralph Vince

October 24, 2016 | Leave a Comment

Rate Hike?

The trend has been for lower rates since the early 80s. It is precisely the "zirp minus" world that is one of the factors (the biggest factor) that will drive things farther and longer than anyone dreams. This condition has persisted far longer than anyone ever expected, and as I;ve said before, all money must now seek risk - and that exists in equities, private and public, real estate and "wild things" (art, sports teams, etc).

The world has been soaked in cash, so much so that there is seemingly no demand for it, and the pensions hunger grows evermore desperate each year.

What is too high a PE when the alternative is a certain loss? The world has changed, profoundly, as a result of this, and I would speculate it may get even stranger. For example, to be long equities is to be short volatility, and vice versa, and that relationship too, is not as cast as the sun rising in the East. That relationship too could flip.

Adaptation is the first rule of survival. Look at the hedge fund industry.

Oct

24

One is Thinking, from Victor Niederhoffer

October 24, 2016 | 2 Comments

One is thinking of retiring and setting up a radio flyer wagon on Wall Street, and selling guidance on markets for 5 bucks a query. One has given up studying the factors that determine the bull or bear of individual stocks., especially since no studies are valid unless they use a compustat as is file and according to Andy Lo, even those are adjusted. One wonders if there is any systematic way of dividing stocks into good and bad that works these days? A related query is whether the Value Line rankings of stocks into group 1-5 have held up now that the great Sam Eisenstat has been eased out. Do you think I could be as good as Kramer?

One is thinking of retiring and setting up a radio flyer wagon on Wall Street, and selling guidance on markets for 5 bucks a query. One has given up studying the factors that determine the bull or bear of individual stocks., especially since no studies are valid unless they use a compustat as is file and according to Andy Lo, even those are adjusted. One wonders if there is any systematic way of dividing stocks into good and bad that works these days? A related query is whether the Value Line rankings of stocks into group 1-5 have held up now that the great Sam Eisenstat has been eased out. Do you think I could be as good as Kramer?

Jim Sogi writes:

Years and years ago I read Value Line regularly in the binders at the brokers office and generally followed it during the bull market. It did well. Later, I subscribed, but found that by the time I got my issue, first by mail, then electronically, that the chosen No 1 stocks already had made their move making it impossible for me to get in with any hope of profit. I always wondered how that worked.

Larry Williams writes:

We tested value line ranking is Q&A software (Thompson/Reuters) about 2006-2009 time frame and were not able to come up with much that rolled into/out of top ones or bought and held for 6 to 9 months. Maybe need a long hold time.

Oct

20

It Was a Good Evening, from John Floyd

October 20, 2016 | Leave a Comment

In a rather simplistic and limited analysis this is the first time after a debate or "election news/event" that was deemed to favor the Dems that the Mexican Peso is lower on the day.

Oct

20

I Will Keep You In Suspense, from John Floyd

October 20, 2016 | 2 Comments

On the way to the office today I was blasted by Bloomberg from so many angles and reporters about Trumps "I will keep you in suspense".

A little context to remember is that during the Republican primary debate, all of Trump's opponents solemnly raised their right arm to pledge to support the Republican nominee, whoever it might be. Trump was the lone holdout, and he took heat for it.

Then more than half of them reneged on their pledges, including Jeb! Bush and St. John Kasich.

The truth is that if any candidate seriously suspected fraud, or a miscount, or whatever, they would field an army of litigatin' lawyers, as did Al Gore. Trump's the only one honest enough to acknowledge that.

Rudolf Hauser writes:

You may recall that Nixon did not do that in 1960 despite the likelihood that the Chicago vote was rigged and that winning Illinois would have given him the presidency. He did not want to put the nation through such a crisis.

Stefan Jovanovich writes:

It is a nice story, which Nixon did his best to promote; but the numbers do not support RH's assertion. Nixon only got 219 votes; adding Illinois and its 27 would have left him 24 short. Subtracting those votes from Kennedy's total of 303 would have left him with 276, 6 more than he needed. What few people mention about the election is that it was the last time a 3rd candidate won electoral votes. Harry Byrd won 15.

