Jun

29

Article of the Day, from Victor Niederhoffer

June 29, 2015 | 3 Comments

One found this article one of the most revealing I've read in sociology:

Gary Phillips writes:

I've been on the road for the last 8 weeks or so, traveling the eastern seaboard with my wife and 3 of our 6 (call it a partial fill). While I had envisioned a trip worthy of Kerouac or even Kuralt, the eventual reality presented was much more griswoldian. Nevertheless, traveling by car does allow one greater freedom, the opportunity to experience extraordinary scenery, and the ability to capture the charm of small towns and the inherent individuality of its people. It also allows one to step back in time to a place where the only cracks visible are in the sidewalks, and not above the baggy trousers worn by rapper wannabes. And, it serves to remind us of the civility that once was part of the rich heritage of this great nation.

One used to receive a hearty "you're welcome" or "it was my pleasure" when one expressed gratitude. The contemporary response appears to be "no problem", as if your social counterparty was doing you a favor. I once believed the ubiquitous sense of entitlement and 'increasing narcissism" I encountered was and primarily contained among the members of generation z, but was disheartened to discover the casual disregard of manners crossed generational, regional, and cultural boundaries. This phenomenon has been summarily rationalized as the result of the internet's effect on the way people communicate. And indeed, social media may have conditioned individuals to be expert parsers of language, meaning, and authorial intent. Perhaps the brevity of discourse does not allow for a subtext of manners and humility. But is it really anybody's fault? "For a flow system to persist in time (to survive) it must evolve in such a way that it provides easier and easier access to the currents that flow through it". According to constructal theory, a written language evolves to "connect" better to the masses. If the elements that constitute a language are complicated, the language will take too long to write and will be more difficult to remember, and global resistance will increase. On the other hand, if the language elements are too simple, the users of the language will lack precision. The meaning of words will be misconstrued. The natural evolution of written language, then, must head for a balance between the complicated and the simple, and twitter seems to fit the bill. And as with the case with language, technological advances in information technology have caused markets to quickly adapt to anomalies and present traders with less and less opportunities. Nevertheless, one may still find an oasis of civility here and there if one looks hard enough and lucky enough, and the same can still be said for trading opportunities.

Jun

29

My IRA Performance and Libertarian Blogs, from Ed Stewart

June 29, 2015 | 1 Comment

I just computed the compound annual return of my IRA for the last six years, which is the period over which I have had it. I made what might be an interesting finding. Perhaps it is just chance, but I doubt it. When I stopped reading libertarian blogs about half-way through the period (3 years ago), my returns from that point forward increased by about 10% yr vs. the average of the prior three years. I was definitely not buying the regular staple of small cap, money losing miners headed towards zero that libertarian sites tend to recommend, but I do think it colored my perceptions in a negative way.

I just computed the compound annual return of my IRA for the last six years, which is the period over which I have had it. I made what might be an interesting finding. Perhaps it is just chance, but I doubt it. When I stopped reading libertarian blogs about half-way through the period (3 years ago), my returns from that point forward increased by about 10% yr vs. the average of the prior three years. I was definitely not buying the regular staple of small cap, money losing miners headed towards zero that libertarian sites tend to recommend, but I do think it colored my perceptions in a negative way.

anonymous writes:

Do libertarian blogs really recommend microcap miners? That sounds like more of a goldbug site. Just want to make sure us libertarian kooks aren't being lumped in unfairly with the goldbugs.

Ed Stewart comments:

There is a lot of overlap, at least on certain sites.

Jun

29

I Just Computed, from Victor Niederhoffer

June 29, 2015 | Leave a Comment

I just computed the rate of return of the web mistress's account at Scott. She doesn't know what the p/e is or the balance sheet although she is very smart and she can climb a pole and make more money per hour than most. In any case, it's about 50 percentage points a year higher than mine, (one almost runs into the problem that idiot savants from academia run into where they can't compute a negative p/e and fail to note that an e/p solves the problems but that would denude their results). In any case she had a few 20 baggers, including Netflix and Tesla, Facebook, and Disney. You might think that it's because of a meaningless low denominator, but we're talking 7 figures. One is tempted to stop trading, give all one's meager funds to Toria, and with the underpluss, see if I can negotiate the Medallion fee down to less than 50%.

I just computed the rate of return of the web mistress's account at Scott. She doesn't know what the p/e is or the balance sheet although she is very smart and she can climb a pole and make more money per hour than most. In any case, it's about 50 percentage points a year higher than mine, (one almost runs into the problem that idiot savants from academia run into where they can't compute a negative p/e and fail to note that an e/p solves the problems but that would denude their results). In any case she had a few 20 baggers, including Netflix and Tesla, Facebook, and Disney. You might think that it's because of a meaningless low denominator, but we're talking 7 figures. One is tempted to stop trading, give all one's meager funds to Toria, and with the underpluss, see if I can negotiate the Medallion fee down to less than 50%.

Jun

26

I don't think history carries a tune, has any lyrics or rhymes, and it most certainly has no moral/political lessons–i.e. the proletariat will triumph. History is always and everywhere just a story about what people did, and one either enjoys stories or one doesn't. The problem with the schoolie versions of history is that they are always fictions with a purpose; the writer reliably distorts, ignores, lies about the known facts of what happened to fit everything to their version of a dialectic. It may not be Marx's but it always has the same presumption of inevitability. They may be "conservatives" like Carlyle or modern day liberals like David McCullough, but either way you end up with a sermon that the writer already knew he wanted to preach. (What makes Gibbon, the historian most often used for lessons in the 19th century, fascinating is that he keeps ignoring the lesson he has in mind in favor of finding the next twist in the truthful narrative. The story wins out over the moral/political lesson.)

I don't think history carries a tune, has any lyrics or rhymes, and it most certainly has no moral/political lessons–i.e. the proletariat will triumph. History is always and everywhere just a story about what people did, and one either enjoys stories or one doesn't. The problem with the schoolie versions of history is that they are always fictions with a purpose; the writer reliably distorts, ignores, lies about the known facts of what happened to fit everything to their version of a dialectic. It may not be Marx's but it always has the same presumption of inevitability. They may be "conservatives" like Carlyle or modern day liberals like David McCullough, but either way you end up with a sermon that the writer already knew he wanted to preach. (What makes Gibbon, the historian most often used for lessons in the 19th century, fascinating is that he keeps ignoring the lesson he has in mind in favor of finding the next twist in the truthful narrative. The story wins out over the moral/political lesson.)

This nattering is my apology for offering a historical comparison that today's anniversary brings to mind. On this date, in 1924, the U.S. Marines finally left the Dominican Republic (they had been there since 1916).

The United States has had thirty years of filibustering (not Senators talking but the other kind–adventuring with guns) in the Middle East. Nearly twice that long if you take away most of the guns and leave only the CIA and the American oil companies. By the time the Marines left Dominica, the filibustering in the Caribbean/Central America had been going on for almost a century, if you start with the Texas War of Independence. To this day the importance of all that chasing after sugar, tropical fruit and petroleum gets largely ignored, except by the Zinnistas who use it as yet another proof of the fundamental evil of the United States of America.

I have no doubt that the saga of Texans and others chasing Saudi/Iranian oil will be equally ignored when it comes to understanding what happened to America after Bush I became President. One can only hope that some day the Marines will go home once and for all.

Jun

26

The Swing Dance Season, from Victor Niederhoffer

June 26, 2015 | Leave a Comment

We're in the swing dance season where anything good for the republicans will be bullish for the stock market, (of course long term bearish for the individualist idea that has gone with the wind), but thank the Good One for the Supremes helping the Republicans by upholding the hateful law that has caused all so much misery, extra expense, and waiting endlessly in line, and filling out paper work rather than seeing your Dr.

We're in the swing dance season where anything good for the republicans will be bullish for the stock market, (of course long term bearish for the individualist idea that has gone with the wind), but thank the Good One for the Supremes helping the Republicans by upholding the hateful law that has caused all so much misery, extra expense, and waiting endlessly in line, and filling out paper work rather than seeing your Dr.

anonymous writes:

Anything that brings clarity to the level of corruption at the top such as important words being clearly interpreted incorrectly in full public view is long term positive. This counteracts the much more common gradual and deliberate shifting of those meanings to the point where everyone accepts them to be very different from what they were a few decades ago. This was an "emperor does have clothes because he clearly meant air to be considered clothes" moment.

anonymous writes:

Every presidential cycle I break out Fear and Loathing on the Campaign Trail '72 by Hunter S. Thompson. It's like a checklist of how the campaign plays out. Plus, it's really funny. I'll start reading it soon once we know who is really running.

It was "the least factual, most accurate account" of the election, according to Frank Mankiewicz, Mr. McGovern's campaign manager.

I'm a big believer is in Hunter's and others' maxim that the truth is never told between 9-5 and this book just expounds on that.

Jun

26

Kurtosis, from anonymous

June 26, 2015 | 1 Comment

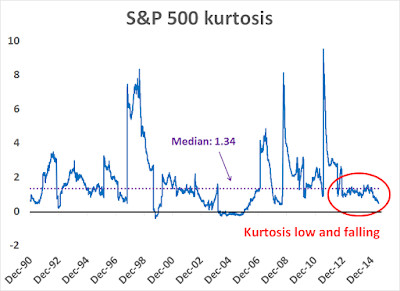

Here is a thought provoking chart that made its way to me this morning. Much in the literature talks about different distribution selection dependant upon the existence or otherwise of 'excess Kurtosis' inter alia. (k = 3 for normal distribution). Much online about this interesting measure. Debatable though if the higher moments are useful in the trenches– as it were.

Here is a thought provoking chart that made its way to me this morning. Much in the literature talks about different distribution selection dependant upon the existence or otherwise of 'excess Kurtosis' inter alia. (k = 3 for normal distribution). Much online about this interesting measure. Debatable though if the higher moments are useful in the trenches– as it were.

Good weekend all.

P.S. Aliens have landed. No, not really, however - in news that has a similar probability of observation - London is set to have a run of two (YES, TWO!) consecutive days where the sky will actually be visible through brief partings of the oppressive, grey clouds . There have even been rumours on the internet that the temperature may scale the heady heights of 25 degrees centigrade. Like the perfect game, that last point may be an event too remote without divine (or at least Flexionic) intervention.

Steve Ellison comments:

In the past year, I did some research on kurtosis to inquire whether there might be any predictive implications when the price change part way through a period of interest was in the "narrow shoulder" of the distribution.

Jun

25

Rentech Secrets Revealed, from Vic Niederhoffer

June 25, 2015 | 5 Comments

"James Simons Interview- Numberphile"

"James Simons Interview- Numberphile"

He changed his profession because of the St. Louis distributor.

Charles Pennington explains:

A helpful colleague alerted me that the business about the "St. Louis distributor" starts around minute 44:00. Short story is that Simons found himself the owner of a computer company of some sort in St. Louis, then was faced with having to have meetings with the "distributor from St. Louis", which he finds distasteful.

Stefan Martinek writes:

Some interesting parts:

28:30: "Trend is an anomaly in data"

29:30: "There are no elaborate equations, some sophisticated math in the area of the last part – how to min. volatility of the whole"

It would be great to see a track record and run it against some benchmarks.

Paul Marino writes:

Thanks for the video, Rocky.

Is it bullish or bearish that he wasn't chain smoking cigarettes throughout? Has he quit? I find it fascinating how people smoke when it doesn't compute with their life like doctors, firefighters, billionaires.

Anatoly Veltman writes:

It seemed half-way through Jim pulled something out of front pocket, and then (I speculate) came an editorial cut. Is your query due to personal experience? I, for one, wouldn't ask that on this site, although I was awestruck with the same thing in this clip.

I had the good fortune to sit on Jim's right shoulder during a five-hour (you immediately know it was ethnic Russian household) lunch. I was so uncomfortable because I haven't had one puff in 30 years so I asked, "Jim, I thought American males didn't smoke?" Jim didn't take more than two seconds to repartee: "you know, you're right on the whole, but the lower classes still do". Later he was less apologetic: "I just enjoy cigarettes too much to stop". I'm a little dumbfounded in this clip Jim credited his dad with bankrolling his investment debut. Can someone pinpoint the minute Jim commented on Madoff? I missed the sound bite.

Paul Marino writes:

I had heard that he was a chain smoker for decades, still smoked as of last summer.

Not trying to demoralize him, I smoked for years myself, it is a tough habit to break, but in New York you're surprised by the type of smoker as I had mentioned earlier plus the city's war on tobacco, sugar, etc. At $13 a pack I guess you need to be a billionaire or doctor to afford to smoke these days here.

anonymous writes:

You could always tell when Simons was at a math department tea by the smell of cigarette smoke. No Smoking allowed in university buildings, but who is going to tell that to the guy who built the place?

Jun

25

Technology Adoption, from Shane James

June 25, 2015 | Leave a Comment

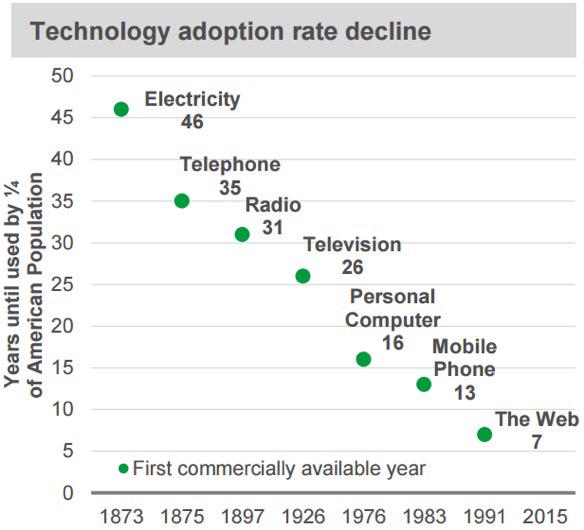

This chart attempts to characterize the decline in the technology adoption rate in the United States. (I.e quicker adoption of new technologies). One gathers there were many accuracy issues that the researches came up against but still, the negative correlation is likely a reasonable supposition. It does lead one to ponder if some type of 'technological singularity' approaches wherein some interface between carbon based life and 'technology' leads to almost automatic adoption of new technologies. Perhaps in some not too distant future we will approach the asymtote–as it were.

This chart attempts to characterize the decline in the technology adoption rate in the United States. (I.e quicker adoption of new technologies). One gathers there were many accuracy issues that the researches came up against but still, the negative correlation is likely a reasonable supposition. It does lead one to ponder if some type of 'technological singularity' approaches wherein some interface between carbon based life and 'technology' leads to almost automatic adoption of new technologies. Perhaps in some not too distant future we will approach the asymtote–as it were.

The more luddite interpretation might be that humanity may begin to rebel against technological adoption as the 'improvements' become increasingly marginal.

We shall see.

anonymous writes:

An alternative explanation is technology diffusion, in which the diffusion time is inversely correlated with the ability to communicate the innovation.

Alston Mabry writes:

The first thing I think of is how each technology laid the foundation for and accelerated the adoption of the next. Electricity took a long time because there were no wires to begin with.

Jun

25

The Next Debt-Based Crisis May Not Be in the US or the EU, from David Lillienfeld

June 25, 2015 | Leave a Comment

Will China liquidate its holdings of US debt to pay for the recovery?

Will China liquidate its holdings of US debt to pay for the recovery?

"BLACKROCK WARNS: China's debt has lost its potency and is now 'turning into poison'"

Jordan Low asks:

What would they do with the US dollar? Convert it back to RMB and hurt Chinese exporters?

Rudy Hauser writes:

To get rid of dollars they could import goods and services, make investments dominated in other currencies or buy other currencies. They could just invest in other U.S. investment possibilities (including equities, real estate, etc.) In the aggregate the only way foreigners can get rid of U.S. dollars is to buy goods and services. They can also make fixed investments, but the returns and proceeds upon sale would be in U.S. dollars, so they would not really have reduced their dollar holdings. They can of course make investments in the U.S. that decline in value. (They could also convert to currency and burn it, but that is not a logical choice.) An other alternative is to give the dollars to Americans as a gift, another unlikely choice. Yes, the Chinese could buy RMB for dollars if they find someone who has RMB to sell. To the extent Americans hold RMB that they would sell for US dollars, the gross positions would change but not the net positions.

Jun

25

Will Someone Explain, from Victor Niederhoffer

June 25, 2015 | Leave a Comment

Will someone explain to me why news of Greece no deal is bullish for bonds, i.e what it has to do with the long term rate of inflation? And why news of a deal is bearish for bonds? Also while at it, why no deal is bearish for stocks and deal is bullish?

Will someone explain to me why news of Greece no deal is bullish for bonds, i.e what it has to do with the long term rate of inflation? And why news of a deal is bearish for bonds? Also while at it, why no deal is bearish for stocks and deal is bullish?

John Floyd writes:

A market pundit might say (not a personal explanation): "if there is no deal in Greece that is bad for Europe and the ECB will have to do more QE and buy European bonds to get confidence up, growth up, and inflation up, that would be bearish for the Euro, the uncertainty around no deal is bad for stocks in the short term." On the next contradictory headline you can expect the mirror image response.

Alston Mabry writes:

From the cheap seats: no deal for Greece, or even Grexit, means a mini-catastrophe, where lots of players will be looking to get out of certain positions and move to safety until the smoke clears and we find out if a Greek exit actually raises the possibility of Portugal or Spain leaving, too. So in this case, Treasuries = safety.

John Floyd writes:

As I sit and watch the headlines on Greece I can't help but recall similar headlines and market reactions prior to the Russian default on August 17, 1998. Hopefully I have learned at least one thing since then. While not financially ruinous, and actually profitable in many ways, it was amongst other things a tiresome and loathsome experience getting up at 1 a.m. NY time to watch the latest headlines and developments.

The first lesson would be to attempt to recognize an untenable position from a macro economic and geopolitical standpoint in the medium to long term. A corollary is to not position investments with the thesis that an untenable position will be resolved in the short term and provide profits.

The wolf of the markets will at some point overpower such a short term view. The PIGS in the periphery perhaps might have their houses and building materials tested further. The wolf will have to be careful though as the cauldron waits in a house and may try and stymy speculative avenues.

Jeff Rollert writes:

In a "normal" world, a large debtor defaulting forces participants via systematic transmission to add Treasuries/AAA bonds to portfolios to return to the prior risk/reward or VAR state for a window of time until asset recovery levels become apparent.

Jun

25

I recently picked up Make: The Annotated Build-It-Yourself Science Laboratory: Build Over 200 Pieces of Science Equipment! to work on some science project ideas with my 7 year old daughter.

I recently picked up Make: The Annotated Build-It-Yourself Science Laboratory: Build Over 200 Pieces of Science Equipment! to work on some science project ideas with my 7 year old daughter.

It was originally published back in 1963 when chemistry sets came with cool stuff that could hurt or maim the unwary. It has been revived and annotated by someone I have a lot of admiration for over at Evil Mad Scientist, Windell H. Oskay. He has done his best to modernize it with annotations, especially in the area of suggesting modern day ingredient equivalents or where to get some now harder to find chemicals.

It's a fantastic book that provides instructions on building out a home lab, while at the same time providing a ton of experimental questions to consider.

Anyways, I would definitely recommend checking it out. Here's an official blurb:

Raymond E. Barrett's Build-It-Yourself Science Laboratory is a classic book that took on an audacious task: to show young readers in the 1960s how to build a complete working science lab for chemistry, biology, and physics–and how to perform experiments with those tools. The experiments in this book are fearless and bold by today's standards–any number of the experiments might never be mentioned in a modern book for young readers! Yet, many from previous generations fondly remember how we as a society used to embrace scientific learning.

This new version of Barrett's book has been updated for today's world with annotations and updates from Windell Oskay of Evil Mad Scientist Laboratories, including extensive notes about modern safety practices, suggestions on where to find the parts you need, and tips for building upon Barrett's ideas with modern technology. With this book, you'll be ready to take on your own scientific explorations at school, work, or home.

Jun

24

Greece, from anonymous

June 24, 2015 | Leave a Comment

I don't know whether to laugh or cry.

EUR drops 200 yesterday on nothing and TODAY Greek PM Tsipras tells the media that the creditors have not accepted the latest raft of proposals.

It is an outstanding example of flexionism. Or more charitably an efficient market discounting mechanism (yeah, sure!).

One decides that laughter should carry the day in this instance.

Jun

24

Today was one of those days where you are both exhilarated and exhausted. The wife had trouble sleeping last night. When that happens, she tosses and turns all night. Her restlessness made it impossible for me to fall asleep. So I was awake until sometime after 2 am and up at 7 am.

Today was one of those days where you are both exhilarated and exhausted. The wife had trouble sleeping last night. When that happens, she tosses and turns all night. Her restlessness made it impossible for me to fall asleep. So I was awake until sometime after 2 am and up at 7 am.

So this may be a short report as there is a deck chair with my name on it and I am experiencing a serious "nap attack".

First a personal observation: We took a bus tour today. Although the tour guide was very knowledgeable, his grasp of the English language was not that great. And maybe we were spoiled in Gibraltar with a tour guide who went out his way to make everything interesting and personal, but that was not the case today. We often couldn't hear our guide because we were in crowd of 40 people. Couple that with other tours, and the noise was just too much.

If I do this again, I'm going to look into hiring a personal tour guide to show us around.

The history of Cartagena is fascinating. We were told that "he who controls Cartagena, controls the Mediterranean.

It is a very strategically located port and that is easy to defend due to it's shape. The father (?) of Hannibal had a wall built around the city that became known as the Punic Wall. It was thought to be a great defense system that would protect the city. When coupled with the shape and location of the harbor, the city was thought to be a very safe place to be (which turned out not to be the case).

The geological wealth of the city, especially in the form of the silver mines grew the wealth of to fantastic proportions.

The wealthy of the city chipped in and built the great Roman Theater of Cartagena. It was very cool touring the theater and learning of it's history and architecture. It was amazing to me that the theater was lost from history until discovered by archeological digs in the 1980s.

They've been able to recreate most of the theater using (they say) 70% of the original materials and building blocks.

We toured the city streets of the area, walked into a small Catholic Church and took pictures of the statues. I'll try and post some of the pictures later.

The Punic Wall was very nice to see. We were told that we stood at the same place that Hannibal gathered his army to march across the Alps. Supposedly, 90,000 men and 100 Elephants.

Of course, while Hannibal was trekking to Rome, The Roman's used that as an opportunity to attack Cartagena (it was called by another name then…I don't recall what it was). The Romans conquered Cartagena. Hannibal was absent.

Not the best military maneuver on the part of Hannibal.

A few personal notes:

Try not to have elbow surgery a few days before you go on a trip. it limits your ability to do stuff.

I had an infected bursa sac and had to have some minor outpatient surgery. Apparently, there is an international law that says if you see Scott, you must find a way to bump his elbow.

There is a basketball court on the ship. So I went out to shot a few free throws. There are maybe 3 or 4 other people on the court shooting around. As I stand on the free throw line getting ready to see if I can go 5 for 5 from the line, SLAM, a ball crashed into my left elbow. Not my knee, not my back, not my butt, my freaking elbow. Of all the places the ball could have gone on that court, it hit me on the elbow.

The kid apologized hitting me in the elbow. I accepted his apology (he certainly didn't do it on purpose…at least I think he didn't ![]() and decided to try some other activity.

and decided to try some other activity.

I tried to get a ping pong game going, but the tables were all full. So I came back to the room. My 16 year old, Hunter was sitting at his desk working on something. I asked him what he was doing, he said, "chemistry".

He set a goal of doing at least a little bit of chemistry or physics or anatomy study on the ship each day in preparation for his AP courses in those classes.

It warmed my heart!

Well, it's off the flow rider to watch the kids ride the boogey boards.

Take care, my friends!

Jun

23

Interesting Take on the CAPM as it Pertains to Mutual Funds, from Paul Marino

June 23, 2015 | Leave a Comment

I was looking at this interesting take on the CAPM as it pertains to mutual funds from Stanford University over the weekend. They used mutual funds for their study but I found it promising that they use a fund's fee changes in the study.

I was looking at this interesting take on the CAPM as it pertains to mutual funds from Stanford University over the weekend. They used mutual funds for their study but I found it promising that they use a fund's fee changes in the study.

"Assessing Asset Pricing Models Using Revealed Preference"

We propose a new way of testing the validity of an asset pricing model. Instead of following the common practice in the literature which relies on moment conditions related to returns, we use mutual fund capital flow data. Our study is motivated by revealed preference theory: if the asset pricing model under consideration correctly prices risk, then investors must be using it, and must be allocating their money based on that risk model. Consistent with this theory, we find that investors' capital flows in and out of mutual funds does reliably distinguish between asset pricing models. We find that the CAPM outperforms all extensions to model, which implies, given our current level of knowledge, that it is the best method to use to compute the cost of capital of an investment opportunity. Perhaps the most important implication of our paper is that it highlights the usefulness and power of mutual fund data when addressing general asset pricing questions. Mutual fund data provides insights into questions that stock market data cannot. Because the market for mutual funds equilibrates through capital flows instead of prices we can directly observe investors' investment decisions. That allows us to infer their risk preferences from their actions. The observability of these choices and what this implies for investor preferences has remained largely unexplored in the literature.

Jun

23

Suez Doubles Down, from Stefan Jovanovich

June 23, 2015 | 1 Comment

"Widened Suez Canal to Open in August"

"Widened Suez Canal to Open in August"

This is the first significant expansion of the canal's carrying capacity in its 145 year history.

Paolo Pezzutti writes:

The Panama Canal is also expanding. The size of ships has increased. They need important changes also to port infrastructure.

"The Panama Canal expansion project (also called the Third Set of Locks Project) is intended to double the capacity of the Panama Canal by 2016 by creating a new lane of traffic and allowing more and larger ships to transit."

anonymous writes:

This latest development is positive for Israeli stocks. The project was underwritten by Egyptian citizens and they are making a bet on the absence of events that will threaten the revenue from the widened canal like and Egyptian attack on Israel or a nuclear bomb exploding in the region. And the fact the Sisi's government decided to undertake it and declared it "military led" is a concrete (no pun intended) sign that their rhetoric of being business-oriented (as opposed to say oriented to destroy Israel).

anonymous writes:

Egypt is a military dictatorship, as such there is of course no "free will" exercised by "the people" of Egypt, but it's certainly a polity. Usually when a dictatorship wants to create an investment by someone other than the core clique it has two choices: coercion or guarantees of repayment of questionable quality. After all, they can change their mind at any time and all the guarantees will be gone with the wind. So observing a non-coercive investment process in a dictatorship is useful to estimate the confidence in the dictatorship by either foreign or local investors. Often large foreign investors have substantially more leverage since they can threaten a military or political retaliation via their own government. In this case, Egyptian citizens, of their own free will, trusted the military to repay them by buying the investment certificates that sold faster than expected. While this is certainly no example of Western property rights, this means that some relatively savvy citizens in a very impoverished country (thus no money to waste) trust their leaders. This is a useful datapoint in evaluating investment and other stability-related prospects in that part of the world.

Gordon Haave writes:

What everyone is missing because (per our discussion last week) the watch and read US propaganda media is that last week the Deputy Crown Prince of Saudi Arabia, The Saudi defense minister, the Saudi foreign minister, and more importantly the Saudi Oil Minister met in Russia and inked 6 new deals including defense, nuclear, and energy deals with a goal towards a "petroleum alliance".

But hey, an Al Jazeera columnist was once quoted as saying something he shouldn't have 15 years ago, so by all means keep reading US media.

Gary Rogan writes:

Gordon, as the likely target of the last comment, let me respond. While this bit of news from All Jazz TV is valuable in it's own right (and most certainly no propaganda) and is likely to have major worldwide implication from the war in Syria, to Russia supplying Iran, to Israel, to the Saudi relationship with the US, the price of oil, Egypt, and more specifically Suez Canal, it is unlikely to have had an impact on why the Suez canal project was started many months ago. If it did, the world is even more convoluted than I could ever imagine.

Jun

23

Wealth Has Causes, from Don Boudreaux

June 23, 2015 | Leave a Comment

Necessary conditions are not necessarily sufficient conditions.

Necessary conditions are not necessarily sufficient conditions.

………………………………..

22 June 2015

Editor, The Washington Post

Dear Editor:

Robert Samuelson correctly notes that CEO pay over the past three decades has become tied more closely to the value of share prices and that CEO pay today is generally higher than it was thirty years ago ("The CEO backlash," June 22). But crediting only lower inflation and interest rates, Mr. Samuelson errs in asserting that "CEOs had nothing to do with this" rise in the overall real value of shares - and, hence, "nothing to do" with the increase in their pay.

While improved monetary and fiscal policies are unquestionably boons (to everyone, and not just to CEOs), companies never manage themselves. Weak leadership, failures to anticipate changing consumer demands, imprudent decisions to expand, and hosts of other executive errors lower a company's market value - and often hurl it into bankruptcy - even under ideal monetary and fiscal conditions. Likewise, sound monetary and fiscal policies do not themselves spontaneously generate iPads, Amazon.com, Facebook, fracking, and the uncountable other goods and services that greatly improve our lives: these things - and the all-important means of making them widely available at affordable prices - require entrepreneurial vision, risk-taking, and hard work. Entrepreneurship, successful management, and wealth creation are not bundles of manna that rain down upon a land if only it is blessed with prudent central bankers and parsimonious budget officials.

Evidence of the continuing importance of the scarce resource 'executive talent' is found in research done by Steven Kaplan and Joshua Rauh. These economists find that (quoting Kaplan) "Analyzing some 1,700 firms, we found that compensation was highly related to performance: the companies that paid their CEOs the most saw their stocks do the best, and those that paid the least saw their stocks do the worst."* This conclusion makes sense to everyone who understands that there is nothing routine about starting and managing successful businesses, and that wealth requires for its creation active and on-going human imagination, enterprise, and effort.

Sincerely, Donald J. Boudreaux Professor of Economics and Martha and Nelson Getchell Chair for the Study of Free Market Capitalism at the Mercatus Center George Mason University Fairfax, VA 22030

* Steven N. Kaplan, "The Real Story Behind Executive Pay," Foreign Affairs, May/June 2013

Jun

23

It’s Too Late For That, from anonymous

June 23, 2015 | Leave a Comment

I wonder if there is a point in time at which it becomes too late (unprofitable) to go against in markets. This is clearly under a time bound, like the day, the week, the month etc.

I wonder if there is a point in time at which it becomes too late (unprofitable) to go against in markets. This is clearly under a time bound, like the day, the week, the month etc.

This needs to be analysed in two frameworks. Firstly, the road to some form of answer is different between 'bounded' futures markets and markets that trade in the fashion of spot currency markets whose short term higher number central moments are often very extreme.

Secondly, my work indicates that the 'answer' is not linear. It will not be a specific time of day. The proponents of the arc-sine work have some measure of empirical evidence on their side for the close as the best guess, but it is a blunt tool in this context.

A fascinating case study is the EURUSD spot market today- down almost every hour since London midnight with the total move of relevant statistical 'weight'.

In other words, you should study if a specific time and magnitude combination negates subsequent reversal strategies for the time period under consideration (regardless of the strategy's historical efficacy).

I'm starting to sweat as the EUR declines as I have a bet with an exceptional trader in the spec list that the EURUSD will trade its 1-1-15 level again before the end of the year. The prize is steak and lobster at The Palm in New York.

Jun

23

Day 2 and 3 of My Cruise, from Scott Brooks

June 23, 2015 | 1 Comment

It's like having a traveling hotel room that follows you around so there's no packing and unpacking. I'd prefer not to do the tours and experience the local "feel" on my own. But with a wife and 4 kids and the need to be back at the cruise ship on time being the paramount concern, we're stuck with tours for now. One nice thing about the tours is that they (supposedly) guarantee that they'll get you back to the boat on time or the cruise line is on the hook to get you back to the boat. I don't know if that's true, but Gwen seems to think it is.

It's like having a traveling hotel room that follows you around so there's no packing and unpacking. I'd prefer not to do the tours and experience the local "feel" on my own. But with a wife and 4 kids and the need to be back at the cruise ship on time being the paramount concern, we're stuck with tours for now. One nice thing about the tours is that they (supposedly) guarantee that they'll get you back to the boat on time or the cruise line is on the hook to get you back to the boat. I don't know if that's true, but Gwen seems to think it is.

And anyway, I'm not as adventurous as our world traveler Prof. Haave (although he did give me some great tips before I left for this trip.

Anyway, we're going to take a taxi tour of Gibraltor tomorrow and going to see the apes (I had no idea there are apes at Gibraltor).

So hopefully I'll have some moderately interesting tidbits to share with the group tomorrow.

It's now 0:45 am (that's the way they talk on the ship), so I'm off to bed so we can wake up at 08:00, eat breakfast at 09:00 and meet at the Royale theater for our tour group at 10:00.

Goodnight, Mateys!

Day 3: Gilbratar

Before, I get to Gibraltor, I need to give some color on the evening of the second day at sea.

First of all, I met an interesting couple. He works for an oil company, formerly Shell, but it was sold to middle eastern interest (a company owned by two brother….the name of which escapes me).

He gave me a breakdown of use of oil in cruise ships. Apparently, the oil used on ships is the "bottom of the barrel" stuff that would be used as tar if cruise lines didn't buy it.

It is very much like thick sludge and requires a lot of heat to make it function as a fuel. It is also not very emissions friendly…but supposedly, there are no emissions standards out on the open sea.

To top off our evening, we watched a comedian and a game show.

The comedian was Grunway Thom. He was British, but we could understand most of what he said. I enjoy a good comedian. Thom was better than good. He was enjoyable. He made us laugh without getting dirty. No obscenities, but he did have the occasional double entendre. He was a juggling a comedian. I don't know whether he was a great juggler or just an ok juggler, but I have to say that the best parts of the show were when he messed up his juggling act. He engaged the audience and involved those that chose to get up and go to the bathroom during his performance.

But the best part of his act was when people came in late and he would show them what they missed…and he would reenact 30 minutes of show in about 2 minutes.

If you ever get a chance to see this gentleman perform, please take the time out of your day to watch him. It was a true pleasure to watch a skilled professional ply out his trade.

After the comedy show, we stayed and watched the "Love and Marriage" show. Here they invite 4 married couples up from the audience and then quiz them very similar to the way Bob Eubanks did on the "Newly Wed Show".

Our kids desperately wanted Gwen and to volunteer to get up on the stage, but alas, there was no way we were going up there. Gwen had seen the show on other cruise ships before and knew what kind of questions we were going to be asked.

There is no way I'm gonna give an answer to, "Where is the strangest place you made whoopee" in front of my kids (BTW the best answer of the evening was given by a couple who had been married for 51 years. They made whoopee in a corn field while her mother slept in the car).

So on to day 3: Gibraltar.

First of all, I believe I made an error in one of my earlier posts when I mentioned that Gibraltar was part of Spain. If one were to look at a map, it would be easy to think that. However, Gibraltar is a UK overseas territory.

If you've never visited Gibraltar it is worth your time too see. The history of this vital piece of real estate is utterly fascinating. I would go so far as to say (apologies in advance to Stefan if he were to say to my forthcoming comment is hyperbole) that this piece of land is one of the most important pieces of land in the history of the world especially as it pertains to war and diplomatic relations between countries, especially England, Spain, and France.

The culture of Gibraltar is rich and diverse with European and African influences as well as Christian and Muslim influences with a bit of Jewish history mixed in.

Up to and even thru WWll, Gibraltar was (is) a strategic piece real estate. From Gibraltar you can guard and control the entire entrance to the Mediterranean. As a matter of fact, you can see Africa from here. There are even guns, dating back into the 1700's (maybe even earlier than that) that could shot all the way to Africa from the heights of Gibraltar.

During WWll, Eisenhower had a runway built so planes could take off and land. It is an interesting airport in that a street (yes a public street) crosses the runway. Let's just say that it's one of those red lights that you do NOT want to run. We crossed over the runway in a taxi (with a green light…..and little trepidation).

I believe the airport was built as a part of "Operation Torch", which (IIRC) was one of the first actions of the US military in WWll. (Stefan, jump in an feel free to clear up any of my historical inaccuracies).

We then drove thru the town of Gibraltar. It is a town of heavy English influence. English is the main language, but I heard a lot of Spanish speaking people. We drove right up the Spanish border and turned around.

The streets were very narrow and very much like you see in the movies. Although there were traffic law, stop lights and speed limits, it almost seemed that people kind of had an understanding about when they could go and not go. It would have been nerve racking for me to drive, but the taxi driver seemed very much at ease driving and giving us a verbal tour of the town and it's history.

Although we paid him for this specific purpose, I have to give him full props for a job well done. The cruise ship said that a tip was already built into the fee we paid for the tour, but when he dropped us off, I gave him an additional $50 (USD) tip on top of it. I don't know if that was too little or too much, but he seemed very pleased…and so were we.

Gibraltar is a growing town…but they only have one way to grow…out into the sea. So they continue to build and build and build further and further in to the bay, the Straits and the Med. We drove along "The Wall(s)" which were built at various times throughout history for defensive purposes…but the walls used to be where the sea was…and now the sea was about 1/4 to 1/2 mile away, driven back by the work and engineering of men!

We drove up the mountain (if you can call it that) nearly to the top of Gibraltar. Along the way, we stopped at some caves that were to be used for hospitals and other strategic war time activities during WWll.

Another interesting aspect of Gibraltar is that most of the online gambling in the world takes place out of Gibraltar. According to our taxi driver, most of the big buildings that we passed were owned by online gambling companies.

I tried to get a feel for how easy or difficult it might be to move to or become a citizen of a place like Gibraltar (not that I'm leaving the comfort of my home in STL), but I couldn't get a clear understanding of it from our taxi driver…I think the question was too much off the beaten path for him.

But he did talk about how safe of a place Gibraltar is. Very low crime. He said that if you tried to steal a car of a motorbike, there was no place to go with it. It was hard to cross the border with a stolen vehicle.

While on top of Gibraltar the driver pointed out other little cities that had sprung up over the years. There was one city called "The Line" (it had a Spanish name but I don't recall what it was).

The Line was set up because it became extremely hard for people to live in Gibraltar because it was becoming crowded. So they wouldn't allow people that didn't already live there to live there…..but they still needed workers. So this town, just over into Spain was set up to house these "less than desirable, but needed workers".

Then there was another town (it's name escapes me) that was set up because those that didn't convert to Christianity (a long time ago) were expelled as well. So they went a few miles over into Spain and set up their own town and life went on.

There was a 15 year period from 1969 - 1984 where it was very difficult, if not impossible for a citizen from Gibraltar to travel into Spain. Everything was cut off by Spain because Gibraltar refused to "reunite" with Spain.

Apparently, Gibraltar had a election about reuniting with Spain the election came out something like 1000 No's to 14 yes's. That apparently aggravated Franco, so he shut out the Gibraltar's from access to Spain.

That lasted until Spain applied for membership in the EU. There was a treaty with Britain and the borders opened.

Here's an unexpected anomalously for you (at least it was too me)….did you know that there are MONKEYS on Gibraltar? I was shocked to learn that myself.

And they are all over the Rock. As we drove up, we ran into more and more monkeys…..they were everywhere. The weren't Ape like, they were much smaller even than chimpanzees.

Here is what they looked like.

Here is what they looked like.

We were told not to feed them and not to approach them especially if they had babies. However that didn't stop other tourist from feeding them. One tourist had a bag of potato chips, when out of nowhere this monkey (with a baby on her belly) ran up and snatched the bag away. The tourist tried to get the bag back, but (as you may have already guessed), the monkey was having none of that.

Here's a hard fast rule that might (loosely) have some trading applications: If a monkey has your bag of potato chips and doesn't want to give it back to you, there is NOTHING you can do get those chips back.

So Rule #1: If you don't want to lose your chips, don't reveal to monkeys that you have chips…..if they know you have chips, they will get your chips.

They have a feeding pit for the monkeys up on the Rock. We visited the pit and all that was there was a very big monkey (big my Gibraltar standards), sitting there, in a pile of fruit and vegetables, spread legged looking like he'd stuffed himself to the point of discomfort.

As a side note: He was obviously a male monkey.

Apparently, someone behind my 18 year old daughter opened up a bag of chips (please note rule #1 above) and the monkey made a beeline for the chips.

Unfortunately, my innocent daughter Abbey was between the monkey and it's chips.

Rule #2: Do NOT get between a monkey and potato chips.

As far as the Monkey was concerned, my daughter was just a prop in it's stealthy ninja like plan to get his hand on those chips.

He ran up to my daughter grabbed her shirt, pulled himself in close to her (I'm guessing to conceal himself form the person holding the chips), then he swung around her, using her clothing (and skin) as a swing to sling shot himself after the person with the chips.

When the monkey got up close to my daughter, she didn't know what do to, she just kinda froze (because it was the biggest monkey we had seen so far), When it drew itself close, my daughters eyes got as big as saucers (keep in mind, that all of this happening in mere seconds).

But when the monkey sling shot himself around my daughter, she let out a yelp (not really a scream….because she didn't want to scare the monkey) and when she felt his grip come loose, he she took off running hearing nothing but screams behind her.

Whether the monkey got those chips or not is a mystery to us……we were all freaked out by the unexpected monkey attack……but we did keep moving on, hoping to find more friendlier monkeys further up the road.

When we got back to the cruise ship, I sat on one of the upper decks eating a chocolate/strawberry ice cream cone looking out over the Bay of Gibraltar watching all the barges and boats dump rock into the water building new places that would likely become docks or maybe house a hotel or apartment complex someday.

As I sat there, I reflected on all the strife and turmoil that surrounded this strategic piece of land over the years. All the countries that coveted it (and still covet it), it's strategic importance as a military base and the economics this land.

They are under British rule (I hope that's the right phrase), but they do not pay taxes to the Brits. As a matter of fact, they pay very low taxes here (at least that's what I was told).

With the advent of the modern air forces around the world, I'm not sure that Gibraltar holds the same strategic military influence that it once held, but then again, I could be wrong.

Much of the worlds oil has to pass thru the waters between Gibraltar and Morroco, and I would guess that he who controls Gibraltar and the Suez Canal controls much of the worlds oil supply. According to our cab driver, Hitler wanted to gain control over the Suez and Gibraltar (again, I'll defer to Stefan on this if it needs adjustment or elaboration).

Regardless of it's strategic importance it is a place worth your time to visit.

The beauty of the old world, the history and the excitement of new construction makes it a must see for any trader, historian or sightseer.

That's all for now.

Take care, my friends!

Jun

22

I haven't read this story because it's in the Times, but it would seem that with all the centrals and internationals hovering about with all their flexionicism in play, and the US backing them, (the agrarian chair from Brooklyn stated there is a contagion effect) to signal where we stand, that somehow a few billion of emoluments will be found, printed, or funded.

"Dealbook: As Deadline Looms, European Central Bank Plays Key Role in Greek Crisis"

Jun

22

I like the part of The Boys in the Boat where the freshman coach pretends that Cal can beat them handily. The necks of Cal swell even further making it even for Washington to cut them off. I followed the same principle in squash, and never admitted that I had a chance to win. I also never admit to a profit in the market for the same reason. It will be interesting to hear what Mr. Rafter has to say about The Boys in the Boat because he has won many national rowing championships. In particular the wisdom and ability of George Peacock, the world's best boat builder, whose materials in wood have now gone with the wind.

I like the part of The Boys in the Boat where the freshman coach pretends that Cal can beat them handily. The necks of Cal swell even further making it even for Washington to cut them off. I followed the same principle in squash, and never admitted that I had a chance to win. I also never admit to a profit in the market for the same reason. It will be interesting to hear what Mr. Rafter has to say about The Boys in the Boat because he has won many national rowing championships. In particular the wisdom and ability of George Peacock, the world's best boat builder, whose materials in wood have now gone with the wind.

David Lillienfeld writes:

The beauty and terror of baseball is that there is no clock; and the second you stop thinking about the next pitch, you are on the way to losing no matter how big a lead you have. What made last year's 7th game so good is that neither team ever once lost that focus; the game score was as close as one can be, but neither team ever for a moment got "tight" thinking about the end result before play was over.

Alston Mabry writes:

Yes, in games like basketball or football or soccer, you can work the clock. But baseball and tennis have that exciting element of the game not being over until it's over.

anonymous writes:

I have had the pleasure of seeing some true greats in action over extended periods of time in the markets. The only time these guys really lost any money was when they ignored time.

A fixed clock on any speculation in the organized macro markets is vital in my opinion and experience.

Unlike most things we discuss, the addition of fixed clocks (or predetermined holding periods for individual speculations) is actually countable and its efficacy is testable.

Jun

22

Ratios, from Carder Dimitroff

June 22, 2015 | Leave a Comment

From my limited experience, assessing equity from balance sheet information can be a non-trivial exercise. An issue is the company's assets. Specifically, what are those assets? How were they acquired? What was the accounting treatment?

I've been involved in situations where companies debated the merits of expensing capital costs and capitalizing expenses. Accountants tend to see this question as a black and white issue. Financial officers tend see it as a strategic issue.

The issue frequently arises in project finance. In particular, long-term capital improvement projects tend to finish with complex cost structures. In my experience, capitalized costs can represent half expenses and half assets (bricks and sticks). Some of those expenses include officer salaries, professional fees, corporate allocations and other distributables. In the end, retirement accounts prorate those costs according to the strategic need of the parent company. Once the accountants retire the plant (that is, allocate final costs across company retirement accounts), the asset capex strategy is locked in.

The issue also appears in operations and maintenance. Sometimes replacing expensive equipment is expensed. Sometimes it is capitalized. Often, there is a combination. Again, accountants tend to see this as a black and white issue. Financing, legal and regulatory people understand it as a strategic issue.

The issue pops up in special cases. It is common for utilities to create regulatory assets out of expenses. They do this with the knowledge and approval of their respective state regulators.

I've found the accounting of assets is not consistent within the utility industry. Policies change over time and by geography. They change as economic conditions change. They also change as corporate administrations change.

Finally, there are the subsequent issues of asset depreciation and mark-to-market values. While depreciation appears simple, it is not. How depreciation schedules are developed and used is complex and difficult [impossible] for third parties to analyze. In addition, the depreciated value of the asset is often uncorrelated to the asset's mark-to-market value.

For me, assets can be fuzzy numbers. Any analysis using asset values as a critical component can also be fuzzy.

Ed Stewart writes:

All good points Carder.

Another issue is when a company clearly has very valuable intangible assets that are almost completely unrepresented on the balance sheet. Consider Nathan's Famous, best known for its flagship hotdog restaurant and sponsorship of the eating contest. They build on top of that brand value to create a licensing business. Last year (ending march 31) they did 18M of this business, which is almost pure pre-tax profit as they just get a % of sales, renting the brand to a manufacturer/distributor. Capitalize that at a reasonable rate (licensing revenue streams usually valued at a premium) u see it is worth quite a bit of money. Yet, on the balance sheet intangible assets is only something like 1.4M, which is absurd from an economic perspective.

Stefan Jovanovich writes:

Accounting was developed to catch internal fraud; the whole point of double-entry was that it required two different people to keep track of every transaction. As long as enterprises were family businesses, single-entry worked just fine (as, for example, in the Rothschilds' books well into the 19th century). In that sense, all "book" numbers will be maddeningly disappointing in terms of their economic logic.

Rocky Humbert writes:

S-man makes an excellent point. To wit, some of my worst investments have been in insurance company stocks that were trading at significant discounts to their stated tangible book value. What seems to happen (with annoying regularity) is that the company "discovers" that they under-reserved for claims and they write-off massive amounts of tangible equity — leaving the stock at a premium to book value. Hence I view a substantial discount to book value as a warning sign of impending bad news rather than a blue plate special. Mr. Market may go through bipolar episodes, but he's quite astute most of the time.

Ed Stewart writes:

Ive seen another situation beyond unforeseen markdowns that can cause trouble for an investor looking at book value to find undervaluation. The issue occurs when an investor marks book value assets "to market" and finds a supposedly huge undervaluation. The first problem I have seen is that it is very easy for a bad or even mediocre business with a good asset to somehow encumber or use that asset in a way that is not helpful to shareholders - feeding a lousy "growth initiative" or simply mortgaging an asset to fund continued operations. It's amazing how many "value bloggers" write about truly crappy, sketchy businesses because they think they spot this type of situation.

In the case where the business is decent, that by no means the business is going to realize the value of the asset over any reasonable time frame, which means that the value must be discounted far off into the future. So far and so uncertain it might be impossible to assign much value to it at all. In this second case, it might add some positive option value to a decent business that is otherwise worth considering, nothing more. My conclusion is that without an activist situation or change of heart by the CEO or some similar circumstance, undervalued assets are not always what they are cracked up to be.

Gary Rogan comments:

A bet on undervalued assets IS a bet on an activist situation and/or if not "change of heart by he CEO" change of the CEO. Undervalued assets will not of course suddenly start performing by themselves. That's why "undervalued" cash on the books or undervalued assets combined with a substantial cash flow are so much better than an "undervalued" steel plant or similar: cash is easy to understand and reuse and attracts activists, acquirers, and CEO replacement.

Andrew Goodwin writes:

Not sure why the talk on ratios attracted so much interest. In a group that favors scientific modeling, why no thoughts on finding the significance of each industry valuation ratio through regression studies?

Charles Pennington writes:

Stefan, what's your definition of "soft jobs"? Do you have an opinion about which companies out there are wasting their money on "soft jobs" and which are acting more wisely?

Stefan Jovanovich replies:

This is a feeble answer to your question, Charles, but it is all I have. Cantillon wrote that nations got into trouble when their tastes for what he called "luxury" outran their capacities to make enough money to pay for them in foreign trade. He was not a mercantilist, but he thought that nations had to accept the verdict of the foreign exchange market when it went against them. They could not use "Chinese paper" (Singleton's phrase for puffed-up securities) when their counter-parties expected coin. As Cantillon put it, nations cannot use use finance as a substitute for commerce and they cannot indefinitely leverage their credit so that rich men's wives could continue buying more lace. For at least some of the time, even the wealthy have to endure being less rich until trade once again comes into something approaching balance.

It seems to me that many, many companies are now like Cantillon's luxurious nation. David's drug companies are one set. Their profits are projected to continue to grow enormously even as the savings and earnings of the hospitals and governments and individual paying customers have stagnated and even begun to fall again. The drug companies' happy futures are based on the assumption that the centrally-banked remedies to the world's savings "glut" can somehow be transmuted into continuing demand without anyone having to endure even temporary insolvency. There is no arguing that the plan has worked up to now (cue John Hussman's explanations of why he has missed the last 5+ years). But, as the Orioles and other clubs regularly demonstrate, the last innings can be very rough even when the guys coming in from the bullpen have had such sterling records.

P.S. Ignore all monetary puns; this is not a recommendation to buy gold.

Jun

22

Mediterranean Cruise Day 1: At Sea, from Scott Brooks

June 22, 2015 | Leave a Comment

David got home from his two year church mission on June 10th and is off to BYU-Idaho in the fall. Abbey has graduated high school is embarking on her life journey.

David got home from his two year church mission on June 10th and is off to BYU-Idaho in the fall. Abbey has graduated high school is embarking on her life journey.

Hunter is off on his mission next year after he graduates. Lydia will still be home for a few more years.

We figured this would possibly be our last chance as a nuclear family to go vacation together. So I surprised everyone with a few months ago by announcing that we're taking a 2 week Mediterranean cruise.

First of all travel.

The St. Louis airport is kind of rat hole. Very old and drab.

We flew out of STL to Toronto on a small plane via Air Canada. The plane was cramped and uncomfortable. On top of that, it was hot. VERY HOT. They kept turning the air vents off. Not a very good flight except I sat next to a nice women (the family was not able to sit together for this part of the journey).

We arrived in Toronto late Friday evening and it was like stepping into another dimension. The airport was modern and comfortable and looked alive. I was very impressed. The only down side was the bathrooms. They were not very clean. But outside of that, it was a delight to wait in the Toronto airport.

We then boarded the Air Canada flight to London Healthrow. It was a big plan, but not huge. seats were 3 3 3 in coach. I was going to upgrade to business class, but with a family of 6, it was a bit pricey for my lower middle class frugal south St. Louis upbringing to swallow.

So I settled for upgrading to exit row seats for the boys (the girls got regular seats and did just fine).

I have to say it was nice being able to stretch my legs out. Also, having the head rests that have the sides that close in and hold your head stable were nice too. The seats were a bit hard and the only thing that kept me from getting more sleep on flight was the fact that my butt kept waking me up from the hard seat.

The stewardesses were really nice and a bit more international than we're used to in the states. But it was pretty interesting talking to people of such diverse backgrounds.

I managed to get around 3 - 4 hours of broken sleep on the plane, so I felt pretty good when we arrived in London.

A few observations about the flights.

1. The bathing habits of some passengers left a lot to be desired.

2. The parenting habits of some passengers left a lot to be desired. There was this one baby that cried and fussed all night on the plane. It turns out, he wasn't a baby, but a toddler. The reason that I learned this is because the crying would get closer and closer, then further and further away as the parents let the screaming crying fussing child run around the plane while they did NOTHING to stop the child.

Luckily, the child was far enough away so that it never got too bad for me where I was sitting. If I had been sitting closer to the child, I'm sure I would have done something or said something to the parents. I can guarantee you that I would I have made sure the parents were awake the whole time if they insisted on letting their kid run around screaming and fussing. Yes, believe it or not, the parents were actually sleeping most of the time all this was going on. (I went back and checked as I was looking to give the parents either assistance or a very dirty look…or even a few words of "encouragement").

Once we landed in Heathrow, we disembarked into a modern looking airport and friendly staff.

The wait for customs was a bit longer than I expected. But it wasn't bad.

Once out, we found our cruise line and loaded up. They said it was an hour to 90 minutes to get to South Hampton. It was a bit over 2 hours and it was, by far, the worst part of the travel day..sitting on a cramped bus with a bunch of exhausted people who hadn't bathed or brushed their teeth in at least 24 hours wasn't too terribly bad. The worst part was the fact that the exhaustion of not getting enough sleep in the last 24 hours was really setting in.

However, even through all of that, nothing was going to take away from the excitement of taking my family on this wonderful trip.

Once on the ship, we decided as a family that we were going to stay awake till a normal time, get a good nights sleep and be on local time to fight off jet lag. We were pretty successful in our endeavor to stay awake….until we ate dinner. As we sat there eating, we made plans for what we were going to do all evening. The kids wanted to do the flowrider, Gwen and I talked about a show…a few of the wanted to "yonder" (a family word for exploring the ship and wandering around)…all good ideas…until we got our belly's full.

As dinner progressed and our belly's got full, all we could think of was the blissful release of sleep.

By the end of dinner, Gwen and I gave up on the plans to go out that evening, and headed back to our stateroom. We figured we'd sit on the balcony and watch the stars and waves go by. The kids decided to "yonder" a bit, but only lasted about an hour (at least that's what Gwen told me…because I didn't even make it onto the balcony.

I slept from 9 pm till 7 pm the next morning…the most I've slept since college…and it felt great. One more good nights sleep and I think I'll be good to go.

In the meantime, I'm gonna relax, get a massage and maybe take in a show with the wife.

One more day at sea and then we hit Gibraltar.

We hit ports in Spain, France, Portugal, Italy and England. I think two ports in each country. I'll update the list as to observations as I am able.

Bon Voyage for now, I'll check back later!

Day 1:

Day 1:

We left Southhampton, went through the English Channel and then into the Sea of Biscayne.

Made friends with random people at meals. Sat with a couple from Wales. He works in IT with Unilever, I don't recall what she did. They talked about how Brits get much more "Holiday" than we American's do…at least 6 weeks.

They also gave me a breakdown of the UK and what was ok to call someone from the UK. Being from Wales, it was perfectly ok to call them English or even British (though they preferred English). Apparently, the Scot's and the Irish do not think of themselves as English and can be offended if you refer to them as such. They are, apparently, a fiercely independent lot.

We met a small group from the Isle of Wight at our Muster Station. Very pleasant group who went out of their way show a little kindness to us (letting us out ahead of the crowd as they were in wheel chairs and/or blind…so they got first shot at the exit area…and let us go ahead).

For dinner, we met a couple from Manchester who were very talkative and interesting. She was a retired postal worker and he was a semi-retired "weight station operator" who had his own business verifying the scales at weigh stations on the highways.

The couple from Manchester were very interested in asking us questions about our children and America. They wanted to understand the gun culture of America. They had both grown up in the day's prior to the prohibition on guns and remember having guns in their household.

Their impression of America from the MSM was that it was a semi-wild west with shootings all the time. Of course they suspected that it wasn't that way at all as they had been to America a few times and never saw a single gun while they were here.

The variety of people on this ship is amazing. One might expect such multiculturalism from the crew (and they are), but the passengers are from all over the world. And the best news is that most of them seem to speak at least a little English. We've no problems communicating with anyone…well…almost…

It takes a while to pick up on the accents. Even when speaking with someone we share a common language with, I'm finding that it really takes concentration on my part to sift through some of the thicker accents. Couple that with strange phrasing and colloquial words, and it can be a bit of a task at times picking up on the message that is being communicated.

Makes me wish I had watched more Monty Python or Fawlty Towers when I was younger.

Well, it's after 1 am here, so I'm gonna call it night and try and report more tomorrow. Hopefully, I'll be able to have some financial conversations about local economies to report on soon.

Chris Tucker writes:

One reason youngsters tend to scream aboard aircraft is failure of their inner ears to equalize to the pressure change. Typically, when cruising in an aircraft above 28,000 ft, the cabin is pressurized to about 10,000 ft. above MSL. This is why your ears pop when climbing or descending. If you have a cold or any inflammation in the sinuses or inner ear, then some cavity within might have some air from sea level pressure that can't escape, creating blinding pain in the skull. An old trick to remedy this, quite effective, is "hot cups". Many older flight attendants will instantly know what you mean if you ask. They will take two small paper or foam coffee cups, stuff a napkin in the bottom, soak it with boiling water and then place them over each ear. It will frequently (not always), provide some relief.

Jun

22

Big Investors and Front Running, from anoymous

June 22, 2015 | Leave a Comment

Oeyvind Schanke runs Norges Bank Investment Management in Oslo. They own about 1.3 % of the global equity market apparently.

Oeyvind Schanke runs Norges Bank Investment Management in Oslo. They own about 1.3 % of the global equity market apparently.

The Singapore business news carried an interesting quote from him:

"We could choose to wait four days before we execute in the hope that during the course of these four days we will find a natural counterparty to cross this up with".

The article was bemoaning high frequency front running. Of note is that the comment made by Mr. Schanke is eminently testable. They believe that opportunity costs are less than getting stuffed by front running.

What is the question they have asked? Likely something resembling:

Given an expected high frequency rip off factor on our execution, how many days (or some other time period) is it best to wait that allows us to benefit from the normal variability of the market in question.

Jun

22

Risk-Factor Compensation for Active Managers: Pay for Alpha, Don’t Overpay for Beta, from John Netto

June 22, 2015 | 2 Comments

Two weeks ago in Chicago I presented the anchor leg of three different presentations on How to Identify and What to Pay for True Alpha.

Jason Roney of Bluegrass Capital Management and Marat Molyboga of Efficient Capital preceded me. Marat brought forth a very impressive presentation on assessing if manager skill actually exists and Jason showed how despite having a lower sharpe ratios, understanding a managers "regime robustness" is critical when making an allocation.

I concluded by presenting an incentive structure which one may use after they believe they have found an active manager worthy of investing in. My idea is "Risk-Factor Compensation". It's meant to be a very simple way to contextualize the profits a manager generates against not only the volatility the account had, but how much predetermined risk said investor was willing to lose. The resulting ratio then corresponds to a chart which tells what percentage incentive fee the manager is entitled to given their "Netto Number".

The bottom line is the current compensation structure of 20 percent of all profits without having a mechanism to contextualize how the return relative to drawdown or how much actual risk capital was at stake is woefully inadequate. I will post the link to the video when Terrappinn makes it available.

Given the sophistication of this group, I would like to hear anyone's comments on either the current 2 and 20 pay structure in hedge funds or my idea to have a score which balances out the focus between both the numerator and denominator as right now the only thing which matters when a manager gets paid is the numerator.

Here is the formula:

Profits / (Risk Budget + max negative drawdown/2)

So if someone made 400k and they had a risk budget of 800k and max negative drawdown of 400k then it would look like this

400k/ 600k

Which would equal .66. A Netto Number of .66 equals a 13 percent incentive fee, or 52k for the manager vs the traditional 20 percent of all profits, which would be 80k. So the investor saves about 28k in fees based on a lower Netto Number.

Now if the manager makes 1 mm and the denominators are constant then he has a Netto Number of 1.66 and now earns 32 percent of profits or 320k. But either way the investor wins because in order for a manger to get paid that the investor receives a SUPERIOR risk-adjusted return on a net basis.

I can email anyone privately the complete presentation upon request.

Jun

20

Sports Psychology and Trading, from Sushant Buttan

June 20, 2015 | Leave a Comment

As I continue on my arduous journey for selecting and also constantly keeping traders at their A-game, I was wondering if Vic, Brett or others on the list have any experience with how Sports Psychology could be used with Traders.

As I continue on my arduous journey for selecting and also constantly keeping traders at their A-game, I was wondering if Vic, Brett or others on the list have any experience with how Sports Psychology could be used with Traders.

A competing athlete goes through pretty much the same psychological challenges that a trader goes through…and I was wondering if any research had been done on this subject.

Mental training helps athletes perform more consistently, find the zone more often, keep a winning streak alive, and learn how to think well under pressure. Or, as one sports psychologist put it, mental toughness is "the ability to consistently perform toward the upper range of your talent and skill regardless of competitive circumstances." As psychologists debate the roles of genetics, environment, and learned skills in determining mental toughness, they do agree (along with athletes and coaches) that high levels of mental toughness are associated with athletic prowess and success. In fact, mental toughness (or "grit") may be the defining factor between finishing at the front of the pack and not finishing at all.

Any thoughts from Specs would be welcome.

Victor Niederhoffer writes: