Mar

31

10 Things We Can Learn From Japan, from Anatoly Veltman

March 31, 2011 | 7 Comments

I didn't make this up, I read it on Facebook and it is pretty interesting:

10 things we can learn from Japan

1. THE CALM Not a single visual of chest-beating or wild grief. Sorrow itself has been elevated.

2. THE DIGNITY Disciplined queues for water and groceries. Not a rough word or a crude gesture.

3. THE ABILITY The incredible architects, for instance. Buildings swayed but didn't fall

4. THE GRACE People bought only what they needed for the present, so everybody could get something.

5. THE ORDER No looting in shops. No honking and no overtaking on the roads. Just understanding.

6. THE SACRIFICE Fifty workers stayed back to pump sea water in the N-reactors. How will they ever be repaid?

7. THE TENDERNESS Restaurants cut prices. An unguarded ATM is left alone. The strong cared for the weak.

8. THE TRAINING The old and the children, everyone knew exactly what to do. And they did just that.

9. THE MEDIA They showed magnificent restraint in the bulletins. No silly reporters. Only calm reportage.

10. THE CONSCIENCE When the power went off in a store, people put things back on the shelves and left quietly.

Jim Sogi adds:

This is the face they want the world to see. What isn't shown is the massive corruption underylying the nuclear plants and electrical system. Much is hidden in the Japanese culture, like an iceberg. You're only meant to see the nice surface. Its a show. Don't be deceived.

Gary Rogan comments:

Is it really deception though? The restaurants didn't cut prices to protect massive corruption in the nuclear plants and the grieving relatives didn't hold back tears to protect the image of the country. The people are orderly, reserved, and polite to each other in public. Are they angels? No.

Mar

31

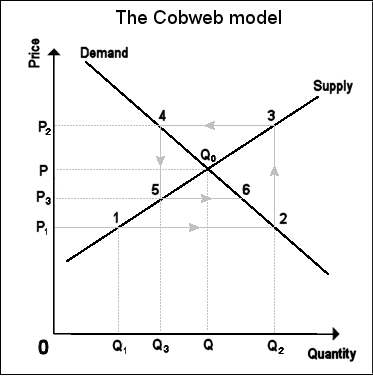

Cobweb Economics, from Victor Niederhoffer

March 31, 2011 | 4 Comments

There's an interesting exercise in cobweb economics setting up in grains.

There's an interesting exercise in cobweb economics setting up in grains.

The idea being that farmers plant for next year based on this year's crop. And when this years price is high, they increase the supply for next year. Thereby lowering the price for the next year. Then they plant less. Prices move in cobweb.

Lorie wrote his PHd thesis on this. Wanted most of all to be a cattle rancher. May corn this year at 6.93 a bushel limit up but December 2012 corn at 5.77.

I took a speculation in honor of Lorie and Watson in the cobweb yesterday and today.

Gary Rogan writes:

Palindrome is taking charge: George Soros making a move to control food and grain production:

Financier and progressive activist George Soros is formulating a move to control food and grain production by purchasing grain elevators in late March in several parts of the United States through his Soros Managment Fund's backed Gavilon Grain . With purchases made in March, Gavilon Grain will become the third largest grain company behind Cargill, and Archer-Daniels Midland.

With strong ties to the Obama administration, Soros now has both the economic, and political clout to begin consolidation of purchasing and shipping domestic agriculture around the world.

U.S. grain firm Gavilon Grain said on Thursday it will buy Union Elevator and Warehouse's 16 grain elevators in the Pacific Northwest , the company's second big purchase of U.S. grain facilities in the last six months.The purchase of 16 elevators at 12 locations in eastern Washington will expand Gavilon's grain capacity by 8.4 mbu.

"The addition of Union Elevator's grain facilities and origination capabilities position us well to support the growing Pacific Northwest export wheat market and serve the Columbian Basin feed grain market," Greg Konsor, VP and GM of Gavilon Grain, said in a statement. The PNW is the No. 1 wheat export terminal in the United States. - Reuters

When food brokers consolidate into just a few large companies controlling the majority of a market, then prices can be set not by supply and demand, but by corporate decisions and manipulation of supply. If the price for food is too low in the United States, then grain can be shipped to other markets for sale, causing then an artifical supply problem in the country that produced the grain itself.With George Soros's making this move in backing Gavilon Grain's purchases to control food and grain distribution in the United States, and becoming the third largest grain company in the country, it will lead to the same results that we see in the energy markets as oil is controlled by a small group of corporations, and the price can be dictated by an artificial control over its supply.

Jeff Watson comments:

Gavilon Grain is just the latest resurrection of Peavey Grain. I expect them to have a big presence in the grain markets as they are true "Grain People." Still, being third place IN THE US behind C@rgill might as well be 50th place. I would not expect the Palindrome to make a dent in C@agill's action, as C@rgill is as politically well connected as anyone. The grain companies were always small in number, and historically were known as the "Big 5." The Big Five were, until the 80's, C@rgill, Continental, Louis Dreyfus, Bunge, and Andre with those companies controlling 75%+ of the world's grain trade and food supply. The big companies still control 75-90% of the grains and food supply, not caring what the prices are as long as they make the deal and don't lose market share. Until recently, most large grain companies were private, family owned corporations. The aforementioned five companies are still private, and huge, but companies like ADM, Ralston Purina, Conti-Commodies, General Mills, Pillsbury, Ralston-Purina, etc are all part of or are public corporations. Despite the small number of grain companies, the profit margins are microscopic, the business is cutthroat, and there is healthy competition between companies, without meaningful quid pro quo's between them. One overlooked aspect of the grain elevators and warehouses is that they are a license to print money if run correctly , which is a reason the big grain companies prefer to remain private, obscure, and below the radar. If C@rgill was a public corporation, it would easily rank in the top ten of the Fortune 500 companies and this is the scale of most of the really big grain companies operations.

Mar

31

Cheating and Attitudes in the Chess Room, from James Tar

March 31, 2011 | Leave a Comment

I am a decent chess player.

I am a decent chess player.

My rating in the room I play in is good, but it varies as much as 250 points. Sloppy play is the obvious factor and is driven by a multitude of reasons: Distractions while watching and trading markets, watching my son, watching tennis, playing after consuming a handful of pints of Stella at the local after the market close with my buddies, or, perhaps just an inconsistent mental capability.

I am often charged with cheating (using a program on the side of the online board). I am not always accused when I beat an opponent who is rated a few hundred above me, but it is often. I don't get upset or offended. Just highly amused.

Chess is a fantastic experiment and exercise of the ego. The fragility of some who typically assume one is cheating when they should just say "well done".

Allan Millhone comments:

Hello James,

At tournaments I always shake hands with my opponent and never make excuses when I lose. I strive to be humble when I win and do my best to guard my ego. I am an average player.

I enjoyed your post and your points.

Regards,

Alan

Mar

31

Racquetball for me started in 1971 at the most pivotal national singles tournament that transformed the sport from amateur to professional.

Racquetball for me started in 1971 at the most pivotal national singles tournament that transformed the sport from amateur to professional.

I was a relative unknown, as was racquetball that year, never having paid it attention except for a few hits against the coming king of the decade, my nemesis Charlie Brumfield. Brumfield had moved from San Diego to become housemates at Michigan State University for the prior summer after I had beaten him in the finals of the '71 paddleball nationals where he screamed at the Flint, Michigan gallery before losing, 'Stick a fork in him, you farmers…he's done!' It was my first championship and when Brum returned to San Diego his mentor, Dr. Bud Muehleisen (present holder of 69 national and international titles) counselled, 'Keeley's your only threat, babe. Go back to Michigan and live and learn from him.' He did, and he did.

Later that year, the '71 national racquetball singles invitational rolled around in Mule and Brum's hometown San Diego. Indeed, they called me a hayseed despite beating in succession the incumbent national champion Bill Schmidtke and New York state champ Charlie Garfinkle, before taking on Brumfield in the quarters.