Oct

20

Who Are the Most Resonant Useful Idiots, from Victor Niederhoffer

October 20, 2016 | 2 Comments

Who are the most resonant useful idiots in our day that can always be counted on to say something idiotic? I find it useful to look at El Erian and Gross, as both are never bullish on stocks.

Steve Ellison writes:

Anything on zerohedge

Oct

20

Fairness, from anonymous

October 20, 2016 | 1 Comment

My daughter Eddy used to be interested in the question of Fairness. Not any more. "Since it is not a question of whether but only one of where and when, why bother?"

My daughter Eddy used to be interested in the question of Fairness. Not any more. "Since it is not a question of whether but only one of where and when, why bother?"

But we do still talk about it with regard to taxes. We still laugh over her reaction to her first paycheck (issued for cleaning the animal cages at the local vet's office on the graveyard shift). "Who is this bitch FICA and why is she getting my money?"

The best that the two of us have come up with for a "fair" tax system is our own variation of the Major League Baseball "luxury tax" and revenue sharing model. Under the collective bargaining agreement that expires this year, each team in MLB puts roughly 1/3rd of its own revenues into a pool. The money in the pool is then divided up and distributed equally to each team. In 2016 the richest teams (those in the 15 largest markets) no longer received their share as a payout but instead received a credit against their revenue share to be paid the following year. (This was, IMHO, an artful way of assuring that the rich teams would agree to have revenue sharing as part of the next CBA.)

The Eddy and I conclude that FDR's unerring political instincts were wise policy. (When his Marxist academic advisers wanted Social Security to be means-tested, he told them to get real. The American people would only support a program that had a fundamental equality; if you paid into the system, you got something out of it.) We would like to see all government benefits to have the same recognition of the Constitution and its equal protection clause; if a benefit is paid to someone simply for breathing, then everyone gets it. If the government collects taxes, then everyone pays the same rate.

Eddy's final word: "Never going to happen, Dad. Too simple and too fair."

Alston Mabry writes:

This reminds me to recommend an excellent recent EconTalk:

How are those in favor of bigger government and those who want smaller government like a couple stuck in a bad marriage? Economist John Cochraneof Stanford University's Hoover Institution talks with EconTalk host Russ Roberts about how to take a different approach to the standard policy arguments. Cochrane wants to get away from the stale big government/small government arguments which he likens to a couple who have gotten stuck in a rut making the same ineffective arguments over and over. Cochrane argues for a fresh approach to economic policy including applications to growth, taxes and financial regulation.

Oct

19

We Are Listening, from Victor Niederhoffer

October 19, 2016 | 1 Comment

We are listening to Rigoletto here, and it occurs that the theme of 90% of the operas before 1870 are with Trump like rich men taking advantage of poor beautiful women before receiving their retribution. Would that be correct?

We are listening to Rigoletto here, and it occurs that the theme of 90% of the operas before 1870 are with Trump like rich men taking advantage of poor beautiful women before receiving their retribution. Would that be correct?

Stefanie Harvey replies:

This is also a war rallying theme. I just finished SPQR: A History of Ancient Rome by Mary Beard. Many a campaign began after a rape or attempted rape of an elite or community of women.

Short book review: a bit of slog due to excessive detail but wonderful humor and a light tone in writing.

Oct

19

Writing it Down, from Stefan Jovanovich

October 19, 2016 | Leave a Comment

Many full moons ago Mr. Bollinger asked me if I could find the source for the remark about Joplin that I quoted. I don't remember what I wrote then, but the gist of it was that Joplin was the only one of the ragtime players who had the guts to write down what he had improvised the night before on the piano. I still have not found the source of the remark; but I have no doubt that it was true.

Many full moons ago Mr. Bollinger asked me if I could find the source for the remark about Joplin that I quoted. I don't remember what I wrote then, but the gist of it was that Joplin was the only one of the ragtime players who had the guts to write down what he had improvised the night before on the piano. I still have not found the source of the remark; but I have no doubt that it was true.

I also have no doubt that we are not going to be seeing Bollinger and Joplin's kind of candor about methods of thinking - where "public opinion" is concerned. The current response rate for telephone polling is - allegedly - 9%. That is the number the Pew people disclosed about their own polling in 2012; and it is now taken as current gospel. In 1997 when the Pew people also disclosed their response rate, the number was 37%. It is likely that the actual response rate now is roughly 1 in 20; but that is a mere guess. The actual polling may be even less.

But, have no fear, the Pew people assure us that their numbers are still good because the results track with the data acquired by the government in its census and other surveys, where the response rate is unquestionably high enough to be accurate. "Pew Research Center devotes considerable effort to ensuring that our surveys are representative of the general population. For individual surveys, this involves making numerous callbacks over several days in order to maximize the chances of reaching respondents and making sure that an appropriate share of our sample are interviewed on cellphones. We carefully weight our surveys to match the general population demographically."

Thurston Trowel III replies:

What is your point on low response rate?

A low response rate merely means the polling outfit has to make more phone calls to get the requisite representative sample.

It does not reflect negatively on the scientific accuracy of a poll in any way, if this is what you were suggesting. No idea if that is the case but it seemed to be where you were going and apologies if wrong.

As to Joplin writing down improvised ideas, musicians everywhere for decades have recorded sketches as part of the creative process of developing ideas. I do this all the time. Whether one does so on paper, magnetic tape, hard drive or cell phone is largely irrelevant, and a matter of personal preference and convenience.

Stefan Jovanovich retorts:

Dear Third Shovel: Joplin had the courage to share his method at a time when the people playing ragtime were selling it as magic. They were not sharing the tricks of their trade. Mr. Bollinger remains exceptional in much the same way. The solution you offer– the polling people just have to make more calls - sounds logical until you ask the question the broker posed to his client. Who are the new people going to be? The reliability of opinion polling has been founded on the assumption that the sample will be homogeneously responsive, that the response rates will not vary no matter what the respondents answers are. But that is no longer the case. Making greater effort becomes a statistical frontal assault; the added costs gain no ground. Then there is the further issue of outright bias. How do you know what the proper weighting should be if you choose to ignore the only data that you have– the results of the most recent elections before this one?

Oct

19

The Life Cycles of Correlations, from Gary Phillips

October 19, 2016 | Leave a Comment

Like any relationship, correlations have life cycles which can vary over time; increasing, decreasing, or even disappearing, depending on the steady or changing market environment. There was a time when there was a positive relationship between yield movements and stock returns, especially when the 10 year treasury yield was below 5%. Rising rates were historically associated with rising stock prices; but when the 10 year yield was above 5% a negative relationship between yield movements and stock returns existed. Since '09 the S&P rallied from 666 to near 2200 while 10 year rates fell from ~4% down to ~1.3 due to central bank monetary policies. However, the Fed's actions may result in changing the correlation between treasuries and equities once again, ushering in a secular regime change where rates are rising and are positively correlated with rising equity returns.

Like any relationship, correlations have life cycles which can vary over time; increasing, decreasing, or even disappearing, depending on the steady or changing market environment. There was a time when there was a positive relationship between yield movements and stock returns, especially when the 10 year treasury yield was below 5%. Rising rates were historically associated with rising stock prices; but when the 10 year yield was above 5% a negative relationship between yield movements and stock returns existed. Since '09 the S&P rallied from 666 to near 2200 while 10 year rates fell from ~4% down to ~1.3 due to central bank monetary policies. However, the Fed's actions may result in changing the correlation between treasuries and equities once again, ushering in a secular regime change where rates are rising and are positively correlated with rising equity returns.

Oct

19

Book Recommendation, from Bo Keely

October 19, 2016 | Leave a Comment

This is a fascinating book of 1848 by an exacting character who writes like Galton: "Eight Years' Wanderings in Ceylon" by Sir Samuel White Baker

This is a fascinating book of 1848 by an exacting character who writes like Galton: "Eight Years' Wanderings in Ceylon" by Sir Samuel White Baker

.

