Jan

29

Seeing The Data, from JT

January 29, 2016 | Leave a Comment

"Future Grains"

"Future Grains"This is seeing the data before the actual data is announced. The rice example leads me to think that the same can be done with corn, wheat, cotton, coffee, poppy, coffee, and any other crop that has color change that is visible from satellite imagery.

It definitely gives a leg up for this to those that get to see the commodity of choice they trade or hedge.

Is it really for the common good of the world or is it to be a tool for a heroic trader?

Jeff Watson writes:

I've been using satellite data since the 80s.

Jan

29

Negative Interest Rates and BOJ, from JT

January 29, 2016 | Leave a Comment

"Japan adopts negative interest rate in surprise move"

Didn't they do this in the 80s as well? Was this on the Commercial and Industrial (C&I) loans in the 80s?

John Floyd writes:

10 year government yields tell you the story [quote]. Factor in the deflation, lack of growth, and JPY move [link]. More recently look at the shifts in the Balance of Payments in large part driven by oil and nuclear issues [link]. But the core of the question is best summarized by asking what are the likely policy actions going to be and how might markets react given where the macro story is likely to move to. For example, consider the sovereign debt levels [link], demographics trends and their influence on consumption, etc., where is future inflation likely to be, and then factor in Japanese stoicism [link].

Jan

29

Book Review: Being Mortal, from Jim Sogi

January 29, 2016 | 1 Comment

Being Mortal by Atul Gawande thoughtfully looks at the process of aging and dying in America. Before modern science, normally people died suddenly at home. Now doctors propose more and more expensive and invasive and often uncomfortable treatments. Hospice provides palliative care to increase the quality of the last days of life, and ironically extends life compared to invasive procedures and aggressive treatment. Doctors, now unable to address this need, need to be able to have this discussion with their patients and receive training in end of life decisions regarding palliative care.

Being Mortal by Atul Gawande thoughtfully looks at the process of aging and dying in America. Before modern science, normally people died suddenly at home. Now doctors propose more and more expensive and invasive and often uncomfortable treatments. Hospice provides palliative care to increase the quality of the last days of life, and ironically extends life compared to invasive procedures and aggressive treatment. Doctors, now unable to address this need, need to be able to have this discussion with their patients and receive training in end of life decisions regarding palliative care.

Aging and diminished capacity requires additional care, but the aged person wants his independence. Assisted care home are evolving to meet these needs.

I highly recommend this book for many who have aging relatives and are dealing with these issues.

Jan

28

Question for the Chair, from Jim Sogi

January 28, 2016 | Leave a Comment

After some practice, a kid can throw a ball and compute the trajectory on the fly. It becomes internalized. Mathematically it is a complicated computation. Normally people don't think statistically unless say after 45 years of doing it it is internalized.

After some practice, a kid can throw a ball and compute the trajectory on the fly. It becomes internalized. Mathematically it is a complicated computation. Normally people don't think statistically unless say after 45 years of doing it it is internalized.

My question to Chair and others is whether after trading for many years using statistically based evidence you have internalized the data and math such that a trade is similar to throwing a ball. Computations of course help reject ideas, or deflate misconception, or identify newly arising cycles but what percent is intuition? Even system traders identify new systems by eyeballing data or plots or using analogies.

Stefan Jovanovich writes:

If we are talking baseball, the throwing equations have their own internal derivatives. To throw a ball well enough to play the game at even a semi-professional level as a pitcher requires a great deal more than "some practice"; for the people who make it all the way to "the show" the internal computations get down to the questions of how much pressure you place on the joint of each toe. The calculations about how you hold the ball for each pitch are maddeningly complex; then there is what you do with your biceps, elbows, trunk, etc.

I suspect surfers have the same kind of subtlety in their thinking about what they do. But, I don't know: can't pitch, wouldn't dream of surfing. What I do know as a catcher is that pitcher's internalization process is never finished; they are flakes because they have to be.

anonymous writes:

When surfing at the home break, most of the good locals have it pretty well wired. Knowledge of the bottom, how the surf breaks on different tides, swell direction, currents, winds, and where the wave will peak allows a local to successfully get waves. When traveling for waves, new breaks tend to present a host of different challenges. While I will never have another place wired like my local break, when visiting a different one, I'll catch a few waves, but the locals will catch many more. I find injuries are more common at other breaks, mainly because of the lack of knowledge of the wave and the lineup. An outsider never knows all of the quirks, inside rules, players, and forces at a beach.

Seems like a good time to present a market analogy. A competent local surfer generally gets more waves than a competent outsider, just like an insider or specialist in a single market generally has more opportunities than outsiders for good trades. The insider/specialist knows his market just like the surfer knows his home break.

Jeff Watson writes:

Surfing is a good example of an intuitive process internalizing complex multiple variables. At my big wave spot I know the secret line up markers: a grass spot on the mountain, the tops of certain palm trees, a rock, some foam. It puts me in a 6 foot square in the ocean. I can see the waves in the distance, sit in a certain spot, and the wave come right to me. Someone 6 feet to the right is in the wrong spot. Newbies often get slaughtered. For example, there was a big crowd out two days ago with medium size waves when a HUGE set came thru and washed almost everyone out who were sitting on the inside.

On the rare occasion that I hit it right, I enter a trade at a good spot and ride it on most of the full move. You can feel the variables, the amount the market has fallen, its speed of trading and movement, the way its trading. The price location in relation to the last week, the last few days, the last few hours give info. When to go out and not watch. Seems like there is a lot of info being processed internally, somewhat unconsciously that has valuable input. Ideally one could quantify all these and have a computer do it with AI better than a human. The multiple variables make it hard to quantify though. I suppose some simple rules apply: after multiple 2% drops is a good time to buy or after a 50 point down move in a day on the third or fourth down day, after fake bad news, on on some stupid announcement like FOMC and the market dives 50 points for no reason. I'm sure there are more rules of thumb that one always keeps in the back of your mind, including all of Chair's caveats, and all Wiswell's proverbs. Maybe that's the point, over time one internalized all the rules, the basic setups, the data, even more complex set ups, without having to count on the fingers as its happening.

Jan

28

Of Course Compulsory Education Works– Look at the Budgets, from Stefan Jovanovich

January 28, 2016 | Leave a Comment

Since 1955 the national student-teacher ratio has gone from 27 to 16. Per pupil expenditures, after adjustment for inflation, have increased by more than 400%. The United States now has the highest per pupil expenditures in the world.

And the winner is… The Program for International Student Assessment has published its rankings for academic achievements by 15-year-old students, in 34 OECD countries, using the most recent data (Calendar year 2012).

In mathematics U.S. students ranked 27th; in reading, 17th; in science, 20th.

Clearly, "we" - i.e. those of us who have already escaped the schoolies–need to spend more money so they can continue to torture the young.

Jan

27

Snow Day Last Weekend, from Jeff Watson

January 27, 2016 | Leave a Comment

Many have seen the brilliant, viral video from Casey Neistadt snowboarding in Manhattan on Saturday. Casey did a brilliant job and millions have seen his artful video which already has 100 million hits on Youtube. I love Casey and my entire family appreciates his work, but at the exact same time he was filming during the blizzard, a couple of surfers in Montauk were hitting it hard with 10' waves, and this would have to be labeled as one of the best surf sessions of all time. Casey did a bang up job with his video, and having Sinatra's song as the background was nice, but this surfing video, with Pearl Jam in the background captures the zeitgeist of hard core, northern, surfing. For what it's worth, both videos are great.

Many have seen the brilliant, viral video from Casey Neistadt snowboarding in Manhattan on Saturday. Casey did a brilliant job and millions have seen his artful video which already has 100 million hits on Youtube. I love Casey and my entire family appreciates his work, but at the exact same time he was filming during the blizzard, a couple of surfers in Montauk were hitting it hard with 10' waves, and this would have to be labeled as one of the best surf sessions of all time. Casey did a bang up job with his video, and having Sinatra's song as the background was nice, but this surfing video, with Pearl Jam in the background captures the zeitgeist of hard core, northern, surfing. For what it's worth, both videos are great.

Jan

26

A Different Take on “Buy and Hold”, from Alston Mabry

January 26, 2016 | Leave a Comment

Many/most analyses of buy & hold use a model where a set amount is invested in the market at a specific time and then tracked over X years, which doesn't seem very realistic and certainly isn't the only viable model. So here is a different model:

The results below are for the following: Invest $1000 every month in the S&P 500 and collect the dividends at the end of each year [1]. For each year, calculate the total value of shares and dividends for the 5 years ending with that year, e.g., 1960-1964. Also calculate the 5-year total's % over/under the $60,000 investment during the 5 years. Negative years highlighted, and mean and sd shown at the end.

Version 2, corrected for overstating dividend, which adds 2009 as a

negative (slightly) year:

date 5yr Total % over investment

Dec-15 $80,943 +34.9%

Dec-14 $91,399 +52.3%

Dec-13 $94,956 +58.3%

Dec-12 $77,990 +30.0%

Dec-11 $68,060 +13.4%

Dec-10 $67,534 +12.6%

—Dec-09 $59,566 -0.7%

—Dec-08 $47,067 -21.6%

Dec-07 $77,666 +29.4%

Dec-06 $80,894 +34.8%

Dec-05 $72,530 +20.9%

Dec-04 $68,208 +13.7%

Dec-03 $60,778 +1.3%

—Dec-02 $47,322 -21.1%

Dec-01 $63,044 +5.1%

Dec-00 $82,804 +38.0%

Dec-99 $112,527 +87.5%

Dec-98 $116,433 +94.1%

Dec-97 $108,250 +80.4%

Dec-96 $95,239 +58.7%

Dec-95 $88,800 +48.0%

Dec-94 $74,533 +24.2%

Dec-93 $81,002 +35.0%

Dec-92 $84,726 +41.2%

Dec-91 $87,246 +45.4%

Dec-90 $76,904 +28.2%

Dec-89 $91,919 +53.2%

Dec-88 $84,916 +41.5%

Dec-87 $84,079 +40.1%

Dec-86 $97,688 +62.8%

Dec-85 $96,159 +60.3%

Dec-84 $84,680 +41.1%

Dec-83 $90,854 +51.4%

Dec-82 $86,713 +44.5%

Dec-81 $79,628 +32.7%

Dec-80 $89,410 +49.0%

Dec-79 $76,722 +27.9%

Dec-78 $72,193 +20.3%

Dec-77 $69,175 +15.3%

Dec-76 $74,530 +24.2%

Dec-75 $63,669 +6.1%

—Dec-74 $50,482 -15.9%

Dec-73 $66,026 +10.0%

Dec-72 $79,389 +32.3%

Dec-71 $71,656 +19.4%

Dec-70 $67,302 +12.2%

Dec-69 $66,362 +10.6%

Dec-68 $76,575 +27.6%

Dec-67 $76,567 +27.6%

Dec-66 $70,349 +17.2%

Dec-65 $83,286 +38.8%

Dec-64 $83,760 +39.6%

mean: $78,856 +31.4%

sd: $14,535 24.2%

max: $116,433 +94.1%

min: $47,067 -21.6%

Jan

25

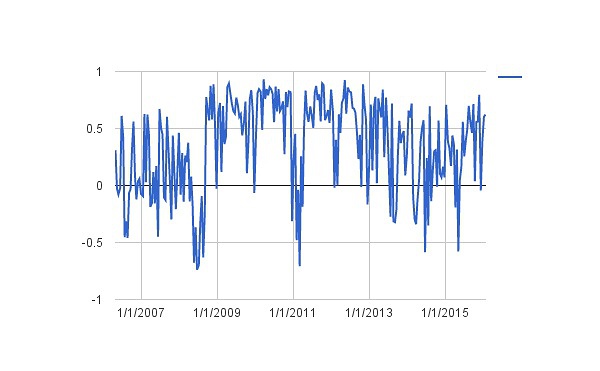

Oil and Stock Correlation, from Kim Zussman

January 25, 2016 | Leave a Comment

The correlation between daily changes in SPY and USO were checked every non-overlapping 10 day period, from present back to 2006. The attached chart shows the result.

Current correlation between stocks and oil is high but consistent with the entire period, though recently somewhat higher than the past two years.

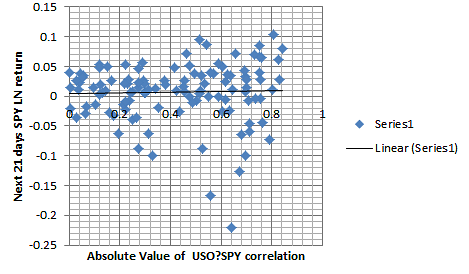

Russ Sears writes:

Here is a scatter of the Absolute value of 21 day correlation of USO/SPY at the start of each calendar month. To the next 21 trading days log normal returns. I used the Absolute value because it appeared high R^2 increase volatility even if the correlation positive or negative. But R^ 2 curves this relationship. Not predictive but clearly implies increased volatility with higher R^2

.

.

.

.

.

.

.

.

I would suggest that there is however much more to this suggested change in regimes on a daily or day trader holding period basis and those interested should study it further .

Jan

25

What Are the M’s Doing? from Bill Rafter

January 25, 2016 | Leave a Comment

Every now and then it is advisable to check out what the Fed is doing. There have been upticks recently in the aggregates (since New Years, and concurrently since the drop started), although in my opinion the upticks do not alarm or impress.

{kind=link}

{kind=link}

Jan

25

Baneful Alpine Gabfest, from Victor Niederhoffer

January 25, 2016 | Leave a Comment

One wonders if with all the people who hate business, the collectivists and world staters who assemble at Davos each year, whether there is a tendency for the market to be bearish during their retreat. Certainly it inspires the palindrome to be bearish as he has so many followers there than can exponentiate his already put on position.

Jan

25

Oil Prices and the Iran Arrests, from Andrew Goodwin

January 25, 2016 | Leave a Comment

I am struck by the news that Iran arrested 100 protesters who torched the Saudi embassy and announced it publicly. As you may recall, Iran usually blames elements like "students" and does not intervene. If they make arrests, it's behind the scenes.

I am struck by the news that Iran arrested 100 protesters who torched the Saudi embassy and announced it publicly. As you may recall, Iran usually blames elements like "students" and does not intervene. If they make arrests, it's behind the scenes.

This may indicate that the Shiites are willing to make a deal with Sunnis to get the price of oil up a bit. As the price of oil drops the volatility used to rise as the chances of OPEC cutting supply increase. When the Saudis cut off the head of Nimr, and the Iranian "radicals" attacked the embassy, it seemed less likely that they would think of even talking. That looks like a item to stick in the bullish column for oil prices.

"Iran arrests 100 people over attack on Saudi embassy"

Jan

20

On Growth and Form, from Andy Aiken

January 20, 2016 | 1 Comment

I first learned about Thompson's On Growth and Form at a talk back in the late 80s by Benoit Mandelbrot, who referenced the book as an influence. I think Thompson's book has relevance to equity markets, philosophically as well as on more practical terms. Thompson simply observed nature and described relationships of form to function. He didn't attempt to infer an evolution process. In this sense the book is an early precursor of Bejan's Constructal Theory.

I first learned about Thompson's On Growth and Form at a talk back in the late 80s by Benoit Mandelbrot, who referenced the book as an influence. I think Thompson's book has relevance to equity markets, philosophically as well as on more practical terms. Thompson simply observed nature and described relationships of form to function. He didn't attempt to infer an evolution process. In this sense the book is an early precursor of Bejan's Constructal Theory.

Examples: Thompson shows that the speed of a fish or ship is proportional to the square root of its length, and that the kinetic energy exerted by an organism is proportional to its mass to the fifth power. Thompson considered form as the product of the dynamic forces acting upon it. Logarithmic spirals reflect a constant proportional growth rate. The logarithmic spirals in pine cone scales or sunflower seeds result in a Fibonacci expansion in the number of scales or seeds. The Fibonacci sequence is just a discrete version of the continuous logarithmic curve.

It's not unrealistic to think that logarithmic spirals and Fib sequences crop up in equity prices. Daily returns are often assumed to be lognormally distributed. The relationships are probably not as simple as "stock x should drop to 38.1% Fib level and bounce".

One of the forces acting on the form in this case is human perception of emerging patterns. One of the more powerful conclusions drawn by Thompson is that many species share features that are invariant under simple linear transformations. So the shape of a gorillas skull and skeleton is the same as a human's through a "stretching" deformation.

If we make an analogy to stocks, this could imply self similarity in price patterns (fractal relationship) or the idea that we need to adjust for both price and time transformations when using historical analogs to predict future returns..

Jan

20

China Rally, from Sushil Kedia

January 20, 2016 | Leave a Comment

Anyone see a 20% move up in SHCOMP by Counting or by Mumbo?

There is consensus that China will take this world down. If there is such a rally, is the world also going to rally by the same amount?

If not can ideas similar to bond convexity be applied to inter relationships between key equity markets and all equity markets and if such convexities shift and or change over time what import do such shifts carry for either quant forecasting or for mumbo jumbo?

Jan

18

The Testing of Support, from Victor Niederhoffer

January 18, 2016 | 6 Comments

Six Charts That Show Stock Indexes Teetering at Key Support. Six major indexes are testing key support levels amid the current market selloff. Whether these hold or break will be a significant factor in determining if the global decline extends. - Bloomberg terminal

One sees a headline on bloom saying that 6 major indexes are now testing support and whether they hold or not will determine the likely course. I don't know what the indicators are but one doesn't know how support can be measure and also whether a break is bullish or bearish. All my studies and the quantifications show that the more the big drop the greater the positive expectation. One indicator is stock to bonds at 11. 78. As far as I can see a multi year low (a well meaning assistant has made it impossible for me to go back for more than a year with alacrity). Which is better, the upside down man's toilet paper view or the 40,000 fold a century view with a view to where it's starting from with a 7% spot from where it was a month ago.

Jan

18

Chris Davis, from David Lillienfeld

January 18, 2016 | Leave a Comment

It will come as no surprise to readers of this list that I am an Orioles fan. Like most fans,

It will come as no surprise to readers of this list that I am an Orioles fan. Like most fans,

(In 33 days, Orioles pitchers and catchers report. Spring is almost here. It's raining in NorCal and there's snowpack at Lake Tahoe. Almost all is right in the world.)

I enjoyed the dominance of the 1970s (actually, 1969) through the early 1980s, and living through the dim times at the beginning of this century. The Orioles traditionally were built around pitching defense and the 3-run home run (aka Earl Weaver Specials). Speed didn't much matter, contact hitting didn't much matter, bunting and such didn't have much of a place, hit and run wasn't of consequence (though these days, the Os are hardly unique in that regard), and so on. And Orioles Park at Camden Yards (aka Camden Yards, or just Yards for the locals—23 years young and still one of the greatest, if not the greatest, places to watch a ball game in the baseball universe) is certainly a ballpark made for power hitting left-handers, with 318 ft down the right field line.

Of course, not every major hitter the Os have sent to the plate at the Yards has been a left handed one. Cal Ripken spent half of his epic career (no, not just the streak, but the 400 HR and 3,000 hits) at the Yards—always as a righty. More recently, Nellie Cruz dominated the HR race as a righty at the Yards. But lefties have an advantage.

Enter Chris Davis, the Os All Star first baseman. Davis started his career in Texas, and it's pretty clear that it's principally been since coming to the Os that he's experienced success. Lots of success. Twice leading the AL in homers, once in RBIs, and if he didn't strike out so much chasing some awful pitches, he may have gotten a Triple Crown. Alas, it was not to be.

This year, Davis is a free agent. He's been offered $150+ mil for 7 years. Not chump change. But the Os have made it clear to Davis's agent, Scott Boras, that the offer is what it is. Some have even suggested that the offer has been withdrawn )including the Os). But if Davis were interested in accepting it, I doubt there would be the least hesitation from the Orioles front office in putting it back on the table. Meanwhile, Boras is shopping Davis as a first baseman-left fielder. That latter one is interesting. I can't imagine Davis hitting as well while learning left field on a permanent basis. But he is getting shopped around, and some have suggested that Detroit will pick him up and drop him into left field. Maybe. But one of the things that no one has ever suggested about the Os, even during the awful 2000-2010 period, is that the team lacks heard, lacks soul. Cruz made it pretty clear that he wanted to stay in Baltimore. Seattle apparently made him an offer impossible to refuse.

So what will happen with Chris Davis? If I were a betting man, I'd bet that Davis is going to play for the Tigers next year. Fortunately, there are only a limited number of games that the Os would have to face him. I think he might find that his performance isn't quite what he's used to, at least for a year while he learns a new position. As for relations between Scott Boras and the Os, well, it's baseball, there's always next year. At least Duquette actually did something this winter.

Jan

18

Clustering, from Alston Mabry

January 18, 2016 | Leave a Comment

Where is SPY 10 tdays later, after >7% drop over 10 tdays, using only first occurrences to eliminate overlap:

count: 27 mean 10d move: +0.2%

Ref: For entire SPY period, 1993-present, including overlapping periods, mean 10-day move is +0.32%.

date / 10d fwd

24-Aug-15 +4.18%

3-Oct-11 +9.37%

4-Aug-11 -4.78%

30-Jun-10 +6.26%

24-May-10 -1.01%

7-May-10 -1.93%

20-Feb-09 -10.98%

16-Jan-09 -2.92%

12-Nov-08 +3.67%

3-Oct-08 -15.52%

17-Sep-08 -0.47%

17-Jan-08 +4.61%

27-Jan-03 -1.40%

23-Sep-02 -5.41%

3-Sep-02 -0.51%

12-Jul-02 -6.80%

2-Jul-02 -4.45%

10-Sep-01 -5.10%

12-Mar-01 -1.81%

21-Feb-01 +1.08%

12-Oct-00 +2.68%

14-Apr-00 +8.13%

7-Oct-98 +9.78%

31-Aug-98 +8.40%

4-Aug-98 +3.15%

27-Oct-97 +5.95%

16-Jul-96 +1.29%

It was easier in the 90s.

Jan

18

A Nice Technical, from Steve Ellison

January 18, 2016 | Leave a Comment

I was discussing the Weibull distribution, the classic bathtub distribution, with a colleague this week in the context of time to failure of computer hardware. He pointed out that the Weibull distribution is really a combination of two distributions, a distribution of the weak (high "infant mortality") and a distribution of the strong (in which wearing out from old age is the primary culprit). This is an interesting insight that might have applications in our field.

Jan

18

Bernie and the WSJ, from Kim Zussman

January 18, 2016 | Leave a Comment

Around the time Bernie Madoff became famous I quit my subscription to the Wall St. Journal. The paper had lost its allure as an erudite alternative to leftist treyf in California, for personal reasons.

Around the time Bernie Madoff became famous I quit my subscription to the Wall St. Journal. The paper had lost its allure as an erudite alternative to leftist treyf in California, for personal reasons.

As a young man I subscribed to the LA Times. Dutifully every morning skimming the headlines and articles over coffee before work because one should stay abreast of current events. However over time one became too sad and too angry at the start of every day, and upon analysis the Times was dumped. Overselling tragedy and engineered remediation, I concluded, and my bid faded away.

The new Wall St Journal subscription paid for itself almost immediately. A local politician / financial planner had been pitching his version of 401K for my business, along with his generous commissions and yearly management fees. Luckily I spotted a Schwab ad for a SARSEP IRA plan - which (then) could provide 401-like benefits for zero fees or commissions. The plan was adopted, later grandfathered, and to this day continues (cost free).

So I owed her big time. And truly appreciated the more balanced views and high school level writing. But as trading evolved I was found to be too weak to view hourly or even daily market updates. It was better to study the moves and avoid the noise because, even emanating from a quasi-non-hystrionic viewpoint, all noise was ultimately detrimental to discipline. (Applies to these lists as well) So the Journal was quit.

Recently Ben and Jerry Leftkowitz of ice cream fame thought to fund a new flavor in honor of socialist fart Bernie Sanders:

"I have fantasized about a Bernie Sanders ice cream, and it would be called 'Bernie's Yearning,'" Cohen said in a recent CNN interview. "It would be a giant chocolate chip on top of the ice cream that covers the entire top. . . . The rest of it is all mint. The giant chip on the top represents all the wealth that has gone to the top 1 percent of the population over the past 10 years," he added, nodding to the Vermont senator's decades-long attack on inequality in America."

For one thing it should be a marshmallow on a mound of chocolate chip. For another………a call to action. Like the clarions of an archaic generation - if not now, when? It was time to re-enlist.

Bernie made me re-subscribe to the Wall St Journal….print edition to be delivered again next week.

Jan

18

That $2.5T in Lost Oil Revenue, from Alston Mabry

January 18, 2016 | Leave a Comment

Listening to fin-tv, one hears over and over, "But low oil prices are good for the economy, so why is the market going lower?" And then a friend posed the same question. I said, well, there's a lag…

On the negative side are the oil producers and their ecosystem, who are no longer receiving that $2.5T in revenues. On the positive side are the consumers who are no longer paying that $2.5T.

On the positive side, the effects of, say, lower gasoline prices are generally subtle. Andy Average fills up the tank and notices that it's under $2 a gallon - cool. But he doesn't project forward the effects on his checking account for the next six months and then decide that now he can afford to buy that nice leather jacket. Instead, six months from now, a few hundred extra dollars have accumulated in the checking account, so he has to decide on the jacket, or paying down credit card debt.

A small business running a fleet of pickups doesn't see the lower prices as a game-changer or anything. Maybe budget for a few extra replacement tools.

But on the negative side, for the people no longer getting the $2.5T, it's a *crisis*. Debt restructuring, default or bankruptcy. Political instability - including the possibility of death - and civil unrest. Job losses, budget cuts, bonuses gone - major impact on individuals and families. Even Norway is having an oil-price crisis.

The negative consequences are immediate and vivid, while many of the positive consequences may go unnoticed for a while.

Jan

18

Speculator Vicissitudes, from Bo Keely

January 18, 2016 | 3 Comments

The appearance of the stock ticker machine in 1867 removed the need for traders to be physically present on the floor of a stock exchange. Speculation underwent dramatic expansion, and with the connection of the internet boundless expansion occurred. Basically, speculation to me means higher risk investment that turns over rapidly. The coin is not in the air long. Another characteristic of speculation is that it's a judicious process of learning which makes it an intellectual competition. The market is like a gigantic chess tournament.

The appearance of the stock ticker machine in 1867 removed the need for traders to be physically present on the floor of a stock exchange. Speculation underwent dramatic expansion, and with the connection of the internet boundless expansion occurred. Basically, speculation to me means higher risk investment that turns over rapidly. The coin is not in the air long. Another characteristic of speculation is that it's a judicious process of learning which makes it an intellectual competition. The market is like a gigantic chess tournament.

Traders then are a set type with traits, or they generally fail. They are usually competitive, individualistic, romantic, capable of bearing risk, athletic, of an addictive nature, scholarly, analytical, and good with numbers.

As a kid perhaps you recognized patterns in your stamp collection or on the baseball field, and sat alone in trees in independent thought analyzing them for the outcomes. You were passionate but rational, and one day went out on a limb to the idea of trading in the markets. Perhaps you had a mentor, or came up the harder way via books and trial and error which fosters patience. You were smart to start out small, and parlayed a stake into larger trades that afforded an augmentative income with dreams of diving full time into the market.

As a fish, to amphibian, to reptile in the market you've done what everyone else has – studied the books, surfed the websites, made some trades, attended a couple of seminars; and then one day it hits you like a ton of bricks - knowledge is power. The more knowledge the more power. However, infinite knowledge is limited by the time to learn it, so you map a plan to first study the central ideas to your trades, and expand from that nucleus outward. And you win.

As the information snowballs and interconnects a second paradigm arrives – I'm not thinking about a hunch or gut feeling. It's not about a trend or percentage game. You will predict the future by thinking. Think, think, think accurately. It gets to be a habit wherever you go. If you think fast you will be first.

One evening you look in the mirror and see a thinking guy or gal who has it all. There are facial creases of frowns and joy, but mostly the latter. That's when the third epitome shatters the glass – it's all about decisions. You keep right on making them even when you don't need to. You get into a what if thing, and start speculating about what you would do if some problem was yours instead of somebody else's.

Trading is a dual major in liberal arts and math. The former provides overview, but math is where you are measured and the ruler of your percentage success. The poetry of math, statistics, govern your choices.

The idea of going up against huge funds on an immense board finding ways to beat them is a real high. The rolls and swells at home become secondary to the lows and highs at the market. Little David vs. an illuminated Goliath and getting rich off the battle.

What you do next is decide to trade full time or not. The general guidance is to try anything new without burning bridges. As a full time trader, you're information is vast, thinking habit is hard, decisiveness is always near, and it doesn't matter how fast the market moves and changes, you're on top of it with a select few.

They are squeezed through the rollers of pressure. Ultimately you must have in your nature the trigger to pull under stress situations. The brighter they burn, the hotter you get.

There are many good analysts in the markets, but because of two Achilles heels few of them are able to translate their analytical prowess into profitable speculation: They must learn to walk away from a bad trade, and to avoid financial greed. There's nothing wrong with breaking Ft. Knox after Ft. Knox, but one day you will make substantial money to discover there are other challenges that speculation may support.

There is not time for romance and coffee now; this isn't a Louis L'Amour novel.

The summit of speculation is scantily populated by those who became high rollers from meager beginnings who play the market hard to win and learn rather than create surplus cash. The real thrill is working the game itself, like a kid on a perpetual peak experience. Turning the math into money, watching the bank grow without breaking character.

If you are original and creative but also a rational thinker, you may have what it takes to get on the road to speculation. Remember that experience counts for more in this profession than most, and paper trade at first, then graduate to trading with minimal funds, and scale up as your training, experience and resolve heighten like a professional athlete.

Success in speculation is a metaphor for achievement of self.

Jan

18

Article of the Day, from Andrew Goodwin

January 18, 2016 | Leave a Comment

This is very good writing starting with The Hateful 8. Economic theory with current events considered.

This is very good writing starting with The Hateful 8. Economic theory with current events considered.

"Slavoj Žižek: The Cologne attacks were an obscene version of carnival"

Andy Aiken comments:

"So what if we conceive of the Cologne incident…as a carnivalesque rebellion of the underdogs?"

To dismiss what happened in Cologne as a droll little Rabelaisian episode is forgetting that the middle class they deride keeps the lights on at the universities. The Euro and US left intellectuals will be surprised at how swiftly they find themselves on the losing end of a cultural counterrevolution, how adamantly the return of Volkish horrors defies their browbeating.

But they have created the preconditions for this. The social sciences have become as detached from the tradition of free inquiry as University of Freiberg was in the 1930s. They have thrown away the weapons that could have fought it.

Jan

18

Deflation, from Anatoly Veltman

January 18, 2016 | 1 Comment

My friend's bearish posture toward Stocks stems from deflationary signs. Yes, they are pronounced. Wage growth has been non-existent. There is no pricing power anywhere. Currently you can't give away raw materials world-wide. Copper at $1.95, Brent led WTI to below $30, grains/fertilizer are cheap. Coal must be given away: just look at US's largest coal Peabody (BTU), down from $1100.00 in 2011 to below $4.00! Uranium is shunned: I notice UEC down from $7 in 2011 to .72 cents! World's largest miner FCX is $4.35 from $60+ in 2011. No wonder credit is being pulled from under most of Canada's enterprises, with Canadian currency depreciating 50% during the same time frame. Investors dread holding the bag over the weekend, as increasingly more corporate treasury shenanigans may need to be disclosed/announced.

My friend's bearish posture toward Stocks stems from deflationary signs. Yes, they are pronounced. Wage growth has been non-existent. There is no pricing power anywhere. Currently you can't give away raw materials world-wide. Copper at $1.95, Brent led WTI to below $30, grains/fertilizer are cheap. Coal must be given away: just look at US's largest coal Peabody (BTU), down from $1100.00 in 2011 to below $4.00! Uranium is shunned: I notice UEC down from $7 in 2011 to .72 cents! World's largest miner FCX is $4.35 from $60+ in 2011. No wonder credit is being pulled from under most of Canada's enterprises, with Canadian currency depreciating 50% during the same time frame. Investors dread holding the bag over the weekend, as increasingly more corporate treasury shenanigans may need to be disclosed/announced.

Yet Chair reminds us that all of that is (eventually) Bullish, as the lower input prices should act to improve margins. But how do you re-ignite demand and revive pricing power? Surely not by interest rate hikes via the lift-off. So what policy actions can we anticipate nowadays, as Bullish weekend surprises?

anonymous replies:

The usual quibbles:

FCX is not the "'world's largest (copper) miner"; SCCO is. Its price has fallen by half from its peak at the end of 2012 and by a third since its recent high in May of last year. Hardly wonderful performance but nothing extraordinary for the copper business. The decline in FCX is a comment on its woeful balance sheet. The company has a quick ratio of .6 and current ratio of 1.7; SCCO's numbers are 2.5 and 3.5.

Even two years ago, none of the public U.S. coal companies had a balance sheet that was anything but a joke, especially if you included the pension liabilities. Peabody was bankrupt 2 years ago; the stock market just didn't know it.

As Carder has patiently explained for over a year now, in the U.S. coal now suffers from having direct price competition from natural gas. Those of us who lost a third of the money we put into a coal mining equipment stock (JOY) last year bought the company because, unlike all the U.S. public coal companies, it had a decent balance sheet. It still does; and if we were not busy trying to lose more money in the refiners, we would be tempted to try for being a 3-time loser now that the private owners of coal reserves (the Lexington KY gang) have gotten some wonderful news.

For those who are looking for possible speculations, the Stowe Coal Index is the best source.

In carbon-based energy, demand is not the problem, even for coal; supply has been. The dramatic increases in output from new production techniques (fracking, continuous miners to name 2) have created a surplus. The question now is how much of a surplus. The EIA now says it will be a year before supply and demand in oil match each other.

Jan

18

Waves Versus Stats, from Andrew Goodwin

January 18, 2016 | Leave a Comment

I think the key to levered macro speculation is that the people who do it have to make public statements to move everyone else to their point of view. The goal they have is to make everyone have the same view of the world. Their weakness is that they have to express their opinion to others to make it viable before they make their big move that finally reverses the prices.

When you get the infrequent statement from a flexion, that is time to switch from short term patterns to wave trading. The flexions don't boast and brag all the time and tell you what they are doing. They wait until they can pounce to tell of their positioning.

They go silent once the market starts going their way and let the other folks do the work. Once you get into a reflexive pattern like oil prices where they have to pump more to get the same amount of money as the price falls, the pattern trader is taking too much risk even if he wins on the buy side.

Jan

18

You Were Asking for Easy Money, from Anatoly Veltman

January 18, 2016 | Leave a Comment

While the world was mesmerized with China currency "manipulation", and played hot potato with equities worldwide - the Japanese retail and institutional investors decided over the weekend that they've had it enough with chasing South African yields. The result was a 10% gap opening that produced a new all-time low in that country's currency. Of course, the opening was overdone, and the extreme quotes were way too wide to deal any substantial size. Yet, the signal went out - even if it was little noticed.

While the world was mesmerized with China currency "manipulation", and played hot potato with equities worldwide - the Japanese retail and institutional investors decided over the weekend that they've had it enough with chasing South African yields. The result was a 10% gap opening that produced a new all-time low in that country's currency. Of course, the opening was overdone, and the extreme quotes were way too wide to deal any substantial size. Yet, the signal went out - even if it was little noticed.

So the South Africa Reserve Bank will have to deal with run on their currency. Indeed, no Central Bank will allow overly rapid devaluation - so they'll have to be buying Rand in the open market, daily. With what? Obviously, they can't spend their meager reserves of US Dollars doing that - and they'll have to auction off or pledge some of their Gold reserves (I believe they hold Platinum bricks as well).

Now, when I pointed that out at last night's CME open, Gold was still up much bigger than Silver - on pure speculation. Speculation based on standard notion that Gold would be more valuable than Silver "during Stock Market uncertainty". That's pure speculation. The dynamics I point out about the South African Central Bank is less of a speculation - they are rather the actual procedural transactions in these kinds of circumstances. Thus buying Silver futures against a sale of Gold futures was a smart thing to do right from the Sunday night open. And that's as close to easy money as one can come!

anonymous writes:

Just read the South African Reserve Bank's annual report and appendix: "Management of gold and foreign exchange reserves." They don't have any platinum. Their forex reserves have increased to over $60 Billion (according to this document). So they've got plenty of ammunition to intervene if they want to.

Markets will do what they want to do. However, if the gold and silver markets are behaving based on Anatoly's theory, the mkts are wrong on the facts.

John Floyd writes:

My African Grey parrot has learned to whistle the beginning of the Rocky theme song. I would frame the opening two rounds between anonymous and Anatoly more broadly by considering the following.

1. To what extent does the move in the South African Rand last night portend for future pockets of illiquidity, for example the stock flash crash, the fixed income flash rally, the Chinese currency devaluation, etc. ? How might that be best handling offensively and defensively?

2. Why has the decline in oil and gasoline prices not transpired to a more robust pickup in consumer spending?

3. Why are corporates generally more willing to buy back stock than increase capital spending?

4. Is it an issue that according to the BIS emerging market debt has risen from $15 trillion in 2010 to $25 trillion today?

5. What happens to domestic risks when foreign currency denominated debt has increased from $1.5 trillion to $5 trillion?

6. What happens to inflation when emerging market currencies plunge and how do central banks respond in an already weak domestic economy?

7. If the Fed was concerned about global risks in September how might this change their behavior?

8. In 2008 troubles in the US$10 trillion mortgage market had broad implications, are there parallels today?

9. What might occur to cause present market themes and trends to reverse?

That is enough for 9 rounds and hopefully we can all make a victory run up the Philadelphia Museum of Art steps and perhaps make enough to buy van Gogh's Sunflowers inside.

anonymous comments:

We all must acknowledge that the stock market (and subsequently bond markets) seem connected at the hip with the crude price right now. Does this make sense? I don't know. But it is what it is.

This oil discussion got me to finally run some quick numbers. I'm sure similar numbers have been in the press, but I like to look things up for myself.

In my cheap-seat view of the world from my gopher hole, I've been thinking about how there are certain crucial parts of the global equilibrium that have gone through important changes, and that part the current volatility is a process of finding the new equilibrium.

The various QEx/on-off moves are part of this. And also China, in that they are (slowly [probably]) moving away from the mercantilist import/currency/capital control system, which created the macro-financial jet stream effect where we bought their stuff, and they sent the dollars back to their Fed account, to the tune of a few hundred billion a year, while they paid off their exporters with new yuan and thus created a global inflation sink.

But the biggest, quickest change has been oil. Some nice rounded numbers, referring to the change in $/bbl from June 2014 to present:

global avg daily consumtion: 90M bbl price change: -$77/bbl loss of revs to oil producers: $6.93B/day annualized loss: $2.53T

A big chunk of that money flows into Saudi (about 1/9 of global oil revs), and they have some kind of pattern of spending and investment. Used to be the Saudis spent a big piece of it on gold. Probably not so much now.

They are like one of those deep-sea hot-water vents where the life grows around it. There has been an equilibrium for a long time with that money flowing into oil producers and providing the hot water for those vents. In a very short time, ~$2.5B of flow has shifted away from that system, not to mention all the downstream segments like the integrateds, mids, E&Ps, etc.

I remember when big numbers had an M. Then we moved to B. Now to be big, a number has to have a T. I figure a $2.5T change in the global equilibrium is going to take a while to digest, not to mention the unrealized political consequences in the Middle East and elsewhere.

Again, without being overly precise, subtract US oil exports from imports, and you wind up with 9.2M bbl/day, which translates to a little over $700M/day in payments, which annualizes to $260B. Which, all other things being equal, should be less downward pressure on the USD.

Cui bono? The American consumer, of course. Again, June 2014 to present:

avg gas price/gal:

June 2014: $3.766

Dec 2015: $2.144

Change: $1.622

US est daily gas consumption: 375M gal

Daily savings: $608M

Annualized: $222B

That's our piece of the action, and it has to be really good for somebody.

I can't think of a clever summary, so there it is.

Jan

14

There is Much Talk, from Victor Niederhoffer

January 14, 2016 | 1 Comment

There is much talk of bearish forecasts and bearish things. I don't buy it. I just believe it's an even better time to garner that 40,000 fold a century return. Quantifying it, the greater it's down over the last relevant 4 day, the more bullish it is. And guess what, almost most bullish of all is down 10% from a hi. I note Israel was relatively strong only down 0.2 % on Monday there as well.

Gary Rogan writes:

I don't claim any consistent ability to predict the next few months. I didn't think the late September to early November snap-back in the stock markets would happen. One can still have an opinion. Victor is pretty much optimistic no matter what. For sure in terms of not unduly exiting one's long-term positions on some hunch that's valuable because of the drift. I was actually quite optimistic in March of '09 after a huge fall, but (possibly mistakenly) only for high-quality consumer non-durable stocks. Until about a year and a half ago I had no particular opinion as it was something in between, and then turned pessimistic. Of course the longer the market stays down and especially goes down the larger the expected returns at that point will be. As I'm mostly in the market as always and only have slightly larger reserves than average to deploy if and when good cheap stocks shows, my only downside is that they never do. If so, so be it. The real question is the effect of low interest rates on how expensive stocks can or "should" get vs. historical stock ratios with respect to their various internal parameters and the tendency of the latter not to grow to the sky. As there is a lack of precedent for how the Fed has behaved in the last almost decade and how all of this will play out at the end of secular interest rate declines and happy days in commodities, there could be a difference of opinions.

Jan

14

Interesting Blog: State of Start-up Funding 2016, from Stephanie Harvey

January 14, 2016 | Leave a Comment

Silicon Valley-centric but a very quick read: "The State Of The Startup: Fundraising Market In 2016"

Silicon Valley-centric but a very quick read: "The State Of The Startup: Fundraising Market In 2016"

Highlights:

- $42B invested in start-ups in 2015

- 34% in seed or series A.

- Substantial shift to consumer investments

Concluding paragraph:

"The late stage market may witness a different phenomenon. More than 40% of the dollars invested in Series B and later rounds originating from corporate venture capital, mutual funds, hedge funds and family offices. This money isn't committed to startup investing. Investment strategies for these types of investors can change quickly. If suddenly all that capital were to disappear and everything else were to remain the same, about $10B would leave the startup ecosystem - a drop of 25%. That would surely be felt across Startupland."

Author is a VC at Redpoint.

It feels a lot like dot-bomb in these here parts…

All the best, Stefanie Harvey

Jan

14

The Gujaratis, from anonymous

January 14, 2016 | Leave a Comment

A popular TV journalist from NZ sent me a link to this story with the comment that it explains lots of things and that I must read it: "The Gujarati Way"

A popular TV journalist from NZ sent me a link to this story with the comment that it explains lots of things and that I must read it: "The Gujarati Way"

Interest has been expressed in the Rothschilds and their business secrets among this group. This story on the secrets of the Gujaratis should be intersting to you as well.

Stefan Jovanovich writes:

If you substitute the word "Lutheran" for Gujaratis, you could tell the same story about their "secret" success in becoming the largest grain farmers of North and South America. It would not actually tell you anything, but it would be an equally plausible fiction and yet another iteration of the Carlisle/Emerson/Roosevelt (TR)/Rhodes fantasy about commercially favored strands of ethnic DNA.

The Rothschilds had no "secrets"; they had connections and the advantage of being permanent outsiders. Since they were Jews, they could be trusted by the Royal Houses of Europe precisely because they had no chance of becoming politically-influential in their own right. They could be trusted to hedge every position. Their influence declined precisely when the Germans and French and British all decided that the answers to questions finance were political and the rewards of empire would pay for all the military peculation.

Jan

14

Our Calendar Color Coding Scheme, from Alex Castaldo

January 14, 2016 | 5 Comments

Can you please outline the color coding rationale for the daily performance chart. I am confused on why some down days are red and the others are yellow..etc - A Reader

We track daily movements in U.S. stocks and bonds (specifically S&P Index futures and Long Bond futures).

The colors are based on the performance of both markets:

Red days: both stocks and bonds down.

Green days: both stocks and bonds up.

Yellow: stocks up, bonds down.

Blue (technically azure): stocks down, bonds up.

The bond futures movements are expressed in points and thirty-seconds of a point. For example 1.25 actually means 1' 25" i.e. 1+25/32. The S&P futures changes are in points.The abbreviation USB stands for US Bonds (the actual futures symbol is US on Bloomberg, ZB on some other systems).

(Original post dated June 25, 2011. Edited January 14, 2016)

Jan

12

Individualist Movie Review:The Revenant, from Bo Keely

January 12, 2016 | 4 Comments

If you want to see individualism at its best go watch mountain man Hugh Glass on a fur trading expedition in the 1820s battle a grizzly, scalped by Indians, swim frozen rivers, fall off a steep cliff onto a tall pine, gunshot, stabbed, and on to the campfire warmth of his own hunting team.

If you want to see individualism at its best go watch mountain man Hugh Glass on a fur trading expedition in the 1820s battle a grizzly, scalped by Indians, swim frozen rivers, fall off a steep cliff onto a tall pine, gunshot, stabbed, and on to the campfire warmth of his own hunting team.

The story is inspired by a real life, though likely enlarged as the frontiersmen biographies I've read. However the acting is decent, especially by the animals, and the photography is exquisite.

It's hard to sit still during the movie and not head for an exit out to the wilds.

Jan

12

If You Were In Charge, from Larry Williams

January 12, 2016 | 7 Comments

If you were the Government of China, what would you do to stabilize the Yuan and stock market?

If you were the Government of China, what would you do to stabilize the Yuan and stock market?

Best answer gets dinner on me at Spec annual rendezvous.

Dylan Distasio comments:

Somewhat tongue in cheek…

1.Eliminate all restrictions on position size for stocks/futures

2. Eliminate all restrictions on foreign ownership of A shares

3. Let the currency float with no intervention

4. Let creative destruction run its course

5. ???

6. Profit

Jan

12

Video of the Day, from anonymous

January 12, 2016 | 1 Comment

Why chart reading is confusing: "When a Circle is a Straight Line"

Jan

12

First Five days of January in 2016, from Kim Zussman

January 12, 2016 | Leave a Comment

The first five days in January were down more than 5% for for SPY. From 1994-2015, here are the returns for the 1st 5d, and the subsequent 5d, 10d, and 30d periods (starting from end of 5th trading day for each year, T test vs zero). First set is subsequent returns for all years–both up and down first %d:

One-Sample T: 1st 5d, nxt 5d, nxt 10d, nxt 30d

Test of mu = 0 vs not = 0

Variable N Mean StDev SE Mean 95% CI T

1st 5d 22 0.007451 0.020490 0.004368 (-0.001634, 0.016536) 1.71

nxt 5d 22 -0.001853 0.022606 0.004820 (-0.011876, 0.008170) -0.38

nxt 10d 22 -0.005438 0.032450 0.006918 (-0.019826, 0.008949) -0.79

nxt 30d 22 -0.001758 0.060676 0.012936 (-0.028660, 0.025145) -0.14

>>slightly down, NS

Next are the subsequent returns when the first 5d of the year were up:

One-Sample T: 1st 5d+, nxt 5d+, nxt 10d+, nxt 30d+

Test of mu = 0 vs not = 0

Variable N Mean StDev SE Mean 95% CI T

1st 5d+ 15 0.018284 0.011132 0.002874 ( 0.012119, 0.024449) 6.36

nxt 5d+ 15 -0.005035 0.026227 0.006772 (-0.019560, 0.009489) -0.74

nxt 10d+ 15 -0.006290 0.034643 0.008945 (-0.025475, 0.012895) -0.70

nxt 30d+ 15 -0.001706 0.065904 0.017016 (-0.038202, 0.034791) -0.10

>>also down, NS

Subsequent returns when 1st 5d were down:

One-Sample T: 1st 5d-, nxt 5d-, nxt 10d-, nxt 30d-

Test of mu = 0 vs not = 0

Variable N Mean StDev SE Mean 95% CI T

1st 5d- 7 -0.015763 0.016067 0.006073 (-0.030623, -0.000904) -2.60

nxt 5d- 7 0.004965 0.010197 0.003854 (-0.004465, 0.014396) 1.29

nxt 10d- 7 -0.003613 0.029654 0.011208 (-0.031038, 0.023812) -0.32

nxt 30d- 7 -0.001870 0.052451 0.019825 (-0.050379, 0.046640) -0.09

>>Mixed, with next 5d averaging +0.5% (albeit NS) and 10 and 30d down

Jan

12

Lord of the Flies and Slab City, from Bo Keely

January 12, 2016 | Leave a Comment

Lord of the Flies takes place on an otherwise uninhabited island among a group of boys who try to govern themselves. Some of the marooned characters are ordinary students, others of a musical choir, and the main castaways. Ralph quickly becomes the leader, not by physical force, but by being elected as having genuine qualities of leadership. Piggy is overweight with asthma and poor eyesight. He is the most physically vulnerable albeit the most intelligent of all the boys. Jack epitomizes the worst aspects of human nature when not under the thumb of society. Roger emerges as the sadist who kicks sand in the little guys' eyes. He will kill Piggy with a boulder that was not aimed to miss. And Simon represents peace and tranquility and positivity, often wandering off in a dreamy state by himself. When the Conch is blown, it calls the children to an assembly, where they agree that only the boy holding the Conch may speak at the meetings to forestall arguments and chaos, and is passed around to those who wish to speak their piece.

Lord of the Flies takes place on an otherwise uninhabited island among a group of boys who try to govern themselves. Some of the marooned characters are ordinary students, others of a musical choir, and the main castaways. Ralph quickly becomes the leader, not by physical force, but by being elected as having genuine qualities of leadership. Piggy is overweight with asthma and poor eyesight. He is the most physically vulnerable albeit the most intelligent of all the boys. Jack epitomizes the worst aspects of human nature when not under the thumb of society. Roger emerges as the sadist who kicks sand in the little guys' eyes. He will kill Piggy with a boulder that was not aimed to miss. And Simon represents peace and tranquility and positivity, often wandering off in a dreamy state by himself. When the Conch is blown, it calls the children to an assembly, where they agree that only the boy holding the Conch may speak at the meetings to forestall arguments and chaos, and is passed around to those who wish to speak their piece.

Slab City is a one square mile toenail of stark Sonoran desert on the edge of the New River that carries waste from Mexico to irrigate the surrounding crops of Imperial Valley, CA. As a World War II training center, Slabs has no jurisdiction, laced with spiderwebs of buckled concrete, and dead ends, where everyone looks you in the eye. Some of the main characters are the Alpha, a former banker and Special Forces, Ellie the Dog Lady who is the earth mother among the 200 residents, Buzz the caretaker of Salvation Mt., my old acquaintance the Mayor who acts as the hanging judge, BamBam the drug dealer, Sarah who plants flowers and kisses on everyone's faces, Builder Bob who runs the Music Range, and I'm tagged as the veterinary spiritualist. Mostly it's a ragtag collection of overintelligent rebellious kids. Everything is a joke to them. They exist entirely in the present, without responsibilities, conscience, or consequence. Each Saturday the Music Range blares free rock and roll with ten live bands that is also a call to stage of anyone who wishes to express his opinion in a rap or short speech.

The Beast in both the novel and Slabs represents the latent savagery lurking within all human beings. I think this is a product of evolution, nothing to be ashamed of, but simply a recapitulation of our remote ancestors. It stances on the controversial subjects of human nature, and individual welfare versus the common good. The theme in both places is a collection of young humans in conflict with the impulses toward civilization – living in harmony by rules – and toward the will to power. You must read the book or visit the Slabs to discover which way the balance teeters.

Lord of the Flies in my childhood set a mainsail in world travel to visit Utopias. I characterize Slab City as the last free place on earth (the others are uninhabited) where good and evil collide. But the study is exhausted.

I'm alone, 24 hours from Utopia, wherever that is.

Jan

11

Speculation vs. Gambling in ‘Bringing Down the House’ - Book Review, from Bo Keely

January 11, 2016 | Leave a Comment

One can hardly deny that making money runs the world today. There are the specialists in making easy money. These are broadly characterized as speculators and gamblers.

One can hardly deny that making money runs the world today. There are the specialists in making easy money. These are broadly characterized as speculators and gamblers.

Speculation and gambling have several differences.

Speculation involves increasing one’s chances to profit by various means such as news study, pondering, technical analysis, margin trading, hedging, options, and some have used psychics all with the aim of gaming profit from short or medium term market value fluctuations.

Gambling is wagering by means of an uncertain event with the aim of gaining additional assets. It requires consideration, chance, and a prize. The striking feature is that a small fee or amount is required with a chancy large return within a short time.

Bringing Down the House is the true story of how six MIT students turned gambling into speculation to fleece Las Vegas for millions. The best and brightest students are recruited by an eccentric former teacher with teeth like a picket fence of spades, diamonds, clubs and hearts to practice in a college backroom as the MIT Blackjack Team before invading the strip.

The nice thing about the book is that the secrets of card counting, shuffle study, ace cutting, hi-low counting, group spotters, third base coaches, card count code words, statistic indexes, and other tips the students used and the casinos don’t want you to know are revealed. Of course, one wonders the secret they did not reveal to win.

MIT proved blackjack is beatable and Ben Mezrich tells it with a suitable degree of suspense.

Speculation and gambling are similar in the manner in which they can acquire profit in a short time. Both methods involve risk but a speculator may learn more skills than a gambler’s plain luck to lower his risk. One may invest his hard earned money in intelligence such as Bringing Down the House.

Jan

11

Common Thoughts Among the Masses, from Stef Estebiza

January 11, 2016 | 1 Comment

Common thoughts among the masses:

Common thoughts among the masses:

Invest in bricks and mortar, you will never lose your money. Invest in banks, whenever a bank has collapsed? Buy oil. It can only continue to rise in price, considering the peak oil, etc…

Ralph Vince writes:

Banks?

Yes I did, starting in the summer of 08…buying and buying and buying and hotel room trauma in zero degree NR US city pacing at 4 am to meet margin call by 10…

My last position, Corus Bancshares, I saw print a 56 cents from a hot dog stand TV in Sarasota in the Winter of 09, and I knew my 55 cent limit was filled, my last position, exited with a profit — about enough to pay for my lunch that day after all of that!

I learned the hard way — banks aren't brick and mortar– they are bags of air, just as industrial companies are a web page with a picture of their parking lot on it, and some CNC drawings that are being used to make the product in Indonesian machine shops.

Jan

11

Oil and Free and Easy Money, from Stefan Jovanovich

January 11, 2016 | Leave a Comment

These are hard times for those of us who live in a Rogers Hornsby world. When asked what he did after the baseball season, Hornsby replied, "Look out the window and wait until spring". Note: he said spring, not spring training. It is only baseball when the games count. So, one is left with the short-timer calendar and idle thoughts.

These are hard times for those of us who live in a Rogers Hornsby world. When asked what he did after the baseball season, Hornsby replied, "Look out the window and wait until spring". Note: he said spring, not spring training. It is only baseball when the games count. So, one is left with the short-timer calendar and idle thoughts.

The idle thought for today is this: the fundamental correlation with stock prices is not "the economy" or even expectations about "the economy". What moves quotes is the supply of free and easy money. Leverage, through central bank and government guarantee lending, offers easy money; but the stuff that is both free and easy is never borrowed. It is the cash flow from businesses, colonies, possessions, conquests that have wonderful margins between what they cost and what they earn. The great bubbles of the early years of stock trading all came from one source: the discovery of a new territory that would duplicate the wealth that the Spanish had enjoyed for nearly two centuries from their ownership of the mines of the New World. "Mississippi" and the "South Sea" were going to produce the same fabulous returns. (Secondary idle thought: bubbles are created when pricing reacts not to the flows of free and easy money but to mattress money - the stuff people have been saving - that is tired of its meager returns.)

Since 1973 the free and easy money of the world has come from one source: the Middle Eastern oil fields. For the third of a century after the embargo that quadrupled the "normal" price of oil, the spread between what it cost to produce the black gold and what it reliably sold for was never less than 20 times the profit margins of everyone else's business. The collapse in prices in 2008-2009 was the first time that the sovereign wealth funds of the oil-exporting countries had had to examine the question of what to sell rather than what to buy. The current episode is a repeat, with the added pressure of the end of the Iranian embargo.

Is there any free and easy money left? The answer may be "yes, but not from energy but from American business itself". The Byron Wiens of this world have no idea of what regulation and taxation do to "average" profit margins. How could they? They live in a city where space itself is rationed by the government. If Mr. Wien's prediction about the Queen of the Night's election proves false, we may have one of those infrequent "ah-hah" moments in American political history when a significant number of the regulators are sent packing. Grant's election in 1868 was one; the Schlesingeristas in academia are still trying to square the circle of how the last third of the 19th century saw the country's greatest ever explosion of wealth, immigration and technology during a period of what they called "ruinous deflation". Harding and Coolidge's election in 1920 was another. 2016 might be yet another. After all, it is another even year. Go Giants!

Vince Fulco writes:

Every seven years, roughly, since 1973/4 at least, we have seen spots of liquidity vacuums, and as I have made mention on here before, it's the liquidity vacuums that re the thing to fear, not the proverbial "bear markets" (though they can coincide, see 80/81). Yes, 94 wasn't much of anything, but the recent action (go look at the opening on big, broad stocks on August 24, 2015) and it all fits the cyclical pattern of 7 year liquidity messes (and translates out into the future years of troubling asteroid flyby's coming up).

Is the liquidity vacuum that began in August over? Or do we have another wave coming? Either way, every single one of these situations we have seen, the market has moved on to higher highs in very short order, and I can;t find any compelling reason for that not to be the case here.

Jan

11

During the French Revolution, from Victor Niederhoffer

January 11, 2016 | 1 Comment

During the French Revolution, especially 1891-1897, the comedie francaise was restricted to performing shows that had no good things about royalty, and showed the peasants and bourgeoisie doing heroic things to slaughter the nobility.

During the French Revolution, especially 1891-1897, the comedie francaise was restricted to performing shows that had no good things about royalty, and showed the peasants and bourgeoisie doing heroic things to slaughter the nobility.

There was censorship and often imprisonment for the whole cast if they showed the lower classes in a bad light. This is according to Durant's "The Age of Napoleon" who documents many examples of this.

It's very much like the current kind of shows we are attuned to now, where the only ones that can manage to hope to score favorable reviews is if they show business in a very bad light and are otherwise consistent with the idea that has the world in its grip.

Jan

11

Movie Review: Ashby, from Scott Brooks

January 11, 2016 | 2 Comments

Starring Mickey Rourke, Sarah Silverman and a few mid - low level Hollywood types.

Starring Mickey Rourke, Sarah Silverman and a few mid - low level Hollywood types.

Asbhy is another coming of age story about a young man (Ed) having to make it in a world that he seems ill equipped for.

After his narcissistic parents get divorced in Oregon, his mother (played by Sarah Silverman) moves her son Ed (the 17 year old suffering from teen angst) to Virginia where his the new guy at school.

Ed is a nerd, but also as it turns out, is a jock.

He quickly becomes an outcast at his school. Meets a girl at school who is a little weird (she has an MRI machine in her basement) and they develop an angst ridden uncomfortable relationship that is has become 100% predictable in today's formulaic "coming of age teen angst movies".

Of course, not surprisingly, Ed has a neighbor (Mickey Rourke) named Ashby who is dying of a brain "something" (we never know what is wrong with his brain) and only has a few months to live. He tells Ed that he is a napkin salesmen, but it turns out that he is really a CIA assassin who has killed 95 targets (people).

Ed knows nothing of Ashby being terminally ill till later of course when the formulaic timeline says it should be revealed….thank goodness the (sorta) girlfriend has an MRI machine in her basement to confirm the assassin Ashby's story.

Ed and Ashby have a few adventures mostly involving (insert formulaic adventures in here) wherein Ashby reveals life's truths to Ed, one of which is that Ed is coward.

Ed denies that he is a coward even though he won't catch passes from the team QB that require him to take a hit (oh yeah…..remember it turns out that he is a jock too and the fastest guy on the team). That is another part of this disjointed story that is increases the "boring and stupid" factor even more.

Does this sound exciting so far? No, you say. Well there's a reason for that. It's because the movie was HORRENDOUS.

Here's a few tidbits that I'll mention. Please note that this is presented in a disjointed manner (like this entire movie review) for a reason….the entire movie, the entire plot line, the character development the story development is just a bunch of random clips put together by a director/editor who may well have been never seen an actual movie before.

Anyway…here you go…a few tidbits from the "plot":

Ashby finds out that the last person he assassinated was ordered to be killed so that his "bosses/compatriots" could make a bunch of money. Asbhy does not like this because he thought that all his kills were justified (remember he's a CIA assassin) because they were enemies of the US. Of course, this sends Ashby on the warpath to kill his former "compatriots" in the most boring and ridiculous manner possible.

Since there is something wrong the Ashby's brain (he's dying of….something), he has Ed drive him around to his "compatriots" houses so he can kill them. Of course, Ed doesn't realize this until the formulaic plot timeline dictates it's time for Ed to know.

And just as one would expect, Ed finds out and reacts in the most ridiculous manner possible that defies all logic and reason.

Ashby teaches Ed to fight when he finds out that Ed doesn't stand up for his "sorta" girlfriend.

When Ed scores the winning touchdown, he is carried off the field and one of the slutty bimbo blondes has sex with him. His "sorta" girlfriend pretends to be upset by this (maybe she was…but the acting was bad, so it's hard to tell the difference). Ashby teaches that Ed that he shouldn't just apologize, but make amends (whatever that means).

The "sorta" girlfriend takes him back when Ed sweeps her off her feet with a "teen angst formulaic speech that no teenager in history has ever delivered."

If all that (and other things I won't bore you with) aren't enough, the movie co-starred Sarah Silverman as Ed's mom.

Silverman played the role she was born to play: A vulgar slut who has no self respect or sense of decorum when it comes to sexual exploits in the presence of her son.

Even though Ed is upset by his mother's slut-hood, he still loves her and is far wiser than she (and let's face it, according to Hollywood, what child isn't smarter and wiser than their parents).

In modern Hollywood, all parents are morons…

Well….Except for Ashby (remember, he is the very forgettable and unlikable "anti-hero" of the story), as he is a wise, but flawed man, just trying to undo all the bad he's done (he was an assassin for the CIA and only killed the bad guys) so that he can go to heaven and be with his daughter (who he wasn't there for when she overdoses on pills because she was a troubled teen girl who needed her absent father to be there for her) and his wife who died a few years later (we never learn how or why she died).

Well, good 'ole Ashby kills two of the three compatriots who had him kill the innocent guy for money. When Ed finds out that he's been acting as the getaway driver for Ashby's assassinations, Ed makes Ashby promise not to kill the 3rd compatriots. Asbhy agrees not to kill the third compatriot (and actually keeps his word.)

I won't say what this results in, but you don't have to be rocket surgeon to figure it out (remember, Ashby now has less than a couple of weeks to live anyway), but let's just say that they (the producers/writers/directors) try to make it a beautiful scenic experience in an outdoor setting to which Ashby willingly goes with the assassins sent by the third compatriot (who Asbhy spared) to kill Ashby…..oh heck, now look what I've done. I've spoiled the plot.

Oh well, it doesn't matter. The movie is so bad that you'd have to have (something) wrong with your brain to go see this movie.

Oh yeah, one last thing, did I mention that Sarah Silverman's character is an unlikable, vile, vulgar, slut who should be ridiculed and ostracized by the entire female community (and any self respecting men as well).

Do NOT under any circumstances go see this movie. It has not a single redeeming quality and not one moment that is believable or even slightly entertaining.

It is vulgar and vile and Hollywood should be ashamed of itself for green-lighting a movie this awful.

No actor, Mickey Rourke included, did their careers any good by appearing in this claptrap.

Stay Away!

Jan

8

Epic Shareholder Value Destruction: Royal Dutch Shell / BG Deal, from anonymous

January 8, 2016 | Leave a Comment

On January 27, shareholders of Royal Dutch Shell will vote on the company's plan to buy BG Group PLC (the upstream remnant of Margret Thatcher's privatized British Gas).

On January 27, shareholders of Royal Dutch Shell will vote on the company's plan to buy BG Group PLC (the upstream remnant of Margret Thatcher's privatized British Gas).

If you are a merger arbitrageur, you are praying that the RDS shareholders will shoot themselves and vote yes, as the deal spread is very wide.

If you are a shareholder in RDS and have carefully studied the assets, forward prices, and assumptions, you have concluded that this deal is likely to be remembered among the largest destructions of shareholder value in the history of the world. I reached this conclusion several weeks ago. Today, Standard Life, RDS' 11th largest shareholder concluded the same thing and said they will vote "no."

Perhaps if you are the analyst at Institutional Shareholder Services (ISS) who recommended that shareholders vote in favor of the deal, you might be assured of a future job at Goldman Sachs, JP Morgan or Rothschilds after the deal closes — as the investment banking success fees will likely be extraordinary.

But — where are the activists? They can easily and rightly point out that there are numerous other assets around the world that RDS can buy at much better prices ; with a better risk/reward…

THIS DEAL IS EERILY REMINISCENT OF BANK OF AMERICA'S KEN LEWIS BUYING MERRILL LYNCH DURING THE FINANCIAL CRISIS OF 2008. The day that this RDS deal closes, billions of RDS equity will be destroyed.

Are we witnessing the downside of billions of dollars of passive index money blindly following the ISS pied piper over a cliff?

Carder Dimitroff writes:

This deal is complicated. Most shareholders lack enough information to form an opinion. While I'm on record as being concerned about the liquefied natural gas industry as an investment, I have no opinion on this deal.

This deal is about BG and RDS's natural gas portfolios and forward values of any combination. To know future values requires a full understanding of their book of contracts, their hedges and their speculative accounts. It also requires the analyst to be certain about future market conditions.

Here's what I know:

1) By definition, liquefied natural gas is an international commodity. There are few to zero domestic markets for this commodity.

2) RDS will likely become the <production> cost leader in Western Pacific's liquefied natural gas markets.