The tournament is memorable for a couple scenarios. At the time I was collecting $50/mo. under the table from Trenway Sports to use their wooden clunker racquet. Then lo, Bud Leach stood in the doorway of the Invitational host Gorham's Sports Center greeting each of the 16 invitees with a green Swinger racquet newly moulded in his garage and a $20 bill wrapped around the handle. I struck a deal with him for equipment and plane tickets to each of the four national tournaments and invitationals in singles and doubles. My genius doubles partner Charlie Drake, also soon to graduate from MSU with a PhD in sociology, hustled Bud at the tournament, and soon owned 51% of the company.

The craziest instant was losing to Brumfield in the quarterfinals. I took the first game with a serve right to surprise him, he flailed a famous forehand and the ball disappeared. He, the ref and gallery searched but could not find it. We adjourned to the drinking fountain where his Swinger racquet dangled by the thong… with the ball stuck between the handle and frame. He screamed to let the gallery know, 'When's Leach going to string the crotch!'

Bikinied girls handed out awards at the '71 Invitational, the Pacific lapped five blocks away, and a year later this hayseed vet school graduate took the sheepskin to California where a snafu in the vet licensing thrust me into the burgeoning sport pro racquetball.

Mar

31

A First, from Ken Drees

March 31, 2011 | 1 Comment

I never saw a resigned CEO on fin tv before doing some "splainen"– Sokol. Nice of them to invite him on.

I never saw a resigned CEO on fin tv before doing some "splainen"– Sokol. Nice of them to invite him on.

Victor Niederhoffer writes:

What was his explanation for those who don't have the luxury of a tv? Did it seem to be favorable to the sage by indirection? Or seem to indicate that it's the kind of thing that the sage wouldn't do (any more)?

Ken Drees writes:

It was pro buff– and you would have like the analogy used by the talking heads– buff wouldn't have anyone on his staff that wasn't playing directly in the field of play, a tennis analogy that he doesn't tolerate behavior in the organization that is even close to the line but in play. So the dealings by Sokol in lub stock were technically ok, but really not up to full standards of mount st buffet and really it had nothing to do with him "resigning" anyway.

So why all the chatter about the stock dealings if it didn't matter? Sokol wants to be a mini buff now career wise. Thank goodness he didn't resign to spend more time with his kids. The whole thing is odd.

Mar

30

One played a game of checkers with someone likely to be a front runner for president in a few months, and we discussed the importance of Tom Wiswell's proverb "moves that disturb your position the least disturb your opponent the most". In checkers, I think it means not to break up your foundation, not to have too many infiltrator single men far removed from the bulk of your pieces. Not to have too many holes in your position. Not to have too many of your forces divided by big spaces. Maintain your dike which is a solid row of checkers on a diagonal of at least 4 or better 5 or 6. In general, make sure you have near neighbors for all pieces. I got to thinking how this applies to markets. It seems very applicable. Don't put all your chips at one price. Do things on a scale down or up. Don't move into other markets with big positions when you have the bulk in one position. Keep your positions at approx the same size. Don't throw all your chips in at a certain time, but gradualize into positions. Don't get out at close or in at open. Maintain a constant capital stream. Be humble.

One played a game of checkers with someone likely to be a front runner for president in a few months, and we discussed the importance of Tom Wiswell's proverb "moves that disturb your position the least disturb your opponent the most". In checkers, I think it means not to break up your foundation, not to have too many infiltrator single men far removed from the bulk of your pieces. Not to have too many holes in your position. Not to have too many of your forces divided by big spaces. Maintain your dike which is a solid row of checkers on a diagonal of at least 4 or better 5 or 6. In general, make sure you have near neighbors for all pieces. I got to thinking how this applies to markets. It seems very applicable. Don't put all your chips at one price. Do things on a scale down or up. Don't move into other markets with big positions when you have the bulk in one position. Keep your positions at approx the same size. Don't throw all your chips in at a certain time, but gradualize into positions. Don't get out at close or in at open. Maintain a constant capital stream. Be humble.

What else would you say? How would it apply to life? Don't move into new investments unrelated to what you do without much reflection and gradualization. No staccato in your movements into your second childhood? What else?

Anatoly Veltman writes:

To add: a grandmaster can't use the same sole opening pattern all the time. High level competition will adopt– and they will no longer be disadvantaged. So while it's important to stick with your successful patterns– see if those patterns can be validated for situations arising out of a different opening sequence.

Nigel Davies writes:

I agree with Anatoly. Actually I've often given up opening systems at the height of their success; waiting crocs plus loss of vigilance etc.

Jordan Neuman writes:

There is a similar thought in baseball strategy. In a situation where one's move will lead to countermoves, it is sometimes best to do the opposite of what your opponent wishes you to do given his perception of his own countermove options.

This is all under the general category of putting yourself in someone else's shoes. I find it very easy to see where others have messed up their or their children's lives. I would say my "win percentage" is much higher in those cases, prospectively, than in my own life. Perhaps the Wiswell proverb describes depersonalizing decisions as a way to make them less emotionally difficult.

Henry Gifford comments:

Regarding the above about ruining the lives of one's children, my uncle used to say he ruined the life of his son, who was a heroin addict.

Looking at what he said from the other side, if what my uncle said was completely true, then parents have the power to stop their children from doing drugs or partaking in other ruinous activities, something many parents are frustrated to know is not true.

This perspective can ease the pain in some situations in life, and maybe in trading losses also.

Allen Gillespie writes:

On the violin to play fast one must leave fingers down for the return.

Mar

30

Proverb of the Day, from Victor Niederhoffer

March 30, 2011 | Leave a Comment

One of Tom's favorite proverbs on the "moves that disturb" point was "take care of the draws and the wins will take care of themselves." I like the Greek proverb "little strokes fell great oaks" and of course Sondheim in his hateful way takes that song in Company and makes it "it's the little things you do together… that make marriage a joy," as he shows two couples fighting like cats and dogs.

One of Tom's favorite proverbs on the "moves that disturb" point was "take care of the draws and the wins will take care of themselves." I like the Greek proverb "little strokes fell great oaks" and of course Sondheim in his hateful way takes that song in Company and makes it "it's the little things you do together… that make marriage a joy," as he shows two couples fighting like cats and dogs.

It would be interesting to see if Nigel agrees that "moves that disturb chess positions the least" are best. I believe Art Bisguier told me to try not to break the tension of a position, and I've also been told that once you give away which side of the board you're likely to castle from, the handwriting is on the wall.

Ken Drees comments:

Sultan Khan an Indian native master player from the 1930s used to wait very long to castle and sometimes not at all since castling was not a legal move option in India where he was schooled in chess. It seems like everychanging strategy and recycling (switches) always is necessary to stay competitive, and fresh. Playing against the unorthodox– like the basketball team full court press (Mr. Watson's recent post), or the uncastled king that seems content in the center with a closed position game illustrates the need to be able to counter the strange or unusual opponent. Get a "book" player out of his book and then your fundamentals will hopefully give you an edge. The emotions that occur when faced with the unorthodox style are one more element that the aggressor has in his favor and one more item that the level headed player must tamp down and counter internally.

As for building and constructing ever more powerful latently strong positions–Nimzovich comes to mind as a chess stylist who always made incrementally stronger and stronger tactical moves. This tension naturally releases at some point in the game and then the gameboard takes on fresh vistas of open lines and changed landscapes. Seeing the new and powerful layouts well ahead of your opponent is key to the entire buildup process.

Mar

30

Drilling to the Earth’s Mantle, from Pitt T. Maner III

March 30, 2011 | Leave a Comment

Drilling to the earth's mantle and the Mohorovičić discontinuity was pursued by the USA back in the late 50s and early 60s under the name Project Mohole and then attempted by the Russians on the Kola peninsula in the 70s and 80s. Thoughts of drilling to the earth's mantle to find out what is there are being revived.

Drilling to the earth's mantle and the Mohorovičić discontinuity was pursued by the USA back in the late 50s and early 60s under the name Project Mohole and then attempted by the Russians on the Kola peninsula in the 70s and 80s. Thoughts of drilling to the earth's mantle to find out what is there are being revived.

1) from a national geographic article:

It may not be a journey to the center of the Earth, but it could be the closest thing yet.

Scientists are planning to drill all the way through the planet's miles-thick crust to Earth's deep, hot mantle and retrieve samples for the first time. The samples, they say, would rival moon rocks for sheer scientific import—and be nearly as hard to get.

"That has been a long-term ambition of earth scientists," geologist Damon Teagle told National Geographic News. But a lack of suitable technology and insufficient understanding of the crust have long tempered that ambition."

2) Check out a second article in April 1961 Life magazine written by John Steinbeck during his time on board CUSS 1 at the start of drilling for Project Mohole.

Charles Pennington asks:

The best place to drill, Teagle said, is in the mid-ocean,

because that's where Earth's crust is thinnest—only about four miles

(six kilometers) thick, versus tens of miles deep in continental

regions.

Is there some simple explanation of how we even know how thick the

earth's crust is and what's below it when we've never drilled through it

before?

Pitt T. Maner replies:

It's the depth at which the seismic velocity changes probably due to a compositional change to periodotite type minerals with perhaps some changes due to temperature regimes.

So the only samples that geologists have to look at from mantle depths were brought to surface enclosed in magma as xenoliths.

Other than that there are probably lots of questions as to what will be

found and whether the mantle differs from location to location in

composition.

One question they hope to find out is how deep life extends below the earth's surface.

A lot has been learned since I studied Geology 29 years ago.

Mar

30

Why America Doesn’t Play Cricket, from Sushil Kedia

March 30, 2011 | Leave a Comment

Cricket is played at all places where the English language has been, from across the Indian Sub-continent, South Africa, Australia, West Indies and even in Canada. America doesn't play this game. What could be the significance of this? America innovates its own games? Soccer played the American way is very distinct from how its played elsewhere, for an example.What do the sports historians trace this to?

Cricket is played at all places where the English language has been, from across the Indian Sub-continent, South Africa, Australia, West Indies and even in Canada. America doesn't play this game. What could be the significance of this? America innovates its own games? Soccer played the American way is very distinct from how its played elsewhere, for an example.What do the sports historians trace this to?

Does this reflect a certain way in which America has come to be what it is and can it provide any insights on how markets and business in general may have been structured differently for, social innovation factors, if any that may have brought a different way of team sports and games in America?

Stefan Jovanovich comments:

Baseball is a direct descendant of another British game - rounders, which was played by the Scots and the Irish. Cricket was the "polite" game played by the English; rounders was the "rowdy" one played by the people whose allegiance to the Crown was dodgy at best. As the Brittanica entry illustrates, "rounders" has had to be banished from the official record on both sides of the Atlantic: in Britain because it is a reminder of the awful days of real disunion and in the U.S. because we all know baseball was invented by Abner Doubleday.

Mar

30

John “Earthquake” Milne: Father of Modern Seismology, from Pitt T. Maner III

March 30, 2011 | 2 Comments

The life of John "Earthquake" Milne, developer of the horizontal pendelum seismograph ("Father of Modern Seismology') is well worthy of a screen or stage play.

The life of John "Earthquake" Milne, developer of the horizontal pendelum seismograph ("Father of Modern Seismology') is well worthy of a screen or stage play.

A quite fascinating person and true gentleman from the Victorian-age. Milne is remembered and honored by the Japanese for his contributions to seismology but little known on his home turf (Shide, Isle of Wight, England) where a pub evidently is named after him.

He must have had a very good sense of humor as this account relates:

'When the seismograph had been set up,' he recalls, 'Milne visited it often but nothing ever seemed to happen. Then, one day, the Professor was excited but puzzled to find a series of enormous swings on the trace for which he could not account. A week later and at the same time of the day they appeared again. Milne eventually deduced that the records were made when the butler and the housekeeper were both off duty together!'

- Earthquake Milne and the Isle of Wight by Leslie Herbert-Gustar and Patrick A. Nott, Vectis Biographies (1974)

Paul Kabrna has written a book about Milne and it is ironic that Milne's great-nephew is pictured holding a print of a Japanese tsunami. Milne's elegant,Japanese wife Tone is frequently shown in pictures from the seismological observatory in Shide, Isle of Wight and must have been a great help and support to Milne.

This great-nephew, Australian doctor William Twycross is making a documentary about Milne that will likely be completed in time for the 100th year commemoration of Milne's death.

from an article about him:

'The English-born Milne was the first to scientifically measure tremors so that he could delineate the earthquake fault line near Japan's east coast, one of many feats that clearly impressed Dr Twycross. "He was quite an extraordinary man, a watercolour artist, an ornithologist, an archaeologist, a very inventive geographer, an inventor, and he played the piano very well, very much a man of the people," he says.'

Mar

30

Quotes of the Day, from Jeff Watson

March 30, 2011 | 2 Comments

Throughout history, poverty is the normal condition of man. Advances which permit this norm to be exceeded—here and there, now and then—are the work of an extremely small minority, frequently despised, often condemned, and almost always opposed by all right-thinking people. Whenever this tiny minority is kept from creating, or (as sometimes happens) is driven out of a society, the people then slip back into abject poverty.

–Robert Heinlein

Mar

30

Best Online Poker Player in the World, from William Weaver

March 30, 2011 | 4 Comments

Here is a very interesting article on a 21 year old online poker player, Daniel Cates. Some facts about him:

Here is a very interesting article on a 21 year old online poker player, Daniel Cates. Some facts about him:

1. Highest online poker earnings in the world in 2010

2. Treats dollars as points, not real money

3. Doesn't understand the utility of the value of $n,000,000; believes this is an edge; less fear/emotion

4. End goal is to create a balance of life and connect the poker player with the person

5. Hypothesis that video games create good real-time decision makers, able to process lots of data, control emotions while taking risks, be aggressive and create seemingly random decisions when they are anything but

6. Extremely conservative spender, yet eats fancy meals at cheaper restaurants (good money management)

Jeff Watson writes:

Ahem. Some people may well have formed the impression that that kid might be cheating.

Jay Pasch comments:

Or reading the cards as they lay, a good bluffer with bad cards, much like a futures trader…

Anatoly Veltman asks:

Could you expand: how is trading = bluffing?

Jay Pasch responds:

Please go read Wall Street books that were printed over 75 years ago. There are countless tactics that are out there and I will restrain from this lesson in taking away from the ability for you to learn on your own. I will however suggest that The Chair has just published about three posts in the last two months that give insight of this tactic of bluffing, just not directly coming out and saying that those who implemented were bluffing.

A couple of points worth mentioning, are that 1) You have heard the sayin' "Paintin' the Tape" 2) Remember it is commonly quoted that Institutions due to vig being lower have taken the individual stock tradin' biz away from small fries 3) Bluffing is form of trading that is categorically multi dimensional not just "buy" or "sell". 4) common trait not learned in law school but one that is picked up in practice is the art of "re-direction" while in trial.

The power or leverage to bluff these days lies in the hands of those that have positions in the respected markets that they choose to bluff with such deep pockets that for you and I to do so is laughable.

Better to learn countin' than bluffin'. Though bluffin' still exists.

J. Humbert adds:

Did this story make it to the US?

Two traders exploited a weakness in Timber Hill's robot. They made some small orders in illiquid stocks (to push up the price). Then the robot would place a large bid above the average purchase price and they could sell with a profit. They repeated this many times and made something in the $100k ballpark, I believe. Then they got convicted. It's apparently illegal to be smarter than a robot.

Mar

30

Outside Days, from Steve Ellison

March 30, 2011 | 1 Comment

Monday was an outside day for the S&P 500 futures, and the close was lower than the low of the previous day. Tuesday was another outside day, this time with the close higher than the high of the previous day. This sequence has occurred only twice in the past 6 years. The changes on the third days in those instances were -1.7% and +0.3%.

Tuesday was the 47th outside day on which the close was higher than the high of the previous day in the past 6 years. After the previous 46 instances, the next day was up 24 times and down 22 times, t=-0.12.

Mar

29

Greenspan and Government Activism, from Paolo Pezzutti

March 29, 2011 | Leave a Comment

We have discussed the role of government in the economy and during crisis many times on this site. Greenspan writes about this topic with the paper "Activism" that I recently read. He writes:

We have discussed the role of government in the economy and during crisis many times on this site. Greenspan writes about this topic with the paper "Activism" that I recently read. He writes:

The current government activism is hampering what should be a broadbased robust economic recovery, driven in significant part by the positive wealth effect of a buoyant U.S. and global stock market.

Equity values, in my experience, have been an underappreciated force driving market economies. Only in recent years has their impact been recognized in terms of 'wealth effects'. This is one form of stimulus that does not require increased debt to fund it. I suspect that equity prices, whether they go up or down from here, will be a major component, along with the degree of activist government, in shaping the U.S. and world economy in the years immediately ahead."

Considerations about the wealth effect are in my view interesting, but well known to those who tried (and managed) to steer a recovery from the crisis.

The wealth effect has supported the economy so far. How much compared to the "stimulus" is hard to say however. "Manipulation" of markets in order to favor a continued move to the upside concerted by strong hands was (and is) in the interest of many forces who have a prominent role.

Victor Niederhoffer writes:

The wealth effect was very big in the 1960s and before, and Latane had good papers on it. Everyone at the Fed has believed in it for 70 years, to the exclusion of looking at interest rates themselves. And Bernanke often times his qualitative announcements with market lows or highs. A good way to trade.

Phil McDonnell writes:

Most of the so called wealth effect is really artificially induced by the QE programs. If the price of your stock rises but the value of the dollars the stock will fetch falls then are you really wealthier? How rich do the folks in Zimbabwe feel?

Jeff Watson writes:

One only has to look at the Weimar to see how the business class in Rhodesia feel. In 1913, the German stock market was at 126. Fourteen years later, the German stock market was at 26,890,000. At the index peak, the value of the Daimler company was only worth 327 of its cars. Interest rates were 900% and the exchange rate went from 4-5 marks per dollar in 1913 to 4+trillion marks per dollar in 1923.

Ian Brakspear writes in:

My portfolio in 1994 was worth aprox ZIM$10 million in 2005 worth ZIM $ 44 billion.

Victor Niederhoffer comments:

What they did to the farmers makes one cry. Brakspear is the guy that posted the funniest spec post ever. He ordered 2 beers for lunch. It was 10 million Zimbabwe. Then by the time he finished lunch, he ordered two more. The price had risen to 15 million Zimbabwe.

Kim Zussman asks:

So does inflation illusion work? What does it feel like to be a billionaire?

Ian Brakspear comments:

I have in my wallet 2 fifty billion dollar notes, a one hundred billion dollar note and one ten trillion dollar note-worthless.

Today the main currency in the streets of Zimbabwe is the US$– how all these US$ notes got here is anyone guess.

They are cleaned regularly in washing machines to prevent the spread of diseases– and hung out to dry on washing lines– always with someone on guard.

Mar

29

Primism, from Kim Zussman

March 29, 2011 | 1 Comment

Nine fatal flaws of hominid finance:

9. Laziness

8. Vanity

7. Hubris

6. Poorly equipped

5/4. Free-riding / dependency

3. Vendetta

2. Distraction

1. Fearlessness

Mar

29

Using Improv for Business, shared by Kim Zussman

March 29, 2011 | Leave a Comment

Here is an interesting article on using improv for business:

"Improvisational comedy offers valuable lessons to business, says Lakshmi Balachandra MBA ’04. An improv comic before working in venture capital and finance, Balachandra brought her spontaneous theater skills into the classroom …"

"Improv teaches you how to think on your feet, she says, to accept the facts, and then build on them. All these are excellent business and negotiation skills. In a CNN article, she offers her five rules of improv:

1. 'Yes, and.' Accept a situation and then deal with it.

2. Avoid asking questions. Continually asking questions makes other

people do all the work.

3. Listening. Focused listening is a crucial skill.

4. Add information. Contribute if you want to guide the conversation.

5. Eye contact. In the workplace it’s important to pay attention to

body language."

Russ Sears writes:

While not improv, here is a humorous Toastmaster speech I gave last year. It won at the club level.

This might have some lessons on risks and reward; parenting and other humorous topics when we think we have it all mastered.

And for those that have not meet me; you get to see my pretty face.

Mar

28

"It is common to think of individuals to use genes to make more individual, but from the gene's eye view of evolution, its the other way around. Genes use individuals to make more genes. The chicken is the egg's way of making more eggs". p. 114 The Seventy Great Mysteries of the Natural World edited by Michael Benton.

"It is common to think of individuals to use genes to make more individual, but from the gene's eye view of evolution, its the other way around. Genes use individuals to make more genes. The chicken is the egg's way of making more eggs". p. 114 The Seventy Great Mysteries of the Natural World edited by Michael Benton.

Yes, and its the digits of the prices way of replicating itself to make individual market players create more of those digits. (I wrote about this before here).

The digit 0 plays a big part in the replication game, and it makes individuals sacrifice themselves to create more 0's.

One notes for example that the double digit 00 in 1300 on the sp has been broaches from below on a closing basis from Feb 03 on three times and gone from above to below on three times.

Similarly for the triple digit 000 in 12000 on the DJI. The DAX crossed the triple digit 7000 on Jan 3rd from below, went above below then above then below on Jan 07, then crossed to 7097 on Jan 13 but stayed above 7000 until March 14, then fell to 6436 on March 16, a decline of 10% for the year, and now for the first time on March 25 hit a high of 7006 but failed to close above 6981, a fact which must cause great disennu to the triple 0's in 7000 and they must be inducing much political change in Germany as we speak to achieve that level.

Similar analysis relates to the Nikkei at 10000 which crossed below 10000 on March 11 briefly, but closed at 100075 and then on the following two days declined 20% captures by the triple 000 at 8000 as its low was 7790, a decline of 25% from its mid December levels of 10300.

A similar analysis could be made with the grains especially corn which has shown a similar affinity to 700 as the Dow to 12000 and the SP to 1300.

Instead of taking closing prices for granted we should ask how the digits themselves influence our actions so that we can make them reappear over and over again.

Kim Zussman writes:

A simpler version of this is the opposite of the usual "the market did Y today because of X": We say X because it did Y and we need why.

The evidence is that for many similar X there are many dissimilar Y.

Price is selfish because its impact demands explanation.

Gay Rogan comments:

I'm having trouble understanding any of this. Genes are selfish in the following sense: if genes don't propagate, they disappear, so the only genes that are here today are proven propagators. How can prices or digits permanently disappear? And why would 0's propagate more than other digits? How do these explanations provide more clarity than simply saying people's brains are attracted to numerical markers, and in the absence of other alternatives they chose round numbers?

Steve Ellison comments:

One possible line of reasoning is that people are more likely to put limit orders at round numbers. People often put stops near round numbers, too, but the research I have seen suggests stops are more likely to cluster on the opposite side of a round number from the current price. Here, then, is a hypothesis: if the last two digits of the S&P 500 closing price are above 90 or below 10 (i.e., near a 00 round), the change the next day is likely to be in the opposite direction as today; if the last two digits are above 10 and below 90 (i.e., away from the 00 round), the change the next day is likely to be in the same direction as today.

Checking the last 1584 trading days of the futures,

Near 00 round:

N: 366

reversal next day: 194

unchanged next day: 3

continuation next day: 169

% continuations excl unch: 46.6%

Away from 00 round:

N: 1200

reversal next day: 592

unchanged next day: 15

continuation next day: 593

% continuations excl unch: 50.0%

The percentage of reversals was higher near rounds, but the difference was not significant.

What was significant was the number of closes near the rounds. One would expect a close within 10 points of a round about 20% of the time, but 23% of actual closes were within 10 points of a round, p=0.0006.

Victor Niederhoffer writes:

Here is an interesting paper on round numbers for individual stocks. It doesn't look at expectations, but does look at bid

asked.

Russ Sears writes:

I believe that this paper could be expanded measure this effect on high volume versus low volume stocks. Therefore its stated cost may not be as large as expected on all stocks. My guess, needing testing is the small stocks have this more frequently than the large stocks, that are often computer traded.

Mar

28

Letter to the Editor, from Donald Boudreaux

March 28, 2011 | 4 Comments

What's good for the green goose is good for the differently colored gander.

What's good for the green goose is good for the differently colored gander.

………………………………….

Editor, USA Today

Dear Editor:

Bjorn Lomborg explains that "Earth Hour" is about feel-good self-indulgence and not about actually changing the world for the better ("'Earth Hour' won't change the world," March 25).

The reasoning that leads "Earth Hour" celebrants to conclude that humans "waste" resources producing artificial lighting and other modern amenities leads me to conclude that "Earth Hour" itself wastes humanity's most precious resource: creative human labor.

In the hour when lights are switched off for the "mere" purpose of making a political statement, much human labor is wastefully idled. During that hour, the process of de-polluting our clothing ("doing the laundry") doesn't happen; likewise for the process of de-polluting our dinner dishes and, indeed, de-polluting our bodies. During that hour, there's less studying for upcoming exams in physics or histology or 19th-century Russian literature. And that tinkering in the garage on projects that might be the progenitors of tomorrow's super-computer, water-fueled automobile engine, or other technological marvels that promote human well-being? It doesn't occur. One entire hour of human creativity down history's drain, lost forever. Kaput.

Of course, if Jones wants to make a political statement by turning off her lights for an hour, she should be free to do so. It's her business and it isn't really wasteful. But Jones should see that if Smith keeps his bulbs burning brightly, she has no more basis for accusing him of "wasting resources," "destroying the planet," or "threatening our children's future" than he has for accusing her of the very same offenses.

Mar

28

Five People Screwed by History, from Jeff Watson

March 28, 2011 | 1 Comment

Here is a humorous article that demonstrates the way history is written is not necessarily the way things really unfolded, or even includes the correct people. Written history is not accurate, and the old saying, "History is written by the winners," is self evident. Because of agendas, PC, and other forces, many historical figures were overlooked in order to make the history more glamorous, or whatever. Needless to say, this quick read is funny and will open your eyes. Unfortunately, all of these people cast aside were the losers, along with the succeeding generations who get an inaccurate portrayal.

Mar

28

The American Dream, from L. J. Endicott

March 28, 2011 | 3 Comments

What is the American Dream?

What is the American Dream?

The Dream is to work, to have a home, to get ahead. You can start as a janitor and become the owner of the building. The American Dream is not written into the constitution but it is so ingrained in the national psyche that it might as well be.

Bo Keely comments:

The American Dream is still alive and that's why I return occasionally to USA from globetrotting to selective Shangri-Las around the world. Though the American Dream there is diminished and threaded with nightmares, after 100+ countries it's still the best place to own property, work to get ahead, and use as a base to travel from during retirement.

Mar

28

Tracking Your Reading, from Dylan Distasio

March 28, 2011 | 2 Comments

I'm about to sit down to read L'Amour's memoir Education of a Wandering Man. One of the things about this book that immediately appeals to me is that he kept a record of everything he read between 1930-1937 that is available at the back of the book. As someone who loves to read, and also loves lists, it doesn't get much better than this. As an aside, if you're a list fanatic like me, check out Eco's The Infinity of Lists : An Illustrated Essay.

I'm about to sit down to read L'Amour's memoir Education of a Wandering Man. One of the things about this book that immediately appeals to me is that he kept a record of everything he read between 1930-1937 that is available at the back of the book. As someone who loves to read, and also loves lists, it doesn't get much better than this. As an aside, if you're a list fanatic like me, check out Eco's The Infinity of Lists : An Illustrated Essay.

I thought I would share some tidbits on his reading appetite.

Over this 8 year time period, he read 731 books. This works out to roughly:

91.4 books a year

7.6 books a month

1.9 books a week

There are a lot of interesting items on his list. His interests appear to cover a wide range of topics and authors. Everything from detective stories to Nietzsche is on here.

Bo Keely writes:

Thanks for the reminder & fresh info on L'Amour, who single-handedly thrust me into a lifetime of adventure and escape. My favorite short story is 'the strong shall live' about a cowpoke who gets stranded in the blazing desert near my rancho where one day and night I unintentionally re-enacted the plight and escaped, with a L'Amour tip, by finding a stone cistern of water and spitting guppies, but lived.

Mar

28

Is the War Business Unaffected by Recessions, from Pitt T. Maner III

March 28, 2011 | Leave a Comment

Is the war business unaffected by recessions? :

Despite the continuing global economic recession in 2009, the total arms sales of the SIPRI Top 100 of the world's largest arms-producing companies increased by $14.8 billion from 2008 to reach $401 billion, a real increase of 8 per cent, according to new data on international arms production released today by Stockholm International Peace Research Institute (SIPRI).

Many Swedes have been surprised by recent newspaper articles detailing shipments to questionable customers. Actions have been taken to curtail some of those sales (for now):

"We have withdrawn licences (for weapons exports) to two countries … due to the situation in the region," Andreas Ekman Duse, the head of the Swedish Agency for Non-Proliferation and Export Controls (ISP), told AFP.

"We cannot say which countries, due to commercial and diplomatic classified information," he said.

His agency, which controls Sweden's exports of military equipment, would closely watch the situation, and the licences could be restored "if the development in these countries goes in a democratic direction," he said, adding "when that will happen I cannot say."

Mar

28

Review of Armadillo, from Marion Dreyfus

March 28, 2011 | Leave a Comment

Armadillo

Armadillo

Directed by Janus Metz and Lars Skree

In February 2009 a group of Danish soldiers, accompanied by documentary filmmaker Janus Metz, arrived at Armadillo, an FOB [Forward operating Base] army camp in the south Afghan province of Helmand. For six months, Metz and cameraman Lars Skree shadowed the doings of young Danish soldiers situated less than a kilometer from dug-in Taliban nests. The outcome of their work is a gritty and almost unbelievably authentic war drama that justly won the Grand Prix de la Semaine de la Critique at the 2011 Cannes Film Festival. Because of the nature of the disclosures in the record of the men's hitches, however, it provoked a firestorm of debate back in Denmark over the controversial behavior of certain soldiers during one pitched shootout with Taliban killers. But 'kinetic military activity' tends to be messy, and not subject to parental supervision.

Through the early tedium of their military entrenchment, through the nightly porn viewings and the computer games, the calls home to Mom on field telephones, through to the steely tension of encounter with the enemy, the filmmakers repeatedly risked their lives shooting this tense, brilliantly edited, and visually sophisticated mirror of the psychology of young men in the midst of a vaguely defined war whose victims seem to be primarily local villagers and farmers. At one point, village Afghanis ask some of the men if they are Jewish or Christian. Momentary pause. "Christian." They ask: American? British? "Danish." The Afghanis are up on their PC bonus points. Surreal scenes remind us that this is a civilian arena, as local children seeking sweets and leftover food rations pop up while the men pick their way through poppy fields ripe for opium manufacture, shooing them off kindly after sharing their food with them. More jostling than scenes in which Taliban tracers zing past their portable cameras is the unblinking footage of the handsome, tattoo'ed and unblemished soldiers as each tries, in the face of constant provocations and problems, to come to terms with waking each day to the realities of being in a terrain of rubble, faced with lethal enemies they rarely see except via overhead drone transmission, green screen computer paradigms and the hasty exits of black-blogged women and children fleeing their villages in advance of what they know to be gunfights ahead.

They are Special Forces, and the array of their equipment is majestic, including medics and translators who play key roles throughout in interplay with the agri harvesters and farmers. Their panoply of gear is the last word in impressive-and contributory to their ability to shout hectic instructions in the field of combat on helmet mikes, making the combat not only frightening, but loud and punctuated with noises and static-y orders, cautions and warnings.

THE HURT LOCKER comes to mind repeatedly, as does APOCALYPSE NOW. But this cinema verite on the ground is something else. Those dead in the ditch are real men, and that is a real corpse. Though the men are warm and comradely with each other, we rarely catch them openly admitting how existentially terrifying their days and nights are with lives constantly on the line. The CO, commanding officer, seems exceptional, articulately reviewing each expedition and engagement, praising the men when needed, upbraiding them when they are careless, reporting on the progress of med-evac'ed comrades back in Denmark hospitals. Awarding the men, who started out at 180 cocky guys, patches of honor, all too aware of the fragility of temporary successes.

They seem admirably prepared, but how prepared is anyone, in the end, to having an IED blow off a leg? Their time is marked off, titles indicating each month, but each day of continued breathing undamaged, alive, a triumph against the inevitable encroaching odds.

________________________________

In Danish, Pashto and Dari. Subtitled in English.

Mar

27

A Good Sunday Read, from Jeff Watson

March 27, 2011 | 2 Comments

A few years ago, Gladwell wrote an interesting story on how the underdog can beat the favorite. When the underdog plays the favorite's game they lose around 65% of the time. When the underdog refuses to play the favorite's game and plays another game entirely, the win/loss reverses and they win over 60% of the time. This magnificent article has many, many lessons in trading and life in general.

A few years ago, Gladwell wrote an interesting story on how the underdog can beat the favorite. When the underdog plays the favorite's game they lose around 65% of the time. When the underdog refuses to play the favorite's game and plays another game entirely, the win/loss reverses and they win over 60% of the time. This magnificent article has many, many lessons in trading and life in general.

Russ Sears comments:

I loved this article also, and have recommended it to many non scientific minded friends.

However, like many of Gladwell's writing that are entertaining summaries of other experts ideas, I believe he misses some of the more relevant points. Perhaps it is literary license, to make it more entertaining to the masses, or perhaps, it is just poor science to focus on what he believes can tie these ideas all together in a nice neat package without the lose ends that reality always messes up tight arguments.

While I can not disagree with his lawyer like presentation style of writing quasi scientific pieces for marketing purposes, most of his works leave me wishing to talk to the real expert's and scientist's whose life work he is putting into these boxes… to get the real story. The end result I believe is that his work often over-reaches to make a scientific case for his pet ideas. In my opinion, the masses buy them as "science" but they tend to fall apart when the rigor of science is really applied.

One thing that bothered me about this piece was his glossing over hard training to achieve the fitness level of the players for the underdog basketball teams. Knowing a few things about how to get peak running performance out of somebody. It would seem that while those coaches that get their players to consistently peak during the March Madness Tournament would have to loss a few games that they could have won because the players trained too hard and did not sufficiently recover. During the regular season the players would have to train so hard they leave their game on the practice field and loss some to teams that have less talent but are fresher. Then near the tourney, the coach would lighten up the practices to let them peak at the right time. Cardiovascular wise you can only really peak for a little over a month. It would appear to me that those teams that are coached to win every game during the regular season would be ranked higher than they should because they cannot "peak" any more. While those that worked harder, lost more games due to fatigue, are ranked lower than they should be. In other words are they "underdogs" because they train so hard during the regular season that they can peak higher than the other teams or are they Cinderella teams like David because they are prepared and fit enough to attack Goliath.

Also the pacing of the game must be such that the underdog's players are able to still match the jump and burst of speeds of the other team at the end. Some of this can be achieved by burning out the other team's fast twitch muscles early on…but some of this also has to be taught to strategically hold back a little at first, so your team does not suffer the same fate.

I have not watched any game this year, I have been too busy, however, this may explain why all the underdogs are left. And Gladwell may very well have made this style of coaching popular in basketball today. Whatever it is teams like Butler certainly have made the tourney exciting this year.

And while I think the numbers may be overstated, it would appear that there is some substance to the 3 ideas he states that underdogs should try:

1. Take an unconventional approach,

2. Try harder than the top dogs

3. Aggressive attack with determination and no thoughts of losing.

The first one helps you believe in yourself, that it is possible. The second gives you moral basis for why you should win. And the third can stun the others into thinking you will win.

Mar

27

Why a Climactic Move is the End, from Kim Zussman

March 27, 2011 | Leave a Comment

A young boy enters a barber shop and the barber whispers to his customer, "This is the dumbest kid in the world. Watch while I prove it."

A young boy enters a barber shop and the barber whispers to his customer, "This is the dumbest kid in the world. Watch while I prove it."

The barber puts a dollar bill in one hand and two quarters in the other, then calls the boy over and asks, "Which do you want, son?" The boy takes the quarters and leaves the dollar.

"What did I tell you?" said the barber. "That kid never learns!"

Later, the customer leaves, and sees the same young boy coming out of the ice cream store. He asks. "Hey, son! May I ask you a question? Why did you take the quarters instead of the dollar bill?" The boy licked his cone and replied, "Because the day I take the dollar, the game's over!"

Mar

26

Grain Prices, from Jeff Watson

March 26, 2011 | Leave a Comment

Farm Journal surveyed farmers and found out some very interesting facts, opinions, and intentions. Corn production is going to increase 3.37% while soybean production will decrease 3.46%. Farmers might decrease production of hay to grow more corn or beans. Increased corn or bean production will come at the expense of either corn or beans depending what the farmers shift to. Cotton farmers plan on growing more cotton at the expense of their corn crops. 24% of respondents plan on waiting until planting time to determine what crops they will plant. 56% are making their decisions based on crop rotation.

Farm Journal surveyed farmers and found out some very interesting facts, opinions, and intentions. Corn production is going to increase 3.37% while soybean production will decrease 3.46%. Farmers might decrease production of hay to grow more corn or beans. Increased corn or bean production will come at the expense of either corn or beans depending what the farmers shift to. Cotton farmers plan on growing more cotton at the expense of their corn crops. 24% of respondents plan on waiting until planting time to determine what crops they will plant. 56% are making their decisions based on crop rotation.

The article also has break even levels for prices which would induce farmers to shift acreage to other crops.

Mar

26

Doctors Without Data, from Pitt T. Maner III

March 26, 2011 | Leave a Comment

This is an article about craft, intuition, art, and "feel" vs science. It's an article and book sure to raise a few hackles in the medical community. Perhaps there are some associations to investing.

This is an article about craft, intuition, art, and "feel" vs science. It's an article and book sure to raise a few hackles in the medical community. Perhaps there are some associations to investing.

I believe most physicians practice in a virtually data-free environment, devoid of feedback on the correctness of their practice. They know very little about the quality and outcomes of their diagnosis and treatment decisions.

And without data indicating that they should change what they're doing, physicians continue doing what they've been doing all along.Physicians rely heavily on the "art" of medicine, practicing not according to solid research evidence, but rather by how they were trained, by the culture of their own practice environment and by their own experiences with their patients.

Mar

26

75 Years of American Finance, from Jeff Sasmor

March 26, 2011 | Leave a Comment

Here are some interesting bits of history:

75 Years of American Finance: A Graphic Presentation 1861-1935

In 1861 the public debt (according to this doc) was 75 million, a whopping $2.83 per capita.

1862 saw the Legal Tender act "150,000,000 Greenbacks authorized".

1866 "this year income tax collections hit peak $73,000,000".

And so on.

Mar

25

Quote of the Day, from T.K Marks

March 25, 2011 | Leave a Comment

There is a quote from the estimable Walt Frazier in this morning's NYPost that echoes in verbatim spirit what Vic's been saying for some time now.

Toward the end of the game against the Celtics he frustratingly observed: "The Knicks are not attacking, not trying to get to the hoop, man. They're just hanging out on the perimeter. See? Look where they are, 30 feet from the basket!"

Mar

25

Rebecca Black’s Friday and the Market, from Kim Zussman

March 25, 2011 | 2 Comments

There appear to be deeper messages in this music "Friday" by Rebecca Black– ostensibly market related:

There appear to be deeper messages in this music "Friday" by Rebecca Black– ostensibly market related:

One notes that in 2011 Fridays have not been particularly strong, but Mondays gave Fridays reason to celebrate (attached compares mean of weekday returns of SPY, cls-cls).

Jan Petter-Janssen writes:

Talking about music… Korean pop is extremely inspired by American culture.

The kids over there apparently cherish individualism and internationalism. It's a very good sign for Korea's future, isn't it?

How do I know about all these? It's impossible not to hear these in Singaporean malls. Much better than Justin Bieber though.

PS: Make a YouTube search on "Indian pop". It's a totally different story.

PS2: Also Chinese pop features some English. And materialism to the extreme…

Mar

25

Reminds Me of the Boy Wonder, from Victor Niederhoffer

March 25, 2011 | Leave a Comment

The moves in Ford where it breaks through a round number and then opens at the high, and goes straight down reminds me of the incorrigible boy wonder who loved to buy a stock like Anaconda when it wend above 200 for first time, and then to scale into it on a pyramiding basis as it went up.

The moves in Ford where it breaks through a round number and then opens at the high, and goes straight down reminds me of the incorrigible boy wonder who loved to buy a stock like Anaconda when it wend above 200 for first time, and then to scale into it on a pyramiding basis as it went up.

The boy wonder must have enjoyed much pleasure from the follies Bergeres girls on his payroll during those moments before he was led into bankruptcy again with such activity.

Jay Pasch writes:

And what better place to open it than right on the 15.18 gap…

Mar

25

Quote: We Are in the Middle of an Epochal Tectonic Shift, from Paolo Pezzutti

March 25, 2011 | 1 Comment

Here is an interesting article about oil: "we are in the middle of an epochal tectonic shift" by Lars Schall.

The hegde funds and banks, who control and own the NYMEX, the ICE Futures and the Dubai Exchange, are using the Middle East events. I think they want to try to use that to push the price up to maybe $ 150 to 200 per barrel over the next months. And why? In order to put massive political pressure on Germany and the European Union.

[…]

Since the end of the First World War, I would say, that the quality of the strategic economic thinking in Germany has become significantly reduced, especially after 1945 and the US-guided German "re-education" efforts. How well the Berlin government understands that this is a currency war against the euro, because the euro is the only currency on the block today worldwide, certainly not the Chinese Yuan or the Japanese Yen, which could challenge the hegemony as a reserve currency of the dollar, I can only speculate. That euro challenge has to be eliminated from the game. The next target will bw Spain. If they can crack Spain, then they will move on to Italy – and then it will really escalate into a colossal mess for the euro as an alternative to the dollar.

Stefan Jovanovich writes:

The numbers for U.S. energy consumption suggests that the U.S. might only need to put one knee on the ground. 37 years ago, with 214 million people, the country consumed 6,453,000 Barrels per day of Gasoline and 2,552,000 Barrels per day of Diesel Fuel. The most recent numbers have consumption of Gasoline at 8,779,000 Barrels per day and Diesel at 4,099,000 Barrels per day for a population 50% larger.

Dylan Distasio writes:

I found your original link very interesting, and hearkening back to the 70s energy shock, I would not put anything past Henry Kissinger, but I don't know what to make of Engdahl's theories, quoted above. The conspiracy nut in me finds them appealing, and after what we've seen happen over the last few years of the "financial crisis," nothing would surprise me.

That said, and this may simply reflect my naivete, but I don't believe the oil market can be easily manipulated long term. I'm sure speculators help trends in motion stay in motion until the positive feedback loop breaks down and the music stops, but I am skeptical of his beliefs that this is a coordinated effort to bring down Europe and China.

This may be my ugly American speaking, but I think the only thing propping the Euro up is the interest rate differential between the USD and it, and the perception that the Fed will continue to allow easy money to flow while the good burghers are tightening the reigns. I don't see the underlying structural issues with the PIIGs going away anytime soon, and despite the US's fiscal mess, still believe it will end up growing faster than the Eurozone ultimately. I don't think it is going to take $150 oil to bring down the Euro.

But concerning this:

CNG has always been 40 percent cheaper then gasoline," Oldham said. "Everyone fears that gas will hit between $4 and $5 a gallon, while CNG is expected to remain steady.

I guess Mr. Oldham, in that article, has not heard of the concept of supply and demand. Granted, the shale finds have changed the face of domestic NG supply, but if the demand were to change radically for NG, the price is going to go up significantly. There is still the issue of the cost of building out a national infrastructure as mentioned also.

I'm not arguing CNG is a bad idea, just that it is foolish to assume prices are not going to move towards a new equilibrium compared to oil if we start to get power plants converting over to NG on a widespread basis combined with this hypothetical fleet of CNG vehicles on the road.

Paolo Pezzutti writes:

The issue is about using energy as a strategic weapon to win currency "wars" and much more… Does it make sense or is it a delirium of pseudo opinionists or worse "conspirationists" at any cost?

Ken Drees adds:

"The conspiracy nut in me finds them appealing, and after what we've seen happen over the last few years of the "financial crisis," nothing would surprise me."

Do we all have a little conspiracy flake inside, the need to believe an extreme idea, the need to see one more card and maybe hit that straight, the need to go short against the trend, the need to date that "troubled yet sexy person", the need to get some action to offset the boredom of accepted reality, accepted principles, the correct fold of the hand, the trend is your friend continuation trade or the usual date or evening at home?

Our gambling flake needs to be rewired into a creative outlet that excites the spirit yet reshapes risky behavior into worthwhile enterprise. risky activity is rooted in ego and power–that force needs to be applied in a new direction instead of being repressed.

Mar

25

Sick? Go to a Vet, from Bo Keely

March 25, 2011 | 2 Comments

If I seem out of place in strange diagnoses with odd treatments of human ailments, it's only because people aren't accustomed to a veterinarian addressing human medicine. Vets take the same courses as medical students but have a long edge in seeing more patients. How many more? About 30x.

If I seem out of place in strange diagnoses with odd treatments of human ailments, it's only because people aren't accustomed to a veterinarian addressing human medicine. Vets take the same courses as medical students but have a long edge in seeing more patients. How many more? About 30x.

We walk lines of kennels and circle pastures while a physician is limited to his practice and hospitals. Vets take a holistic approach to treatment that should be applied to human medicine, accounting for the weather to what kind of scraps farmer John's wife throws to the pigs. We diagnose by gaze and touch more than by dialogue and lab tests. Vets are not specialists, and have been trained in the anatomy, diagnosis and treatment of four species: dog, cat, cow and horse. Finally, the two vets I worked for treated their own kids, from stitches to prescriptions in their clinic. There are masterful human physicians, but if I had kids who got sick, I would tell them to first go to a veterinarian and get a second opinion from a physician.

Rip McKenzie writes:

I tell others, doctors deal with one species that can talk. Vets deal with multiple species that can't.

Mar

24

The Oracle in India, from Dan Grossman

March 24, 2011 | 2 Comments

I see the Chair is too busy with market extremes (and doubtless the Knicks' loss) to comment on the Oracle in India.

Sort of seems like a last hurrah, Netjetting to all the large, third-world countries in which he's never had the pleasure of personal acclaim before he finishes his Cokes.

Mar

24

One Raises the Razor Blade, from Victor Niederhoffer

March 24, 2011 | 2 Comments

One raises the razor blade and puts some lather on the face and checks the prices at 7am and notes many markets near local extremes including stocks, fixed income, oil and the beard is still there, as well as the shaving cream.

Mar

24

Briefly Speaking, from Victor Niederhoffer

March 24, 2011 | 2 Comments

I used to love to play an opponent who couldn't win because he was trying to do something that would definitely lose. Like setting his feet leaning towards the left and hitting to right, or hitting me a drop shot when I was always fast enough to return it regardless of where it went. The Knicks are like that. They can't possibly win regardless of what they do, or how good the players are, because their system is bad. The 7 seconds shoot doesn't work. It's not percentage play.

I used to love to play an opponent who couldn't win because he was trying to do something that would definitely lose. Like setting his feet leaning towards the left and hitting to right, or hitting me a drop shot when I was always fast enough to return it regardless of where it went. The Knicks are like that. They can't possibly win regardless of what they do, or how good the players are, because their system is bad. The 7 seconds shoot doesn't work. It's not percentage play.

Fortunately some others seem to realize it now and the coach says "with all the problems I have, I am not going to comment on others problems". Hopefully he realizes it's his problem not the players.

It reminds one of my friend Joe Yuhas, the Christmas tree guy, who tapped out on a silver trade, from the long side below $ 4 and I said, "you shouldn't have been so big" and he said "but I keep thinking what would have happened if I had been short. I could have made as much as I lost" and I said, "but Joe, it didn't matter whichever way you went, you would have lost either way".

Many systems that people use for markets are like that. And those who day trade and give an implicit vig of a few 100% a year, are in similar positions in the main. They play against people whose costs are 1/10 of theirs, capital 1000 times as great, (and they can borrow from a fairy godmother at 0 % also ), and who have much better equipment and speed. And if all those advantages fail, they can force one out at the close, only to move back to where the profit would have been realized at the next open. And yet, the game must continue.

There is hope if D'Antoni trades places with the fake doc as I asked the sullen Patrick Ewing to do who would consign the Knicks to eternal crossings of the river Styx if he were to get back. There is hope for day traders if they go stay overnight.

Jay Pasch writes:

Words of wisdom on the treachery of daytrade margin as the rope seller is glad to offer plenty of product with which to fashion one's own noose…

Kim Zussman comments:

Don't think it's all the broker's fault. Blame EMH. E.g, if all the rational, logical, comfortable, patternistic things are bid every tick, the only things left are irrational, illogical, uncomfortable, and non-patterned. The only people who thrive like that are successful traders and schizophrenics.

Mar

24

The day-to-day changes in SPY (SP500) and TLT (20+yr Treasury ETF) was checked every 20 days (non-overlapping) for correlation. The attached plots correlation every 20D over time, 2002-present.

There is considerable variation, and two apparent regimes:

~7/03-6/07 with correlation varying around zero 6/07-present, with correlation bobbing around -0.5.

Is a high stock/bond risk dichotomy healthier?

Mar

24

The Art of Raquetball, from Bo Keely

March 24, 2011 | Leave a Comment

Here is the website of Ruben Gonzalez, a great painter of racquetball.

Mar

24

Anne Hathaway and Berkshire Hathaway, from Sushil Kedia

March 24, 2011 | Leave a Comment

There was an interesting story recently about how actress Anne Hathaway impacts the share price of the Sage's firm. I wonder if someone created a fund called the B3rks#ire Black Swan fund and hired a capable Search Engine Optimisation specialist then what would happen?

There was an interesting story recently about how actress Anne Hathaway impacts the share price of the Sage's firm. I wonder if someone created a fund called the B3rks#ire Black Swan fund and hired a capable Search Engine Optimisation specialist then what would happen?

The stock price of the firm will be in permanent declines or robotic trading firms will get shocked again and again?

Mar

24

Timing the Carry Trade, from Tim Hesselsweet

March 24, 2011 | 2 Comments

I'm starting to look for systematic ways to play currencies. The most apparent one is the carry trade based on relative interest rates. I'm also going to look at relative real interest rates, relative gdp, income, balance of payments, and money supply.

First pass: literature suggests carry trade is volatility dependent. Looking at PowerShares DB G10 Currency Harvest fund (DBV) which buys the 3 highest yielding currencies in g10 and shorts the 3 weakest, is down 6% since inception on 9/18/06. Indicator: compute 21-day standard deviation of close-close[1] changes and then rank today's reading over the last 90-days.

Buy DBV when the indicator is in the bottom 1/3 of the range and sell when it exits the bottom 1/3 (vol is low)

Total Return 32%

Avg 1.1%

Count 29

Std 3.0%

t 2.0

Sell short when the indicator is in the top 1/3 of the range and buy to cover when it exits the top 1/3 (vol is high)

Total Return 21%

Avg 1.2%

Count 17

Std 6.2%

t 0.8

Seems to work symmetrically although this crude strategy appears better at capturing the positive risk premia of the carry trade.

Mar

22

How to Play Innovation and Booms, from Allen Gillespie

March 22, 2011 | 2 Comments

I conducted a study on this [what would the return on buying one share of every internet related company have been for various beginning and end periods] during 1999 when we were trying to measure the opportunity costs for not participating in investing in internet stocks. I have also used some papers that appeared in the various CFA Journals about the steam engine where it was 13 years between development and commercialization and one on the value to 3 or 4th generation adopters or implementers of new technology. The Nifty 50, etc. The biotechs in my study earned the equivalent of t-note return but with obviously higher volatility for 7 years, then surpassed it. The upside was, however, if you invested after the bust or even waited until the first signs of profitability returns were between 45% and 20% per annum respectfully. My conclusions were successfully to buy Google on its first day of trading and are behind my thoughts how to play china, solar, and cloud computing now.

I conducted a study on this [what would the return on buying one share of every internet related company have been for various beginning and end periods] during 1999 when we were trying to measure the opportunity costs for not participating in investing in internet stocks. I have also used some papers that appeared in the various CFA Journals about the steam engine where it was 13 years between development and commercialization and one on the value to 3 or 4th generation adopters or implementers of new technology. The Nifty 50, etc. The biotechs in my study earned the equivalent of t-note return but with obviously higher volatility for 7 years, then surpassed it. The upside was, however, if you invested after the bust or even waited until the first signs of profitability returns were between 45% and 20% per annum respectfully. My conclusions were successfully to buy Google on its first day of trading and are behind my thoughts how to play china, solar, and cloud computing now.

1) In the mania - long/short (go long profitable ventures and short the unprofitable ones) - but in a more paired fashion (you need the industry and sector and multiple hedges– mismatched books can get difficult (i.e. the MSFT v. cloud issue now). The market when it achieves good clarity will price things on par with "risk free" investments, however, the unprofitable will always collapse at a faster rate than the profitable even within the bubble space. The best thought on this was from John Griffin who suggested shorting those brought public by second tier underwriters. He's logic - if even Goldman, Morgan, Merrill won't IPO it how bad is it. He found 30 internet stocks brought public by Whale Securities.

2) During the bust - redouble positions on profitable names - and pile in on 3 and 4 generation situations. i.e. Google was not the first search engine. AMZN has surpassed its highs just like AMGN and BIIIB of the prior study. EBAY is on the move again. QCOM - the biggest mover of 1999 has moved past its old highs.

3) Develop comps (for Google, we assumed the internet was as important at the PC, so we took Google's EPS divided into MSFT's EPS but assumed a 3x growth rate - on par for ho the PC industry developed). In the case of a NFLX, GOOG, SNDK, etc. look for what existing industry can be cannibalized for valuation purposes. GOOG was about TV ad revenue, NFLX put blockbuster under, and SNDK and the digital camera ate EK. The two way pair test on this would be a company on the Altman Z-Score test like Blockbuster or EK with its opposite on the sales and earnings growth momentum screens.

Current thoughts along these lines - if the Chinese are already the largest player in the physical markets (oil, copper, etc) and they are the mercantilist they seem to be (i.e. BIDU v. GOOG) then won't their financial markets ultimately be the same? If so, they what companies - probably not the ones listed now - who built the interstate? but who has a store on every exist?

SOLAR and alt energies rest on subsidies but if the productivity gains are real there is a cross over but there will be a bust - with only the ones getting to legitimacy surviving.

Cloud computing– another fine area

4) Spin-Offs & cross holding- follow smart company monetization strategies (i.e the Barnes & Noble v. B&N.com effect). Today see LVS, MGM, WYNN, on their Macau holdings. PM v. MO. It is a trend that should be concerning to the country. The companies are showing there is no growth here, so you spin the domestic and load it with debt (aka MO) and price the other for growth. In solar, CY, etc.

Mar

22

Parasites, Edges, and Trading Success, from Craig Mee

March 22, 2011 | Leave a Comment

You think you don't have an edge in the market, well, if you don't have this you may just have one…… Toxoplasmosis: