Dec

30

Russian Voting Statistical Anomalies, from Kim Zussman

December 30, 2011 | 1 Comment

There's an interesting WSJ article on recent Russian parliamentary election (subscription required for now though):

Data analysis shows higher % voting for the "United Russia" party in districts with round numbers of voter turnout (ie, 70%, 75%, 80%, etc) as well as for districts with unusually high turnout (>=98%). Strongly suggests ballot stuffing, manufactured counts, etc.

Evidently vaunted Russian mathematicians are not part of the current apparatchik.

Dec

30

Street Level Economic Indicators, from Alan Millhone

December 30, 2011 | Leave a Comment

In my area in the past year I have seen an increase of people holding signs that they are homeless and begging for money. I note more couples doing the same and note more women begging at intersections etc. Also note more men on foot with back packs that look "bummy" traveling through town. Most without gloves. I have given out several pairs now that it is colder in Southern Ohio.

Regards,

Alan

Phil McDonnell writes:

Every four years the number of highly visible 'homeless' people rises significantly in sync with the presidential election year. The number of real homeless people or residents of drug houses does not really change much but at this time certain unions and re-election committees hire low cost people to man the highly visible street intersections. In my area I have seen them change shifts at even hour intervals. When the replacement approaches about a half block away the one on the corner sees them and puts his or her sign down and casually walks in their direction and does not acknowledge the replacement in any way–as they pass–on the sidewalk. The replacement then picks up the hard luck sign and begins their shift.

Dec

26

Land Rushes, from Stefan Jovanovich

December 26, 2011 | Leave a Comment

Walter P. Fuller bought 40 acres in what is now Pinellas Park, Florida for $45.27 in 1920; less than four years later, he resold it for $40,000. Nine months later, in 1924, the land was resold again for $60,000. The next change of title was in 1933 when the property was sold at auction for $450 - to discharge the county's tax lien. Like Bernard Baruch, Fuller became a millionaire by selling too soon.

Dec

26

The Index Man Lashes Out, from Anton Johnson

December 26, 2011 | Leave a Comment

It is amazing that this divisive "fair share" and "honesty" drivel emanates from someone who extracted the majority of his fortune from the financial markets. Reeling from the lost decade, his motive is to affect a future where after-tax comparisons will be more favorable to his passive brethren. From the John Bogle interview:

It is amazing that this divisive "fair share" and "honesty" drivel emanates from someone who extracted the majority of his fortune from the financial markets. Reeling from the lost decade, his motive is to affect a future where after-tax comparisons will be more favorable to his passive brethren. From the John Bogle interview:

Q: What do you think about the ongoing discussion over tax fairness?

A: I believe the rich should pay more, but that's not a good platform for tax policy. What has gone wrong is that we've failed to recognize the difference between earned income and unearned income. Is it really fair for gamblers on Wall Street to pay a 15 percent rate when they make a winning investment, and an honest working person - a bricklayer for example - may pay an equal or higher tax on their wages than a gambler? That's absolute absurdity.

Dec

26

Review of Shame, from Marion Dreyfus

December 26, 2011 | 2 Comments

At the first, long take of the film, as it opens, we stare at the naked chest of Michael Fassbender, the person whose grim life of privilege and addiction we are forced to endure for several hours. The unsmiling protagonist stays so still, for so long, that we begin to look for signs that he is still in life. Is he breathing? Will he eventually blink?

At the first, long take of the film, as it opens, we stare at the naked chest of Michael Fassbender, the person whose grim life of privilege and addiction we are forced to endure for several hours. The unsmiling protagonist stays so still, for so long, that we begin to look for signs that he is still in life. Is he breathing? Will he eventually blink?

The too-long take is repeated in scenes that are of his sister, played by a gamey Carey Mulligan—a part that decisively removes her from the ingénue of "An Education" (2009)—and scenes that involve a mulligatawny of sexual couplings of protagonist with the paid and unpaid; with duos; alone; in stalls, at home, in public/private spaces, even at work. The overlong takes do not serve for much other than to remind us of what Peggy Noonan inveighs against in the Wall Street Journal in mid-December about the pervasive "flatness" of "movie depictions of our sexuality." My escort joked that men seemed to be leaving to go to the restroom far more often than for other films; but the sex was squalid, painful, not in the least joyous. Unsexy, in the end. Death is not defied by these matings, but somehow beckoned by their dullness and decayed solipsism. Embarrassing, for the most part. (It was probably prostate, not projection, that shook these men from their seats.)

In a current, curiously shadowy NYC, Brandon's carefully compartmentalized private life, which gives him unfettered indulgence for his addiction, is suddenly invaded and compromised when his sad, ungovernable sibling, Cissy, arrives for an unannounced drop-in and stay-over. Their odd familial interaction raises a few eyebrows.

Not one line of humor in the film. Not a minute of erotic enjoyment, for all the naked real estate and fleshly writhing. It reminds one of the Dustin Hoffman/Jon Voight dark-street, bankrupt-old New York icky icon, "Midnight Cowboy" (1969) for pre-Giuliani no-tourist Manhattan griminess. Or of the bleak ice-cold vision of Christian Bale's gloved metrosexual automaton, mid-Gordon Gekko financial scrimshaw, a feral murderer in the unwholesome, relentless "American Psycho" (2000).

In the linear and episodic unspooling of the obsessive captive of sexual encounters, SHAME does not feature much dialogue. Under the entire film is a dirge-like melancholic musical frieze that serves instead of missing dialogue. As much as there is a dearth of talk for the most part, save for bursts of unconnected fits and sibling spats, the scenes are cool, blue, icy surfaces: unfaceted silhouettes and vistas of Manhattan from different vantage-points than those Woody Allen devotees are accustomed to, the glistening City postcards of cinematographer Gordon Willis. Not here.

Brandon's apartment, in the low 30s, Midtown West, is scrupulously neat and featureless, as opposed to his squint-eyed undiscriminating prowl for new sexual partners for do 'em/forget 'em pairings. His wordless exchanges leave no aftertaste, like cheap wine, gasps and gulps that get no revisiting by the affectless addict. His life is clean to the outward glance. He appears to be a decent man, not skeevy as our mind's eye would predict, despite his panther-like visits to late-night dungeons, lonely subways and clubby brothels. His workmates have no idea what he does, where he goes, or with whom, when away from his desk. Events and world news have no purchase here. He is absorbed in his next barren assignation or, more likely, non-nutritive rut.

Brandon's compulsiveness is so blatant for anyone with half an eye that it is only his male comradeship at some unnamed but upper-middle job that convince us that men are not looking to ID each other's foibles. They don't wonder about his liaisons or solitary entertainments. But women are drawn. He flirts with the faintest flicker of a come-hither intensity. Moments later, they are silently heaving—again, for scenes with too much unclothed flesh, too much writhing.

The extended graphic orchestration of grimaces and groaning proves nothing, teaches us nothing more than we already know. McQueen could easily have chopped half an hour sure to have its NC-17 (was X) rating plastered on its official public window, the way restaurants proudly post their A ratings. Scenes without dialog run too long, making sure we get the poke-poke of this emotional battle. But the resonance is not epic. We all battle some sort of addiction, perhaps, though ours are probably less dangerous and time-consuming. And probably less lifeless. The film seems an orphanage for our lust.

Fassbender is a lock for an Oscar nom, and his face and body, while not memorable for the most part, are handsome and indeed attractive. Especially nude. A woman being pushed out of the theatre by her granddaughter, a wheelchair commuter looking to be in her 90s, was delighted to be asked her opinion of the film. Her 30-something granddaughter quickly interpolated she had been "bored" by it. (Yes. It is no Brad Bird "Impossible" action adventure.) Grandma, grinning broadly, slyly exulted, "He was gorgeous! I'm going to see this in 3D!"

Whatever would make a woman of 30 take her swee'pea elder to such a deeply unhumorous, profoundly graphic film with such a title, even were she unacquainted with the unrelieved, tawdry subject matter?

And in the end, the director plays games with the viewer, which may or may not make you even more antsy and uncomfortable than you've been throughout. Not quite a holiday movie. What is saddest is that this is the film everyone will continue to talk up, a daring Euro-approx that is pretending to a soul it does not evince. A 12-stepper would take the heart out of the thing. But then the film would have no excuse for making us squirm with discomfort.

Not a date movie. Even with Grandma's excited post-mount-'em.

Dec

22

Stubby Pringle’s Christmas, from Victor Niederhoffer and the Dailyspec

December 22, 2011 | 7 Comments

[Editor’s Note: Every year at Dailyspec we post the story of "Stubby Pringle's Christmas" by Jack Schaefer. It is a wonderful, heartwarming story. Hope you enjoy it and Happy Holidays.]

[Editor’s Note: Every year at Dailyspec we post the story of "Stubby Pringle's Christmas" by Jack Schaefer. It is a wonderful, heartwarming story. Hope you enjoy it and Happy Holidays.]

High on the mountainside by the little line cabin in the crisp clean dusk of evening Stubby Pringle swings into saddle. He has shape of bear in the dimness, bundled thick against cold. Double stocks crowd scarred boots. Leather chaps with hair out cover patched corduroy pants. Fleece-lined jacket with wear of winters on it bulges body and heavy gloves blunt fingers. Two gay red bandannas folded together fatten throat under chin. Battered hat is pulled down to sit on ears and in side pocket of jacket are rabbit-skin earmuffs he can put to use if he needs them.

Stubby Pringle swings up into saddle. He looks out and down over worlds of snow and ice and tree and rock. He spreads arms wide and they embrace whole ranges of hills. He stretches tall and hat brushes stars in sky. He is Stubby Pringle, cowhand of the Triple X, and this is his night to howl. He is Stubby Pringle, son of the wild jackass, and he is heading for the Christmas dance at the schoolhouse in the valley.

[For the entire text of the story, please follow this link or this link].

Dec

22

10 Things You Can Learn About the Market from Greek and Roman Times and Myths, from Victor Niederhoffer

December 22, 2011 | 2 Comments

1. There is a critical point in the market, a critical decision that the market gods weigh on a scale like Zeus with his balance scale deciding whether Achilles or Hector will win, that determines the market fate, and it is key and should be the focus of all news stories and market considerations but never is.

1. There is a critical point in the market, a critical decision that the market gods weigh on a scale like Zeus with his balance scale deciding whether Achilles or Hector will win, that determines the market fate, and it is key and should be the focus of all news stories and market considerations but never is.

2. Never trust anyone but your family and best friend because everyone is disloyal in a pinch. Peleus was left for dead by his father in law after killing his brother in law to become ruler and this led to the Trojan war. Caesar trusted his best friends but they turned on him when an opportunity for power, money, and romance reared its ugly head.

3. Deception is key. The most successful Greek was the Deceiver Odysseus, and he tricked everyone he dealt with as the market tries to trick you with Odyssean power.

4. The goal is always to come home. Odysseus went home, as does the market. The only loyal ones were the wife and son and the best servant. The market retraces and comes home to break even an inordinate number of times.

5. Never mix romance with business or the market. The Trojan was was started by Paris intervening in romance and being swept off his feet by Aphrodite, and Achilles killed tens of thousands and prolonged the war by 10 years when Menelaus stole his mistress.

6. Don't try to walk with the Gods. Peleus married a half God and married her the last time the Gods and mortals mingled at a celebration and it caused him to be the most distressful of men. Trying to emulate Soros or the other greats is the seed of destruction.

7. Okay, give me the rest. And correct and tighten the above. I'm out of my depth but wanted to get the gist across.

Ken Drees comments:

Like using a mirror against Medusa, one must plan against the adversary and sometimes use their expected attacks to beat them. Like shielding oneself from the siren song, one must be totally prepared, seek council before the journey (the trade) about what dangers are expected.

Like using a mirror against Medusa, one must plan against the adversary and sometimes use their expected attacks to beat them. Like shielding oneself from the siren song, one must be totally prepared, seek council before the journey (the trade) about what dangers are expected.

Also, it seems every entity in mythology had a weak spot. It's probably best to note these weaknesses in your thinking and in your emotions, not how can I beat the market, but how can the market beat me today?

Bill Rafter writes:

The greatest two rules:

(1) nothing to excess and (2) know yourself.

Pete Earle writes:

One lesson from mythology which resonates with me is the oracles/prophets/predictors almost always forecast correctly, but rarely in an obvious or immediately relevant way. The predictions made are usually realized, but not before taking extremely circuitous, and usually counterintuitive ways to reach fulfillment.

In my experience, predictions regarding the direction of equities or commodities inferred from option markets so often prove accurate…but only after traveling in the most wrong, most unanticipated ways.

Alston Mabry responds:

Pete, I think of that as "shaking the tree", i.e., we're gonna get there, but we're gonna shake out as many weak hands as we can along the way.

Pete, I think of that as "shaking the tree", i.e., we're gonna get there, but we're gonna shake out as many weak hands as we can along the way.

Peter Earle replies:

Absolutely. Stop-running and the like as the "gods" way of seeing who's "worthy"; who can withstand the flood, the fire, the sturm und drang.

Jim Lackey writes:

In 2008 I learned from Ryan Carlson– Sisyphus. There is a little useless book Wit and Wisdom from Wallstreet. So many of the quotes are the exact opposite from 3 pages ago… yet for a day they are seemingly sage advice. Worse for the long term. It's all good advice, yet in the mean time we must eat, and in the long term we all end up dust in the wind.

Traders lament when we miss profits. We are miserable when we lose. If we are not careful we are never happy. I have the habit of having to work myself up into a fury to win a race, pass a test or trade. My wife calls it "business mode" everyone else calls it being a jerk. Finally this year I have the ability to take a loss and this week miss a glorious rally and profit… yet at 4:20 PM its over. I am done pushing the boulder back up the hill for the day. I will return at 1:30am or by 7am, all but two business days a year. It can be torture if you do not like to trade, but if you love it…

Here is a quote from my kids music, "This is Our Science" by Astronautalis: "Our work is never done/ We are Sisyphus".

p.s I notice that if I don't like the rap beats I miss quite a bit of new poetry. I hear my teenagers say random lines and say what! That is amazing. Then I hear the song and say no wonder I never heard that line before. Damn drum machines.

Jack Tierney adds:

Recently I've been reading up on complexity, system dynamics, and the unpredictable consequences that occur when tinkering with non-linear systems. The markets seems subject to all and, if I'm even remotely correct in interpreting the literature, there's only one certainty: expecting linear consequences (e.g, provide banks with more liquidity, bringing about an increase in business borrowing, resulting in a resurgent economy) is rarely, if ever, realized.

Instead, the unseen effects on unimagined factors, almost always derails the logic train. A source I've referred to on occasion is "Cassandra's legacy." Appropriately enough, the custodian of that site provides an interesting historical allegory, in the form of Goth Princess/Roman Empress, Galla Placidia, and her part in the demise of the Roman Empire. It's a very lengthy read and, unless history like this interests you, tough going. So, a few highlights:

"Managing any large structure is difficult and we tend to do it badly; a whole empire may be an especially difficult case. To do it well, we would need to use a method what I mentioned before: system dynamics; which is a way to describe systems and the relation of the various elements that compose them.

"…every time that the Romans fought the Barbarians, they could win or lose, but each battle made the Empire a little poorer and a little weaker. The empire was using resources that could not be replaced; non-renewable resources, as we would say today….the solution was not more troops but less troops. It was not more imperial bureaucracy but less imperial bureaucracy, not more taxes but less taxes.

"In the end, the solution was right there and it was simple: it was Middle Ages. Middle ages meant getting rid of the suffocating imperial bureaucracy; it meant transforming the expensive legions into local militias; have people paying taxes locally, in short transforming the centralized empire into a decentralized constellation of small states. Without the terrible expenses of the Imperial court and of the Imperial bureaucracy, these small states had a chance to rebuild their economy and start a new phase of prosperity, as indeed it happened during the Middle Ages.

"What Placidia could do as an Empress was, mainly, to enact laws….It seems that Placidia was acting according to her style; ease the unavoidable, don't fight it….Placidia forbade the coloni, the peasants bound to the land, to enlist in the army. That deprived the army of one of its sources of manpower and we may imagine that it greatly weakened it. Another law enacted by Placidia, allowed the great landowners to tax their subjects themselves. This deprived the Imperial Court of its main source of revenues."

Stefan Jovanovich comments:

As much as King George's scribbler Edmund Gibbon despised Christianity, he had the Middle Ages even more because its bureaucracies were the worst of all — local and mean and stupid.

Professor Bard should revise his history. What he wrote here — "Middle ages meant getting rid of the suffocating imperial bureaucracy; it meant transforming the expensive legions into local militias; have people paying taxes locally, in short transforming the centralized empire into a decentralized constellation of small states. Without the terrible expenses of the Imperial court and of the Imperial bureaucracy, these small states had a chance to rebuild their economy and start a new phase of prosperity, as indeed it happened during the Middle Ages." - is nonsense.

The Roman Empire's tax collections were always "local"; that is why Roman politicians were willing to pay such enormous bribes to be appointed provincial governors. The legions were also "local"; the Empire's expansion came from granting "foreigners" - i.e. the people we would today call Spaniards, French and Syrians - the privileges of citizenship, which meant they were also qualified to serve in the local legions. This was equally true under the Republic; "crossing the Rubicon" would not persist as a bad metaphor if Rome's soldiery had been centralized.

As for economics, whatever the "terrible expenses of the imperial court", they were nothing compared to the ravages of coin clipping. The solidus of the Eastern Empire maintained an unchanged weight and measure for 4+ centuries - a record that is likely never to be broken. (It exceeds the span of sound money for the British Empire and the United States of America put together.) After Princess Placida's day coinage, under the wonderful decentralization of the Middle Ages, effectively disappeared.

"Dearth of provisions, too, increased by degrees, and the scarcity of good money was so great, from its being counterfeited, that, sometimes out of ten or more shillings, hardly a dozen pence would be received. The king himself was reported to have ordered the weight of the penny, as established in King Henry's time, to be reduced, because, having exhausted the vast treasures of his predecessor, he was unable to provide for the expense of so many soldiers. All things, then, became venal in England; and churches and abbeys were no longer secretly, but even publicly exposed to sale." - William of Malmsbury wrote this in 1140 AD - the period that Professor Bard praises so highly for its progress over the degeneracies of the Empire.

Hume deserves the last word on this and most other subjects that interested him.

"Mankind are so much the same, in all times and places, that history informs us of nothing new or strange in this particular. Its chief use is only to discover the constant and universal principles of human nature."

Easan Katir adds:

The Greeks have fooled people since the Bronze Age. Instead of a horse, they now have Trojan bonds.

Steve Ellison comments:

Jack, the Atlantic had an article about why projects that had successful pilots often failed when rolled out to the general population.

Why Pilot Projects Fail– Here are some excerpts:

Promising pilot projects often don't scale … Rolling something out across an existing system is substantially different from even a well run test, and often, it simply doesn't translate.

Sometimes the 'success' of the earlier project was simply a result of random chance …

Sometimes the success was due to what you might call a 'hidden parameter', something that researchers don't realize is affecting their test. Remember the New Coke debacle? …

Sometimes the success was due to the high quality, fully committed staff. …

Sometimes the program becomes unmanageable as it gets larger. You can think about all sorts of technical issues, where architectures that work for a few nodes completely break down when too many connections or users are added. …

Sometimes the results are survivor bias. This is an especially big problem with studying health care, and the poor. Health care, because compliance rates are quite low (by one estimate I heard, something like 3/4 of the blood pressure medication prescribed is not being taken 9 months in) and the poor, because their lives are chaotic and they tend to move around a lot … In the end, you've got a study of unusually compliant and stable people (who may be different in all sorts of ways) and oops! that's not what the general population looks like.

Dec

22

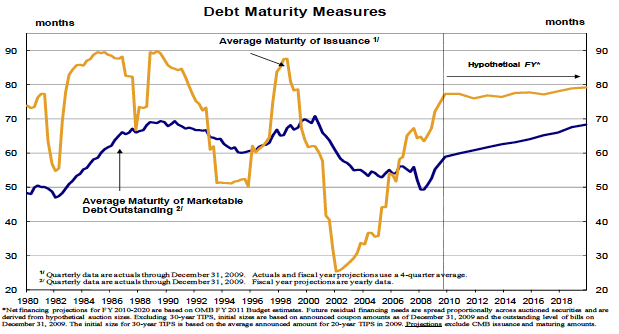

Why the Static US Deficit is Much Better, from Rocky Humbert

December 22, 2011 | Leave a Comment

Bill Gross recently penned an essay in the FT entitled "The Ugly Side of Ultra-Cheap Money". He makes some provocative (and questionable) generalizations regarding the effects of zero interest rates on the real economy, but:

Bill Gross recently penned an essay in the FT entitled "The Ugly Side of Ultra-Cheap Money". He makes some provocative (and questionable) generalizations regarding the effects of zero interest rates on the real economy, but:

1. He importantly ignores the important differences between zero nominal interest rates and zero real interest rates. (Due to deflation, Japan has run a tight monetary policy for years, and the Yen's multi-decade appreciation to 78/$ provides a reasonable proxy of the relative inflation rates between the USA and Japan.)

2. He fails to openly acknowledge that ultra-cheap money is terrible for his business. He laments people keeping dollars under their mattress (because it pays the same as money market funds). Yet, he doesn't mention that the current interest rates out to the 5 year result in his management fees being rather larger than the investor's yield to maturity.

I submit that there IS a pretty side of ultra-cheap money:

Mr. Market (and foreign owners of US debt) are giving a gift to the US Treasury that is truly remarkable. A Bill (the paper, not the Gross) yields 0% (negative ~3% trailing real yield) and the 5-year yields .9% (negative 1% real). Most of the US debt maturities are 5 years and under. And the Fed owns about 10% of the total debt…soaking up the outter maturities. This means, with $15T in debt, the REAL static debt burden is decreasing by about 600+ Billion per year. (Of course, when Mr. Market grows angry with the US Treasury, this pretty picture could viciously swing the other way as various pundits, including Taleb, Grant, Mauldin, etc are warning.)

Here's a chart that shows the US Debt Maturity.

{kind=link}

Yes, Viriginia, there IS a Santa Claus. If you pull off the long white beard, you'll see Santa is actually the people who are buying US Government paper and holding cash. And we should all thank them as they come down the chimney.

Ken Drees writes:

Forget Santa, what about VIXen? He is laid out, 5 months cold. Is it another Christmas in July for the VIX?

Dec

22

18 Charts, from Dan Grossman

December 22, 2011 | Leave a Comment

It's striking to me that not one of the 18 charts covering virtually every significant economic topic refers in the slightest to the massive legal and illegal immigration into the US over the last few decades, and how this could have correlated with chart topics such as working-age male unemployment, amount of toil to rent a house served by average school, medical care spending, etc, etc.

It's striking to me that not one of the 18 charts covering virtually every significant economic topic refers in the slightest to the massive legal and illegal immigration into the US over the last few decades, and how this could have correlated with chart topics such as working-age male unemployment, amount of toil to rent a house served by average school, medical care spending, etc, etc.

Stefan Jovanovich comments:

Thank you, Daniel. he decline in wealth for the "average" American since the collapse of the dot.com boom matches the slow, steady ruin that the 50% of the U.S. population who lived on farms endured after the end of the WW I boom. The migration to the industrial north of the white and black-skinned sharecroppers/small-hold farmers that is now celebrated as the precursor of the civil rights movement was an index of the desperation people felt. If people had really wanted to trade Tennessee for Chicago and Detroit, their children would not be moving back "home" as fast as they have in the past few decades. No one was talking about the depression of the 1920s on the radio any more than they are mentioning it on Twitter now; but it was occurring and continuing to grow in severity.

Dec

22

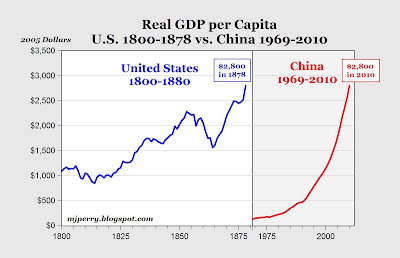

An Interesting Chart, from Leo Systrader

December 22, 2011 | Leave a Comment

I wonder if there is anything economic to be learned from this chart from Mark Perry's blog. The per-capita growth from 1810 to 1850 was more than 120% in 40 years. According to the wiki, by 1860, manufacturing (primarily limited to the Northeast) accounted for 30% of the nation's income, with cotton cloth production the leading industry. This indicates that some strong contrast/conflicts between the industrial northeast and the farming south existed.

I wonder if there is anything economic to be learned from this chart from Mark Perry's blog. The per-capita growth from 1810 to 1850 was more than 120% in 40 years. According to the wiki, by 1860, manufacturing (primarily limited to the Northeast) accounted for 30% of the nation's income, with cotton cloth production the leading industry. This indicates that some strong contrast/conflicts between the industrial northeast and the farming south existed.

Is it reasonable to believe that these economic conflicts were among the underlying causes for the eventual war?

Obviously the economic conflicts were the result of a fast and an uneven development. Perhaps it serves as a very valuable indicator for today.

Dec

22

Thought of the Day, from James Goldcamp

December 22, 2011 | Leave a Comment

The fundamental flaw in systems based on past fundamental data which are published in a book and now used as a stalking horse for investments from outsiders is that each time he comes out with a new book he has found better methods based on a moving window of retrospective data.

I'd also suggest that value-momentum is a widely known and disseminated alleged anomaly, and like many things that worked better before everyone knew about it, I suspect the strategy's prospects are not as good as the back tested history. Moreover, given the rate of compounding, if it works, then the many billions pursuing this already will have grown to a substantial part of (more than?) the total market capitalization of equity markets (to say nothing about any capitalization effect that would be nullified by large amounts of capital pursuing the same strategy in anything but large caps).

Dec

22

More Cheap (Apparently) Stock Tidbits, from Charles Pennington

December 22, 2011 | 1 Comment

The Dec. 12 Barron's, page 32, lists some big cap stocks that have big cash holdings.

I list them in a table below, along with Value Line projections for 2012 earnings, and an "adjusted" P/E–the (price-cash)/earnings, which makes sense if you sort of assume that the cash earned nothing.

column labels:

ticker / cash per share / price / 2012 earnings from ValueLine / (price-cash)/earnings

msft $7 $26 $2.80 7

csco $8 $18 $1.45 7

goog $129 $630 $40 12.5

orcl $6 $29 $2.42 9.5

jnj $11 $64 $5.25 10

pfe $5 $21 $1.60 10

aapl $87 $395 $32.50 9.5

cvx $10 $103 $13.10 7

wlp $53 $65(!) $7.70 1.3

amgn $19 $61 $5.50 7.5

As has been observed here before, stocks are pretty cheap these days.

Kim Zussman adds:

On the subject of AMGN, one of my first posts on spec-list was "Amgen in P/E Stratosphere", ca 2004 or so. Though having no local insights about the stock, the then high P/E ratio was subsequently rectified in the denominator. (and has remained range-bound in Russian fashion since).

Presumably high-flying growth stocks either become value with dividends (also see MSFT) or debubblize (also see HOV, AMD, etc.

Dec

22

Pit Simulation, from Duncan Coker

December 22, 2011 | 1 Comment

Since the pit trading floors have mostly closed I have an excellent simulation for being able to think under pressure and react quickly in difficult conditions. That would be to care for a cranky and hungry two year old at 6 am, while reviewing and placing trades for the day, and subject to high decibel protestations of the aforementioned. By the time the market actually opens one has developed nerves of steal from the ordeal and ready for anything.

Since the pit trading floors have mostly closed I have an excellent simulation for being able to think under pressure and react quickly in difficult conditions. That would be to care for a cranky and hungry two year old at 6 am, while reviewing and placing trades for the day, and subject to high decibel protestations of the aforementioned. By the time the market actually opens one has developed nerves of steal from the ordeal and ready for anything.

Craig Mee writes:

Good call, Duncan.

With the keen eye of the youngster and their intense gazing at the pretty colours of the charts, it may be worth asking the two year olds what their thoughts are.

Dec

22

Existing Home Sales Revised Down by 15%, from Rocky Humbert

December 22, 2011 | 1 Comment

If you use the NAR sales and inventory data in a model, you might want to pay attention to this and this. This downward revision will also feed through to the Commerce Department data series… That is, the GDP component from home sales from 2007 to 2010 will be lowered. And people complain about the "quality" of Chinese data!

Dec

21

3 Tips for Traders from John Wooden

December 21, 2011 | 1 Comment

Here are three good suggestions from The Essential John Wooden that are good for trading.

Here are three good suggestions from The Essential John Wooden that are good for trading.

1. Start and end every practice at exactly the same time.

2. Expect failure. Assume every shot will be missed. Be ready for what comes, be it a tip in, rebound, fast break or something else.

3. Get the fundamentals right. Double tie all shoelaces. Make the uniforms fit perfectly and get in position for every rebound the perfection of little things usually determines if a job is well done.

Anatoly Veltman comments:

This reminds your "Base of Operations" post last year. I commented that I beat out almost a million checker challengers in the old country by merely sitting straight down the precise middle of the checkerboard, which allowed me to quickly count as much as 30 moves ahead on 100-square board.

Dec

21

Thoughts on Value and Growth, from Russ Sears

December 21, 2011 | Leave a Comment

After looking at some Fama French data it would seem to me that Value tends to outperform in periods where the Fed's monetary policy is in disarray. [web site ]

The inflation of 1970-1984 seemed to play into the hands of W. Buffett, whose strategy could perhaps be best defined as buying companies that could raise the cost of goods to the public. Often he was right that there was much less competitive pressure for price than the company leaders had come to believe, perhaps a misperception that evolved through territorial battles that were basically over but still being fought in the minds of these executives.

Now we are in a period of deflation, where feds are trying to prop housing prices up, to save the TBTF banks. It would seem that in such a risk adverse environment, "value" would again out perform growth. But what is the "new value" proposition that will put value companies strategy ahead of their peers?

One thought is that it is high cash with strategy of maximizing high intangible assets (people/ideas).

Dec

21

Value Line Deserves Some Credit, from Samuel Eisenstadt

December 21, 2011 | 3 Comments

"The Momentum Effect in stocks was discovered by Jegadeesh and Titman" - A finance pundit

How about some credit to Value Line which was using price momentum in its Ranking System all the way back in 1965, long before academia provided recognition? See Fischer Black's "Yes, Virginia, There is Hope - Tests of the Value Line Ranking System", which dates back to the early 1970s. I'm proud that I was there in the early days.

Sam Marx replies:

Mr. Eisenstadt,

I'm a Value Line Subscriber to its Stock Service and its Option/Convertible Service. They deserve credit for being early in using momentum and earning changes for stock prediction. Mark Hulbert still rates it highly. I understand W.E. Buffett recommends it for a data source.

However, I feel they have become somewhat stodgy lately and other services/newsletters have become very competitive offering data Value Line doesn't. MorningStar and Zacks for example.

I believe Value Line Stock services should expand its services to include earnings data, earnings surprises and stock's intrinsic value.

Their Option Service is loaded with information that I've found very useful. The man in charge, Dr. Larry Cavanagh, took over a simplistic service and made it truly professional. If you know how to use the data, it is the best buy in an option service. He also has done a fine job with the convertible service. I also commend you on your service and contributions in making the Value Line Stock Service the success it became.

Trivia question for you; Way back before Value Line started their convertible service/newsletter, when we both were young men, there was a trailblazer convertible bond newsletter. It was the only one I knew of or could find back then and I found it useful. Value Line went into competition with it and eventually put them out of business. I believe it was published in Long Island and as a hint the first letter of its name was "R".

Dec

21

Fast Track Salmon Evolution, from Pitt T. Maner III

December 21, 2011 | Leave a Comment

Here is some interesting research that has possible implications for other organisms.

Here is some interesting research that has possible implications for other organisms.

1) The impact of hatcheries on salmon is so profound that in just one generation traits are selected that allow fish to survive and prosper in the hatchery environment, at the cost of their ability to thrive and reproduce in a wild environment.

2)

Captive breeding programs are widely used for the conservation and restoration of threatened and endangered species. Nevertheless, captive-born individuals frequently have reduced fitness when reintroduced into the wild. The mechanism for these fitness declines has remained elusive, but hypotheses include environmental effects of captive rearing, inbreeding among close relatives, relaxed natural selection, and unintentional domestication selection (adaptation to captivity).

We used a multigenerational pedigree analysis to demonstrate that domestication selection can explain the precipitous decline in fitness observed in hatchery steelhead released into the Hood River in Oregon. After returning from the ocean, wild-born and first-generation hatchery fish were used as broodstock in the hatchery, and their offspring were released into the wild as smolts. First-generation hatchery fish had nearly double the lifetime reproductive success (measured as the number of returning adult offspring) when spawned in captivity compared with wild fish spawned under identical conditions, which is a clear demonstration of adaptation to captivity.

We also documented a tradeoff among the wild-born broodstock: Those with the greatest fitness in a captive environment produced offspring that performed the worst in the wild. Specifically, captive-born individuals with five (the median) or more returning siblings (i.e., offspring of successful broodstock) averaged 0.62 returning offspring in the wild, whereas captive-born individuals with less than five siblings averaged 2.05 returning offspring in the wild.

These results demonstrate that a single generation in captivity can result in a substantial response to selection on traits that are beneficial in captivity but severely maladaptive in the wild.

Dec

19

All That Glitters Isn’t Silver, from Kim Zussman

December 19, 2011 | 1 Comment

Here is the ratio of GLD/SLV (gold to silver ETFs), 2006-present.

The mean ratio over the past 5 years is 5.6. From July to October 2008 GLD/SLV spiked — possibly evidencing flight to safety (gold being safer than silver as silver oxidizes and you have to keep polishing it). The ratio gradually declined, then plummeted from August 2010 to April 2011. Over the past 8 months GLD/SLV rose to the current 5.4 - quite near the 5 year mean.

In hindsight, there was some good spread trading in silver and gold [link to music video].

Dec

19

War Premium Over? from Kim Zussman

December 19, 2011 | Leave a Comment

Using Wiki data there does appear to be a reduction in % of world population killed in war over time.

http://en.wikipedia.org/wiki/List_of_wars_and_anthropogenic_disasters_by_death_toll

The high and low death toll estimates were averaged for the dependent variable, and the mid-point year of the war period was used as the independent variable. Regressing mean estimated % of world population killed in war vs year:

The regression equation is

mean est % world pop killed = 9.94 - 0.00466 avg year

Predictor Coef SE Coef T P

Constant 9.938 2.693 3.69 0.001

avg year -0.005 0.0016 -2.97 0.007

S = 3.26307 R-Sq = 29.6% R-Sq(adj) = 26.2%

>>Significant; year explains 26% of the variance. However a plot suggests though war has become less deadly over time, it is more frequent.

Dec

16

The Key to No Regrets, from Tim Melvin

December 16, 2011 | 2 Comments

What do we regret as we lie on the proverbial bed awaiting the last gasp that marks our passing from this realm? It is a great question and one I have spent some time thinking and reading about over the years. How do we live our lives to minimize the regrets as we anticipate the end of our earthly experience? Is there some magic formula we can all use to make sure that we pass this live with as few regrets as possible?

What do we regret as we lie on the proverbial bed awaiting the last gasp that marks our passing from this realm? It is a great question and one I have spent some time thinking and reading about over the years. How do we live our lives to minimize the regrets as we anticipate the end of our earthly experience? Is there some magic formula we can all use to make sure that we pass this live with as few regrets as possible?

A few years back I read an interview with a hospice worker on this very subject. In her many discussions with those about to pass through the door of life she found that most people regret the things they did not do far more than the things they may have done. Regardless of their crimes and misdeeds throughout their life their regrets were about not taking that trip, not kissing the girl, not chasing their dreams and not being who they wanted to be as they took their journey.

It is quite correct to point out that the whole wishing you spent more time with family and friends and other greeting card sentiments is probably a cliché of sorts. While there are not many headstones that say I wish I spent more time at work it is also true that very few of us actually pick our own epitaph. I am quite sure that many do pass those last hours wishing they had been better husbands, wife's and parents. I am also sure many spend their last hours wishing they had done more with their careers, their business and professional life. We are all different and as much as we live different lives we will have different regrets as we approach our individual deaths.

The real regrets come from the fact that far too many of us do indeed live lives of quiet desperation. We are born, go to school, get married, have a family, get divorced, work at jobs we hate, raise kids we don't understand, settle for less than we dreamed and do what we think we are supposed to do along the way. Our lives get shaped by television and pop culture and we drift along on a sea of conformity and apathy. I see it every day and I am sure the rest of you do as well. We all start out with dreams, hopes and desires and somewhere along the way let go of them to get along as best we can. I have yet to talk to a recent college or high school grad who told me they were going to get a job they hated, have a couple of kids who would stop talking to them in twenty years, spend thirty years drinking bud and watching Survivor reruns before dropping dead mowing the lawn in a house they hate while their ex-wife spends their hard earned retirement funds on a cruise to Cancun. I have however talked to a lot of folks my age whose life has played out exactly that way.

How the hell does this happen to us? We start out full of fire and hope. I never met a lawyer who planned to spend his years getting his soul crushed as a mid-level associate or a doctor who planned to spend a few decades doing colonoscopies at the VA clinic. We all want to change the world, to get rich, to create great art and chase big dreams as we start of the path of adulthood. None of us start out to become what so many of us do.

How the hell does this happen to us? We start out full of fire and hope. I never met a lawyer who planned to spend his years getting his soul crushed as a mid-level associate or a doctor who planned to spend a few decades doing colonoscopies at the VA clinic. We all want to change the world, to get rich, to create great art and chase big dreams as we start of the path of adulthood. None of us start out to become what so many of us do.

Little boys dream of being the star center fielder and or the hot gloved third baseman with the big bat not the backup utility infielder. Little girls want to be the prima ballerina or the singing star with the big hair and bigger voice, not the back up chorus singer. We all have the big dreams and hopes as life begins. That of course is much of the problem. We cannot all be the star we hope to be. If that was true I would currently be managing the Orioles after a long career as the much loved replacement for Brooksie on third base. I am not. I love baseball but I am about as athletic as a door stop. Never mind a curve ball I couldn't hit a little league non fastball. Cant sing, cant dance and the only thing I can do with a paint brush is make a mess. I was never going to be a star ballplayer or artist no matter how much I dreamed.

This can be crushing. We get into the world and find out bills need to be paid, food costs money, bosses will work you into a nub of yourself without so much as a thank you or a f you. The world does not care about you or your dreams and no one was sitting around anxiously awaiting your arrival on the scene. You take a job to get by and next thing you know you are sitting in La-z- Boy bud in hand noticing that the only thing more absent than your hairline is your happiness. It is too easy to let live dictate you instead of you dictating life. You have to be vigilant to protect your passion and your dreams.

I can dream with regret of not being the hot handed third baseman and the world's greatest baseball manager or I can love the fact that I can be a fan and sit in the stands on a summer day with a cold beer and a scorecard. I can bitch and moan about not going to college and maybe going to work for Goldman Sachs or even better the New York Times or I can love the fact that I am a pretty good writer and decent manager of investments and have managed to build a life around those two facts. I can spend my days wishing this or that or I can love what my life is and the fact that I have chased my dreams and made pretty good headway towards achieving parts of them.

Often life is just not going to go the way we want and wish. This does not mean that life cannot still be magical and absent of regrets for the most part. Even if life has forced you into circumstances you never wanted and instead of being the accountant that saved the world you are an IRS auditor does not mean that all the things you love and desire about life are gone. IRS auditors can still listen to Beethoven, watch sunsets, fall in love (just not with my daughter please) and appreciate the beauty of life. Just because you are selling Fords instead of driving one to victory at Daytona does not mean that life is not capable of being a beautiful and wonderful experience. There are still books, knowledge, music, art, and other parts of life that can produce great passion and meaning.

Life is precious and as far as we know we can only have one of them. We have to protect our passions and no matter what life deals out stay focused on what we love about living. We will all screw up along the way and it is probably not going to work exactly as hoped as we crossed the stage to pick out diploma. That does not mean we need to just lay down and accept what comes along the way and miss out on the adventure. So having kids kept you from going to Tibet and contemplating the navel of a Yak in search of the world's great answers. You can let that beat you back into the chair and take in Snookies latest adventures or appreciate and love the fact that you have the chance to mold the spirit of adventure, love of beauty and learning in your kids and share the adventures with them as they grow. So you are not Clarence Darrow and the superstar of the legal world but to those you help on a day to day basis you just might be.

Life is precious and as far as we know we can only have one of them. We have to protect our passions and no matter what life deals out stay focused on what we love about living. We will all screw up along the way and it is probably not going to work exactly as hoped as we crossed the stage to pick out diploma. That does not mean we need to just lay down and accept what comes along the way and miss out on the adventure. So having kids kept you from going to Tibet and contemplating the navel of a Yak in search of the world's great answers. You can let that beat you back into the chair and take in Snookies latest adventures or appreciate and love the fact that you have the chance to mold the spirit of adventure, love of beauty and learning in your kids and share the adventures with them as they grow. So you are not Clarence Darrow and the superstar of the legal world but to those you help on a day to day basis you just might be.

The problem with many of us is letting fear dictate our actions, or more accurately our inactions. Just because we got divorced or had a bad relationship does not mean we should harden our hearts against the possibility of love in the future. Just because our Fried Liver Chips franchise idea failed does not mean we should never explore another opportunity. If your first novel is rejected you have joined than ranks of just about every author who ever lived and it's not a reason to set down the pen and turn on the TV. If you are not the star learn to appreciate and live the fact that most people never even make it to the chorus. Chase you dreams, your passion and enjoy where it takes you. Life will give you a lot of choices and paths along the way. I promise you life will give lots of chances to just quit. You will not be able to hit the curve ball. You voice will sound like amplified sandpaper scrubbed on cement. You will not promoted to department head. Someone you love will not love you back. It is not all going to go your way. It will be easy to quit. If you do you will spend those last days and hours thinking of all the things you did not do and struggling to remember who was the last one voted off the island.

I think the key to no regrets is to embrace the romance and beauty of life and to chase your dreams and your passions. You may not get all you want but there is a good chance you will get the life you want. Read the book, turn up the music, kiss the girl, take the chance. You will win some, you will lose some. But the dream come true really is the journey and adventure of it all. Don't, as they say, sweat the small stuff because its all small stuff. If you want to spend more time with your family then do that. If you want to spend more time building your company, then that's how you should spend your time and energy. It is your life. Live it. Then perhaps you can be able to die without regretting the choices you made along the way

I think the key to no regrets is to embrace the romance and beauty of life and to chase your dreams and your passions. You may not get all you want but there is a good chance you will get the life you want. Read the book, turn up the music, kiss the girl, take the chance. You will win some, you will lose some. But the dream come true really is the journey and adventure of it all. Don't, as they say, sweat the small stuff because its all small stuff. If you want to spend more time with your family then do that. If you want to spend more time building your company, then that's how you should spend your time and energy. It is your life. Live it. Then perhaps you can be able to die without regretting the choices you made along the way

Dec

16

The Atlanta Hockey Team Indicator, from Stefan Jovanovich

December 16, 2011 | Leave a Comment

As the serious readers of this site (Blackhawks, Penguins, Flyers– er, even Rangers fans) know, Atlanta had a hockey team named the Thrashers until this May of this year when they became the Winnipeg Jets. This is the second export of Southern ice culture to Canada. In May 1980 the Atlanta Flames became the Calgary Flames.

As the serious readers of this site (Blackhawks, Penguins, Flyers– er, even Rangers fans) know, Atlanta had a hockey team named the Thrashers until this May of this year when they became the Winnipeg Jets. This is the second export of Southern ice culture to Canada. In May 1980 the Atlanta Flames became the Calgary Flames.

Admittedly, it is not certain that 2011 will equal 1980 as an opportune time to being accumulating U.S. equities; but the indicator has been flawless in calling tops. The Thrashers were given their franchise rights in 1997 and played their first game on October 2, 1999. The Flames received their franchise in November 1971 and began play in October 1972. What else does one need to know?

Dec

16

Are Introverts More Gifted? from Leo Systrader

December 16, 2011 | Leave a Comment

I have heard that about 25 percent of the population are introverts, but as many as 60 percent of gifted children are introverts.

I have heard that about 25 percent of the population are introverts, but as many as 60 percent of gifted children are introverts.

I don't find this strange. But our understanding about the brain is too minimal to explain for instance the intrinsic links between being an introvert and being gifted. In addition, the concept of being gifted is very vague– it perhaps simply means that he/she can perform something somewhat better than an ordinary human.

With all these unknowns, many wonders often appear to us.

Dec

16

Knock and Run, from Craig Mee

December 16, 2011 | Leave a Comment

In my younger years, a popular game by the local crew in the neighborhood was knock and run, where you would knock on the front door of a neighbor, and then go hide in the bushes, while they searched around trying to find the culprit. Watching the AUS USD last night attack some "key" upside levels, reminded me of this pursuit.

In my younger years, a popular game by the local crew in the neighborhood was knock and run, where you would knock on the front door of a neighbor, and then go hide in the bushes, while they searched around trying to find the culprit. Watching the AUS USD last night attack some "key" upside levels, reminded me of this pursuit.

Time and again the aussie rushed into knock on the door, only to get scared off by some lights, or wind rustling the branches and retreat back until finally it got close enough to make contact with the wooden door, knock, and run for the hills.

Makes me consider if a market's velocity into and then out of range highs gives a heads up as to whether a retracement will hold. No doubt you have to time it well, as you cant stay in the bushes all night awaiting the optimum "conditions".

Dec

16

The Tyranny of Round Numbers, from Peter Saint-Andre

December 16, 2011 | 1 Comment

Lots of chatter yesterday about gold breaking through its 200-day moving average. Ron Griess says to consider the 300-day moving average instead. Has anyone done research on the benefits of using non-round-number moving averages, such as numbers slightly lower than 200 or 300?

Lots of chatter yesterday about gold breaking through its 200-day moving average. Ron Griess says to consider the 300-day moving average instead. Has anyone done research on the benefits of using non-round-number moving averages, such as numbers slightly lower than 200 or 300?

Phil McDonnell writes:

I have tested them all from about 2 days to maybe 1000 days. Generally speaking there is little difference between two 'nearby' moving averages. If you think about it the 200 day has 190 terms in common with the 190 day average. Generally speaking they almost all work as long as the average is longer than about 100 days or so.

All such methods are weak at best. For example the 200 day yields about .04% per day if above the average. But adding a 50 day/200 day crossover reduces the yield to only .03%. In other words the so called golden cross does not really work.

Dec

16

Housing, from Duncan Coker

December 16, 2011 | 1 Comment

One particularly nasty feature regarding the housing market which I am surprised to have seen no writing on is the treatment of capital loss. Losses on primary residences can not be deducted from other capital gains. What you eat, so to speak, you must pay tax again on making that capital back. Using a 20% tax rate of say 6 trillion in lost housing capital, that is roughly $1.2 trillion that the public will have to pay in incremental tax. (true if housing rebounds the loss may not be realized or incurred. Also true that some of the capital loss may be transferred to the banks if owner walk on the loan) But thinking like a politician and using government finance should they not include this potential for windfall tax receipts over the next decade or so as new "revenue". And why not just bring it all forward to 2012 and solve the whole budget gap for next year.

One particularly nasty feature regarding the housing market which I am surprised to have seen no writing on is the treatment of capital loss. Losses on primary residences can not be deducted from other capital gains. What you eat, so to speak, you must pay tax again on making that capital back. Using a 20% tax rate of say 6 trillion in lost housing capital, that is roughly $1.2 trillion that the public will have to pay in incremental tax. (true if housing rebounds the loss may not be realized or incurred. Also true that some of the capital loss may be transferred to the banks if owner walk on the loan) But thinking like a politician and using government finance should they not include this potential for windfall tax receipts over the next decade or so as new "revenue". And why not just bring it all forward to 2012 and solve the whole budget gap for next year.

Dec

16

Password Cracking, from Vince Fulco

December 16, 2011 | Leave a Comment

This may be elementary for some but I happened to watch a video from October's Defcon conference last night and a presenter made an extremely persuasive argument for two factor password authentication. Gmail gives it away for free and I have been using for 6 months without a hitch. Something for list members to seriously consider in their business practices. While its a little irreverent, as defcon folks can be, the security pro reminded listeners multiple times that the Chinese are developing some of the most powerful systems in the world and even 6-8 digit passwords are not safe.

This may be elementary for some but I happened to watch a video from October's Defcon conference last night and a presenter made an extremely persuasive argument for two factor password authentication. Gmail gives it away for free and I have been using for 6 months without a hitch. Something for list members to seriously consider in their business practices. While its a little irreverent, as defcon folks can be, the security pro reminded listeners multiple times that the Chinese are developing some of the most powerful systems in the world and even 6-8 digit passwords are not safe.

Dec

16

The Long Term Outlook, from Laurel Kenner

December 16, 2011 | 1 Comment

The best returns on investment will be in the U.S. over the next decade. That’s the word from Louis Gave of Gavekal Research, a research firm that provides consistently smart, independent macroeconomic analysis to Wall Street.

The best returns on investment will be in the U.S. over the next decade. That’s the word from Louis Gave of Gavekal Research, a research firm that provides consistently smart, independent macroeconomic analysis to Wall Street.

The three defining trends of the past decade – skyrocketing U.S. spending on guns and butter, the economic rise of China, and the single European currency – are all coming to a screeching halt. That’s why, says Hong Kong-based Gave, “all of the clients we’ve seen on this trip have been exhausted and grumpy.”

Looking forward, according to presentations by Gave and his colleagues at the University Club in New York City on Dec. 15, the picture brightens in the United States. Government spending, for the first time in decades, has slowed to zero growth. Private job creation has resumed growing. Increasing automation in manufacturing will encourage factories to be located once more in the United States, to minimize transport costs. To get dollars in the future, countries will need to sell not manufactured goods, but assets, and the dollar will strengthen accordingly.

In the self-admittedly Panglossian Gavekal analysis, fears of a 2008-style disaster emanating from a freeze in European banking or a bursting bubble in China are overblown.

Despite all the noisy headlines about European foot-dragging, the European Central Bank has in fact been much more active than the U.S. Federal Reserve in assuring that no Lehman-like event occurs in Europe. The ECB’s decision to provide unlimited liquidity to the banking system for the next three years is the key, rather than any announced deals between Sarkozy and Merkel. The world is already moving ahead. Central banks are preparing for an orderly breakup of the euro. The downside risks have largely been discounted (and no surprises on the upside are possible, given Northern Europe’s unwillingness to assume the collective liabilities that would necessarily accompany a US.-style fiscal union.) The bad news is that European consumer and government spending will decline massively, according to Charles Gave, the senior member of the father-son Gavekal team. The good news for the U.S. is that Europe’s decline will bring about lower commodities prices, a change as significant as resulted from the fall of the Berlin Wall.

As for China, Louis Gave predicts that China will be able to keep its economy growing strongly by moving beyond fixed lending rates and credit quotas to develop a true capital market. The first step was the establishment of the renminbi-denominated “Dim Sum” bond market in Hong Kong at the beginning of this year. The government’s goal was to establish the Chinese currency in Asia as the medium for trade, displacing the dollar – a step as significant as the rise of the Deutsche Mark in postwar Europe. (The French idea of curbing German power by creating the euro has turned out to be less than happy.) The Dim Sum market had a shaky start, as China’s trading partners had a limited appetite for Chinese government bonds and Chinese corporate bonds to hold in reserves. Lately, a parade of U.S. multinationals has been doing $500 million bond issues in Hong Kong with, one assumes, gracious notice taken by the Chinese government.

The bottom line, from the senior Gave: “Buy Schumpeter.”

Dec

16

Blame the Speculators, from Rocky Humbert

December 16, 2011 | Leave a Comment

This paper from the New York Fed blaming the real estate crisis partially on the flippers (speculators) is actually a rather sensible paper that makes some obvious and more subtle points. Most interesting is they quantify the extent of speculative purchase activity during the bubble years in some creative ways.

This paper from the New York Fed blaming the real estate crisis partially on the flippers (speculators) is actually a rather sensible paper that makes some obvious and more subtle points. Most interesting is they quantify the extent of speculative purchase activity during the bubble years in some creative ways.

They note:

1. Housing is both a consumption good and an investment/store-of-wealth. During the bubble years, the latter trumped the former and attracted speculative/investment interest. i.e. irrational exuberance.

2. Investment/Speculative buyer motivation can be based on (1) rental income; (2) buy and hold for long periods; (3) buy & flip. #3 grew to be a major factor near the zenith.

3. They demonstrate that 1/3 of ALL home purchases were 2nd buyers during the bubble years, AND, in the worst states (NV, AZ, FL etc), more than half of the purchasers were second home buyers and/or flippers and/or multiple lien holders.

They are quantifying what we already knew — that the seemingly endless demand for homes was coming from investment/speculative buyers. However, unlike during the internet bubble, these speculators walked away (as many had no-money-down) and they handed the keys to the banks…

It would be analagous to having a leveraged trading account with no initial margin….!

Stefan Jovanovich comments:

And, no recourse. If the speculators were clever/dishonest enough to state on the disclosure forms that they were buying the properties as principal residences, here in California and Arizona and the other non-recourse states, their liability was limited to their option payment - er, their down payment (which could be as little as 3%). Here is the list of the non-recourse states:

Alaska (AK)

Arizona (AZ)

California (CA)

Connecticut (CT)

Idaho (ID)

Minnesota (MN)

North Carolina (NC)

North Dakota (ND)

Oregon (OR)

Texas (TX)

Utah (UT)

Washington State (WA)

The rumor is that the AGs have reached a settlement.

The settlement of $25B is not going to make much of a dent in the outstanding mortgage deficiencies that are recourse. Core Logic says that 10.7 million houses (22.1% of all residential properties with a mortgage) were in negative equity at the end of the third quarter of 2011 and an additional 2.4 million properties (5% of all mortgaged residences) had less than 5 percent equity. The negative-equity and near-negative equity mortgages accounted for 27.1 percent of all residential properties with a mortgage nationwide. But there is good news - Core Logic says the 27.1% is down .4% from the total in the 2nd quarter.

Also, the Federal Reserve's calculation of "owner equity as percentage of household real estate" was 38.6% as of Q3 this year; in 2005 it peaked at 60%. Approximately 1 out of 3 homes in the U.S. has no mortgage. I may need Big Al's help (as I did when calculating the current market price of the U.S. Treasury's gold reserve) but my handy calculator suggests that this leaves 40% of homes that are "conventional" - i.e. neither free and clear nor so leveraged that they have negative and near-negative equity. The bad news is that, after you subtract 33% from 38.6%, that means the average cushion for the conventionally-mortgaged homes is 5.6%/40% - 14%. Didn't someone say something about this being a solvency problem and not a liquidity problem?

Final random thinking:

According to the folks at Calculated Risk, there are now 4.1 million seriously delinquent loans (90 day and in-foreclosure). In a "normal" market there a 1 million seriously delinquent home loans. Recently, there was "good news" (sic) about the decline in the numbers of REO properties held by Fannie (in Q3 their REO inventory fell to 122,616 houses, a decline of 10% from the number at the end of Q2). That made it the 4th straight quarter in which Fannie's REO inventory declined. One small problem: this is the same period during which foreclosures ground to a halt because of the litigation over mortgage servicing (robosigning, etc.). While it is likely that some of the seriously delinquent loans will cure as part of the settlement (see below), many more will go into foreclosure; and Fannie's inventories will rise.

Alston Mabry writes:

In Phoenix the RE bubble started in the valley and then moved up into the mountain towns 2-3 hours away, where people have summer homes to escape the heat. It was like a tide of money that rose up the mountainside. In August/September 2006, I was driving around and listening to NPR, when a report came on about the local RE market.

A woman who was a broker in the mountain towns said that business was absolutely booming…oh, except that last week there was nothing…strangest thing…but we're sure it will pick up again next week, after the kids are settled in school, etc etc.

An image popped into my mind: A flipper had an open house, but the only people who showed up were other flippers, and by that time they all knew each other. They looked at each other and said, "Holy sh*t…", and got in their cars and left, wondering how quickly they could unload their properties. It was over. And the tide rolled back down the mountain.

Dec

15

The Legend of Bo Keeley Grows, from Art Shay

December 15, 2011 | 1 Comment

Here's a link to my article about Bo Keeley "The Legend of Bo Keeley grows". They or I got the photo credits goofed up. Sorry. Story comes out in NYC, SF, LA, Seattle, Austin, TX, DC, Chicago, Shanghai, London. Welcome home.

Here's a link to my article about Bo Keeley "The Legend of Bo Keeley grows". They or I got the photo credits goofed up. Sorry. Story comes out in NYC, SF, LA, Seattle, Austin, TX, DC, Chicago, Shanghai, London. Welcome home.

Ken Drees sends us a poem to honor Bo's welfare:

.

.

.

Bo Left Us Dead

(Written after reflection on good news of Bo Keely's safety)

Finished Bo's book, just put it down,

Next thing I hear

Sad tragic news,

Keely's not to be found.

No, not in anytown,

Got himself killed this time 'roun.

Them Mex think he's undercover narc,

Down there, too tall and off white

He sticks out,

One too many rides in the dark.

DocBo, The speculator surmises,

Has run plum out of lucky devices.

No facebook, email or phone, G*d please help Bo,

Sadly, its over for him;

No more of his stories, and that grin.

Please bring him back whole.

But if he's truly dead Lord,

Least his soul's in your yard.

Praying is over, Bo left us dead,

No more tales, rails or boxes

To inspire, tranfix,

To dazzle our heads.

Keely has jumped one reefer too far,

Somber, even the bulls at roundhouse bar.

And then like rain that drought licks for,

Bo's Alive for sure. For sure!

Been in the desert, all this time,

Playing with spiders, rocks, and slime.

Those mental puts on Bo expired,

Luckily not the man, that a freight train sired.

So comes the end of this tiny tale

Let the celebration begin,

Dead, now alive, its all win-win.

February's, cruel winter's gale,

Will no doubt herald,

A cupid hearted Hobo, quite undead sans peril.

Dec

15

Top 5 Regrets in Life, from Jeff Watson

December 15, 2011 | 2 Comments

Have you seen this article about the top 5 regrets of the dying? It is a must read.

Have you seen this article about the top 5 regrets of the dying? It is a must read.

Gary Rogan writes:

I really liked all of them, except based on everything that I know I disagree with the statement that "happiness is a choice". Irrational fears are not a choice, depression is not a choice, and neither is happiness.

Gibbons Burke writes:

Well, happiness is dependent on one's attitude, and in many cases, you can choose, control or direct your attitude.

My theory is unhappiness and depression happen when reality does not live up to one's expectations of what life is "supposed" to be like. I think the key to happiness is letting go of those expectations. That action at least is within an individuals purview and control. There is an old Zen maxim: If you are not happy in the here and now, you never will be.

Russ Sears adds:

I think most irrational fears and depression stem from the unintended consequences of one's choices or often, the lack of decisions, such as little or no exercise. However, I believe many of these choices are made when we are children, and we do not fully understand the consequences. Many of these bad choices may be taught often though example by adults or sometimes it is just one's unproductive coping methods that are simply not countered with productive coping methods by the adults in their lives. I think some people are more prone to fall into these ruts, but most of these ruts are dug none the less.

Jim Sogi writes:

The regrets are perhaps easily said on the deathbed but implementing these choices in life is very difficult. Many can not afford the luxury of such choices. When there is no financial security hard work is a necessity. Such regrets are not much different than daydreams such as, oh I wish I could live in Hawaii and surf everyday. The fact of the matter is that the grass always seems greener on the other side. Speak to the lifestyle guys in their old age. Will they say I wish I worked harder and had a career and made more meaning of life than being a ski bum or surf bum?

Gary Rogan responds:

What you say is true about the effects of exercise. But that's just one of many factors that are biochemical in nature. Pre-natal environment, genetics, and related chemical balances and imbalances are highly important in the subjective perception of the level of happiness. There are proteins in your brain that effect how the levels of happiness-inducing hormones and neurotransmitters are regulated and there is nothing you can do about it without a major medical intervention. Certainly some choices that people make affect their eventual subjective perceptions through the resultant stresses and satisfying achievements in their lives, so the choice part of it can clearly be argued. My main point was that by the time the person is an adult, their disposition is as good as inherited. They can vary the levels of subjective perception of happiness around that level through their actions, but they are still stuck with the range, mostly through no fault or choice of their own.

Since a few literally quotations on the subject have been posted, let me end with the quote from William Blake that was used before the chapter on the biological basis of personality I recently read:

Every Night & every Morn

Some to Misery are Born.

Every Morn & every Night

Some are Born to sweet Delight.

Ken Drees writes in:

I believe that you must put effort towards a goal and that exercise in itself begets a reward that bends toward happiness. It's the journey, not the end result. You must cultivate to grow. A perfectly plowed field left untended grows weeds–the pull is down if nothing is done.

Russ Sears adds:

It has been my experience with helping others put exercise into their lives that few teens and young adults have reached such a narrow range that they cannot achieve happiness in their lives. This would include people that have been abused and people that have a natural dispensation to anxiety. Their "range" increases often well beyond what we are currently capable of achieving with "major medical intervention". As we age however our capacity to exercise decreases. While the effects of exercise can still be remarkable; they too are limited by the accelerated decay due to unhappiness within an older body's capacity. Allowing time for our bodies is an art. Art that can bring the delights of youth back to the old and a understanding of the content happiness of a disciplined life to the young.

It has been my experience with helping others put exercise into their lives that few teens and young adults have reached such a narrow range that they cannot achieve happiness in their lives. This would include people that have been abused and people that have a natural dispensation to anxiety. Their "range" increases often well beyond what we are currently capable of achieving with "major medical intervention". As we age however our capacity to exercise decreases. While the effects of exercise can still be remarkable; they too are limited by the accelerated decay due to unhappiness within an older body's capacity. Allowing time for our bodies is an art. Art that can bring the delights of youth back to the old and a understanding of the content happiness of a disciplined life to the young.

Peter Saint-Andre replies:

Horsefeathers.

Yes, hard work is often a necessity. But hard work does not prevent one from pursuing other priorities in parallel (writing, music, athletics, investing, whatever you're interested in). Very few people in America have absolutely no leisure time — in fact they have a lot more leisure time than our forebears, but they waste it on television and Facebook and other worthless activities.

Between working 100 hours a week (which few do) and being a ski bum (which few also do) there lies the vast majority of people. Too many of them have ample opportunity to bring forth some of the songs inside them, but instead they fritter their time away and thus end up leading lives of quiet desperation.

It does not need to be so.

Dan Grossman adds:

Jim Sogi has a good point. The deathbed regret that one didn't spend more time with one's family is frequently an unrealistic cliche, similar to fired high level executives expressing the same sentimental goal.

The fact is that being good at family life is a talent not everyone has. And family life can be difficult, messy and not easy to make progress with. Which is perhaps one of the reasons more women these days prefer to have jobs rather than deal all day with family.