.

Oct

19

The Cistern, from Bo Keely

October 19, 2016 | 1 Comment

The cistern crouched beneath the creaking windmill in a slight breeze. It was a hot day out from Slab City, CA. An ancient lock prevented my refreshment.

The cistern crouched beneath the creaking windmill in a slight breeze. It was a hot day out from Slab City, CA. An ancient lock prevented my refreshment.

An old desert lock is a cue to look for a 'dummy' latch because who keeps the key so long? The strap hinge on the cistern cover was bolted such that its nuts hand screwed loose!

The concrete cistern itself measured 10'x10' and who knows how deep it falls into the ground?

I lifted the 100-pound steel cover on its rusty hinge with a full body effort and peered down… The inside was a dripping cement cell, measuring 10'x10' and 6' deep with two feet of water at the bottom.

A pink stick – no, a 4.5' racer snake! had crawled in a crack of the cistern top and rested with its head on a protruding inch of rebar, while the rest of its slender body dangled underwater. The lifeless eyes were enlarged blue marbles like a Halloween mask. The thirsty serpent could have been there for weeks, as even October is a thirsty month.

I dropped a pebble and it sprang to life, swimming the perimeter of the cell again and again.

How to get it out, so I could go in for a drink and dunk? I talked to the snake bouncing my voice off the water for a few minutes, and as it calmed, reached and lowered a branch under its head and gently lifted it out onto the concrete top. Snakes don't have eyelids to blink; this one stared for a few seconds, and then slithered across the concrete top onto an overhanging limb, stretched out and air dried.

I jumped into the cement tank and splashed like a gleeful kid, and drank heartily.

In a few minutes, it was time to go and I peered up at the head high opening. Uh oh. I reached up but couldn't drag myself out the tank. So, I sat back down in the water and looked up through the 3' square at the snake on the branch.

We had traded positions. I yelled but received only echoes.

The significant thing at the moment that distinguished me from the snake was my shorts. I removed and stuffed them into a 3" opening in a side wall for a drain pipe that went off underground, and limited the water's rise.

In twenty minutes the water level climbed a half-inch. I could float to the ceiling in 32 hours, as long as the breeze kept up.

The water dripped from the hard-wearing windmill above into the cistern top.

The snake slithered off, and I was alone for the longest time. As the water rose, my eyes adapted to the dim and I spotted the rebar that had been the snake's hard pillow for so many days. I stood, and stuck one boot on it, and with the ceiling opening near its side wall, could boost myself up and out the watery crypt.

But the first step was to string an 8' length of abandoned hose in one corner of the cistern up from the water to the crack in the top that the snake had entered, and out into the sunlight.

Then with a big effort I leaped out.

Now I sip the memories of my escape from the cistern.

Oct

18

The Best One Wall Handball Player, from Vic Niederhoffer

October 18, 2016 | Leave a Comment

The best one-wall handball player in the world in 1940 was Joe Garber. He was drafted an Ace, and got killed flying in a Boeing B-17G over Munich on 21/7/1944. The Brighton Beach Baths, now Russian condos, built a handball stadium holding 500 in his honor. Artie Niederhoffer, my father, and I watched the handball sweeps every weekend from a perch in fourth tier. To add to excitement, Artie always sat next to Bookie, and they played a game of checkers as they watched the handball, often the notorious Uncle Howie teamed up with Hershkowitz against the runner Moey Orenstein and Mortie Alexander, who could kill the ball from 20 feet behind the long line. Bookie took bets on all the games, at 11-10. Pick em on Moey. Or Eisenberg, +3 against the Milkman. (That game was rained out, but that's another story.) It was hot in the concrete stadium and if the score got to 18-11 or some such in a game Bookie would pay out all the bets on the winning teams so that the winners could get a swim in the adjacent public ocean. Shades of Paddy Power paying out all the bets on the Cattle Trader.

Stefan Jovanovich comments:

Political bets are not really like athletic contests since there is no running tally. The polls issued throughout the election campaigns used to be a kind of pseudo-line score so you could use some of the techniques that the Brighton Beach bookies used for in-game sport betting. But that is now gone, like the Baths. The public polls are now so thoroughly corrupted (statistically, not morally) that you cannot think you are watching a game progress. Even if Vic had not decided that state polls' collective predictions for the Electoral College were an inappropriate intrusion of politics, I would have abandoned the daily score-keeping. The collapse in sampling that has occurred this year makes the fall-off in TV ratings for the NFL seem moderate by comparison; and there has been a quantum increase in the distortions in pollster's models. Those distortions are partly the result of the sampling problem but they are also from political bias. The models' partisan break-downs are completely inconsistent with anything seen in the actual elections last year and in 2014. The only information out there that is statistically valid are the longitudinal polls like the LA Times/USC poll - where the same people are repeatedly polled. Those continue to show a score that is 13-11, not 18-11. Nate Silver made the smart move over to ESPN just in time.

Oct

17

The Election and the Market, from Ralph Vince

October 17, 2016 | 2 Comments

Regardless of who wins this election, this market is going to rip to the upside — and I can be quite certain of that without even looking at the numbers, just the very tentative nature of nearly everyone around it. I've smelled this dish cooking before, and so have a lot of folks on this site. I don't know who is going to win this, but I do know that a 500 bln stop (not even flip) in the hemorrhage of balance of payments translates into an instant 3% GDP growth, and the multiplier effect on that puts us at 1965 growth, or even Truman-era growth. I was fortunate, in the 1980s and latter half of the 90s, anyone who showed up on time with their shoes on did pretty well. I had some lucky breaks too, which didn't hurt (and, as I have said repeatedly, and bears repetition for no one's sake other than my own perspective — "Anything that I may have has been given to me.").

Regardless of who wins this election, this market is going to rip to the upside — and I can be quite certain of that without even looking at the numbers, just the very tentative nature of nearly everyone around it. I've smelled this dish cooking before, and so have a lot of folks on this site. I don't know who is going to win this, but I do know that a 500 bln stop (not even flip) in the hemorrhage of balance of payments translates into an instant 3% GDP growth, and the multiplier effect on that puts us at 1965 growth, or even Truman-era growth. I was fortunate, in the 1980s and latter half of the 90s, anyone who showed up on time with their shoes on did pretty well. I had some lucky breaks too, which didn't hurt (and, as I have said repeatedly, and bears repetition for no one's sake other than my own perspective — "Anything that I may have has been given to me.").

But nothing has gone anywhere since the Spring of 2001. It would be wonderful to see growth in double digits, or just robust, 80s-90s style for the morass of all these millennials. People teasingly refer to them as "Snowflakes," but I have proactively and of my own volition gone out of my way in the past since 2007 to get into their heads, to work alongside them — not your typical snowflakes but snowflakes of all varieties. For all the negatives said about these kids (which I do not disagree with!), they are a much harder working, industrious, adaptable and far more pleasant gang than we boomers were. And for exactly them, I hope they get a break here and get the the change they deserve, and the economic growth they can use.

Stefan Martinek writes:

Ralph,

The whole 2014, maybe the first part of 2015, you mentioned multiple times the issue of liquidity, the risk of a huge crash, structural liquidity problems, ETFs, etc. Do you consider all that is over? I always thought that the trend in equities (from 2009) will take some time to reverse, that there will be some chopping on the top before the next up move. I never tested this, but the chopping for another 1-2 years would look proportional, beautiful, expected… Of course growth will resume at some point. I thought that maybe market needs to take back some easy money generated in the last decade before going forward.

Jack Tierney, the President of the Old Speculator's Club writes in:

A few observations on this thread.

First, perhaps because of its nature, Dailyspec tends to look for the cause of many social phenomena in financial terms. In our discussions, Mr. Haave suggested "that while the Southern states get more benefits those benefits go predominantly to the minority that votes democratic." Mr. Aiken's thoughts illustrate exactly why: "NY and IL are 'red states' outside of NYC and Chicago, respectively…" I can't speak for NY, but "ethnic demographics" are the key driver Big D majorities in IL…I have no idea how to quantify, or define, the effect of "cultural indices."

Mr. Hauser added a vital insight in suggesting that "many elderly move South in their retirement years" and, by extension, while their benefits add to the states' totals, it does not necessarily translate into democrat votes. I am one of those "expats" and can say with some certainty that we have had a marginal impact.

But several very important issues are either overlooked or avoided to explain why these states remain in the red column. First, and most important, many in the current (and, more than likely, continual regime) have quite boldly and heavy handedly attacked the religious foundations of many individuals in these states…certainly enough to swing the vote.

Second, gun control is no minor issue. Its rare to find a resident in my part of the state who doesn't own both a shotgun and a deer rifle…their purposes, though, are concentrated on bringing down consumable game and/or eliminating non-human varmints. Though many own pistols, their numbers are dwarfed by the many in our larger cities who use them for quite different purposes.

Third is education or, more specifically, the make-up of the curriculum and the content of the mandated text books. Many of today's parents and grandparents are now, after a significant amount of published and broadcast news, aware that they have received a less than adequate education. When school prayer was outlawed they were upset, but, over time, grudgingly came to accept it. However, when the study of Islam was made part of required courses, things became (and remain) a point of relentless debate.

Other points of contention which aren't appreciated outside the immediate area, but which lead many to the red side of the spectrum are the "elite" dictates discouraging, eliminating, or outlawing the Confederate flag, tobacco farming, soft drinks, fried food, salt, and "dipping."

Individually, these may seem to be trivial matters and, in many cases, "settled issues." Big mistake. Taken together, these represent stark examples of big government going well beyond its mandate. It took the Tea Party to underscore this and galvanize the voters…not just here but in other states as well. The current Democrat platform offers them nothing of substance and can do nothing to alter this situation.

Will things change? Sure they will. Despite a growing number of home schoolers and charters, an overwhelming majority of young students remain classroom captives in a system that has essentially replaced much that shaped western civ with new age agitprop.

But there will always be a remnant and as surely as all grand socialist experiments fail, this, too, shall pass.

Andy Aiken responds:

It's tricky to quantify in toto, but consider a simple variable: married vs. unmarried. There is a stark difference in party ID and voting behavior between the two subgroups, all else being equal.

Oct

17

The Quantum Theory of Markets, from Jim Sogi

October 17, 2016 | 1 Comment

The market has been in range mode for quite a while, then one day it breaks out/down into a new range where, in this theory, it will stay for a while. Sub atomic particles have a probability that the particle will be in a certain energy sphere, but not its specific location. In the market, there would be a probability that the price will be in a certain range, but one might not know the exact price. At some point due to energy input of some sort, the particle or price jumps to a different level. The ranges seem to have some regularity as do the jumps.

The market has been in range mode for quite a while, then one day it breaks out/down into a new range where, in this theory, it will stay for a while. Sub atomic particles have a probability that the particle will be in a certain energy sphere, but not its specific location. In the market, there would be a probability that the price will be in a certain range, but one might not know the exact price. At some point due to energy input of some sort, the particle or price jumps to a different level. The ranges seem to have some regularity as do the jumps.

Peter Grieve writes:

Very nice– the quantum theory of markets. Particles can also "tunnel" out of boxes which they shouldn't be able to leave under classical theories, and get into other boxes. There may be a market analogy here also.

I took a class from Feynman in my undergradute days (about a million years ago) and he was a powerhouse. He had tremendous intellectual integrity, and was a strong advocate of intellectual discipline. He said something like "the person you least want to fool is yourself, and you are the easiest one for you to fool".

Oct

17

Never Mind the Polls, from Stefan Jovanovich

October 17, 2016 | 2 Comments

In every election since 1984 and in 19 of the 22 elections since the Composite Index was introduced in 1923, the S&P 500 Index has been the most reliable gauge of Presidential election results. If the Index on election day is higher than it was three months earlier, the incumbent party retains the White House. 2181 is the magic number; that was the close on August 8th. Back to life not lived through "the news"….

In every election since 1984 and in 19 of the 22 elections since the Composite Index was introduced in 1923, the S&P 500 Index has been the most reliable gauge of Presidential election results. If the Index on election day is higher than it was three months earlier, the incumbent party retains the White House. 2181 is the magic number; that was the close on August 8th. Back to life not lived through "the news"….

Andy Aiken writes:

I am also low-news/high-information. I seek out primary sources, e.g. read the academic paper or CBO study instead of a journalism student's usually flawed interpretation of it. As Nietzsche said, "All things are subject to interpretation. Whichever interpretation prevails at a given time is a function of power and not truth." The major media in the US have been speaking power to truth for a long time.

Oct

17

Thoughts, from Natural Philosopher

October 17, 2016 | Leave a Comment

The S&P 500 has been in backwardation continuously since October 17, 2008 as the dividend yield on the S&P 500 has exceeded the risk-free interest rate. Prior to that date, the S&P 500 was always in contango except for a few days in March 2008. I think the backwardation is bullish; Philip Carret said in 1931 in The Art of Speculation that "borrowed money is the lifeblood of speculation", and it is very bullish when "stocks carry themselves."

Oct

15

All These Possibillities, from Victor Niederhoffer

October 15, 2016 | Leave a Comment

All these possibilities are quite analogous to those who like to fight the drift in the market. There are so many things that could go wrong. There are so many factors that people don't consider that could cause a big drop. Just in the last 4 days, there was the w.f. wagon, the Chinese trade, the alcoa signal, the Hillary speech. Every day there's some unaccounted for worry. My goodness, that's what the market takes into account, why it is where it is, where people put their money on it, and equilibrate taking into account all the positive and negative factors. That's how it is with the predictive markets. They take account of the turnouts, the prevalence of preference, the changes in votes as the election nears, the states, the coming news, the efforts to bring out the vote. If it gets too far out of line, money comes in to move it to the right direction. It's just like the market, and the reason that the best estimate of the market for the next period is always the drift.

Oct

12

Sell on Rosh Hashanah and Buy Back on Yom Kippur, from Jeff Hirsch

October 12, 2016 | Leave a Comment

I tested the old Jewish trader axiom "Sell on Rosh Hashanah and buy back on Yom Kippur?".

I tested the old Jewish trader axiom "Sell on Rosh Hashanah and buy back on Yom Kippur?".

Andy Aiken writes:

Historically, returns between the two holidays are negative, but not often enough so to be a reliable calendar trade. Average returns are distorted by 2008.

Year SPX change (%)

2000 -2.40%

2001 -1.94%

2002 -0.32%

2003 3.76%

2004 -0.92%

2005 -4.06%

2006 1.26%

2007 3.68%

2008 -17.76%

2009 -0.50%

2010 2.43%

2011 0.38%

2012 -2.21%

2013 1.77%

2014 -2.03%

2015 0.31%

% negative 56.3%

average return -1.16%

median return -0.41%

A 2004 paper suggests that the negative returns during this period may be due to lower-than-usual volume.

Oct

12

In Our Opinion, A Wind Shift, from Bill Rafter

October 12, 2016 | Leave a Comment

One of the off-the-radar things we watch is the length of time various subsets of options are held. The flip side of that is the turnover rate of those options. Several years ago I put out a white paper on the concept, and about a year ago there was a small WSJ piece. There is evidence; it's not anecdotal.

The general gist is that those who are more conscious of attuning their options positions (i.e. greater turnover) tend to be correct. Conversely, those who are complacent tend to pay for their complacency. Whoever is longest in a position tends to be "wrongest". As of this evening it is the holders of call equity options who are the more complacent.

One beautiful thing about this indicator is that it appears to measure portfolio shifts rather than mere trading shifts. That is, there isn't much fluttering back and forth.

Disclosure: we have been out of our longs for about 2 months (on the strength of other indicators) and we don't ever short equities.

Oct

12

Ghostly Phytoremediators, from Pitt T. Maner III

October 12, 2016 | Leave a Comment

As Cleese would say, "now for something completely different." And just in time for Halloween. Well certain species of trees and plants have already been used to clean up former landfills and contaminated soil areas but it would be very neat if a way were found to further modify them genetically to make them even more efficient at extracting contaminants ("enhanced phytoremediation"). Time is money and reduced cleanup times for impacted properties can save significant amounts of money!

As Cleese would say, "now for something completely different." And just in time for Halloween. Well certain species of trees and plants have already been used to clean up former landfills and contaminated soil areas but it would be very neat if a way were found to further modify them genetically to make them even more efficient at extracting contaminants ("enhanced phytoremediation"). Time is money and reduced cleanup times for impacted properties can save significant amounts of money!

'Mystery of 'ghost trees' unlocked?:

'Now a San Jose researcher is showing that these "ghosts of the forest" may be more than a biological novelty, perhaps solving a generations-old question. Zane Moore, a doctoral student at UC Davis, analyzed the needles of albino redwood leaves in a lab and found that they contain high levels of the toxic heavy metals nickel, copper and cadmium.

The phantom-like plants, which rarely grow more than 10 feet tall, appear to be drawing away and storing pollution, some of it occurring naturally in the soils — particularly shale soils — and some left from railroads, highways and other man-made sources that otherwise could degrade or kill redwoods.

Oct

12

Homecoming, from Bo Keely

October 12, 2016 | 1 Comment

The thrill of coming home has never changed.

The thrill of coming home has never changed.

Homecoming is an annual tradition in the United States. People, towns, and particularly high schools come together, usually in early October, to welcome back alumni and former residents. It is built around a central event, such as a banquet, parade, and, most often, a game of football.

The field lights drew me from deep in the desert where I'd been hiking all day. I stared long and hard and was taken back to my last visit seven years ago at the Blythe, CA high school homecoming. I was a newly fired sub-teacher at the high school – the most treasured by the students and teachers echoed their evaluations – after dismissal for trying to stop a playground war. In California a teacher is expected to stand back and let kids clobber each other.

Why not? I drove toward the field lights. I was curious to discover how the rules of engagement had changed.

The last time, in about 2009, I had sat on the opposing side bleachers to avoid the embarrassment of the kids standing and cheering when I entered the barbed wire perimeter, way out by the cotton and cow pastures, onto the sidelines. It was 90 degrees at 7pm at the kickoff, and the opposing team bench warmers sat after the pledge of allegiance as the kicker teed up the ball. A hissing and chugging behind me drew my attention from the field, as the city insect fogging machine bumped along directly behind the rival team bleacher and fogged them with insecticide. Tackles and guards puked, a cheerleader fell to the ground in convulsions, and hot, dead bugs rained on the visiting families' hair like Briylcream.

By the time the visiting team recovered from the exterminator, they were down 13-0 and never recovered. The Blythe Yellow Jackets won the homecoming.

But now, seven years later, a new stadium had been built with a perimeter chain link fence that prevented the fogging truck from entering. Brawley high school, my new home, was the visiting team. Clear headed, the Wild Cats took the ball to the goal posts every time in the first quarter, holding the Yellow Jackets to zero yardage as the first quarter gun shot. Final score, as Brawley started substituting everyone but the water boy from the bench: Brawley 35 – Blythe 0.

Blythe had lost its cheating edge.

The student body had changed dramatically since I taught in every room on campus for almost ten years. They were overweight, listless, and lacked the usual spark in desert kids' eyes. They were soulless fans.

It was good to leave for my new home.

Oct

11

Trading on the Brain, from Orson Terrill

October 11, 2016 | 1 Comment

It's somewhat relieving to know that one is not an automaton, a psychopath, or possessing low expectations because one is mostly indifferent when trading.