May

29

According to my Data, from Anatoly Veltman

May 29, 2015 | 1 Comment

The thesis of this article is that with the increased volume you have an algo driven "pump up" during the last minutes of the day.

According to the data I have that is not the case.

Since 1 Jan 2012 closing the trade at 1600 you can see the results below:

Buy at 1520 49% up 0 pts t -42

1530 48% up -0.1 pts t -120

1540 46% up -0.2 pts t -270

1550 45% up -0.1 pts t -208

There might be other edges around the close. This is due to the index funds managing their positions and day-traders closing their trades. In some case this might create inefficiencies that a small speculator can exploit to make a decent living. Good for those who can find them. But for sure it is not what zerohedge brags about from time to time.

May

29

Superswarms, from Pitt T. Maner III

May 29, 2015 | Leave a Comment

Romance among the termites:

Romance among the termites:

1. "Two of the most destructive termite species in the world– responsible for much of the $40 billion in economic loss caused by termites annually– are now swarming simultaneously in South Florida, creating hybrid colonies that grow quickly and have the potential to migrate to other states. In an article published today in the journal PLOS ONE, a team of University of Florida entomologists has documented that the Asian and Formosan subterranean termite simultaneously produce hundreds of thousands of alates, or winged males and females. Both species have evolved separately for thousands of years, but in South Florida, they now have the opportunity to meet, mate and start new hybrid colonies."

(and here's the PLOS scientific paper)

May

28

FTSE, from anonymous

May 28, 2015 | Leave a Comment

One has developed a completely irrational 'concern' about the FTSE INDEX.

The current June Futures contract has criss-crossed the 'SuperRound' number of 7000 many, many times since first closing above it on the 10th April 2015.

In the 30 trading days since it has closed above 7000 12 times and below 7000 some 18 times. It has managed to trade 1.2% above the round and 3.2% below it in the time since the first close above.

I guess it will just go up in time in line with the drift or whatever….but something is out of order somewhere…

My apologies for the purely descriptive nature of this post.

May

28

Tortoise and the Hare, from Victor Niederhoffer

May 28, 2015 | Leave a Comment

Moves in Japan versus China which were down 7% yesterday to 30 day low recalls the story of tortoise and hare.

anonymous writes:

No need to run. You have to start on time. The story repeats itself.

May

28

Fantastic New Yorker Article on Surfing and Coming of Age, from Jeff Watson

May 28, 2015 | Leave a Comment

New Yorker staff writer William Finnegan hit one out of the park when he wrote about about moving to Hawaii as a kid. This very well written piece discussed family, middle school, friends, enemies, romance, surfing, and trying to survive as a racial minority. He did a great job of describing the culture shock felt by a white boy from affluent S. Cal, moving to a rough, working class part of Oahu.

New Yorker staff writer William Finnegan hit one out of the park when he wrote about about moving to Hawaii as a kid. This very well written piece discussed family, middle school, friends, enemies, romance, surfing, and trying to survive as a racial minority. He did a great job of describing the culture shock felt by a white boy from affluent S. Cal, moving to a rough, working class part of Oahu.

It's quite a long read, but it's well worth saving for a rainy day. Finnegan has written a few other articles about surfing for the New Yorker. In another story featuring the famous Dr. Renneker, Finnegan wrote the following description of famous surf breaks, comparing them to different composers.

Finnegan wrote:

Ocean Beach is the polar opposite of Waikiki—cold, gritty, scary, not for beginners. I find beauty in it, but an utterly different, more challenging, modernist beauty. Captain Cook, when he first saw surfing, compared its effects to those of listening to music. When I think of Waikiki, I hear early classical compositions: fugues and Bach concertos, sacred music. Being out at Ocean Beach is like surfing to Mahler. This glistening morning at Four Mile has a score by Handel. That wave in Indonesia might have been composed by Mozart. Sunset Beach is pure Beethoven. Strangely, when I think of the best wave I've ever surfed—the one breaking off an uninhabited island in Fiji—I hear no music at all.

That is some of the best surf literature, ever. Many specs, the Chair especially, like to make comparison between different kinds of music vs different kind of markets. Just as one can compare music to markets or music to surfing, a few of us compare markets to surfing. To quote Mr. Sogi San: "There are many market lessons in surfing." I agree totally and learn new ones all the time. Both of those articles contain food and nourishment, maybe not a meal for a lifetime, but certainly a hearty snack.

May

28

Churchill Downs Memories, from Anonymous

May 28, 2015 | 1 Comment

Perhaps it was a good 25, 30 years ago, Gramps and made the track to L'ville, this particular time, arriving early, for the Friday races, the Oaks — roses for the Fillies.

We had gotten there early, the first race hadn't gone off, and there was a platoon of school kids visiting Churchill (before the garish remodeling). Their teacher was a woman, and this kids couldn't have been more than 7 or 8 years old. They young buys, couldn't reach the urinals, they simply weren't tall enough.

In the days before blue M&Ms, when you would offer to do such things without fear of being accused of something, we offered to hold the youngsters up, in front of the urinal, one by one, asking each a question, "Where do you go to school?" or "What's your name," to ease the tension and so they could do what they had to do.

There must have been a dozen or so of them we each held up, and finally Gramps lifted one, who, I couldn't help but noticing, was particularly blessed.

"What grade are you in young man?" Gramps asked the little fellow he was holding suspended above the urinal.

"I'm riding Silver Spurs in the seventh, I've been outta school as long as you old man," the little man shot back, "But thanks for the lift."

May

27

Clustering of Events, from anonymous

May 27, 2015 | 3 Comments

Here is an article from the world of transport engineering. It's not too much of a stretch to apply something similar to observations and timings of magnitudes in financial markets:

Here is an article from the world of transport engineering. It's not too much of a stretch to apply something similar to observations and timings of magnitudes in financial markets:

Extract: "Why Buses Bunch at Single Stops"

Maybe you've waited at a bus stop for longer than usual, and your bus finally shows up. And then, immediately after, a second bus on the same route pulls up right behind. What gives? Why can't they stay evenly spaced to improve everyone's waiting time? Lewis Lehe provides an explanation in a small interactive game.

Two buses travel along the same route, starting off in opposite positions. They make stops and pick up passengers right on schedule. But then add in your own small delays, and you see bunching relatively quickly. It really doesn't take much to throw off the equal spacing…..'

Jim Sogi writes:

Watch the ocean for a while, or the beach. Random waves cluster to form set waves, larger than the rest, or rogue waves, which can be magnitudes greater than the average. I believe this is a function of randomness or alternately pattern formation from simple binary functions a la Wolfram.

Here's some good information about Three Phase Traffic Theory.

Jim Sogi writes:

When I go to the US Mainland and drive the big freeways for long distances, I try to drive about 2 or 3 miles per hour slower than traffic. Most try to drive as fast as they can and bump up against slower traffic groups, and results in waves of clusters of cars. It's more effort and emotional cost to try drive fast and requires more attention to try pass, notice and avoid slower cars, and cars next door. Driving a bit slower requires less attention, less stress as you set you speed, and allow other drivers to pass, avoids coming up on slower traffic, and allows you to drive in the spaces between clusters, the "lulls" so to speak. I'm not in a rush and find it more relaxing and you can see the clusters in the distance, and adjust to drive between them. In large urban areas, the clusters tend to be time of day (rush hours) and location oriented, except for accidents.

In markets, vol clusters and it's good to be aware of the lulls and clusters, the timing of them, the length of the lulls. It's like the lulls and sets in surfing. Trading also seems to cluster around the rounds, and time of day (arc sine).

In playing and composing music, it's important to leave "space" in the music, where there are fewer notes to allow emotional development.

Jonathan Bower writes:

Mr. Sogi makes some very good observations. I drive 150 miles round trip every day for work. I see people in such a rush to "slow down" when they inevitably meet slower traffic (or jam). Maintaining a high average speed is much more important in determining length of drive (and better on gas). There is also a strong behavior bias to get in the left lane that frequently staying right, particularly in heavy stop and go, is frequently and consistently optimal.

Mr. Sogi makes some very good observations. I drive 150 miles round trip every day for work. I see people in such a rush to "slow down" when they inevitably meet slower traffic (or jam). Maintaining a high average speed is much more important in determining length of drive (and better on gas). There is also a strong behavior bias to get in the left lane that frequently staying right, particularly in heavy stop and go, is frequently and consistently optimal.

Jim Wildman writes:

And mathematically, except on long, open road drives, speeding won't save you signification time even assuming you succeed in increasing your average speed.

You can't save 5 minutes on the typical 20 minute commute by speeding. You can if you are willing (and able) to run stop signs and stoplights.

I used to drive from East Texas (Longview area) into Dallas every day (about 115 miles). It was my observation that most radical speeding (10 MPH over) occurred where it would do the least good. Very few drivers speed in the truly rural areas, but once you get into the more potentially congested areas, the number of speeders goes up.

David Lillienfeld adds:

I've found that the frequency of speeding is inversely proportional to the density of police cars on the side of the road. The result is that you have lots of speeding going on on the interstates, punctuated by islands of drivers going at the stated speed limit. I don't know that the state makes much off of speeding tickets in this setting; I do know that it presents a nice the opportunity for accidents as cars slow down and then speed up. Twice, I've seen cars flip in the course of trying to avoid an accident while slowing down—once was just out of range of a radar gun.

Stefan Martinek writes:

I found that a good solution is to reverse the time zone. I had one period when I was living in the US time zone while in Europe. It is always good to avoid crowds. Gyms are also nice and empty around midnight. No clustering.

May

27

Changes, from anonymous

May 27, 2015 | Leave a Comment

I am very interested in changes in relationships between tradeable financial markets. The key words here are changes and tradeable.

Using a period of, say, three years (totally arbitrary choice I know) most relationships between tradeable assets and other tradeable assets with a lag of, say, 1 day usually present R-squared readings circa 0.00. ( maybe a -0.01 to a + 0.01 range). You might be tempted to call this random and that is probably a reasonable categorisation.

What is of interest is when seemingly out of the blue, the two tradeable assets start exhibiting a strong positive or negative relationship. So what is of interest is the 'inflection point' from 'random' to something potentially predictive.

Studying this phenomenon is truly a meal for several lifetimes. These times should be co-incident with strong periods of either trend following or countertrend performance depending on the resultant positive or negative correlation to previous moves.

What is also very true is this. The market allows these departures from 'randomness' for varying periods of time but almost always takes them back to R-squared = 0 territory again. The lifecycle of the move from a horizontal line of best fit to a positive or negative slope and back again is very interesting.

One example would be the DAX futures contract and the EUR USD spot FX rate. Now over the last few years the movement of the DAX today had little to do with yesterday's movement EURUSD. Of late (looking at the moves in a more complex fashion) the movement in the DAX today has been negatively correlated with the movement in the EURUSD yesterday.

I wonder what caused this change. The proximate reason would be the QE program of the European Central Bank and that is a reasonable assertion.

What we should look at are magnitudes, runs & durations in relationships to see if the departures from randomness and back again are predictive.

My own analysis found one of the more incredible relationships I have ever seen between a weak EUR in a previous period to a strong DAX in the next producing some 2000 DAX points in short order. In subsequent testing this has flatlined and indeed started losing.

I strongly believe that most relationships are pulled back to 'randomness' by ever changing cycles.

Here is a prediction: the easily derived DAX bullish signals from EUR weakness will revert back to a win some, lose some proposition from recent 'Rosetta Stone' significance.

I hope this example helps us clarify our thinking further on these important issues.

May

26

It is Common, from Victor Niederhoffer

May 26, 2015 | Leave a Comment

It is common in athletic events for the sagametricians to say at certain points, things like "the home team has won 87% of their games when ahead by 2 or more run in the seventh inning." Or "the bigs have gone on to win 92% of their 7 game series when they win the first two".

It is common in athletic events for the sagametricians to say at certain points, things like "the home team has won 87% of their games when ahead by 2 or more run in the seventh inning." Or "the bigs have gone on to win 92% of their 7 game series when they win the first two".

Most of these utterances are completely consistent with randomness. But the question emerges: is there a time in the market when the scales are taken out and Zeus decides whether Achilles or Hector will win the battle based on the calculations from his sexy partners or even his own volition. I would hypothesize that 1:30 pm Eastern Standard is the key hour where the scale is tipped and the market decides whether to head further up or down.

David Hillman comments:

Exactly the hour when our dear departed Ed's 'big boys' return from lunch sated by filet or dover sole and are deciding if they will dine with their sexy partners that evening at Daniel or take them to Nathan's for a full dress dog. No more testing of the hypothesis seems required.

anonymous writes:

I believe that there is much to this post from the Chair.

Much of the difference in technique required to trade different financial instruments is due to this type of error in my opinion.

These points are open to conjecture but they are certainly thought provoking:

To say something like, "every time the Dow does X then the result has been Y with such and such summary statistics over the past 100 years". Arguably it has some pitfalls in common with the sports analogy, namely, the composition of the stock index (sports team) has not been constant over the entire test period and so one may not be comparing apples with apples. This is mitigated somewhat by phenomena with a relatively larger number of occurrences.

Stretching it a little more, the LA Lakers team of Magic Johnson and Kareem AJ (wow! What an era - do you remember the playoffs against Boston in the 1980s) is different from that of today. The "Y when X" piece may continue but I think it is these type of statistics that end in Black Swan events. With AAPL being in the DOW, the index arguably has different characteristics than when when U.S. Steel ruled the show.

It is my view that analysis of the major currencies does not suffer from any of this as a JPY is a JPY is a JPY. By the same token one should consider theoretically calculated EUR data before its launch as trash and one may need to change analysis if Greece were to depart the single currency. I believe the same is true of commodity futures markets (grades, etc aside).

May

25

In Defense of Education, from Peter Grieve

May 25, 2015 | 1 Comment

Many intelligent people think that they rarely use their educations. This may be true in many fields as far as specific material goes. However, if these same people tried to function without the hard-won habits of thinking precisely about abstract ideas, of paying attention to detail even in long, uninteresting tasks, and of reading and listening carefully to presentations and instructions, they might not take their educations for granted. Even the essential habit of being on time is hard won for many (including me).

Many intelligent people think that they rarely use their educations. This may be true in many fields as far as specific material goes. However, if these same people tried to function without the hard-won habits of thinking precisely about abstract ideas, of paying attention to detail even in long, uninteresting tasks, and of reading and listening carefully to presentations and instructions, they might not take their educations for granted. Even the essential habit of being on time is hard won for many (including me).

I teach students every day who were not required to develop these skills in their elementary and secondary educations, and the result is not pretty. Innovation, or even routine technical work, is very difficult without this foundation.

Of course I realize that many of the future engineers that I teach will not use the techniques that I require them to know (partly because employers no longer trust them to have the skills above). I imagine that gymnastics coaches realize that few of their athletes have a practical need to dance on narrow beams or flip around parallel bars. But the enhanced coordination and confidence developed in the one case, and the precise thought and careful observation developed in the other are an obvious benefit to the student.

Take note of the people from other cultures who are successful in the technical world, they mostly were educated under strong forms of this regimented, restricting Prussian system. Talented and brilliant people are better able to develop these skills on their own.

May

25

A Terrible Story, from Victor Niederhoffer

May 25, 2015 | Leave a Comment

I read a terrible story about why children are abandoning baseball from Forbes based on a WSJ story of same title.

I read a terrible story about why children are abandoning baseball from Forbes based on a WSJ story of same title.

Stefan Jovanovich comments:

Baseball was never the "default" sport for young children. The ball is damn hard and a good one has always been expensive enough to be worth stealing. It was the sport for "grown-ups" that you could hope to play when you got big enough to keep up. Until then, you would play catch with your family adult (thanks, Mom) and use a tennis or rubber ball to pitch and hit with your neighbor/brother/sister, using the barn/garage for a backstop. It took years of those repetitions before you could even hope to play well enough to keep up with the men and have it actually be baseball. The game flourished in all the places where men played the sport and let children join them. That is why it still flourishes in all the places where men and their children play it together for fun– the American Southeast, the Dominican, Cuba (although that is dying), South Korea, Japan. Little League was baby-sitting and adults pretending to teach the game instead of simply showing how it is done out on the field against each other.

Paul Marino writes:

This story lends no credence to the fact that southern states play baseball year round vs more northern regional leagues and the population disparity between the two. Baseball is a regional sport on all levels, pro on down vs football and basketball which are national sports.

This story lends no credence to the fact that southern states play baseball year round vs more northern regional leagues and the population disparity between the two. Baseball is a regional sport on all levels, pro on down vs football and basketball which are national sports.

Also, this article makes no reference to global, specifically lat-am baseball which is a religion in places such as Cuba, DR, PR, etc. last I checked Puerto Rico is part of the U.S. Unless they default on their munis. Plus immigration will lead to a generalized balance in players against the author's "the Great Recession no-baby meme" which has had us all feel poor as humans since they state red the meme. I can tell you my family and friends in their 20-30s are having babies, just a little later in life.

The article would have been more relevant to US if distinguishing the lack of African Americans choosing basketball and football over baseball. White kids will always play baseball at one point or another out of love of the sport or parental pressure to do something where you can't get too hurt.

Stefan Jovanovich replies:

If Paul means that baseball is "regional" in the same sense that hunting/shooting is "regional", I agree. But the notion that "white kids" will play baseball at one point or another because of "love" or "parental pressure to do something where you can't get hurt" seems to me very far off the mark. No one in their right mind "loves" baseball; it is so relentlessly demanding that it has minute-by-minute failures. There is no room for the fantasy of "we are the champions" that football (American and world) and basketball allow. The best teams in baseball have won-loss records that would disqualify them from the Champions League or the basketball or football playoffs; and the home-away advantage is trivial (52-48%) while, in the other sports, it is nearly overwhelming. It is like chess; you either have the addiction or you don't see the point.

None of this says anything about the game's popularity as a spectator sport. People now love going to professional baseball games more than at any time in the past because: (1) compared to basketball and football ticket prices, it is still a very cheap date, (2) it is like visiting the old amusement parks like Elich Gardens - you can stuff yourself silly while walking around and you don't really have to watch the game, and (3) unlike almost all the other public spaces in American cities the parks themselves are not dumps. Coors Field in Denver, which is a delightful place to see a game even if the altitude makes the game itself seem like a parody, is the 3rd oldest baseball park in the country. Only Wrigley and Fenway are older.

Paul Marino adds:

I should clarify "love" as in the love a child has for a player and that gets them interested in playing, the other love is the kind I had where I played for 15 years and got into the minutiae of the game over time.

May

25

It is Regrettable, from Victor Niederhoffer

May 25, 2015 | Leave a Comment

It is regrettable to see Goldman forecasting $45 oil along with concomitant declines in all other commodities. And one wonders what the agenda is for such absurd forecasts and whether it is possible to make money by systematically coppering such self serving things.

It is regrettable to see Goldman forecasting $45 oil along with concomitant declines in all other commodities. And one wonders what the agenda is for such absurd forecasts and whether it is possible to make money by systematically coppering such self serving things.

Anatoly Veltman writes:

Not sure what they are seeing in other markets, but the supply side of oil remains hard to abruptly turn– thus their reasonable projection. Subdued energy price is also a politically correct position, so not much near term headwind there. But eventually, yes: absurdly low oil was always resolved via war initiative by a foreign power.

May

25

The Right Mind Set, from Craig Mee

May 25, 2015 | Leave a Comment

Amber Halliday, (Australian Olympic rower and recent stroke victim), recently said: "the mind-set that you need to become an Olympic athlete is pretty similar to the mind-set that you need to recover from serious injury or illness."

Amber Halliday, (Australian Olympic rower and recent stroke victim), recently said: "the mind-set that you need to become an Olympic athlete is pretty similar to the mind-set that you need to recover from serious injury or illness."

… or trading, applying and dedicating yourself more than the next guy.

Jim Sogi adds:

As my skier guide friend says: "pain is just weakness leaving the body."

May

25

Get a Job, from anonymous

May 25, 2015 | 2 Comments

I think it is scandalous that many of my daughter's friends think it is beneath them to work in a menial position and earn a paycheck, all while their parents both complain and enable the behavior. Many of these kids would rather spend the summer building huts in Costa Rica in the guise of "giving back" and/or taking un or under-paid internships demonstrating that you get what you pay for.

I think it is scandalous that many of my daughter's friends think it is beneath them to work in a menial position and earn a paycheck, all while their parents both complain and enable the behavior. Many of these kids would rather spend the summer building huts in Costa Rica in the guise of "giving back" and/or taking un or under-paid internships demonstrating that you get what you pay for.

My first job was as a keypunch operator for what was then known as Kelly Girl. I have no regrets. Not even a single letter. My daughter is working in a lab this summer undoubtedly exposing herself to products containing chemicals known to the State of California to cause cancer, and birth defects or other reproductive harm. And long after I'm dead and buried, and she's in Stockholm for the award presentation, she'll hopefully thank me.

Scott Brooks writes:

I completely agree with Rocky on this. I don't understand people that can't find a job or that think a job is beneath them. That is a completely load of BS.

I remember when I came home from college I went to the local strip malls and went door to door asking to speak to the manager of the establishment so that I could personally ask them if I could have a job. I went even a step further and told them that I would be the hardest working employee they had and that I would make them money.

I never had to knock on more than a few doors before I got hired. Filling out an application become an afterthought (i.e. I was hired based on the fact that I came in and asked for the job and told them the value I would bring….and they were like, "Oh, yeah….even though we've hired you, we need an application on file. Would you please fill this out").

As to today's college graduates who can't find a job or think a job is beneath them…WAKE UP AND SMELL THE COFFEE. The world is a hard place and it ain't just waitin' to hand you the job of your dreams because you graduated from college (big whup-de-do….so did 100's of thousands of other kids) and have shelf filled with participation trophies. Get out and find your job.

If you think a business person is interested in hiring you because you sent them a resume, you're nuts (hint: Your resume' is in a pile with hundreds of other resume's they received just this week).

What are you doing to differentiate yourself? What are you doing in the meantime to make money so that you can have, at the very least, the pride that comes with knowing that you can make yourself self-sufficient.

Let's say you want to get into the financial world but are finding it hard to get that job that you see in the movies where the guys sit at a desk all day, watching a computer screen making brilliant investment choices that enrich him and allows him to then go out all night for hookers and blow in a limousine.

What might you do in the meantime until a modern version of Gordon Gecko recognizes your brilliance and makes you his next Bud Fox?

Here's a plan:

Go to your local State Farm or Farmer's office. Call around to find a local Primerica or World Financial Group. Yeah, I know those companies are way beneath you. Heck, some of them even have an MLM function to them (ok, avoid the MLM one's if you want). But there are plenty of financial services companies out there that will hire you on a commission basis in exchange for having access to your warm market.

Yeah, yeah, yeah, I know this is way beneath you and you have an education and participation trophy shelf to prove that you don't have to stoop this low, but….get over yourself.

Find a job, learn how to sell, learn how to interact with people, learn how to get referrals, learn how to take your profits and pour them into other types of marketing campaigns so you can grow your business. And you can do all of this while living in your parents basement…and working out of the basement.

Eventually, you'll start making real money. Pour a chunk of that into getting an assistant and then eventually some staff and then an office.

Within 5 years you can be making 6 figures of income (not just revenues) and be on your way to bigger and better things.

The bottom line: Get up and go out and make something happen. Even if you don't like what I've suggested, get up, go out, and make something happen.

May

23

Some Hypotheses, from Victor Niederhoffer

May 23, 2015 | Leave a Comment

1. Germany is a semiconductor that expands energy in other markets in the East and West.

1. Germany is a semiconductor that expands energy in other markets in the East and West.

2. The Upside Down Man and the 100 Million Man, formerly his partner before and after Harvard, talk a much better game than they play. The more bearish they are for stocks, the more bullish it is.

3. The more the media feature startling bearish forecasts, the more bullish it is.

4. The cobweb theorem holds for all markets.

5. the low vol in the stock market during recent days can't continue because the public would not lose enough if it continues.

6. Sales growth is much less important for stocks than profit growth.

7. The agrarian reformers at the Central Banks will not allow cattle trading operatives to recede.

8. The leaks in Brussels to hedge funds were rampant and premontory. They will arabesque to other forms now that early release to the media of the transcripts has been curtailed. The good one knows how it plays out in other countries.

May

23

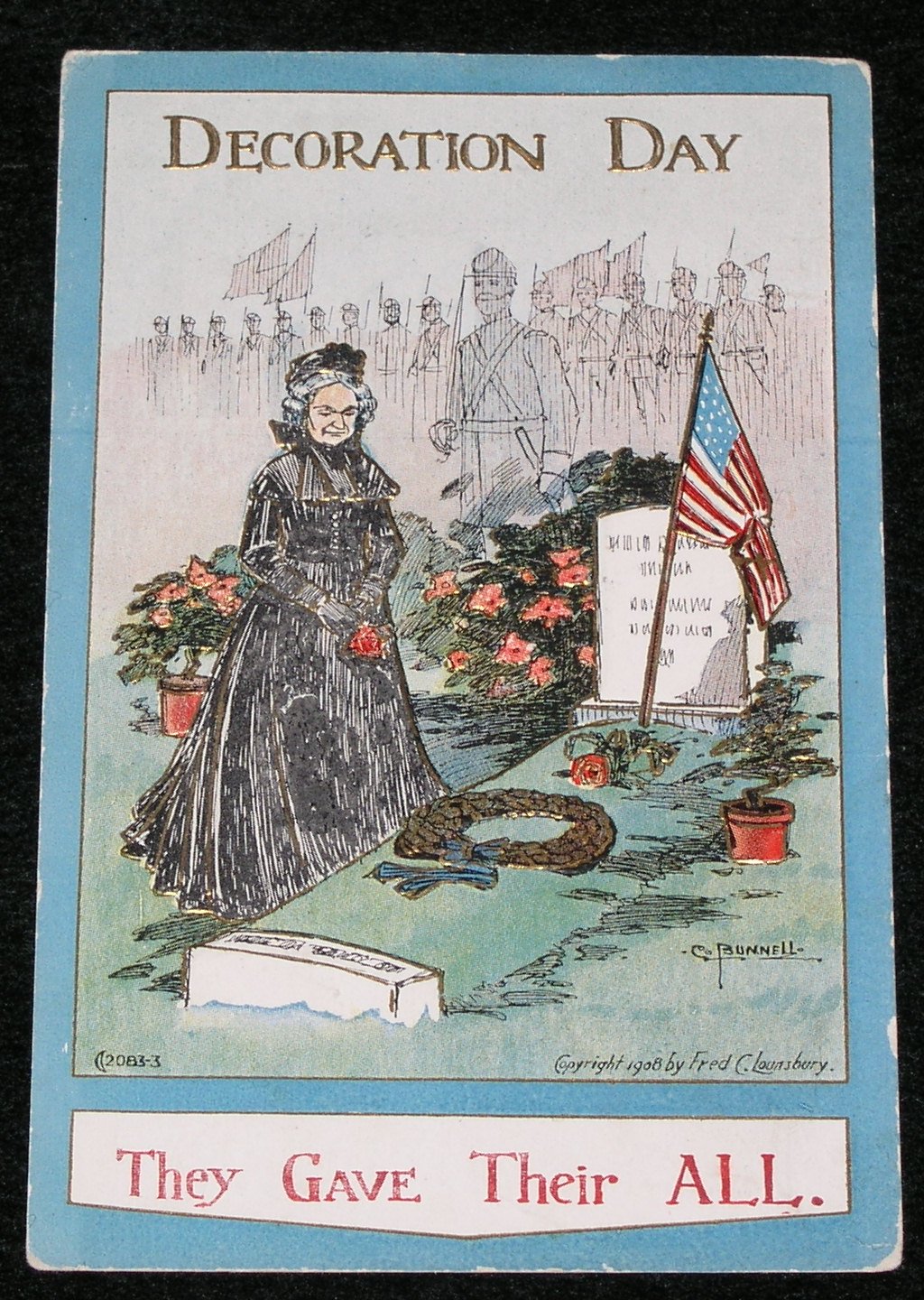

Memorial Day, from David Lillienfeld

May 23, 2015 | Leave a Comment

This coming Monday is Memorial Day. That means different things to different people. For me, it will be my mother's yahrzeit, as well as remembering those whose efforts provided the cover under which the USA lives. But it also means the running of the Indy 500. And switching to the summer comforters. For one of my neighbors, it's setting up the outside grill for the summer—which he does after visiting his brother's grave (he died in Vietnam) at the national cemetery up the road. I'm sure there are lots of similar activities at one another's homes. Some many no longer give much thought to those whose deeds provide that cover, to those who sacrifice assured that we may live under it. But they should.

This coming Monday is Memorial Day. That means different things to different people. For me, it will be my mother's yahrzeit, as well as remembering those whose efforts provided the cover under which the USA lives. But it also means the running of the Indy 500. And switching to the summer comforters. For one of my neighbors, it's setting up the outside grill for the summer—which he does after visiting his brother's grave (he died in Vietnam) at the national cemetery up the road. I'm sure there are lots of similar activities at one another's homes. Some many no longer give much thought to those whose deeds provide that cover, to those who sacrifice assured that we may live under it. But they should.

A couple of years back, Tim Melvin penned a piece that encapsulates the meaning—for at least some of us—of the day. (It will be reposted below)

It is one of the more eloquent expositions of the holiday.

Stefan Jovanovich comments:

First of all, it was not Memorial Day. It was Decoration Day; the particular day on which the public would officially do what people regularly did on their own–go to the cemetery and put flowers on the graves of the departed. And it was a Sunday, not a Monday.

First of all, it was not Memorial Day. It was Decoration Day; the particular day on which the public would officially do what people regularly did on their own–go to the cemetery and put flowers on the graves of the departed. And it was a Sunday, not a Monday.

Second of all, how does anyone presume to speak for the dead in war? That is the sickest of all sick jokes. If you are lucky/skillful enough to survive one, the one thing you know is that medals for the living are pure vanity; and Grant was–as with so many things– right: parades are only tolerable if they are parties where you throw ticker tape out the windows (ticker tape, windows?) and can make noise in praise of the living. For the dead there should only be flowers, no speeches.

FWIW, the first decoration day was on May 1, 1865 in Charleston, SC. It was held in honor of the Union soldiers who had been held and died as prisoners of war and buried in a common grave. After the Federals occupied Charleston, one of the first things they did was give each of the soldiers' remains its own individual burial and marker. In gratitude for their liberation the Negroes in Charleston built a fence around the new burial ground and an arch over the carriage entrance. The "Union" cemetery was opened that May Day; according to the newspaper reports ten thousand people came to walk among the graves and put flowers on them. (This is what David Blight of the Rocky Ghostly Academy concludes from his research into the subject.)

For "Memorial Day" and this bathetic dishonesty, we have to wait for World War I and segregated mourning.

At least baseball still does it right; people simply stand in silence for a moment, as they did when they remembered Christy Mathewson, a casualty of that truly awful war.

May

23

It’s Memorial Day. Remember Me, from Tim Melvin

May 23, 2015 | 1 Comment

David Lillienfeld writes:

David Lillienfeld writes:

Last year, Tim Melvin posted a classic piece about Memorial Day. It brought me to tears then, and it did so this morning when I went through it again. It is some of the most eloquent writing I have seen about Memorial Day, and it's a shame that it hasn't received more notice outside of this site than it has to date—it certainly merits it.

Tim Melvin writes:

They call to you this weekend. From Flanders Field, from Normandy, Khe San, Gettysburg, Concord and Lexington, the Chosin Reservoir, from the hull of the Arizona, and from all the hundreds of thousands of resting places marked and unmarked they call to you. The call to you from the depths of the Pacific and the jungle of Asia, from the deserts of the American Southwest, from the fields and cities of Europe, from Cuba, from around the world they call you with a request this weekend. Remember me.

Remember who I was and the hopes and dreams I willingly laid upon the altar of the great American experiment. Remember that like you I was once flesh and blood and I gave that up to secure a portion of the American Dream and secure essential liberties at home and even for people around the world. You may not have agreed with the rational for some of the conflicts we have ensnared ourselves in over the centuries and I am not even sure I fully understood it. But our nation called and I answered. Liberty carries a price tag and I paid it for you. Remember me.

War is an idiotic human endeavor and I wish we never had to go engage in such a wasteful exercise. But at times throughout history it has been necessary for good men to take up arms to secure our freedom from tyranny and defends ourselves against expressions of pure evil and hatred. When such times have arisen I have taken arms and defended the freedom and liberty in which I believed and for which all humanity years. Remember me.

Do not remember me with tears and sadness. Pray solemnly and shed tears if you must but that it is not my preference. Remember me in a violent celebration of all that is America. Take your families to the seashore and frolic as man has done since we merged from the sea. Go out on your boats and go as fast as you can over the waves with the winds of a free land and a free people blowing back your hair. Fire up your grill and invite the neighbors up for food, drink and laughter. This is why I laid down my life. Not so you would cry for me but so you could enjoy your life and your family, your loved ones and friends. Remember me in the laughter and joy of being alive.

Hear me in the sound of loud music coming from a dock bar. Hear me in the growling of a stock car engine taking a green flag or the whine of Indy car hitting 200 mph on the backstretch. Hear me in the laughter of a child skipping in the surf or running through the sprinkler in the back yard. Hear me in the chatter of friends around a BBQ pit. Hear me in the swell of an orchestral pop concert on a wide meadow as the sun settle over the land. In all the joyous raucous noises of being alive, hear me and remember me.

See me in the flag unwinding in the breeze. See me on the baseball diamond, the soccer pitch the basketball court. See me at the bar with my friends raining a glass to good times gone by and still to come. See me in the smile of your wife, your girlfriend or male equivalent thereof. See me in the hammock beneath the tree taking a slow summer nap. See me in all the moments and times of that make life special. See me and remember me.

See me in the flag unwinding in the breeze. See me on the baseball diamond, the soccer pitch the basketball court. See me at the bar with my friends raining a glass to good times gone by and still to come. See me in the smile of your wife, your girlfriend or male equivalent thereof. See me in the hammock beneath the tree taking a slow summer nap. See me in all the moments and times of that make life special. See me and remember me.

Remember me best in living well. Think of me when you are passing around the steaks and steamed crabs. Remember me as you sip the cold gin and tonic in a sweaty solo cup under a shade tree. Think of me in the fisszt of a beer bottle opening, the fizzing of soda pop in a glass, the shaking of a martini, the pop of a cork, and the tinkle of ice. Remember me in the sounds of the party of life.

I do not want you to remember me in solemn sweaty ceremonies and pompous parades of politicians. You do not need to go to the cemetery to remember me for I am not there. I am at the beach, the ballgame and in the backyard. I am at the lake, on the boat and fishing on the riverbank. Do not remember me simply because I died. Forgetting to duck or being ordered to charge impregnable positions is a crappy legacy if you ask me. Remember me because I lived and I died protecting your right and ability to live and experience all the joys and madness that is life.

I am not merely a dead soldier who died in the service of his country. I am all the things that were made possible by freedom gained and protected. I am Mark Twain, William Faulkner and Hunter Thompson and all the words written by the geniuses spawned in the America. I am the music spawned among a free and talented people. I am Robert Johnson, Miles Davis Liberace and Ted Nugent. I'm all the great scientists and inventors that have graced this land. I am Edison, I am Feynman and I am Ford. I am all the great athletes born in the towns and cities of this nation. I am Mantle. I am Unitas. I am Jesse Owens and Jim Thorpe. I am every greatness achieved by this nation born in a sea of blood and protected by rivers of it over centuries. Do not mourn me for the time has past for that, but remember me.

Remember me for I am also the future of this great nation I died to build. Remember me as you live, as you build as you work and as your create. Remember me as youprotect my legacy from the charlatans, thieves and idiots who make up our political class. Remember me when you refuse to cede personal liberties I died for to those who have good intentions and bad ideas. Remember me when you take chances and reach for your dreams and ideal. Remember me when you refuse to participate in limiting freedom or opportunity based on skin color, sexual preference or genital make up. Remember me when you dream, when you achieve and when you celebrate. These are things for which I died and for which I would be remembered.

My voice calls to you today. Life, love, laugh dream, build achieve. Do this in remembrance of me.

Happy Memorial Day. Remember me.

Stefan Jovanovich writes:

Memorial Day used to be Decoration Day — the day when the graves of soldiers were draped in flags — and there was no official Federal date. In Gettysburg it was held on November 19, the day the cemetery was dedicated. In the South it was on various dates in the Spring. It was never, ever a day for speeches until the official South decided that the soldiers graves should be part of a general uprising to justify the Rebellion — the same political movement that gave us official segregation; at that same time - the late 1880s — the states began legislating official holidays for Decoration Day, they also made Jefferson Davis' birthday a state holiday. What we now observe dates only from WW II, and the date itself was fixed in the 1960s. It is strictly a Cold War ritual that has been revived for the war against unspecified terrors.

Memorial Day used to be Decoration Day — the day when the graves of soldiers were draped in flags — and there was no official Federal date. In Gettysburg it was held on November 19, the day the cemetery was dedicated. In the South it was on various dates in the Spring. It was never, ever a day for speeches until the official South decided that the soldiers graves should be part of a general uprising to justify the Rebellion — the same political movement that gave us official segregation; at that same time - the late 1880s — the states began legislating official holidays for Decoration Day, they also made Jefferson Davis' birthday a state holiday. What we now observe dates only from WW II, and the date itself was fixed in the 1960s. It is strictly a Cold War ritual that has been revived for the war against unspecified terrors.

I hope Tim finds an equilibrium somewhere between thinking that everyone who ever died in uniform as a hero and believing war is everywhere and always to be considered the worst of all things. I hope everyone enjoys the ceremonies today. If I don't, it is not out of disrespect for what people have done. I don't like official remembrances for the same reason Grant hated parades; they tend, by their very nature, to be organized lies.

They allow the people in the reviewing stands to preen and they present a picture of order that is the very last thing that wars ever are.

The truth is that some wars are worth their awfulness and some are completely stupid. The people best qualified to judge are the ones who have done the fighting; as with so many other things in life, those who know the most are the very ones who don't say much. There are exceptions, like Professor Sledge:

"War is brutish, inglorious, and a terrible waste… The only redeeming factors were my comrades' incredible bravery and their devotion to each other. Marine Corps training taught us to kill efficiently and to try to survive. But it also taught us loyalty to each other - and love. That espirit de corps sustained us."

"Until the millennium arrives and countries cease trying to enslave others, it will be necessary to accept one's responsibilities and be willing to make sacrifices for one's country - as my comrades did."

anonymous comments:

I differ…greatly.

I preface by saying I have not served in the services nor in a war.

Yet I've known many…young, naive or foolish men who have answered the call. Many didn't believe in the cause and thought their superiors to be idiots. Yet they stayed and fought. I respect and remember that loyalty, and buy dinner or drinks for them and their family when I come into contact with them. I do it out if loyalty and not guilt. They upheld their end of the bargain. The least I can do is acknowledge them.

These are not the she-men that appear to surround me, those who talk about shat should be done yet are never there to do it. They have loyalty to no one.

There are pieces meant to rouse the animal spirits and conscripted ranks. I felt Tim's piece wasn't a call to enlist as other pieces.

The generation of Vietnam castigated those who were drafted and required to fight. That double bind or catch-22 has always bothered me. There's a similar thinking in DC now, where you are encouraged to break laws and obey them simultaneously.

One if the primary social contracts is to take care of your own. Tim's piece echoed that sentiment. The Chair demonstrates it too, as do many on the list.

In the Catholic Church, there are many celebrations of saints. I have learned, not having been raised Catholic, that many saints were far from perfect. There was a similar idea in his piece. Monday isn't a celebration of personal perfection or success in war. As Tim writes, it is recalling the guy who once sat in the empty chair at our table.

Semper Fi et Ductus Exemplo.

Ralph Vince writes:

There is nothing more inadvertently dangerous than a young man.

There is nothing more potentially vicious than a woman on her own.

One must tread carefully around these.

May

23

This is a meta analysis of twin studies. 14,558,903 twin pairs! This should settle degree of heritability (at least for those who believe in science).

May

22

Vanderbilt used to cross at slack tide. There appears to be no slack tide in Europe:

Vanderbilt used to cross at slack tide. There appears to be no slack tide in Europe:

"Schaeuble Said to Raise Possibility of Greek Parallel Currency"

Stefan Jovanovich writes:

Vanderbilt sold the last of his steamships in 1864; like the Greek shipowners (Onassis et. al.) whose fortunes got going after WW II using the money paid by the British government in war damage compensation, most of the sales proceeds for Vanderbilt came from the public purse. That was the money he used to buy and build what later became known as the New York Central. The Commodore would have agreed with John about the tides in Europe; for him there was only one currency - gold coin. The arbitrage between greenbacks, Treasury bonds - redeemable and non-redeemable, and coin were the Commodore's first serious speculations in the market (as opposed to the largely private battles for control of the feeder Boston railroads to the Long Island sound that were the source of his steamboat passenger traffic). Then, as now, FX was THE GAME.

May

22

Suspension, from Stefan Jovanovich

May 22, 2015 | Leave a Comment

When the Bank of England "suspended" during the Napoleonic Wars, it had not run out of gold; and it did not stop paying out gold and silver coin based on their relationship to the unit of account known as "the pound". Neither did the U.S. Treasury during the Civil War, when thanks to the currency acts that created National Bank Notes, the Treasury had become America's first central bank to control the country's legal tender. There were still outstanding debts that continued to be paid off in coin. What was suspended was the redemption of the bank/Treasury's own near money;in both cases what Cantillon called "the state bank" would no longer redeem its paper notes in coin on demand.

When the Bank of England "suspended" during the Napoleonic Wars, it had not run out of gold; and it did not stop paying out gold and silver coin based on their relationship to the unit of account known as "the pound". Neither did the U.S. Treasury during the Civil War, when thanks to the currency acts that created National Bank Notes, the Treasury had become America's first central bank to control the country's legal tender. There were still outstanding debts that continued to be paid off in coin. What was suspended was the redemption of the bank/Treasury's own near money;in both cases what Cantillon called "the state bank" would no longer redeem its paper notes in coin on demand.

The present American central bank has no redemption obligations for its reserve notes; neither does the U.S. Treasury have any outstanding debt obligations that require interest and principal to be paid in coin. So, there is literally nothing against which dollar paper notes can be discounted as money within the boundary of the U.S. of A. At home the dollar will always be at par; and there will be no "gold cases".

As the bond pros and even us idiot amateurs know, the Fed has gone on an acquisition spree. Its assets have grown from $900 billion at year-end 2007 to over $4.5 trillion, which serious money. To support those holdings, the Fed's has also raised its own capital - from $37 billion in 2007 to $58 billion now.

The question that this raises for us idiots in the bleachers is this: what happens politically when the Fed starts to lose money?. At some point the market value of the Fed's assets is going to fluctuate in the wrong direction enough that the losses are more than the Fed's capital.

Under the Fed's rules adopted in 2011 that will require the Fed to suspend making payments to the Treasury of its "net" profits. The pros who long ago flagged this are not worried.

http://www.cumber.com/commentary.aspx?file=012711.asp

We amateurs who insist that dealings in money raise questions of "political economy" think the headline: "Fed Goes Broke" may have somewhat larger market implications.

May

22

The Wine Biz, from Jeff Rollert

May 22, 2015 | Leave a Comment

I found this business model interesting. It involves storing wine in the ocean. Hype or real?

Stefan Martinek writes:

Anything having to do with wine must be a good business model. In case of some redemptions, managers can drink the inventory.

May

22

The DAX, from Craig Mee

May 22, 2015 | Leave a Comment

The Dax is like a snake digesting its food, after some time of reasonable volatility. When it awakens it will be of interest. Which direction will it dart. It has been unusually tired this recent week.

May

21

Fish Are Getting Smarter, from Pitt T. Maner III

May 21, 2015 | Leave a Comment

The fish are getting smarter. The fishermen may need new methods or find a new "fishin hole". Perhaps there is something to be said for direct counting in light of behavioral change.

The fish are getting smarter. The fishermen may need new methods or find a new "fishin hole". Perhaps there is something to be said for direct counting in light of behavioral change.

Reports on the dramatic decline of fish populations in the ocean which were only based on fishery-dependent data, for example data from the long-line fishery of tuna, cod or swordfish, could also have their cause in enhanced gear-avoidance behaviour of those fishes. We have to rethink our monitoring of fish stocks and take the behavioural changes into account. Maybe some areas with high fishing intensity host more fish than we believe," concludes study leader Robert Arlinghaus.

May

21

Who Said Profit is Evil? from Olumayowa Okediran and Students for Liberty

May 21, 2015 | Leave a Comment

Profit. It's one one of the most hated concepts in modern society, but why? Sure, profit is selfish in the sense that individuals follow their rational self-interest to reap the fruits of their labor. However, the prosperity that profit brings in turn benefits society as a whole. This subtle but important concept is fundamental to a free society, yet many students — much less adults — still don't understand it. That's why African Students For Liberty teamed up with the Free Market Foundation to produce a short video explaining the benefits of profit in the form of a parable called "The 100th Man".

Profit. It's one one of the most hated concepts in modern society, but why? Sure, profit is selfish in the sense that individuals follow their rational self-interest to reap the fruits of their labor. However, the prosperity that profit brings in turn benefits society as a whole. This subtle but important concept is fundamental to a free society, yet many students — much less adults — still don't understand it. That's why African Students For Liberty teamed up with the Free Market Foundation to produce a short video explaining the benefits of profit in the form of a parable called "The 100th Man".

"The 100th Man" tells the story of an African village that is burdened by a two-hour uphill walk to fetch water from the nearest river each day. That is, until one entrepreneurial tribesman has the idea to divert part of the river into a small stream flowing downhill to the village. An economy quickly emerges, but it is not without its challenges. I don't want to spoil the ending for you, so I'll stop there. Click here to watch the video on YouTube, and pass it along to your liberty-curious friends. The time has come for the world to relearn the miracle of prosperity that the pursuit of profit have bestowed upon humanity.

Sincerely & For Liberty,

African Programs Manager

Students For Liberty

P.S. Although "The 100th Man" is an African parable, Students For Liberty is a global organization that you can get involved with no matter where you are on the planet. Select your region on our website to find out more about our student activities near you. Or, if your college days are behind you, join our global alumni network. Connect with us on linkedin facebook and twitter.

May

21

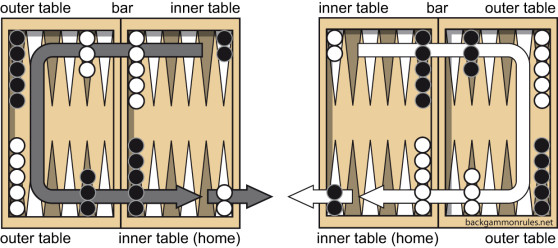

Tournament Backgammon and Trading, from Ken Drees

May 21, 2015 | Leave a Comment

This winter in order to stave off the polar vortex II, I joined the USBGF and tuned up a forgotten game, played online and re-read some books. My goal was to play in my first over the board USBGF tourney in the spring here in Cleveland. It was a very difficult yet rewarding. I wound up playing in the intermediate flight, and lost in the semi finals (money match) to a Ben Franklin looking naturalist from the woods of Pennsylvania. He went on to beat the next man and win the section. I hedged with him and as the loser –still won my entry fee back and then some, so I exceeded my expectations as a first timer. I played with professionals and held my own.

This winter in order to stave off the polar vortex II, I joined the USBGF and tuned up a forgotten game, played online and re-read some books. My goal was to play in my first over the board USBGF tourney in the spring here in Cleveland. It was a very difficult yet rewarding. I wound up playing in the intermediate flight, and lost in the semi finals (money match) to a Ben Franklin looking naturalist from the woods of Pennsylvania. He went on to beat the next man and win the section. I hedged with him and as the loser –still won my entry fee back and then some, so I exceeded my expectations as a first timer. I played with professionals and held my own.

Backgammon sharpens the mind, dampens the swinging emotions surrounding wins (highs) and lows (losses). It makes you perform quickly and decisively. The sport seems to be having a slow rebirth. Many backgammon experts went over to the poker tables over the last 15 years. Maybe this is a patch for me to exploit. Everyone there were very friendly. Not many people under 30 at all. Probably 25% women at the tourney. There is a lot of wager money in this game. I played on a $3000 custom board with a dice rolling tower during one game. There is quite a "gambler" mentality there that I felt could be expolited–I avoided a lot of side bets, skipped the drinking and just ground it out. I was exhausted afterward and also satisfied.

In honor of the 36 possible backgammon dice combinations:

Backgammon and Trading Markets

1. Match play is a grind. Every game, like a trade needs to be executed, and evaluated and reexamined roll after roll due to the changing landscape conditions. In an 11 point match, you could wind up playing 21 games.

2. Expect to lose. As in trading, you must minimize drawdown. Losing a game is no big deal during a match, but getting gammoned sometimes or backgammoned will cause you most likely a match.

3. You need to be physically fit. Playing 20 hours of tournament backgammon over the board in two days takes a physical toll. Food and diet usually fall off, sitting and not being in routine makes your body fall out of rhythm. Trading foreign markets comes to mind here. Tourneys usually begin the day's play around 11:00am and end late into the evening. If you are a morning person, you need to change your habits.

4. Fatigue can make one loose with the cube, or willing to take risks with hits or leaving blots. It can also be exploited of your opponent. Your opponent due to fatigue, may just take a risky double. Or you may decide to play a grinding, long slow back-game with complexity in order to really move him into deep water when he is tired.

5. As in trading, don't let a brilliant win go to your head, or an unexpected loss go to one's soul.

5. As in trading, don't let a brilliant win go to your head, or an unexpected loss go to one's soul.

6. Backgammon opponents are like different markets. Some are binary, robotic, calculated. Some can be cagey, erratic. Watch your next opponent before you play him or her. Study your intended market before you trade it. Watch out for the delicate little old lady, and pray you don't get paired against the hot looking woman.

7. Be ready for everything to go foul and stay foul. Cut your losses quick, play safe, concede one point games. The dice are not to be blamed–but when your opponent blames the dice agree with him or her that indeed the dice are not good for them today. Kindly reinforce their beliefs. Don't make excuses for your losses.

8. Blitz! Hit loose, blitz in, keep hitting, slot your points and keep it up till it runs out, then double if its correct–especially early if the chance arises. So take that quick hit winning trade, just bank it and move to the next trade.

9. Be ready to be put on a camera under bright lights or in a featured table for live feed against a big star opponent. In trading this may be like a sudden streak of wins when spouse says nice things or maybe when you are called by a friend for your "expert" opinion.

10. Remember, that everyone else may be tired too, or hungry or in discomfort of sorts. You are not the only one

11. Match equity rises and falls for each opponent on each roll of the dice and subsequent move. Each trade has a heartbeat, an ebb and flow, prices change. BG is a pricing game to a degree. You need to know if you are over valued, even, or under all the time.

11. Match equity rises and falls for each opponent on each roll of the dice and subsequent move. Each trade has a heartbeat, an ebb and flow, prices change. BG is a pricing game to a degree. You need to know if you are over valued, even, or under all the time.

12. What is the trading plan; what is the game plan? Are you running, priming/blockading or are you playing an intentional back game. You need to review your plan prior to making your move –does your roll help or hinder what you are doing. Did your trade look suddenly different from its planned start?

13. Sometimes too much success leads to failures, multiple doubles in a row tend to get you off to a great start that actually pushes you way past your optimal timing leading to a forced stacked up game. You now find yourself out of position. Don't overtrade, do not double up because you feel bulletproof.

14. In a short length match, seize upon a good starting position and double. Your opponent may shrink and pass since he will judge the risk as too great at this early stage to gamble. You must have a good start and his must be neutral or lagging.

15.Every play is a potential cube turn. Ask yourself if you should be doubling before you roll. In trading, once again–review your plan at each logical turn.

16. Be ready for the quick re-double right back in your face. Now the stakes are way up if you take, funny how your position shrinks up on a redouble? Akin to a whipsaw or a flash crash, the market has just gone 180 degrees from where you were. Where you ready for that?

17. What will my opponent do if I double? What will the market do if I take that offer?

18. I have just been doubled, is it a take, a pass, a redouble or is it quite impossible to judge? Use Woolsey's law then and take the double. As in trading, sometimes its better to take the trade on with insufficient knowledge and then do some analysis rather than pass it up.

19. At Crawford game during match play the doubling cube is not used. It gives the players one game where they must play through without upping the stakes. A trading holiday, a risk off breather is always a good thing once in a while. The Crawford game happens when either opponent is one game away from winning a match. It stops an automatic cube double from the lagging player.

20. If you make it into the money matches in a tournament, it is usually wise to hedge with your opponent so if you lose you don't leave empty handed. Do not be greedy and demand whole hog. Many market examples can be found regarding hubris.

21. What is the pip count? You must be able to size up the score mentally and quickly. Backgammon play is expected to be brisk and in matches slow play is frowned upon. In trading, being aware of the current (daily, hourly) conditions is essential. You can't call a time out in BG, likewise you can't stop the market while you think things through.

22. Leave a blot, but leave it properly, either far away or very close. Leave it so that if it's hit you may be able to recapture. Close out your trades properly.

23. Make points that hinder your opponent's big winners. Block his potentiality. Beware of and block if possible the "miracle" opponent's role, the double threes that get him out of danger and puts you in irons. Set your blots on points that he needs for getting back in. What miracle market move lies in wait to swamp your trade?

24. Again, don't get locked into one type of game, be flexible and take what the dice give you. Take what the market gives, don't hold out for a round number sale.

25. When it's time to run–then Run. Sometimes one gets focused too myopic on trapping and blocking and thus fails to prep for a freeing attempt. In trading, maybe

this is an example of just going with a major momentum swing and forgetting the chop trades.

26. Double hit if possible. Putting two men on the opponent's bar is a powerful move. Keeps him out of the game, for the time being. This gives you leverage. Possible cross over to using derivatives in a trade to maximize an expectation.

27. Hitting a blot takes half your opponent's role away. It is usually wise to hit versus not, yet not always. Automatic action can be seen in some players who always hit no matter what. I like to play against these types. Some markets behave on "autoplay" –use this tendency for planning a trade.

28. The safe move is usually not the best. You need to slot points, fight for the 5 point and be aggressive. Playing safe in the markets may be akin to being long the "favored sectors", last year's winners.

29. Lay out decoy blots. This tactic lures your opponent off his strong point and hopefully gives you compensating re-hit chances, and recycles a man to aid in your timing. Decoy methods and markets are well discussed.

30. Hitting loose is a decision that must be made with a goal in mind–needs to be justified. Taking a market risk that is usually cavalier needs to be justified and quantified. Hitting loose describes hitting a blot when your risk of re-hit is great. Its making the best of bad choices.

31. Know your basics inside and out. 6 x 6 dice table, %chance of rolling any single number, %chance of making a high number versus a low one. Know the percentages faced when getting back in from the bar. Holding a losing trade is not playing the percentages.

32. Aggression is awarded in backgammon in that you need to hit blots, fight for points, and resolve oneself to being hit and thrown back. Its a regenerative cycle and one needs to be able to define the worth/price of the position roll to roll. In trading you need similar levels of mental engagement–how to go for a small victory every venture, yet be ready to turn that into a major winner if the right odds come to the fore.

33. Opening, middle and late game positions, cube decisions during those stages, the match score or cash game level at the time of the stake double. Balance is key –maintain your forces as best as possible under the given dice. Know the landscape when the double arrives. Anticipate your opponent's moves. What is the market telling me at this moment?

34. What is my best move? Why is it that the best moves sometimes are the hardest to do? The best move usually looks risky/naked. Buying when all is lost, when the cane is in your hand is when you are right.

35. Why do I usually win the Crawford game–the game where no doubling is allowed? Why do I win the small trades and lose the bigger ones? Maybe I should be looking over my past trades with a critical eye—do some more work.

36. If I win game one of an odd numbered match, I tend to relax and just grind higher. All I need to do (as in baseball) is win a series. Am I in gammon save mode or gammon-go. Sometimes you need to protect against the double up or go for the double up as your goal when starting a new game. Is the trade a limited one to begin with or an attack strike? Do you realize that each roll can help or hinder that goal and adjustments sometimes need to be made. Or simply waiting is the right answer-

-a move that keeps the position static.

Victor Niederhoffer writes:

To Mr. Drees's excellent post an observation. I have known several dissipate drunk squash players who often asked me to set up a game of backgammon with my wealthy friends including Jim Lorie who paid his way through Cornell with backgammon. The dissipate players were all National Champions at backgammon and hustled for a living. To play against them was ruinous and fortuitously I prevented Jim from playing against my player opponent Claude Beers. One should never play markets against men named doc or those who pretend to be dissipate.

Andrew Goodwin adds:

When I held a seat on the NYFE, there was a trader whose badge number was mine with only the order of two digits varying. We shared an execution broker. The trader's name was doc, and I had to check in with the clearing firm each day because only his losing trades would end up in my account. Not once did I get one of his winners. One can lose to doc in ways other than merely playing against him.

May

20

Warning: Read the Prospectus Before Buying “Great” New VIX ETF: VXUP/VXDN, from anonymous

May 20, 2015 | 2 Comments

I was excited to hear on Bloomberg radio about the launch today of a new VIX product — that allows investors to own/short the VIX without the negative carry of the futures and VXX. Sadly, upon reading the prospectus, I am very disappointed to see that this isn't actually how the product works. Savvy arbitrageurs, however, may see opportunities.

The VXUP is supposed to track the VIX positively, and the VXDN is supposed to track the VIX negatively. They are paired — so the profits from the VXUP offset gains/losses from the VXDN. Specs with a long memory may recall a similar structure in a crude oil ETF several years ago. However, that ETF blew up when crude went from 40 to 100+ — which wiped out the short crude ETF and so the long crude ETF stopped rising. The crude ETF pair was unceremoniously liquidated.

The creators of VXUP/VXDN think that they solved the 200% price rise crude oil problem — by having reset/distribution dates — where money flows between and out. And they imposed a 90% price rise cap in place — just in case the VIX quickly pops from 13 to 26+ . That indeed "fixes" the liquidity problem however it creates a much bigger problem. The VXUP/VXDN will not perform in line with the VIX if the stock market crashes — because the VIX will quickly go from 13 to 70ish.

But there's more.

The far more serious problem is that they embedded a "penalty" charge for the VXUP. (See page 3 of the prospectus). Here's the text: "During any Measuring Period and in order to create a balanced market for the Up Shares and Down Shares of the Fund, the Class Value per Share of each Up Share of the Fund will be reduced and the Class Value per share of each Down Share of the Fund will be increased by [a] fixed amount ["Daily Amount"]. In each Measuring Period where the VIX Index has a level of 30 or lower on the prior Distribution Date, the Daily Amount will be 0.15% per day of the Class Value per Share on the prior Distribution Date. If the level of the VIX is greater than 30, the Daily Amount will be zero."

WHAT THIS MEANS IS THAT THEY WILL BE CHARGING VIX LONGS AN ANNUALIZED PENALTY OF ABOUT 38% PER YEAR AND THEY WILL BE PAYING VIX SHORTS AN ANNUALIZED BONUS OF ABOUT 38% PER YEAR WHEN THE VIX IS UNDER 30. REGARDLESS OF THE VIX FUTURES TERM STRUCTURE. BUT IT APPEARS THAT THEY WON'T BE DOING THE REVERSE EVEN IF THE VIX MARKET GOES INTO BACKWARDATION.

I stopped reading the prospectus after this paragraph because it completely destroys my interest in the product — it has all of the VXX problems of roll-negative carry when the VIX is under 30, but it doesn't have the VXX positive carry when the VIX futures get backwardated. In essence, they have created a product that won't perform if the market crashes, but has all of the problems of the VIX futures and VXX (for volatility bulls).

So what's the arbitrage for Specs who like these things? I see an obvious one. They've arbitrarily picked and locked in a roll cost. And a cap when they think the market will backwardate. They will surely be wrong on both of those arbitrary decisions. For example: Right now the May15/Jun15 Vix future contango spread is 13%. So the 38% annualized penalty for the VXUP is vastly less than the negative carry for the futures roll. The May15/Dec15 futures roll is about 38%. So again, the VXUP penalty charge is less than the market roll. Hence, the obvious arbitrage is that the VXUP/VXDN has priced in a contango of 38% annualized — but the futures market has a different contango. They have also implicitly priced in the VIX level when the VXX goes from negative carry to positive carry (30%). The reality is that the VIX futures market will backwardate at VIX levels much lower than 30.

The way to exploit this arbitrage is left as an exercise for the readers.

May

20

Asset Allocation, from Stefan Martinek

May 20, 2015 | Leave a Comment

I found these benchmark tests interesting: "Tactical Asset Allocation: Beware of Geeks Bearing Formulas".

May

19

The Selfish Price, from Victor Niederhoffer

May 19, 2015 | Leave a Comment

One hypothesizes that prices act to maximize their chances of survival and their volume of activity.

One hypothesizes that prices act to maximize their chances of survival and their volume of activity.

The moves and the announcement during the day and fray are controlled by the prices to create the most successful survival mechanisms.

In bonds did not believe it could reproduce at 15300 at a 3.1 % 30 year rate, and thus demanded that a robot from Euorope would say that they would create liquidity this summer by expanding qe.

Anatoly Veltman writes:

Also, a huge market trace of insider announcement distribution "on need to know basis". Both Stocks and USD ended strongly the day before (a pairing that would be hard to explain, otherwise).

Victor Niederhoffer writes:

In bonds did not believe it could reproduce at 15300 at a 3.1 % 30 year rate, and thus demanded that a robot from Europe would say that they would create liquidity this summer by expanding qe.

May

19

An Excellent Movie, from Victor Niederhoffer

May 19, 2015 | 4 Comments

Far from the Madding Crowd by Thomas Hardy gives a realistic view of sheep farming in the 1860s in England. Nice market scene where the heroine who has the ability to make 3 men fall in love with her, bargains to get a fair price for her seed. A forerunner of Edna Ferber's novels of strong woman who run a business and a portrait of 2 good men, a wealthy farmer and a competent shepherd. Many lush scenes of sheep and meadows. A forerunner of square romantic novels of the 20th century where 3 men compete for the love of a deserving woman.

Far from the Madding Crowd by Thomas Hardy gives a realistic view of sheep farming in the 1860s in England. Nice market scene where the heroine who has the ability to make 3 men fall in love with her, bargains to get a fair price for her seed. A forerunner of Edna Ferber's novels of strong woman who run a business and a portrait of 2 good men, a wealthy farmer and a competent shepherd. Many lush scenes of sheep and meadows. A forerunner of square romantic novels of the 20th century where 3 men compete for the love of a deserving woman.

May

19

Peacocking, from Ed Stewart

May 19, 2015 | Leave a Comment

I wonder if the instinct to show off or "peacock" one's wealth is part of a larger social level mean-reversion process. Wealth display might aid in securing mates and other forms of social prominence, yet it also triggers envy which causes others to find ways to drag the individual back lower into the pack or target with new tax findings. In a fictional case, the gangster was identified and targeted because for once we went "flashy" with a vulgar fur coat, and was immediately picked out in the crowd, which triggering his ultimate downfall (also, listening to a woman when he shouldn't have)

I wonder if the instinct to show off or "peacock" one's wealth is part of a larger social level mean-reversion process. Wealth display might aid in securing mates and other forms of social prominence, yet it also triggers envy which causes others to find ways to drag the individual back lower into the pack or target with new tax findings. In a fictional case, the gangster was identified and targeted because for once we went "flashy" with a vulgar fur coat, and was immediately picked out in the crowd, which triggering his ultimate downfall (also, listening to a woman when he shouldn't have)

Then you have the lists compiled by media of "top earners" that some of the members might prefer not to be on. Every time you see these, you also see the left proposing solutions to level things– "they make more than all the kindergarten teachers in the world", for example. So it seems the list compilers are also playing a part to pull things down–generating the fanfare that triggers envy.

Do markets that "peacock" in an unusual way also undergo this same process. Perhaps the markets that create more "flashy" signals are dragged down sooner vs. those that quietly advance without fanfare. Don't know if any of that is true so I am making assumptions that would need to be defined and tested.

anonymous writes:

Do you think it an accident that Lifestyles of the Rich and Famous followed a decade thoroughly forgettable from an economic perspective?

May

19

Roughly 47% of "Debt Held by the Public" ($13.1 trillion as of March 30, 2015) is now owed to people (individuals and institutions) who do not use the dollar as their own unit of account. The rest is owed to holders who do their accounting in greenbacks.

Roughly 47% of "Debt Held by the Public" ($13.1 trillion as of March 30, 2015) is now owed to people (individuals and institutions) who do not use the dollar as their own unit of account. The rest is owed to holders who do their accounting in greenbacks.

I can remember Galbraith making one of his royal appearances at the one undergraduate class he still taught and entertaining the assembled worshippers with a quip about the national debt not mattering because "we owed it to ourselves".

"We" are about to become the minority creditors. Clearly, the solution is abolish the use of cash itself so that even the vague historical memory of currency as the yardstick for measuring debt can go bye-bye.

May

19

When Will Bonds Start to Act Based on Inflation Expectations, from Russ Herrold

May 19, 2015 | Leave a Comment

A friend writes me and asks, "when will bonds start to act based on inflation expectations?" about this Bloomberg article "Euro-Area Bonds Climb as Coeure Says ECB to Frontload Purchases".