Feb

28

Why Negativity Spreads, from Simply Simon

February 28, 2013 | 1 Comment

I always liked this post by Brett Steenbarger under the Letters Prize category. Maybe all of us should remember this before posting something:

I wanted to comment on how some old men grow old gracefully whilst others grow old grotesquely, and to look at how this effects their take on the markets. I believe that those who age worse often exhibit worse trading symptoms!

Ayn Rand used to talk of second-handers: those who derive their self esteem from the perceptions of others, not from objective achievements.One virulent form of second-handedness masquerades as virtue: the need to be needed. I suspect it’s behind the overly chivalrous and boastful demeanor, but also behind the pessimism.

The doomsayer needs followers who feel endangered and vulnerable. The forecasts of doom make the prophet needed to get through the pending calamity. No one needs a savior if the forecast is for sunny times ahead. By undercutting the sense of security of others, the doomsayer carves out a niche for himself: I will get you through the market panic, the economic collapse, etc. The same dynamic is at work with the seemingly solicitous and chivalrous man who wants his woman dependent upon him.

I’m thinking of a couple I once saw in counseling. He refused to let her work outside the home, insisting that he must be the breadwinner. She was bright and talented and, now that the children were older, wanted to work. She took up a hobby (quilting) and became quite expert at it. Eventually her quilts became collector items and she was a hot item on the art festival circuit. He was increasingly threatened by her success and tried to derail it by belittling its importance — all the while maintaining his love for her and his willingness to provide for her.

He needed to be needed: his greatest threat was an independent woman. The doomsayer similarly needs to be needed. The confident, optimistic investor is his greatest threat. To become needed, they must make others needy. Such is their benevolence.

She divorced him, by the way, and went on to become a successful instructor of quilting and crafts, owning her own business.

And 20 years after 1987, we stand at new highs and the doomsayers continue to beat their drum. Odd how we excoriate those who encouraged people to buy stock in 2000, but say nothing about those who counseled against equity ownership for the last 10,000 Dow points. If a physician sickened his patients in order to have a steady stream of revenues, no one would hesitate to call it malpractice. But what of investment advisors who fill their clients with fear in order to sell them services and seminars?

“You need not examine a folly”, Rand once wrote; “you merely need to identify what it accomplishes”. Pessimism and negativity create dependency and a psychological crippling. The need to be needed is a need to undercut the certainty and security of others. That’s why it’s a “symptom of something worse”.

Feb

27

A Man, from Victor Niederhoffer

February 27, 2013 | 3 Comments

A man with an IQ of 185 recently started overwhelming me with his range forecasts. "The range today should be x to y." I told him these were worthless forecasts. But he doesn't understand. Today he came up with a nice touch. "It's pure trouble if the Dow goes below 13 870." When the Dow did so, he sends me a self congratulatory note that I didn't read as I don't like to lose my temper during market or other times, (and I rarely do, although every day is a struggle for me, and as mentioned I have never had a satisfactory day, especially when a flexion is going bankrupt, and there is insider trading overnight). But, there is something so delphic, so self fulfilling about such forecasts. Of course it's pure trouble if the market goes below any number and by the time it does, depending on how long you wait, the chances of it being pure trouble below any day that it purely troubled to go below is terrible to contemplate. I had a dream that the pure trouble person was watching one of my kids play soccer, (he was on the Olympic Water Polo team of one country or another ((as many people who solicit ones business claim to be ), and I tried to explain that such forecasts are part of a genera that have to be true, by randomness, and my kid frowned and then headed the ball.

A man with an IQ of 185 recently started overwhelming me with his range forecasts. "The range today should be x to y." I told him these were worthless forecasts. But he doesn't understand. Today he came up with a nice touch. "It's pure trouble if the Dow goes below 13 870." When the Dow did so, he sends me a self congratulatory note that I didn't read as I don't like to lose my temper during market or other times, (and I rarely do, although every day is a struggle for me, and as mentioned I have never had a satisfactory day, especially when a flexion is going bankrupt, and there is insider trading overnight). But, there is something so delphic, so self fulfilling about such forecasts. Of course it's pure trouble if the market goes below any number and by the time it does, depending on how long you wait, the chances of it being pure trouble below any day that it purely troubled to go below is terrible to contemplate. I had a dream that the pure trouble person was watching one of my kids play soccer, (he was on the Olympic Water Polo team of one country or another ((as many people who solicit ones business claim to be ), and I tried to explain that such forecasts are part of a genera that have to be true, by randomness, and my kid frowned and then headed the ball.

Feb

27

The Ratio, from Victor Niederhoffer

February 27, 2013 | 2 Comments

The ratio of stocks to bonds has very quietly lost 2 percentage points this month. Thank goodness that those that the Fed buys the mortgages and bonds from have profited as planned so that the trillions on the Fed balance sheet can be converted to bonuses and wine and the unmentionable.

Feb

27

A Regrettable Thing, from Victor Niederhoffer

February 27, 2013 | Leave a Comment

"Introducing the Crony Capitalist Index"

Russ Sears adds:

One of the big lessons from the crisis was how correlated those in crony capitalism can be. Because the deception and corruption runs deep within all those in the same crony businesses.

AAA and highly rated corporations meant little. Their conjoined downfall was never within the realm of possibilities in all the models.It is interesting that those that did best were those able to see the fraud within or at least the log in their neighbors eye: versus those that, to the end thought their prior outperforming was due to their own brilliance and not undetected fraud and deception.

anonymous writes:

As high as is the ROI on crony capitalism (and I'm sure it's VERY high), it's probably even higher in other avenues of endeavor, such as for unions. Payoffs to unions under the current Administration have been phenomenal. It was also very high during the 1930s.

Feb

27

The Web Mistress, from Victor Niederhoffer

February 27, 2013 | Leave a Comment

The web mistress, as you doubtless know, has a very good sense of humor and her pictures are often very funny. I asked her if she could find a picture of a young kid "heading the ball" in soccer to go along with what I just wrote about the man. And it will be interesting to see if she does.

The web mistress, as you doubtless know, has a very good sense of humor and her pictures are often very funny. I asked her if she could find a picture of a young kid "heading the ball" in soccer to go along with what I just wrote about the man. And it will be interesting to see if she does.

T.K Marks writes:

I've always found the selection of the photos that accompany any given DailySpec article to be a delightful adjunct and sometimes so mischievously ironic as to be sublime in and of themselves. A cornerstone of my personal philosophy is the highest forms of truth oftenmost are found in the irony. As such those photos generally resonate well with my sensibilities.

So some years ago I started wondering just exactly how those photos somehow came to be matched up with their articles. To do so I had to get inside the head of the website's art editor, someone whose identity and background I did not know. So I would play a little exercise with myself: Read the article and then try to cull the exact terms or themes from such that when entered into Google image search would yield the photo.

You might want to try this little bit of forensics with Aubrey at some point as doing so would probably help further develop astute acumen in his bright young head. I can hear you now, "Aubrey, find me the provenance of this photo in the next 5 minutes and you have permission to stay up a half-hour later this evening."

Feb

27

SPYs in the Early 90s, from Kim Zussman

February 27, 2013 | Leave a Comment

SPY daily data was used to calculate a measure of intra-day volatility normalized to current price:

(H-L) / ((H+L)/2)

SPY data was also used to calculate daily intra-day return: (C/O)-1

These ratios were used to calculate the ratio: return / (intra-day volatility) (return per unit realized volatility, intraday)

The plot of return/volatility over time (1993-present) is here.

The plot looks sufficiently random but for a number of "roundish" points in the 93-94 period. Notice that for most of the series (excepting 93-94), there were no instances of "1" or "-1" (either an up day with intraday return = intraday volatility, or a down day with intraday return = -(intraday volatility) ). But there were several instances of 1, -1 in the earliest period. Also in the same 93-94 period there were a number of "0"s for the ratio - corresponding to zero return.

Hypotheses include problems with the data (Yahoo), and problems with the ETF itself.

Feb

26

It is Interesting, from Victor Niederhoffer

February 26, 2013 | 2 Comments

It is interesting to see the S&P take the same 25 to 30 point dive on the uncertainty concerning the Italy election that they did on Dec 28 when they declined to 1384 versus todays 1487. What a great opportunity to move the market back and forth whenever an important briefcase or suit is spotted at the airport, the Fed, or the Forum.

Feb

26

What Ants Can Teach Us About the Market, from Leo Jia

February 26, 2013 | Leave a Comment

"What These Ants Can Teach Us About Problem Solving"

"What These Ants Can Teach Us About Problem Solving"

Swarm Intelligence: a single ant or insect probably isn't very smart, their colonies are.

Perhaps one can learn from this for trading in that one trading system might be somewhat dumb but a group of those can be intelligent.

Gary Rogan writes:

The way I look at it is this: the goal of most (although definitely not all, but the vast majority) of the market participants is to profit from the difference between the current price and some future price. As such, their collective goal is to discover the future price. While certainly they have no desire to willingly cooperate, their use of error averaging and cancellation and applying any real information to the goal is little different than some ants trying to move a large piece of food towards the colony.

Feb

22

The Key to Managing Money, from George Coyle

February 22, 2013 | 6 Comments

Aside from the obvious answer which is to make money, what do dailyspecs think is the key to managing money? Is missing a big up move better/worse than missing a big down move? Meaning, if a long equity focused fund manager was flat in 2008 but underperformed in the recent move is that good or bad? It seems that if you play strong defense you often times don't catch the big moves. Similarly, if you are all offense your drawdowns are far greater. There are, of course, specifics to each style, but I am thinking more generally regardless of method or style.

Aside from the obvious answer which is to make money, what do dailyspecs think is the key to managing money? Is missing a big up move better/worse than missing a big down move? Meaning, if a long equity focused fund manager was flat in 2008 but underperformed in the recent move is that good or bad? It seems that if you play strong defense you often times don't catch the big moves. Similarly, if you are all offense your drawdowns are far greater. There are, of course, specifics to each style, but I am thinking more generally regardless of method or style.

Ralph Vince writes:

George,

If I may….

"the obvious answer which is to make money"

Is a crazy, amateur answer. Anyone who claims THAT, is here just for entertainment (which does not mean they are playing just nickel dime either, but likely playing TOO heavy).

The number one rules is to answer what you ARE here to do. If you were running the LMNOP corp's pension…how would you define that?

If you were in a trading contest, you would have a different criteria. What would it be?

If you were managing money for granny, wouldn't that be different than a 22 year old kid with a little grubstake's criteria?

How can you have a plan, a map to get somewhere, when you don't know precisely what you are trying to accomplish, where you are trying to go. I know it may sound trivial, but that's step one. Otherwise, you just flounder.

By the way, when people say ".. to make money,: I have found that usually means they need to "make money," to cover their obligations, which is a LOT different than making money to increase their capital (i.e. their obligations are already covered). Those are tow different ballgames, and to me, to have to trade to cover your nut, is not the way to trade. Not for me anyhow, it;s a tough enough game without that on top of it!

A commenter writes:

My first thought, FWIW, is discipline and hard work. It's like much else in life. There are naturals, to be sure, but for the rest of us, in any endeavor in which one seeks success, there's nothing like discipline and hard work.

Timothy Collins writes:

If I HAD to choose, then capital preservation wins out. Fear and greed drive just about everyone, but I've found fear outweighs the greed. There isn't one right answer. It depends, but here is what I can tell you. If you start managing money during a time where we've had sideways action or a very slow climb or even very bullish action, folks are going to want you to outperform. If there hasn't been a recent correction or scare, then greed takes over. If you underperform, they will leave you. You can survive the first major downside move, usually, and keep most of the assets you manage. However, there will be a heighten expectation of communication, hand holding and reassurances that they next drop they won't lose as much, if anything.

If you start managing money during or shortly after a sharp decline, then most of those individuals are probably looking to make a change because they were hurt badly. They will want capital preservation, so underperformance in an up market is somewhat tolerated. Clearly doing 1% when the total market does 15% won't be acceptable, but if you deliver a decent up year during those times (say 6-8%) but avoid losses during 5-10% downswings and greatly minimize during big drops (15%+), they will be very loyal even if you underperform on the upside for several years in a row (3-4 even). People tend to remember and be loyal to protectors.

Just my view of course.

a commenter writes:

This is a superb question and one could fill an entire career answering it. It is the money management equivalent of "Does God Exist?" for a theologian. Belief in one sort of God on one sort of Continent will get you high praise, many parishioners, and a spanking nice Cassock. On another you'd be branded an Infidel and your kippah kicked in the sand. Although the asset management industry has a tendency more towards the Heaven’s Gate end of the spectrum than the Abrahamic.

another commenter writes:

Capital preservation is very similar to when one is playing a strong defensive game and in top shape. Even a player with a weak offense, if he has a strong defense, that and fortitude can grind the opponent down.

Alex Castaldo writes:

The business of money management requires two separate things: first the ability to attract (and retain) Other People's Money (OPM), and second the ability to successfully invest/trade. In my experience it is rare for one person to be good at both, so to have a successful firm you probably need some people who are good at one and some who are good at the other.

Raising money involves marketing skills and also good communication with the clients so you understand what the client wants and so you keep the client informed/reassured about what is going on (even when they should be worried instead!). Basically these are people skills.

For investing/trading on the other hand you need the ability to see things differently from others (so called "variant perception", seeing things that are true but that other people don't see). This skill is partly an intellectual skill and partly guts/courage to do things your own way rather than follow the consensus.

Feb

22

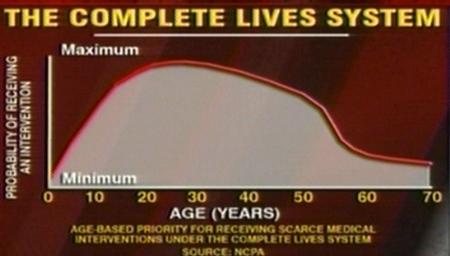

Found: A Libertarian MD Looks at the ‘Complete Lives System’, from Russ Herrold

February 22, 2013 | Leave a Comment

I came across these articles today, thinking about and researching what the health care system is going to look like, now that the Affordable Care Act is being rolled it.

I came across these articles today, thinking about and researching what the health care system is going to look like, now that the Affordable Care Act is being rolled it.

I formerly considered the 'health' part of my long term portfolio design a sector to emphasize, anticipating the bulge of the baby boomers turning into net health care 'over'-consumers, and in line with the long term move in the US economy to over-weight the health services sector, and the formality of that sector over the last fifty years to make sure a structured income stream is flowing into it without interruption

The article and the trail it leads to, point out that part of the healthcare delivery system is laying an 'allocation' formula, or 'curve' of who will get what level of care, over the span of their statistically projected lifetime (which 'manages' 'demand' for resources, rather than letting 'more free' market approaches prevail work) [1] [2]

I am not so sure that the sector was perhaps not 'too' successful, causing the emergence of a political will to put it under control of the central planners, and so ending that reason to over-weight it

1. "The "Complete Lives System"-why so little comment from the medical blogger world?"

Feb

22

Sinatra Has a Cold, from Pitt T. Maner III

February 22, 2013 | Leave a Comment

This is a nice piece of writing revisited, from an Alabama grad by way of NJ. A touch of the butterfly effect with the deleterious effects of reduced patronage suggested here. My Way or the highway–gangster-style resonations:

This is a nice piece of writing revisited, from an Alabama grad by way of NJ. A touch of the butterfly effect with the deleterious effects of reduced patronage suggested here. My Way or the highway–gangster-style resonations:

Sinatra with a cold is Picasso without paint, Ferrari without fuel — only worse. For the common cold robs Sinatra of that uninsurable jewel, his voice, cutting into the core of his confidence, and it affects not only his own psyche but also seems to cause a kind of psychosomatic nasal drip within dozens of people who work for him, drink with him, love him, depend on him for their own welfare and stability. A Sinatra with a cold can, in a small way, send vibrations through the entertainment industry and beyond as surely as a President of the United States, suddenly sick, can shake the national economy.

Read more: Frank Sinatra Has a Cold - Gay Talese - Best Profile of Sinatra - Esquire

Feb

22

Next Month, from Duncan Coker

February 22, 2013 | 1 Comment

No doubt that any cuts next month will be targeted to inconvenience the public most directly like travel, preferably during school breaks. After all if no one noticed what's to stop them from making, horrors, additional cuts.

Feb

21

James Wynne, from Victor Niederhoffer

February 21, 2013 | 1 Comment

James Wynne, my college roommate of 4 years, won the Russ Prize given every 3 years for invention of use of excimer laser surgery. The invention led to modern refractive surgery including PRK and Lasik. More than 25 million people have received Lasik therapy. Another winner of the Draper prize was a team of 5 who were the key to inventing the cell phone. The winners were Martin Cooper, Joel Engel, Richard Frenkiel, Thomas Haug and Yoshihissa Okumura. More then 6 billion people now have cell phones.

James Wynne, my college roommate of 4 years, won the Russ Prize given every 3 years for invention of use of excimer laser surgery. The invention led to modern refractive surgery including PRK and Lasik. More than 25 million people have received Lasik therapy. Another winner of the Draper prize was a team of 5 who were the key to inventing the cell phone. The winners were Martin Cooper, Joel Engel, Richard Frenkiel, Thomas Haug and Yoshihissa Okumura. More then 6 billion people now have cell phones.

The occasion was the National Academy of Engineering awards. On the trip to the awards, $500,000 each, I passed the BLS, and the Fed and the Service in succession. Much wailing in the paper was headlined over the coming sequestration and the terrible layoffs and reductions in budgeted salary increases. Who is to blame, the front page Post headline proclaimed. You could hardly pass a block in Washington where cranes were not aloft building new structures. What a contract of pride and revulsion I felt.

We stayed on embassy row, and the loathsome spectacle of zombies wearing necklaces holding their name tags, and multimillion dollar mansions containing every embassy under the sun, was broken in part by the sight of George Washington University students dining at Le Pain Quotidian and walking down Mass avenue as if they had not been already snatched.

Feb

21

Boom and Bust, from Gary Rogan

February 21, 2013 | 3 Comments

I came across this interesting graph, which isn't likely much of a surprise given where the market is these days–no fear and all is well in the world. What I don't get is that absent 1987, there are few drops in the trendline, and it's been a notable feast and famine starting in 1997 or so. Question from the ignorant: what happened in 1997? There was LTM in 1998, but the upswing seems to precede that.

{kind=link}

Jordan Neumann writes:

Asian currency crisis. Some on this site could tell you more about it.

Pete Earle writes:

Currency hi-jinks which began in Thailand, spread to Indonesia, South Korea, the Philippines, Malaysia, Singapore, Hong Kong, and resulted in a number of short, sharp recessions.

Gary Rogan writes:

I read something about that series of recessions a few months ago that seemed quite instructive to me. While there were a small number of countries that had what could be described as hi-jinks, most of them did not. The way global investors reacted was indiscriminate though, and they pulled out capital from anything that remotely resembled a dangerous Asian duck, whether or not it walked or quacked like one. This fear response can probably be generalized to how different panics start.

Feb

21

DIY Weapons of the Syrian Revolution, from Vince Fulco

February 21, 2013 | Leave a Comment

I found this article about DIY weapons of the Syrian rebels.

I found this article about DIY weapons of the Syrian rebels.

There is tremendous ingenuity there despite difficult odds especially as the EU and US yawn.

Were the pics only slightly different during the American Revolution?

Stefan Jovanovich writes:

Nothing happening in Syria matches the scale of the American revolution or its duration. It was not, in any sense, an uprising; it was a civil war comparable to the one that began in Britain in 1640 and it was fought between organized armies, both of which have current serving units that can trace their ancestry back to 1776.

Army National Guard and Active Regular Army Units

The American Revolution began with the New England militias and the Regular Army literally kicking the British out of Boston using artillery taken from Fort Ticonderoga and muskets that they already owned. What Washington struggled with for the rest of the war was the fact that the British were not going to stay gone but were going to use their Navy to come back. The fleet that arrived offshore in New York harbor was the largest amphibious invasion in human history - more men and more ship tonnage than the Mongols' attempted invasion of Japan, Alexander's siege of Tyre, Anthony and Augustus' triremes at Actium. It was also, by far, the longest voyage. That effort wasn't matched again in size and distance until the Allies landed in North Africa during WW II.

The financial scale is also one that we have difficulty understanding. The war lasted for over 6 years and took Britain to the edge of bankruptcy. For what became the United States the result was total insolvency.

Feb

21

Seba’s Curve, from Pitt T. Maner III

February 21, 2013 | Leave a Comment

It's time for another article roundup from me. This time around I found a couple of interesting articles related to universality.

1. "Spacing out: Plotting the distance between individuals"

"That internal calculation of impending impact kicks in and helps carve a comfortable space every time a starling swoops in to negotiate a spot on a wire and every time you pull up behind another car at a stop light."

2. "In Mysterious Pattern, Math and Nature Converge"

'In 1999, while sitting at a bus stop in Cuernavaca, Mexico, a Czech physicist named Petr Šeba noticed young men handing slips of paper to the bus drivers in exchange for cash. It wasn't organized crime, he learned, but another shadow trade: Each driver paid a "spy" to record when the bus ahead of his had departed the stop. If it had left recently, he would slow down, letting passengers accumulate at the next stop. If it had departed long ago, he sped up to keep other buses from passing him. This system maximized profits for the drivers. And it gave Šeba an idea.

"We felt here some kind of similarity with quantum chaotic systems," explained Šeba's co-author, Milan Krbálek, in an email.

Feb

19

Article of the Day: Do We Live Inside a Mathematical Equation, shared by Stefan Jovanovich

February 19, 2013 | 4 Comments

Do We Live Inside a Mathematical Equation?

BOSTON—From the arc of a baseball to the orbits of the planets, mathematical patterns are everywhere. But according to physicist Max Tegmark of the Massachusetts Institute of Technology in Cambridge, it's not enough to say that math governs our universe. Rather, he believes that reality itself is a mathematical structure. What the heck does that mean? We caught up with Tegmark after his presentation at yesterday's symposium "Is Beauty Truth?" at the annual meeting of AAAS (which publishes ScienceNOW).

Gary Rogan writes:

I have long believed that the most puzzling thing about the universe is that fundamental mathematical laws and constants seem to hold reliably over vast stretches of the universe. Until we understand how a photon "knows" that it needs to travels through vacuum at exactly the same speed everywhere in the universe, or why any two objects anywhere attract each other gravitationally with exactly the same exponent attached to the distance between them and exactly the same constant attached to that equation, and any number of such things, we are just observing the symptoms of something on a deeper and deeper level without understanding how the whole thing is constructed. Sooner or later this has to come down to some fantastic explanation, like a single basic particle "painting" the universe on its own timescale, or every fundamental particle simultaneously communicating with every other fundamental particle to maintain consistency, or the universe being constructed on some level via a very small number of types of discreet building blocks that are completely invariant.

David Lillienfeld writes:

That's the one issue I have with the Big Bang–where did all that energy come from?

Gary Rogan writes:

Well, that's just one issue of several with the Big Bang, like

-What caused it to occur?

-What was there before it?

-How did all the physical constants settle on particular values (regardless of consistency)?

The Big Bang is just another descriptive theory of the form "the universe behaves according to these laws", but provides no explanation for the "why?" on the fundamental mathematical level. And no, religion doesn't help. The "global computer simulation" theory is highly attractive: constant laws and constants across time and space and a definitive beginning out of nothing with a lot of energy are just so easy to explain!

Gibbons Burke adds:

Further, why are all the physical constants so precisely dialed in that if any one of the 30 or so parameters which define the immutable characteristics of the universe so tightly dependent that a variation in any one of those parameters, to one part in a million, would make life, or indeed the universe, impossible?

Feb

19

Israel Turkey Relations and Natural Gas, from David Lilienfeld

February 19, 2013 | Leave a Comment

It seems Turkey and Israel are patching up their recent spat with some arms deals. At one time, Turkey and Israel were close–so much so that when the recent earthquake hit, Israel was the first country to extend aid, something which was approvingly noted in Turkey's newspapers. However, since 2010, when the Israel Navy stopped an effort backed by a Turkish foundation to break the Gaza quarantine, relations between the two nations have been tense. (Relations were already somewhat troubled, but it was only after the incidence that ambassadors were withdrawn.)

It seems Turkey and Israel are patching up their recent spat with some arms deals. At one time, Turkey and Israel were close–so much so that when the recent earthquake hit, Israel was the first country to extend aid, something which was approvingly noted in Turkey's newspapers. However, since 2010, when the Israel Navy stopped an effort backed by a Turkish foundation to break the Gaza quarantine, relations between the two nations have been tense. (Relations were already somewhat troubled, but it was only after the incidence that ambassadors were withdrawn.)

Why do I bring this to attention, particularly to this site about markets? Natural gas, and possibly oil. For anyone investing in the energy arena, with the exception perhaps of electric power, the Eastern Mediterranean is–or should be–of interest. When Turkey and Israel were on the outs, Israel approached Cypress seeking a deal on who had rights to what part of the offshore natural gas fields and constructing a pipeline through Cypress to Europe.

Turkey wasn't pleased with this development, since it claimed the northern part of the fields for itself (Lebanon has also staked a claim, but no one seems to be paying much attention to it). Things got sufficiently tense last year that when an exploration rig left Israel for further explorations in these fields (in the hope of find oil and not just natural gas) last year, Turkey dispatched two ships from its navy to "patrol" the northern fields it had claimed. What the ships would have done had the rig gone into those northern fields is unclear.

At the same time, Turkey has played a key role in helping Iran work around the economic sanctions imposed by the West as a means of stopping Iran's effort to build a nuclear bomb. Hence, the surprise of Israeli weapons sales to Turkey (particularly given the concerns about the weapons going to potential terrorists), not to mention Turkish efforts to secure Israeli natural gas.

These natural gas fields are estimated to be large–not yet at the level of the Qatari ones, but the estimates have been increasing with each new exploration well drilled. Noble Energy has a big interest in these fields, and so does one of the majors (I think it may be Chevron, but I'm blocking on which one in specific).

Feb

19

Great Books Programs, from Gibbons Burke

February 19, 2013 | 2 Comments

A Great Books program is designed to teach history by having first-hand experience reading the primary works of thinkers upon whose shoulders the edifice of Western Thought rests. The works are to be read in chronological order, to the ideas are arranged and built in the mind in the order by which Western Civilization was built. They are like building blocks.

A Great Books program is designed to teach history by having first-hand experience reading the primary works of thinkers upon whose shoulders the edifice of Western Thought rests. The works are to be read in chronological order, to the ideas are arranged and built in the mind in the order by which Western Civilization was built. They are like building blocks.

Listening to a re-digested synthesis of all that material, selected and edited and interpreted according to some unknown theory (but likely, given today's academic gestalt to be a form of Marxism) and regurgitated into your earphone by a for-profit company undermines the very idea of the program.

Fortunately most of the Great Books are out of copyright, and so may be downloaded and read at no cost from Project Gutenberg, and that reading greatly aided by the electronic resources for learning and contextualizing available at one's fingertips in most capable ebook readers (highlighting with auto-compiled indexes of highlights, wikipedia search, web search, Google Maps).

The reasonable excuses for ignorance in this world, apart from apathy, sloth, incorrigible stupidity, and willfulness, are quickly becoming endangered species in this Brave New World, and are on the brink of extinction.

Feb

18

Idiocracy, from Dan Grossman

February 18, 2013 | 3 Comments

Last night Elizabeth and I watched the 2006 Mike Judge movie Idiocracy, available on Amazon prime streaming.

Last night Elizabeth and I watched the 2006 Mike Judge movie Idiocracy, available on Amazon prime streaming.

It is not great cinema and only mildly funny, but it's the most subversive, un-PC movie I've ever seen. The story is based on reasonably accurate reverse eugenics (dysgenetic?) of the country becoming genetically stupider. More relevant today than when made because of all the current talk about Hispanics and even the Republican Stupid Party having to transform itself to appeal to Hispanics, the movie features a President Camacho.

Supposedly Fox wanted to bury the movie, only doing its contractual minimum in theatrical release, with no trailer promotion or screenings for critics, and open in minimal cities. But it has apparently acquired something of a cult following, with DVD revenues now nine times the theatrical.

Anyway, I was amazed how honest (if you have any fear IQ in the country is genetically declining). Although I guess the usual MSM critics, instead of having a fit over it, either didn't see it, or thought it was somehow a proponent or example of the stupidity that the movie was satirizing.

Feb

18

Fairness Day, from Stefan Jovanovich

February 18, 2013 | Leave a Comment

Last Friday, February 15th, should be at least one of the minor memorial days for the Law is Fairness doctrine. Ronald Dworkin's obituary made the Telegraph, and John Burt's book on Lincoln was reviewed by the WSJ. For those of you who are not besotted by the Constitution, this may not mean anything; but for us few remaining Neanderthals it is another reminder of how how pernicious modern legal scholarship has become. Dworkin believed with all his heart that the U.S. Constitution existed to "benefit society not just by providing predictability and procedural fairness, or in some instrumental way, but by securing a kind of equality among citizens that make their community more genuine and improves its moral justification for exercising the political power it does". Professor Burt remains convinced that freedom is really just a "code word" for "racism" (whatever that means) and that markets function only as a form of "Darwinist brutality."

Last Friday, February 15th, should be at least one of the minor memorial days for the Law is Fairness doctrine. Ronald Dworkin's obituary made the Telegraph, and John Burt's book on Lincoln was reviewed by the WSJ. For those of you who are not besotted by the Constitution, this may not mean anything; but for us few remaining Neanderthals it is another reminder of how how pernicious modern legal scholarship has become. Dworkin believed with all his heart that the U.S. Constitution existed to "benefit society not just by providing predictability and procedural fairness, or in some instrumental way, but by securing a kind of equality among citizens that make their community more genuine and improves its moral justification for exercising the political power it does". Professor Burt remains convinced that freedom is really just a "code word" for "racism" (whatever that means) and that markets function only as a form of "Darwinist brutality."

The belief that the Constitutions of our Union were, as written, the "law of the land" is probably the only religion that Abraham Lincoln had. He used the vocabulary that Washington and Grant did and spoke and wrote regularly about Almighty Providence; but he did not have the soldier's acceptance of fate. What he did believe was that the Constitutions were sacred documents because they represented, in tangible form, the will of the People. However, for those of us who remain anarchist enough to think that the only foundation of "the law" in this country is the United States Constitution and the Constitutions of the various states, as written. The resonance of the words in Gettysburg Address is real because it is Lincoln's own catechism as an American: "that this nation, under God, shall have a new birth of freedom—and that government of the people, by the people, for the people, shall not perish from the earth." "Fairness" - in the communitarian sense of let's all share the rich guys' stuff so dear to academics and intellectuals everywhere - was not even mentioned.

Feb

18

Call it a Cascade, from Victor Niederhoffer

February 18, 2013 | Leave a Comment

Call it a cascade or call it the conservation of energy, or call it signaling or money outflows—- But the decline of 60 bucks of gold in a week to below 1600 intra day sends the storm signals up. It could happen while one was long. I looked at the effect of gold down 60 bucks in a week as of a Friday. And it's happened 18 times in last 13 years. It seems to have no inordinate effects statisticlly– being bearish for the stocks and oil and bullish for the dollar and bonds and gold in the next few days and someewhat bullish for the stocks on a 2 week basis.

Call it a cascade or call it the conservation of energy, or call it signaling or money outflows—- But the decline of 60 bucks of gold in a week to below 1600 intra day sends the storm signals up. It could happen while one was long. I looked at the effect of gold down 60 bucks in a week as of a Friday. And it's happened 18 times in last 13 years. It seems to have no inordinate effects statisticlly– being bearish for the stocks and oil and bullish for the dollar and bonds and gold in the next few days and someewhat bullish for the stocks on a 2 week basis.

Anatoly Veltman writes:

Ok, so you did derive those slight biases you mention. But how is "60 bucks", and exactly Fri-to-Fri supposed to be a determinant? 60 bucks 13 years ago would be 20% depreciation; while today it's less than 4%. A few mega-funds like Pimco, Bridgewater, Paulson were not in gold until a few years ago. China, Russia were not significant players until a few years ago. EU was not in liquidity crisis until a few years ago. Cash gold was not above Comex gold. The dollar/gold relationship has waffled between negative and positive corellation last few years. There were no QE-infinity until a few years ago, no ZIRP. What if the entire this week's slide was due to China market holiday? There are just too many cross-currents for this kind of 13-year statistical sampling. Unless significantly fine-tuned, the conclusions will inevitably be of little use.

Feb

18

Land in Detroit, from David Lilienfeld

February 18, 2013 | 4 Comments

Does anyone know anything about housing values in Detroit? Of particular interest are empty lots.

Victor Niederhoffer writes:

30 bucks will get you a good abandoned big home without the copper. Reason has a very good video on the bargains among the abandoned and its causes from excessive service rates and unionization. Chicago is the next Detroit I'm told.

David Lilienfeld writes:

I ask because a good friend of mine, a little older, is an ophthalmologist who bought four adjacent lots off of Woodward (?) near the center of town. The cost was practically nothing. Two of the lots are empty, the other two have abandoned homes (he compared them to Ridgely's Delight (in Baltimore) in the 1960s–that area of the city was in pretty poor shape at that time. The lots themselves are "big". Marty's thinking of when he can turn his practice over to his son and retire. (I can't picture Marty retired. The man runs on adrenaline and his great rapport with his patients. He would have gone into cardiology, but he thought ophthalmologists were paid more and didn't have to work as hard–leaving him time for his woodworking and a bunch of other hobbies.) He hopes to build a "large" house on the property sometime in the next 5-10 years as a summer home. I think he's crazy, but given his investing record, which is pretty good, I have to wonder if he's just really early, nuts, or onto something. Hence, my question.

GM and Ford do seem to be on the rebound, though. What's on the rebound in Chicago, except for gun sales?

Ralph Vince writes:

I imagine it is much like Cleveland, where you can buy property for the back taxes owed. Young people not taking advantage of this are silly.

The mineral rights under most of these places, eventually, exceeds the cost

Feb

18

The Importance of Being Well-Stacked, from Pitt T. Maner III

February 18, 2013 | Leave a Comment

As a geologist whose first job was returning library books to shelves and who later had stints as a bag boy in an uncle's grocery store, I would be the last to underappreciate the efforts of the stacking professions. The following quote, however, is quite amusing on many levels:

As a geologist whose first job was returning library books to shelves and who later had stints as a bag boy in an uncle's grocery store, I would be the last to underappreciate the efforts of the stacking professions. The following quote, however, is quite amusing on many levels:

"The next time somebody goes in - those smart people who say there's something wrong with this - they go into their supermarket, ask themselves this simple question, when they can't find the food they want on the shelves, who is more important - them, the geologist, or the person who stacked the shelves?"

But egads, what would the "snobbish"and "useless" job seeker do without the beneficence of the government secretary? After all making men small and needy is hard work.

Can one say the odds are stacked against you in finding suitable employment in the UK?

Heaven knows, the unimaginable waste of geological talent out in the North Sea that could be put to productive stacking is absolutely appalling!

Feb

18

Looking for Development Examples, from Richard Owen

February 18, 2013 | Leave a Comment

If folks would be so kind: could they name their favorite examples of intelligent and rapid economic development of poor countries (but with reasonable educated workforces, so you're not starting with e.g., Afghanistan)?

Famous examples are: Singapore, HK (although these have a unique entrepot status, and therefore wider learnings are not so great?). And then South Korea was impressive.

And of course China, but this was so big and diverse that its hard to reapply. I am looking for more "turnkey" type stories.

Those few examples went totally against the "Washington consensus" for many of their policies, much to their benefit.

Any further case studies people would recommend?

Many thanks.

Gary Rogan writes:

Chile and the Chicago Boys come to mind.

Jan-Peter Janssen writes:

I recommend looking at Estonia. It's a tiny Baltic state which is remarkably advanced in IT . Skype was invented in Estonia. Programming is taught at school from age seven. The government aims to reduce bureaucracy through a so-called eGovernment. It is linguistically and culturally close to Finland (where Nokia is from) and together these two nations should have the critical mass of talents needed to create a high tech industry.

Estonia is ranked the world's 13th freest by Heritage Foundation.

Richard Owen writes:

Ok, here is a consolidated list of suggestions. Thanks to all.

Estonia

Tysons Corner, VA

Reston, VA

Japan WWII

Chile

Poland (Mazowiecki)

Latvia in 90s

Drexel Burnham under Mike Milken

Jaimaica vs. Singapore

Taiwan

Vietnam

Mauritius

Feb

18

Meteor Aftermath, shared by Pitt. T. Maner III

February 18, 2013 | Leave a Comment

"Russians Wade Into the Snow to Seek Treasure From the Sky"

"Villagers here have plastic bags, matchboxes and jars filled with dozens of stones. One even tore a hole in the coat one woman was wearing outside Friday morning.

But this is Russia, so the excitement became tinged with anxiety on Monday as unknown cars appeared, cruising the streets and bearing men who refused to answer questions but offered stacks of rubles worth hundreds, then thousands, of dollars for the fragments. Strangely, no authorities were anywhere in sight. "

Feb

18

It was Surprising to Hear, from Victor Niederhoffer

February 18, 2013 | Leave a Comment

It was surprising to hear that in the new book about being smart (and a world traveler), he talks about losses, as I have never heard him acknowledge a loss before, and he seems the most insecure and least humble of men. The loss must have been of the kind that Harry Brown writes about "we said gold would go to 950 from its then current level of 450, but we were wrong as it only fell to 450 before rising to the specified level". The false humility of it all. Similar to the Palindrome. "Well, my. This man is so honest and so good. If he calls it a mistake to just miss it by 10 bucks, imagine what he must make when he's right. I'll invest with him immediately". The perfect lie often starts with a false admission of wrongness to throw the victim off the track. Cole Porter was a master of this, i.e. his admission that he was a captain in the french legion "only because they wanted to have an American in the force". Of course, he never got near the French legion and was there to evade the draft and of course the other thing he liked to do at night. img.imageResizerActiveClass{cursor:nw-resize !important;outline:1px dashed black !important;} img.imageResizerChangedClass{z-index:300 !important;max-width:none !important;max-height:none !important;} img.imageResizerBoxClass{margin:auto; z-index:99999 !important; position:fixed; top:0; left:0; right:0; bottom:0; border:1px solid white; outline:1px solid black;}

It was surprising to hear that in the new book about being smart (and a world traveler), he talks about losses, as I have never heard him acknowledge a loss before, and he seems the most insecure and least humble of men. The loss must have been of the kind that Harry Brown writes about "we said gold would go to 950 from its then current level of 450, but we were wrong as it only fell to 450 before rising to the specified level". The false humility of it all. Similar to the Palindrome. "Well, my. This man is so honest and so good. If he calls it a mistake to just miss it by 10 bucks, imagine what he must make when he's right. I'll invest with him immediately". The perfect lie often starts with a false admission of wrongness to throw the victim off the track. Cole Porter was a master of this, i.e. his admission that he was a captain in the french legion "only because they wanted to have an American in the force". Of course, he never got near the French legion and was there to evade the draft and of course the other thing he liked to do at night. img.imageResizerActiveClass{cursor:nw-resize !important;outline:1px dashed black !important;} img.imageResizerChangedClass{z-index:300 !important;max-width:none !important;max-height:none !important;} img.imageResizerBoxClass{margin:auto; z-index:99999 !important; position:fixed; top:0; left:0; right:0; bottom:0; border:1px solid white; outline:1px solid black;}

Feb

18

An Interesting Aspect, from Victor Niederhoffer

February 18, 2013 | Leave a Comment

An interesting aspect of the asymmetry between big mimina and big maxima in stocks is that given that the last 20 day minimum occurred from 5 to 100 days ago, the expected duration to the next minimum is 30 days whereas the comparable for 20 day maxima is 15 days.

Feb

18

Weekly, One Looks at Israel’s Market, from Victor Niederhoffer

February 18, 2013 | 3 Comments

Weekly, one looks at Israel's market for benchmarks and guidance as they read our mail and are so much more scholarly than we. And to do it, I often scroll through 100 returns for every world market. In looking at these, one notes that about 90 of the markets are performing significantly worse year to date than the US. Canada and Europe are up 2% on the year to unchanged versus our up 6% are typical. Only Japan is up 10% and a few Arab countries are in our ball park. In conjunction with the run 20 percentage point increase in stocks relative to bonds, and the duration of 75 days since bonds set a big max, and the dissipation of wealth in the long precious metals, and the incredible run of max after max in US stocks, and the little woman's (who is very sagacious and always gives me good advice about the market) waving of the sceptre each morning over the head "but dear, yes. You're making, but what happens when it goes down 100 points 5 days in a row. Don't give it all back", one is somewhat less exuberant than one would be without all these Cassandra like warnings. If all my kids start calling me saying that they notice they have a few bucks in money markets receiving 0% interest, and should they invest in stocks, like they did at the height of 6000 nasdaq in 2000, then I'll know it's time to join Maturin in leaning over the boat and noting the behavior of the flying fish. Hopefully, I will take my shoes off if I fall in the water.

Weekly, one looks at Israel's market for benchmarks and guidance as they read our mail and are so much more scholarly than we. And to do it, I often scroll through 100 returns for every world market. In looking at these, one notes that about 90 of the markets are performing significantly worse year to date than the US. Canada and Europe are up 2% on the year to unchanged versus our up 6% are typical. Only Japan is up 10% and a few Arab countries are in our ball park. In conjunction with the run 20 percentage point increase in stocks relative to bonds, and the duration of 75 days since bonds set a big max, and the dissipation of wealth in the long precious metals, and the incredible run of max after max in US stocks, and the little woman's (who is very sagacious and always gives me good advice about the market) waving of the sceptre each morning over the head "but dear, yes. You're making, but what happens when it goes down 100 points 5 days in a row. Don't give it all back", one is somewhat less exuberant than one would be without all these Cassandra like warnings. If all my kids start calling me saying that they notice they have a few bucks in money markets receiving 0% interest, and should they invest in stocks, like they did at the height of 6000 nasdaq in 2000, then I'll know it's time to join Maturin in leaning over the boat and noting the behavior of the flying fish. Hopefully, I will take my shoes off if I fall in the water.

Rocky Humbert writes:

Well put. Alas, the wife of the man who is long S&P calls because he sees little if any value in stocks (or bonds either for that matter, but accepts that the market is always right and he doesn't fight the fed or fight his wife) is already asking, "after the market goes down 100 points 5 days in a row, is that time to sell or time to buy?" The trendfollower replies, "depends on your timeframe."

Feb

15

A Housing Anecdote, from David Hillman

February 15, 2013 | Leave a Comment

For about 3 years, I've been monitoring the trend in public notices of foreclosures and sheriff sales in the local newspaper. These have gone from nearly a full section 2-3 years ago, to several pages a year ago, to near zero today. Similar observations in other locals while traveling have been made.

For about 3 years, I've been monitoring the trend in public notices of foreclosures and sheriff sales in the local newspaper. These have gone from nearly a full section 2-3 years ago, to several pages a year ago, to near zero today. Similar observations in other locals while traveling have been made.

It looked a couple of years ago that goo would be flushed from the system by the second half of this year. The upward trend in new construction, home prices and building materials in the last half of last year caught me by surprise as well.

Out here in the boonies [at least in my boonies], we were not hit nearly as hard as the coastal regions in either the housing or employment markets. In reviewing and measuring housing, let's not forget……geography matters, as does what is selling.

I wanna think maybe this is a combination of having paid down or reorganized our debt, learning our lesson about over-extending and being house-poor, having begun to save and invest and spend more wisely again, and with the market up we're feeling better about our fortunes and the future, we notice there are still vestigial housing deals out there as well as new ones, recognize they might not be there for long as home prices are increasing, and figure the time is right to buy again. Kind of like recognizing a market bottom has occurred and buying in at the beginning of the upswing.

I don't think this is a head fake, but a certain amount of prudence is not ill-advised, because, as we saw in 2007, nothing lasts forever.

Henry Gifford writes:

One time I was negotiating to buy a house and I told the seller "Your house is in mint condition." The broker in the background was cringing, and repeatedly recommended I hire a home inspector, and the only thing that would quiet her down was explaining that the home inspectors have an association, which has a magazine they read to learn about what to look for when they inspect a house, and the latest issue had a cover article I had written.

I told the seller I was going to make an offer to the realtor within the hour, and my offer would be contingent on me not dying. No mortgage contingency, no inspection, no nothing. We agree, we sign, we close.

My offer was lower than other offers that day. We closed soon after without hassle.

When selling property I generally ask for an "as is" contract, to avoid the games.

The legal side of it all says that a seller is more obligated than a buyer because "specific performance" says the seller is promising something very specific (a unique house) while they buyer is not. As a practical matter, a buyer can threaten to sue for some obscure term of the contract, tying the property up indefinitely if they are not refunded all their money.

It is all just another way honest people are at a huge disadvantage in life, but it is the life I have chosen.

Jim Lackey writes:

A hold back near nashvegas: rent exceeds the cost of carry here. Even @ 0% down FHA rate + tax tag and title (yet minus the unknowable maintain costs) if you rented it yourself, no management fees, i.e, rent 1500 per month, cost of carry 1200 on 4br all brick nice hood and schools. Yeah, if it was a cash buyer it is grocery store, wait AMZN margins so it can trade 100X earnings. lol. I just figured it out as a few of my friends have moved (bought new new) and held on to their old house and we have renters in the hood. Yet, it's still cheaper to buy new vs. used. Hipsters are in deep buying East Nashville tear down/ guy rebuild. My buddy told me it was dead 20 years ago. His new wife as a college kid bought dead homes for 3,000 bucks. Yes, you can imagine correctly.

Feb

15

Near Misses, Misses and Big Impacts, from Pitt T. Maner III

February 15, 2013 | Leave a Comment

Today was a rather interesting day for astronomers… with a bit of Russian deja vu and dinosaur demise added in for good measure. Here is my round up of multiple links for you all. Click on the numbers for the links.

The Near Miss "Asteroid 2012 DA14 is about 150 feet (45 meters) in diameter. It is expected to fly about 17,200 miles (27,000 kilometers) above Earth's surface at the time of closest approach, which is about 11:25 a.m. PST (2:25 p.m. EST) on Feb. 15. This distance is well away from Earth and the swarm of low Earth-orbiting satellites, including the International Space Station, but it is inside the belt of satellites in geostationary orbit (about 22,200 miles, or 35,800 kilometers, above Earth's surface.) The flyby of 2012 DA14 is the closest-ever predicted approach to Earth for an object this large."

"A meteorite shot across the sky in central Russia early on Friday and sent fireballs crashing to Earth, smashing windows, setting off car alarms and injuring 150 people.

Residents heard what sounded like an explosion, saw a bright light and then felt a shockwave as they went to work in Chelyabinsk, according to a Reuters correspondent in the industrial city 1,500 km (950 miles) east of Moscow."

"Some of the numerous videos that quickly emerged of the incident highlighted a distinctly Russian phenomenon: the dashboard cam. As Business Insider recently pointed out, they are commonplace in Russia partly because of the dangerous driving conditions that lead to so many accidents, and with an unreliable police force such cameras can provide valuable evidence following a crash."

4.

Tunguska 1908

"The year is 1908, and it's just after seven in the morning. A man is sitting on the front porch of a trading post at Vanavara in Siberia. Little does he know, in a few moments, he will be hurled from his chair and the heat will be so intense he will feel as though his shirt is on fire.

That's how the Tunguska event felt 40 miles from ground zero."

Past extinction event

A) "UC Berkeley researchers have discovered new evidence linking an asteroid impact to the extinction of the dinosaurs.

UC Berkeley Professor Paul Renne and a team of researchers, using isotope analysis, have found that both an asteroid impact and the extinction of the dinosaurs took place nearly synchronously 66 million years ago."

B) Abstract for Renne's work

"Mass extinctions manifest in Earth's geologic record were turning points in biotic evolution. We present 40Ar/39Ar data that establish synchrony between the Cretaceous-Paleogene boundary and associated mass extinctions with the Chicxulub bolid

Feb

14

One Sees That, from Victor Niederhoffer

February 14, 2013 | 2 Comments

One sees that he has called for an increase in the minimum wage. It will be interesting to see the annual economic report that usually accompanies The State of the Union and see how economists can show that raising a cost like this will not lead to decreased employment and layoffs for the unskilled. Economists are no better than the aforementioned counselors who tortured and ruined the Biker's whistleblowers it would seem. Indeed, as Rabelais would say, almost all of our professions are as laughable and flawed but wonderful as well as the economists and counselors.

One sees that he has called for an increase in the minimum wage. It will be interesting to see the annual economic report that usually accompanies The State of the Union and see how economists can show that raising a cost like this will not lead to decreased employment and layoffs for the unskilled. Economists are no better than the aforementioned counselors who tortured and ruined the Biker's whistleblowers it would seem. Indeed, as Rabelais would say, almost all of our professions are as laughable and flawed but wonderful as well as the economists and counselors.

anonymous writes:

I only listened to a part of the speech but from what I understand he, and the rebuttals that will/did follow will all try to outbid each other about calling the illegals "immigrants" who are welcome like the high achievers that they are. As Milton Friedman said, you can you can have open borders or you can have the welfare state, but you cannot have both. When 10-20 million are legalized and are finished bringing in the 50 million with family reunification and 30 million of the total will go on welfare with five kids per couple this will dwarf all the other nonsense. This is clearly not sustainable.

Stefan Jovanovich replies:

Apologies to anonymous for this mini-rant. The United States never had "open borders" any more than it had "free trade". What it did have in the 19th and early 20th centuries were very straigntforward rules about what people and goods had to do to cross the border. People had to pass physical health inspections (1 out of 5 did not), and goods had to pay a tariff. If you did not have tuberculosis or syphilis, you got in; if your importer paid the duties, your goods could be sold here. There was no presumption that having the right to live in the United States entitled someone to vote; that required the same citizenship examination that people now have to pass and a period of residency without being found guilty of a criminal offense (the definition included the non-payment of taxes). To be eligible for what the Constitution calls "Naturalization" a person also had to have no criminal record and avoid being placed on the attorney general's blacklist. Neither of my paternal grandparents ever became a citizen. My grandfather did not because he had been on the blacklist for being an anarchist. He was one; like Bakunin he thought that nothing could justify oppression, whether it was in the name of country (vide the Russians keeping down the Poles) or in the name of the revolution (Nechayev and Marx's authoritarian socialism). Grandmother's explanation was simpler; she never learned to read English or Polish, for that matter. (She suffered from severe dyslexia.)

My grandfather never thought he had been oppressed by the government for their failure to allow him to vote. He never considered the United States his homeland; but it was his children's, and he thought that he had an obligation to defend their country so, in December 1941, after they were all grown adults, he tried to join the Marine Corps. They turned him down (he was 52); but the Navy Department did accept the enlistments of all 3 of his children. He would have laughed at the notion that the United States had an obligation to allow people who broke the law - both by coming to the United States illegally and by committing crimes after they were here - to become citizens. If the country decided that these people could stay, that was up to the decision of the citizens; but he would have considered it a grave insult if other people had been allowed to become citizens after breaking the law or being illiterate in English. As a peaceful revolutionary (the very kind all the Marxists love to despise), he believed that "if you won't do the time, you don't have the character for crime". Surely, the same rule should apply to all current illegals.

Feb

14

How to Detect an Avalanche, from Jim Sogi

February 14, 2013 | 1 Comment

I'm in Valdez Alaska. It snowed 2 feet the day before I got, here, and 3 feet the day I got here, and 2 feet today, and it's still snowing. When backcountry skiing, avoiding avalanches is a constant concern and a matter of life and death. I've talked to a few real experts on the subject here, Dean Cummings, former World Extreme Ski 2nd place champion and owner of H2O Heli ski, and Matt Kinney.

I'm in Valdez Alaska. It snowed 2 feet the day before I got, here, and 3 feet the day I got here, and 2 feet today, and it's still snowing. When backcountry skiing, avoiding avalanches is a constant concern and a matter of life and death. I've talked to a few real experts on the subject here, Dean Cummings, former World Extreme Ski 2nd place champion and owner of H2O Heli ski, and Matt Kinney.

One of the basic ways to understand the snowpack and the potential danger of avalanches is to dig a pit in the snow and examine the layers of snow over the season and test its structural properties. Snow, when viewed cut away in a pit, shows the layers of snow over the season like the rings of a tree, exposing the various attributes of the snow. One of the things to look for is a weak layer in the snow, such as a layer of ice formed by rain or sun melt, or powdery sugar snow called hoar frost. The other thing to look for is slab formation caused by wind blown snow. The danger is when a slab slides on a layer of ice, or sugarlike snow and forms an avalanche.

The pit exposes the layers and the skiier examines each layer by touching it to feel its consistency. The skiier then isolates a 1 or two foot wide column of snow which can be 240 cm tall where that is the depth of the snow. After tapping the top and counting the number of taps, if the column of snow collapses at the icy or sugary layer, it is a sign of weakness in the snow, a potential place where an avalanche might trigger at the weak layer in the snow structure. Avalanche experts use microscopes and examine the snow crystals and see how they have metamorphed over time with temperature. A pit is only a snap shot of the snow in one area of the mountain and the snow cannot be assumed to be the same elsewhere, but it gives information about the relationship of the layers.

I could not help to think of the similarities in the historical evidence of snow to the order book. I wish one could look to see the structure of the entire order book up and down the prices. Especially nowadays with computer traders, the order book rapidly and constantly changes, but there would be information in the changes in the order book. There would be weak layers, or strong layers in the book. There may be structures in the order book near or around round numbers, and in time around announcements, closings. Even better would be to see whose orders there were. I've read that CME full members can see the tags identifying the order makers' identites. I'm sure the complete order book is available to someone somewhere, perhaps the market makers see this. Without the information it feels like flying blind sometimes. It certainly would be an advantage.

Feb

13

Racquet Grip Glue and the One-Grip System, from Bo Keely

February 13, 2013 | Leave a Comment

The bent handle racquetball racquet of the early 80’s reminds me of a one month experiment with every type of adhesive on the market, about thirty in all from Elmer’s to Superglue, using various styles of gloves and racquet grips to stop grip slippage. I recognized with the onslaught of the fast ball and tightly strung racquets of the early 80's that the primary problem of most players in their entire games was ball deflection on contact due to grip slip.

The bent handle racquetball racquet of the early 80’s reminds me of a one month experiment with every type of adhesive on the market, about thirty in all from Elmer’s to Superglue, using various styles of gloves and racquet grips to stop grip slippage. I recognized with the onslaught of the fast ball and tightly strung racquets of the early 80's that the primary problem of most players in their entire games was ball deflection on contact due to grip slip.

It started moments after the coin toss in tournaments when the glove, hand and handle got sweaty. Everything in the strokes and strategies of millions of advanced players across the nation was right except the angle the ball came off the strings. Given a good eye or fast camera, the handle rolled about two degrees within the strongest palm. Even power racquetball’s inventor Marty Hogan screamed at the injustice. I needed a glue to stop it. Over the course of a month in my secret 'laboratory' of a Michigan garage via tedious daily hours of applying adhesives to gloves, my palm and handle, I gripped and formed opinions of the best glues… and went to the courts to test them. The best was Barge Cement and to this day I keep a quart on my desert property for all purpose contact.

The result of the glue experiment was conclusive for cement type, but over a period of ten minutes of hard play though the grip didn't slip twixt the glove and handle, it started to rotate between the hand and glove for the same misdirection. Gluing the hand to the racquet was the logical next step which I did for a new one grip system for forehand and backhand. Yet I couldn't let go during timeouts, plus the heating glue felt unhealthy climbing my circulation from palm to armpit, so I abandoned the idea of gluing the hand to handle.

The nationwide grip slippage of the early 80's due to the advent of superballs, tight strings, Tarzans hands, and double ball speeds I believe to this day is the prime reason for the concurrent historic introduction of the one-grip system that previously was all but unknown in racquetball.

Feb

13

The Doormat, from Craig Mee

February 13, 2013 | Leave a Comment

It's amazing how the general public, mostly low risk takers and even those who are relatively well off, will swoon around those that are perceived to be in another stratosphere in wealth, no matter their line of business.

It's amazing how the general public, mostly low risk takers and even those who are relatively well off, will swoon around those that are perceived to be in another stratosphere in wealth, no matter their line of business.

Glamour and dreaming allows people to escape, and it would seem the swooning is some selfishness on the publics behalf, allowing them to ponder a life less worked.

It makes sense that the man devoting his life to others allows for a lot less interest unfortunately.

This human trait probably allows traders to gain an edge, as the public wash from one latest craze to another, and nobody likes the doormat, on its lows, going nowhere fast.

Feb

13

A Whisper in Market Breezes, from Carder Dimitroff

February 13, 2013 | Leave a Comment

Beware the Ides of March. They come to demonstrate, not to legislate.

As damages are tallied, cash becomes king.

Opportunities abound as rubble is cleared. Swept away will be demonstrators, who rue the day they forced a great nation to the edge of the abyss.

Feb

12

Cultural Clues, from Richard Owen

February 12, 2013 | 2 Comments

Queen's Lady Gaga was a huge hit globally. It was beloved in the UK. It was Queen's major seller before their "live aid" moment which spurred them on to their greatest album and peak success.

Queen's Lady Gaga was a huge hit globally. It was beloved in the UK. It was Queen's major seller before their "live aid" moment which spurred them on to their greatest album and peak success.

I recently read, however, that it was a dud in the USA. Queen had been on the ascendant there. Thereafter, their name in the US was on a downward spiral. Which was aberrational as Queen were major sellers in pretty much every major western country.

Why? Apparently the comedic video, featuring the band all dressed up as women, left Americans with a funny feeling in their gut.

I guess to politics, religion and honeys one needs to add humour?

The market equivalent would be Blackstone (i) buying Celanese in Germany, (ii) fussing around and doing some jazz hands in the interim, and then (iii) reselling the same company in the USA for twice the price.

Feb

11

This History of Racketball and Markets, from Victor Niederhoffer

February 11, 2013 | Leave a Comment

While most of you don't play racketball, I believe the hobo's history of racketball on site was very educational for those with kids who wish to play it or anyone who plays any racket sport. The torque and the backswings on the backhand and the bends in the pictures are most enlightening. One notes that there have been 4 champions who ruled the racketball world for about 5 years each, winning almost every tournament. I noted the same thing in squash, and tennis isn't too far away in that area also.

While most of you don't play racketball, I believe the hobo's history of racketball on site was very educational for those with kids who wish to play it or anyone who plays any racket sport. The torque and the backswings on the backhand and the bends in the pictures are most enlightening. One notes that there have been 4 champions who ruled the racketball world for about 5 years each, winning almost every tournament. I noted the same thing in squash, and tennis isn't too far away in that area also.

One wonders if a similar phenomenon relates to markets. e.g. is there one stock that can outclass all the others in performance for a certain number of years, like Hogan, Swan, and Kane. Eventually those champions receded due to age, competition, or injury. Is there a predictable turning point?

Alston Mabry writes:

Obviously, AAPL is the current version of this. And looking at AAPL, one sees an example of a company that stumbles as it fails to effectively deploy the very capital it accumulates due to its success.

A commenter writes:

This is the measure of how good a CEO Jobs was. He may have been a great innovator and manager, but he may not have been that strong of a CEO. A good CEO assures succession, and it isn't clear that Jobs was successful in this regard. The same was true of RCA and David Sarnoff, By comparison, Alfred P. Sloan accomplished this task for GM, Adolph Ochs for the NY Times, Hershey with Hershey Foods, and the Mars family with the Mars candy business. That hasn't been the case with Apple, at least not yet. Any guesses on how long the Board waits until Cook is replaced?

David Lillienfeld writes:

There will always be outliers.

There are also companies at the other tail with managements performing more for "enjoyment" (like me athletically–I suck at racketball but I very much enjoy playing it and when I've had access to a court, done so for 3+ hours a week). Are there stocks in which management is in it for fun rather than shareholder value "enhancement"? Sure. It isn't hard to identify underperforming companies.

As for a predictable turning point, there should to be tells in each industry, but that doesn't address your question about one sentinel stock. I don't think there is a sentinel today the way GM was in the 1950s and 1960s. (Some might argue that Johns-Manville was a better sentinel. Either way, there was a single stock.) You've got a globalized market and no one company occupies a dominant position in a sentinel industry (such as autos in the 1950s and 1960s). Of course, implicit in this uninformed comment is that a connection exists between stock performance and corporate performance.

Or have I misunderstood your question?

Alston Mabry writes:

Just to do a little bit of counting, here are the 48 non-financial US-based cos with cash of $5B or more, with LT investments added in. The amounts are in billions of dollars, and the list is sorted by the Total column.

total cash: 729.4

total LT inv: 337.7

cash + LTinv: 1067.1

Ticker/TotalCash/LTinv/Total

AAPL 39.8 97.3 137.1

MSFT 68.1 9.8 77.9

GOOG 48.1 1.5 49.6

CSCO 45.0 3.7 48.7

CVX 21.6 26.5 48.1

GM 31.9 14.4 46.3

WLP 20.6 22.1 42.7

PFE 23.0 13.4 36.4

ORCL 33.7 0.0 33.7

QCOM 13.3 15.1 28.4

KO 18.1 10.2 28.2

IBM 11.1 15.8 26.9

F 24.1 2.7 26.8

AMGN 24.1 0.0 24.1

MRK 18.1 5.6 23.7

INTC 18.2 4.4 22.6

HPQ 11.3 10.6 21.9

JNJ 19.8 0.0 19.8

BA 13.6 5.2 18.8

CMCSA 10.3 6.0 16.3

DELL 11.3 4.3 15.5

UNH 11.4 2.6 14.1

NWSA 7.8 5.2 13.0

EBAY 9.4 3.0 12.5

LLY 6.9 5.2 12.1

ABT 11.5 0.4 11.9

AMZN 11.4 0.0 11.4

EMC 6.2 5.1 11.3

HUM 9.3 1.0 10.3

FB 9.6 0.0 9.6

UPS 9.0 0.3 9.3

WMT 8.6 0.0 8.6

SLB 6.3 1.7 8.0

DVN 7.5 0.0 7.5

S 6.3 1.1 7.5

PEP 5.7 1.6 7.3

UAL 6.7 0.0 6.7

HON 5.3 1.3 6.5

DISH 6.4 0.1 6.5

RIG 6.0 0.0 6.0

ACN 5.7 0.0 5.7

NTAP 5.6 0.0 5.6

DE 5.0 0.2 5.2

Richard Owen adds:

This is a brilliant list with many lessons.

- 80/20 rule: $2tr of surplus cash is bandied about as the figure for US corporations. Here are 50 covering over half of that sum.

- The 1% have an internal dissonance. Here is their accumulated share of National Product, all stored up and failed to be reinvested. The 1% neither wish to reinvest their cash, to reduce their share of Product, nor to have GDP decline, nor to run deficits. This is in aggregate impossible.