Oct

31

Do Stocks Fall Faster than They Rise? from Jon Goodman

October 31, 2008 | 11 Comments

In the lengthy thread regarding "whether markets decline faster than they rise," I did not see any mention of the put/call skew in S&P. It's well documented that, at least since 1987, during most "normal" periods, out-of-the-money puts are rather more expensive than out-of-the-money calls. There are several ways to explain this phenomenon:

In the lengthy thread regarding "whether markets decline faster than they rise," I did not see any mention of the put/call skew in S&P. It's well documented that, at least since 1987, during most "normal" periods, out-of-the-money puts are rather more expensive than out-of-the-money calls. There are several ways to explain this phenomenon:

1) Markets fall faster than they rise — and options traders know this. Otherwise, arbitraging this difference would be a meal for a lifetime.

2) Market participants perhaps anticipate that the realized volatility during a bear market is greater than a bull market. However, the problem with this analysis is one might expect to see an upward sloping volatility yield curve in out-of-the-money puts (during bull markets), and yet that does not usually occur based on my tests. Conversely, right now have a downward sloping yield curve in out of the money calls — which confirms the hypothesis that market participants anticipate slower price rises in the future. [Note to quants: I am not confusing delta, gamma and vega. I'm using options to predict terminal price at expiration.]

3) For most humans, fear of loss is a stronger emotion/motivator than the pleasure of gain (greed). This is well documented in the psychology and behavioral finance literature. Hence, ceterus paribus, capital market participants (who have a net long position) will, as a group, pull their rip cord faster — to flee from risk — than they will embrace the possibility of profit.

4) Lastly, my tests show that, in certain commodities, the exact opposite behavior to S&P occurs. For example, and perhaps due to the inelasticity of demand for grains, more-often-than-not one sees a call/put skew on the call side. Every so often, after a quiet "normal" period, one does indeed find an upward acceleration in price change correctly predicted by the put/call skew. Once suppy/demand is normalized, the (inevitable) ensuing bear market is much slower. These are generalizations of course, but I've found them to be true over the years. Bottom line: Market participants anticipate that stocks do indeed decline faster than they rise. The options market is priced for this outcome. And if it were not true, you could arbitrage the put/call skew.

Oct

31

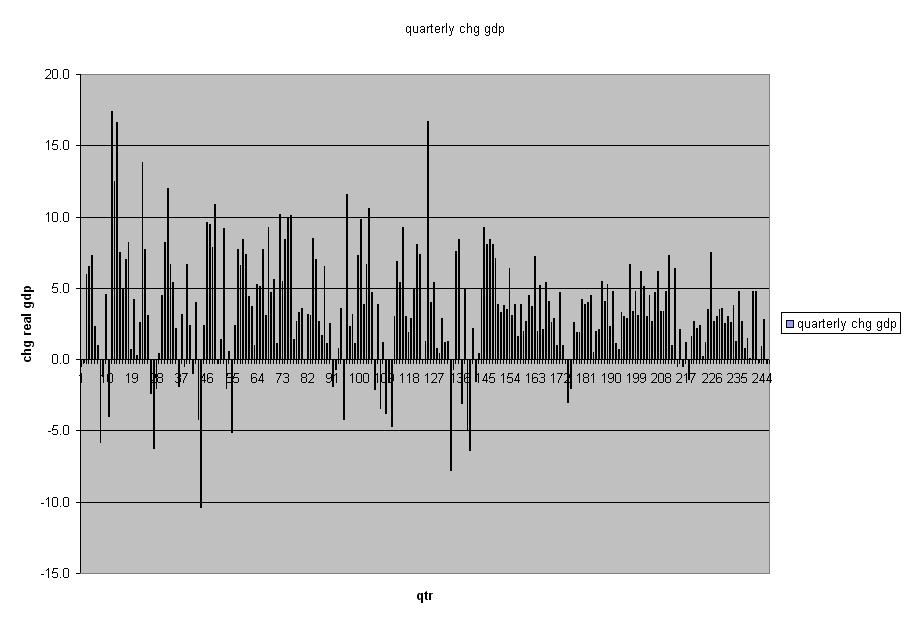

Moderation in GDP Volatility, from Kim Zussman

October 31, 2008 | 1 Comment

(This is in the literature, but wanted to check it).

Using quarterly-change in (%, 2000 dollar adjusted) GDP, checked stdev

every 16 quarters starting back from Q3 2008, to 1952:

Date 16Q stdev

2008q3 1.75

2004q3 2.02

2000q3 2.05

1996q3 1.80

1992q3 2.36

1988q3 1.57

1984q3 5.21

1980q3 5.19

1976q3 4.70

1972q3 4.13

1968q3 3.48

1964q3 3.50

1960q3 5.87

1956q3 5.47

1952q3 6.65

Noticeable reduction in volatility since the late 1980s, dating with the Greenspan tenure. The attached chart shows the source data, which suggests we have been in much more stable economy in the recent 20 years.

{kind=link}

Looking at the quarterly GDP data, checked for the pattern "UDX" (up qtr, down qtr, next=X). Found that 30% of X were negative (2 consecutive down GDP qtr), whereas in the whole series (1947-present) down quarters were 15%. And the means of X and all qtr were not significantly different (test not shown).

Also checked DJIA quarterly returns with respect to QTR GDP changes. Here is test of mean quarterly returns for DJIA for all qtr of the series (DOW QTR), simultaneous with down GDP QTR (DOW SQ), and those qtr following down GDP QTR (DOW NQ):

One-Sample T: DOW QTR, DOW SQ, DOW NQ

Test of mu = 0 vs not = 0

Variable N Mean StDev SE Mean 95% CI T P

DOW QTR 243 0.0197 0.0737 0.0047 ( 0.0104, 0.0290) 4.17 0.000

DOW SQ 35 0.0155 0.0858 0.0145 (-0.0139, 0.0450) 1.07 0.292

DOW NQ 34 0.0262 0.0893 0.0153 (-0.0049, 0.0574) 1.71 0.096

Stocks average up during down GDP QTR, and interestingly up even more the following QTRs.

Oct

31

Jos A. Bank, from Alan Millhone

October 31, 2008 | 1 Comment

I note they are having a 50% off sale on all suits and shirts, etc. (gift cards and shoes excluded) this Saturday. So if you need a new set of 'threads' this sounds like quite a sale if you have one of their stores in your area.

I note they are having a 50% off sale on all suits and shirts, etc. (gift cards and shoes excluded) this Saturday. So if you need a new set of 'threads' this sounds like quite a sale if you have one of their stores in your area.

Jay Pasch writes:

A nice 50% off sale to go along with an -85% sale price on the stock over time, back to 12/1998 highs by the looks of things…

Oct

31

Polar Plots, from Jim Sogi

October 31, 2008 | 5 Comments

Winter surf is starting up. Surf prediction is almost as important, (to me) as stock prediction. One of the tools for surf prediction are polar plots of wind and swell direction from the offshore buoys. A few years back Chair mentioned polar coordinates and plots. These can be done in R. I thought a simple plot of the direction and angle of market price might be helpful in some models to predict. For waves, NOAA uses data from offshore data buoys and says:

Winter surf is starting up. Surf prediction is almost as important, (to me) as stock prediction. One of the tools for surf prediction are polar plots of wind and swell direction from the offshore buoys. A few years back Chair mentioned polar coordinates and plots. These can be done in R. I thought a simple plot of the direction and angle of market price might be helpful in some models to predict. For waves, NOAA uses data from offshore data buoys and says:

Spectra and source term are presented for selected output locations in the form of polar plots. The radial lines in the polar plots depict the directional resolution of the model. The concentric circles are plotted at 0.05 Hz intervals, where the innermost circle corresponds to 0.05 Hz and the outermost circle corresponds to 0.25 Hz. Wave energy plotted in the lower left quadrant travels in SW directions etc. The blue arrow in the center of the plots depicts wind speed and direction. Colors represent wave energy density for spectra and rates of change of energy density for source terms and are plotted at a logarithmic scale where the contours separating the colors increase by a factor of 2.

This application might be good for markets as a different sort of plot on the question, "Is the market going up or down, and how fast?". Surf direction and speed is critical to choose the spot, and equipment. Market direction and intensity is critical, but hard to predict. Surf travels generally from north to south in the winter. Market forces generally tend to travel East to West. Perhaps a polar plot of the prevailing market winds, and the concentrations of energy might be helpful in predicting market direction and intensity.

Jeff Watson writes:

As a serious student of surf prediction, I note and live by the seasonality of the swells. Different seasons bring swells from different directions, and Sogi-San is lucky to live in a place that gets swell from all 360 degrees, ensuring year round surf somewhere in the islands. Surf prediction is easy at my location as we have roughly two primary causes of swell; Cold fronts and hurricanes. We only have a window of roughly 90 degrees where conditions will produce rideable waves I check our weather maps daily and look at all the buoy information from the NOAA, whether it's surf season or not. From my location it is pretty easy to predict when we will get swells, although predicting the size gets rather tricky. To predict the size takes a lot of experience, comparisons of past data, and a firm grasp of current weather conditions…much like looking at the markets. Although it's anecdotal, I find it much easier to predict the possibility of waves than future market action.

One thing of note, sometimes mysto swells will appear out of nowhere, lasting only a very short time, with no apparent cause, disappearing as quickly as they arrive much to the chagrin of the locals. The swells that hit with no warning cause a lot of surfers to miss out on waves, because they aren't positioned to hit the swell. The markets do the same thing with movements that come out of nowhere, surprising the participants who are out of position, causing the players to be frantic while trying to catch the move which is usually missed. All of this, whether with the waves or markets, sometimes comes with no valid explanation. When I talk to groms about the waves and swell, I sometimes resort to using the cliche, "It is what it is." The same thing can be said about market moves.

Vinh Tu adds:

Mathematically, angles are even closer to correlations. Two series of t observations can be represented as two vectors in t-dimensional space. You get the cosine from dividing the dot product of the two series by the volatility of each series.

I'm not sure whether, with more than two instruments, you can still flatten it to a circle and still have it show anything useful. But restricting the plot to two series, we could take one series to be "North" –logical candidates for this might be an interest rate, or a "market portfolio", or a major market index. Then the other series could be examined in relation to North. Samples of the other series could be colour coded and assigned polar positions.

Alternatively, perhaps north could be a straight line representing a desired or hypothesized drift. The result would be somewhat related to the R-squared technical trend indicator.

Alex Castaldo quibbles:

A correlation is exactly like the cosine of an angle, as opposed to an angle. Because cosine is an even function, there is an ambiguity as to the sign of the angle. For example if Bonds represent North and Stocks are correlated 0.5 with Bonds, how should that be plotted? As +60 degrees (approx. W-N-W) or -60 degrees (approx E-N-E)?

Oct

30

Briefly Speaking, from Victor Niederhoffer

October 30, 2008 | 4 Comments

Some of the sophisticated media, including the most used ones are subtle in how they bias their news for their own man in the election. They report original studies using their own data that in the last 20 elections the market has moved better under their favored administration than in their least favored one in the first year. With 25 elections, and a starting point, and one of four years, or cumulatives to work with, and leaving out that the main reason the market is down is that the election is in the bag already, they leave it to the reader to overcome their natural aversion to favor the administration that will enable them in their platform to keep more of their after service gains.

Some of the sophisticated media, including the most used ones are subtle in how they bias their news for their own man in the election. They report original studies using their own data that in the last 20 elections the market has moved better under their favored administration than in their least favored one in the first year. With 25 elections, and a starting point, and one of four years, or cumulatives to work with, and leaving out that the main reason the market is down is that the election is in the bag already, they leave it to the reader to overcome their natural aversion to favor the administration that will enable them in their platform to keep more of their after service gains.

The attempt to propagandize using stats in an indirect way, rather subtle compared to their usual attempts to objectively debunk any claims that the other side makes against their favorite,(thereby maintaining their je na sais quoi with their founder and his votaries), elicits an important formula. The variation or standard error of a mean without replacement is considerably lower than its variation with replacement. Thus, a sample of the stats that we all use when searching for regularities in past patterns are based on replacement. The standard error withour replacement is lower than the standard error with replacement by a factor sqrt ( 1 - n/N) where n is the sample size and N the population. Thus with a sample of 10 from a population of 25 where the standard deviation is 25 %, the standard error would not be the usual 25/3 but 8 x 3/4 = 6. 25% of the area of a normal curve is within 0.7e standard dev from the mean. That means that we would expect 1/2 of all means of 10 observations from such a distribution to be greater than 4 away from the grand mean of say 10 percentage points. The average difference between the better performaing group and the worse performing group would be approximately 8 percantage points. When we look for regularities we generally don't choose just one split but 3 or 4 or 10 until we find the best one. That runs into another statistical problem relating to the average difference between succesive samples from a distribution. A short approximation for that is contained in Kendall and Stuart, but looks to be approximately equal to an average difference for a normal distribution of 2/3 of a standard deviation (one must check that). Thus if we take the best of 2 cuts of 10 from a distrition like the above, we could expect the best one to be 8 away( 4 +2/3 x 6 ) from the grand mean a full 80% more than the grand mean approximately 1/2 of the time. This explains why so many of the regularities discovered with many different qualifiers, if's and or buts, stops et al are purely artifices of randomness rather than propaganda as above. It also explains why such programs as artificial interaction detector and cart often give such spurious results. The whole subject cries out the artful simulater.

Steve Ellison replies:

The Political Economist studied this last month:

I've run the numbers myself. Superficially at least, the Democratic claims are true: Since 1948, the Standard & Poor's 500 total return (capital gains plus dividends) has averaged 15.6% when a Democrat was in the White House and only 11.1% when a Republican was in the White House.

You get a similar result if you look at growth in real gross domestic product. Under Democratic presidents, the average since 1948 has been 4.2%. Under Republican presidents it has been only 2.8%.

But it's not so simple when you study that 'study.' … While stocks could be expected to react very quickly to changes and expectations of changes in the political environment, the whole economy doesn't just turn on a dime. So when we compare real GDP growth under Democratic and Republican presidents, maybe we should lag the results by a couple years. That is, we'll assume that the growth in a given year was the result of the president's policies from two years ago.

When we do that … we find that the economy performed pretty much exactly the same regardless of the president's party: 3.5% under Democrats and 3.4% under Republicans.

But then who ever said that the president alone determines the economy or the stock market? It's Congress that makes the laws. The president just signs them. Based on congressional control, the study results look very different. Under Republican Congresses, stocks have averaged a 19% return, while under Democratic Congresses only 11.9%. Real GDP growth, lagged two years, has averaged 3.7% under Republican Congresses, and only 3.2% under Democratic ones.

Oct

30

Volatility and the Yen, from Riz Din

October 30, 2008 | 5 Comments

I was just perusing a "Hedge Fund Monitor (27 Oct)" note from Merrill. It cites Trimtabs research reporting record high hedge fund redemptions in September of $43bn, and says:

Such forced selling drive asset prices lower which in turn creates more losses for HFs and lead to more selling- a vicious circle. …We also think that losses to large prime brokers who provide funding to HFs, may have exacerbated some of the forced selling. While HF returns over the past 12 months are negatively correlated to Financials overall they are positively correlated with investment banks, who are also prime brokers to HFs. Just as HFs' cash needs were rising, funding became more difficult.

The note goes on to comment that a popular hedge fund strategy was to invest in equities with cheap yen and points to the strong correlation between USD/JPY and the S&P, giving us yet another variant of the carry trade.

In this narrative, the move in the USD/JPY is less a result of new flows into yen than it is a consequence of severe hedge fund liquidations that have forced an aggressive unwinding of the equity-yen trade. For what it's worth, the ML note looks to the latest COT data (already stale as it reports positions as of last Tuesday's close) and finds crowded net long speculative positions in USD and JPY, suggesting USD/JPY may have further to go on the downside. It's all interesting reading, and almost everyone seems to agree that these violent moves are the result of forced hands, not of a fair reassessment of fundamentals. A good time for the long-term investor to scale in to global equity markets, perhaps. The other thought I had when reading this report is that while I have been expecting a massive rally in USD/JPY when risk appetite subsides, if the USD and other currencies also have super low interest rates by that time, then the yen could have some competition on its hands as the funding currency of choice.

Phil McDonnell writes:

In recent days the yen has been incredibly strong. The other notable feature of recent trading is that volatility has been historically high. Since 9/11 this year there have been 30 trading days. Only four of those have shown less than a 1% move in either direction. High change days are the norm, not the exception these days. VIX has been rising and made repeated new highs and still resides at high levels.

To see if there is a relationship between these it is often good to look at correlations between coterminous changes. Some of the more notable coincident correlations over the last three months are:

VIX Yen 71%

VIX TBill 68%

Yen TBill 59%

All these relationships are substantial. From these we can conclude that when investors perceive increased risk the money flees to both tbills and yen.

Dr. McDonnell is the author of Optimal Portfolio Modeling, Wiley, 2008

Riz Din adds:

A couple of additional thoughts on the carry trade:

1. One can imagine another reason why the market has fed off itself on the downside is that the carry trade is itself entwined with volatility. The carry trade thrives in a low volatility environment and it is not so long ago that we were experiencing what some called the Great Moderation, an apparently new era of low volatility in the real and financial economy. In such a world where investors are confident that fx rates will lie somewhere within a tight range x months hence, the attractiveness of the interest rate component of low rate currencies grew massively, and the yen and other low rate currencies became cheap financing vehicles for other investments. Alas, to benefit from these low financing rates these investments would have had to have been unhedged for fx risk, and when volatility spiked up, the perceived cushion of saving provided by the lower interest rates paled in comparison to the daily swings in the fx prices. Add this factor to margin calls, margin calls, redemptions, etc and you have another powerful reason for the recent aggressive, self-perpetuating, forced selling that took place across the markets. Always thinking from the other side, after such a large reversal and cleaning out of carry traders, I wonder if there will be opportunities to put this trade on as volatility heads lower– history could be a guide for those who have access to the data. I hear Iceland is offering 18%.

2. I must be missing something obvious here, and maybe this thought can be easily skewered, but I wonder if this simple explanation can be used to show why the carry trade seems to defy economic theory (uncovered interest rate parity) over prolonged periods, only to eventually come crashing down: If two similar bonds or similar stocks are trading massively apart for no reason, immediate buying of one and selling of the other closes the price gap. The price corrects back very quickly and the opportunity disappears in the blink of a eye (Porsche/VW aside). However, entering in to the fx carry trade by selling the low yielding currency and buying the high yielding currency surely only pulls prices further apart, making the carry trade even more attractive to those who use history as a guide. Is this a self-perpetuating cycle that simply carries prices to unsustainable levels?

Alston Mabry replies:

Can't help but think that it has been the other way around: The carry trade and other cheap money forces were what kept volatility low. The image that comes to mind is the pressure of air inside a big balloon, or water inside a sprinkler system; when the pressure is constant, the system is smooth and stable, but when the pressure slacks off, the system sputters and collapses.

Oct

30

Internet Radio, from Kim Zussman

October 30, 2008 | 2 Comments

There are a number of free internet radio stations, and in honor of the pending savage bear market rally, here is a good site.

There are a number of free internet radio stations, and in honor of the pending savage bear market rally, here is a good site.

I like the Bartok station from Hungary, and of course Zappateers which is on now (that man died too young).

But since this is a trading list, certainly you have read, "Trader know thyself". Which I think means that when you are intimately involved with the market it is difficult to disentangle your interpretations from unbiased signals, because you kind of merge with it. As if it is about you.

Last week while sitting in the kitchen with a mug of Costco coffee (Jose brand), a hapless bird struck the nearby bay window with a loud thud. I went out and found that she had banked off the glass into a waste bin; not dead but disoriented and bleeding. I picked her up –it looked like she could make it, so I set her on the lawn to recuperate.

Half hour later she had flown; but suspecting not far, I put out some bread crumbs and filled the bird-bath. Almost immediately she flitted from a tree into the bath, sipped it, and looked at me in appreciation. It felt good to bridge across inter-species bigotries (I eat her cousins), and being recognized by her felt like how Adam must have before he got poisoned.

When we came back later that night she was perched incautiously on our porch looking quizzically at her savior, and it was hard to resist thoughts of Cult Cargo Science and that she might now worship me.

The next morning I found her dead there. Clinically, probably internal bleeding, shock, and cardiac arrest. But at least someone was nice to her in her last day.

The next day I saw another bird like her; a kind of "tit".

If you read the description, when you have seen one tit, you have seen them all (which in all species never derails the inquisition). And over the next few days I noticed there were many, and it occurred to me that the bird which hit the window may not have been the one who came to the bath. And it also may not have been the one that was stooped on the patio, and maybe even a different one had died. Maybe this "one bird" was all a self-constructed story, originating at the center of the universe, like the one running in every one of us.

All of which perhaps argues for another conservation law: The more you strive to know yourself, the more self-obsessed you become, and the less accurately you can visualize your unique irrelevance.

Oct

30

Colors in Nature, from Riz Din

October 30, 2008 | Leave a Comment

Harvard Magazine leads with an interesting look at the multiple uses of colour in nature. The article is promoting a new 'Language of Color' exhibition at the Harvard Museum of Natural History and is well worth reading for a broader appreciation of the various whys and hows of colour as a signalling mechanism in nature, with colours featuring as part of the evolutionary predator-prey arms race, and reminders that because humans are not the intended observers of most colour displays, the intended viewer often sees something different to the human eye. Also contains some great pictures. This stuff never ceases to amaze.

Harvard Magazine leads with an interesting look at the multiple uses of colour in nature. The article is promoting a new 'Language of Color' exhibition at the Harvard Museum of Natural History and is well worth reading for a broader appreciation of the various whys and hows of colour as a signalling mechanism in nature, with colours featuring as part of the evolutionary predator-prey arms race, and reminders that because humans are not the intended observers of most colour displays, the intended viewer often sees something different to the human eye. Also contains some great pictures. This stuff never ceases to amaze.

Quote: "One sex story fit for the tabloids concerns wrasses and parrotfish. In many species, the females in a group are much less colorful than the dominant male. If the male gets eaten, the dominant female changes her sex—and puts on those brilliant colors." Source.

Oct

29

Notes, from Steve Leslie

October 29, 2008 | 20 Comments

I know to many this is very basic commentary but it may prove helpful to some here: This explains in one paragraph why things go down a lot faster than they go up. Hedgefunds, mutual funds and pension funds must sell on the way down. They have no choice. They must meet margin requirements and other technical requirements. This forced liquidation scenario is the most wicked of wickeds that the unfortunate fundamental investor faces in their education.

Remember near the end of the movie Trading Places where the Duke brothers (Ralph Bellamy and Don Ameche) are approached by the exchange with their margin calls. Their comment was “we don’t have that kind of money!” Same thing there as here. This is the cataclysm when people trade with OPM (other people's money). They are universally more cavalier and reckless than if they have their own capital at risk. LTCM in 1998 suffered the same fate when they had a famous decoupling of their spreads. Their models, suddenly and evidently without warning, [stopped working; the firm faced margin calls and] had to liquidate. Then, the Investment Banks and Commercial banks came to the rescue because they saw ultimate value in the spreads. Otherwise they would have not gotten involved and the Fed would have had to step in and take over the company. At the time, they controlled over a trillion dollars of assets on their books. Whereas with an intangible to go up in price it takes many months to build up a position and to trade ahead of the fundamental estimates.

This scenario is very well described by Dr. Hersh Shefrin in his book Beyond Greed and Fear: Understanding Behavioral Finance. He eloquently describes how it takes a fundamental analyst approximately nine months for their estimates to catch up with a stock price. What we see today especially with the stock market is pure technical trading. It has everything to do with liquidity needs in an environment where credit is non-existent. Until this picture becomes clearer when Investment Banks and Commercial Banks will give up their new found capital and help companies thaw out from this very arctic deep freeze credit crisis, we shall continue to trade in a black hole of confusion. I actually heard a “professional” comment, “It has been three weeks since the Federal Reserve and the Treasury put forth their solutions. How long do you think it will take for these things to start to work?” Summary: It took years for us to get into this mess, we are not going to get out of this one overnight.

Oct

29

The Bronte Blogger, from Riz Din

October 29, 2008 | 1 Comment

The Bronte Capital blogger finds fascinating similarities between the Porsche/VW affair and the Stutz Motor Car Company debacle in 1920, when major shareholder Alan Aloysius Ryan defended Stutz against short sellers and ended up owning 105% of the company. This put him in the enviable position of being able to to name a price, but it all ended in ruin for both Ryan and Stutz.

(For history buffs, the blog links to archived articles in the New York Times).

Oct

28

Some Keys to the Biggest Rally Ever, from Victor Niederhoffer

October 28, 2008 | 10 Comments

2008 1997

Date S&P close S&P close

10/23 915 1309

10/24 866 1297

10/27 835 1227

10/28 939 1278

10/29 1278

1. The Nikkei broke through 7000 at 22:30 GMT, a 26 year low, but closed up 6% at 7621. The last 10 day max in the S&P was Aug 11, a lapse so far of 55 trading days, the longest dry spell in history. Dax was up 10 % at 10:00 GMT today while the S&P was up 2%.

2. 99% of financial news articles have been bearish. Oat futures at a 6 year low at 219 showing horse power is still a bargain for what must be the most basic, and, one believes, the purest agricultural commodity to be. These prices are typical for all other commodities.

3. The odds for the incumbent party in the Presidential race which have almost gone off the board at 1 in 10 are so low that there is no need for the teetotum that Nock described to keep the Dow down any further. And most important of all, with the market down 30 yesterday, normally good for a VIX rise of 8 these days, it was only up 1.

4. What else?

Oct

27

21, from Steve Ellison

October 27, 2008 | 2 Comments

I enjoyed the movie "21" about students at my alma mater counting cards at blackjack. The main character, Ben Campbell (loosely based on the real-life Jeffrey Ma), catches the attention of his math professor by correctly answering the question that has been discussed on this site about whether it would be advantageous to change one's door selection in "Let's Make a Deal" after being shown what is behind one of the other doors.

I enjoyed the movie "21" about students at my alma mater counting cards at blackjack. The main character, Ben Campbell (loosely based on the real-life Jeffrey Ma), catches the attention of his math professor by correctly answering the question that has been discussed on this site about whether it would be advantageous to change one's door selection in "Let's Make a Deal" after being shown what is behind one of the other doors.

The movie has many applications to speculation. The professor recruits Ben for the blackjack team because he believes that Ben will make decisions based on statistics, not emotions. Ben is reluctant to join, but is desperately short of funds for medical school. He decides to join, but only for long enough to earn the money he needs.

The professor tests Ben by having two men suddenly throw a pillowcase over Ben's head in the midst of a game at a Boston Chinatown gambling den. The men drag him into a back room. As Ben protests, "Let me go! I haven't done anything!", the men demand, "What is the count?". Ben answers, correctly, "Plus 17". The men remove the pillowcase, and Ben sees his professor, who says he had to test whether Ben would remember the count even under great stress.

Later, the professor says, "Remember, Ben, this is a business. It is not gambling. In the excitement it can be easy to lose your head. You will not do that."

To avoid detection by casino managers determined to prevent card counting, the team uses elaborate methods of deception. All the players have assumed names and fake IDs. One team member plays, betting only the minimum. When the count becomes highly favorable, this drone player uses a gesture to signal the big player, Ben, to come to the table and place large bets. The teammates act as if they do not know one another, but the drone makes a casual comment to the dealer containing a code word to convey the count to the big player.

As Ben consistently wins, he becomes hooked on the game and keeps playing even after he has enough money for medical school. He betrays his friends, fights with a teammate, and finally lets his emotions get the best of him at the blackjack table, losing $200,000 in a night. Meanwhile, a casino enforcer determines that Ben is a counter. It all makes for a thrilling climax.

Charles Pennington writes:

They made a few hundred thousand dollars in Vegas, and that's a story worthy of a $35 million dollar film that grossed $150 million? They made real money snowing the public, not the casino.

Chris Cooper says:

Prof. Pennington is, of course correct. It is worth mentioning that casino gaming has served as a springboard into trading and speculation for many, who have become much more successful in that arena than they ever could have been in the casinos. Ed Thorp is the legendary example, but there have been many others. My gaming experiences certainly inspired me, many years ago, to return to school so I could learn the math (control systems, signal processing) I thought I would need for trading. Also there was the "Eudaemonic Pie" team. Blair Hull is another instance.

Trying to make a living via casino gaming teaches you many lessons which are directly applicable, even essential, to effective speculation.

John Floyd observes:

There is a lot to be learned from casino games, much of it applies to trading. In particular, deciding when you have a positive expected return, varying bet size, risk of ruin, etc. Not to mention that one should study the games, as is true in financial markets, and develop an understanding before putting serious capital at risk.

There is a lot to be learned from casino games, much of it applies to trading. In particular, deciding when you have a positive expected return, varying bet size, risk of ruin, etc. Not to mention that one should study the games, as is true in financial markets, and develop an understanding before putting serious capital at risk.

Many of the games offer one the ability to get a statistical edge on the house such as blackjack and some of the progressive poker machines. The problem is that any success is usually found quickly by the house. The house then takes methods to decrease your odds such as reshuffling often in blackjack and then asking you to not play anymore at their fine establishment.

A player therefore needs to take several steps to camouflage what they are doing, such as: spreading bets across several hands, decreasing bet size, not varying bet size too much, making some "dumb" bets to throw them off the scent, moving around casinos and tables when necessary, playing odd hours, wearing hats, etc. The casino runs like a machine and grinds out the vig. The pit boss is evaluated on a per hour basis of what he takes in, a hit of a few thousand dollars draws his and the house's attention very quickly.

While the challenge is fun for some time it can get tedious. Furthermore, the return on an hourly basis even if one is a good player pales in comparison to successful trading in the financial markets.

Oct

26

Picking Coffee, from Jim Sogi

October 26, 2008 | 4 Comments

It's coffee picking season again [here in Hawaii] and the coffee cherry beans are turning red. I hate picking coffee and have just enough trees to call myself a gentleman farmer (emphases on the former). The process starts with waiting for the rows of beans on the tree branches to turn red and pick only the red ones, not the green ones. I pick just enough to drink so go for the quality over quantity, and pick the best and easiest to pick beans. So in my humble opinion my coffee is the best coffee I have ever drunk. The commercial pickers who are paid by the pound include many green and unripe beans to add weight, but not taste or quality. It's easy to see how incentives shape behaviors. What are the incentives are for mortgage holders who have a moratorium on foreclosures, or the incentives to banks who can sell their mortgages to the fed for 90% rather than move them now for 60%.

It's coffee picking season again [here in Hawaii] and the coffee cherry beans are turning red. I hate picking coffee and have just enough trees to call myself a gentleman farmer (emphases on the former). The process starts with waiting for the rows of beans on the tree branches to turn red and pick only the red ones, not the green ones. I pick just enough to drink so go for the quality over quantity, and pick the best and easiest to pick beans. So in my humble opinion my coffee is the best coffee I have ever drunk. The commercial pickers who are paid by the pound include many green and unripe beans to add weight, but not taste or quality. It's easy to see how incentives shape behaviors. What are the incentives are for mortgage holders who have a moratorium on foreclosures, or the incentives to banks who can sell their mortgages to the fed for 90% rather than move them now for 60%.

After the beans are picked, they are run through a pulper, an industrial device made of cast iron in England from a design from the Industrial Revolution. Mine had a hand crank, but a friend in the neighborhood to whom I lent it to pulp his coffee added a small motor bringing it squarely into the modern age. The pulper takes off the fleshing fruit leaving a seed in a wrapper. This is soaked overnight, then dried in the sun to 14% moisture. This is called parchment. Most of the value in the operation is in this simple processing and provides a much higher return than the farmer or picker receives. The sun drying is the key to the flavor. Most commercial coffee is dried in heated machines. This takes away the mellow soft palate to the coffee and gives a harsher bitterness that is often criticized in some Kona coffees. Be sure your gourmet coffee is sun dried. After the parchment is dried, a husker machine takes off the thin skin and leaves the green bean which is shipped to the roaster. These huskers are large and rather expensive so I go across the street where there is a coffee farm and have them do it. I strongly recommend buying just green beans, then using a small roaster such as "I Roast" to roast a weekly batch for drinking to enjoy the best flavor. As soon as the bean is roasted, the gases start to escape and with it the flavor. There is nothing like a fresh roasted cup of coffee hand picked from your own yard.

Oct

26

The Naturalness of Coincidences, from Victor Niederhoffer

October 26, 2008 | 4 Comments

Jeff Watson thoughtful post below about the relevance of George Seurat to trading inspired me to think about the many lessons about markets I learned from Sondheim's Sunday in the Park with George, and asked my assistant Linda to send him a copy of it tonight. Two hours later, as I looked through the jacket of my pink coat that I wore to my brother Roy's Halloween party, I found a playbill — Sunday in the Park with George. The 1 in 16 chance of five days' repeating each other like last Friday, makes me think of coincidences and the many times that I have had patterns with 25 of 25 correct predictions at the hand ready for use, only to find the 26th, in real life, totally wrong. The power of probabilities to make truly unlikely events when taken in isolation very probable, a variant of the birthday problem, is astonishing and if one was not a man of lack of faith, it would be eerie.

Jeff Watson thoughtful post below about the relevance of George Seurat to trading inspired me to think about the many lessons about markets I learned from Sondheim's Sunday in the Park with George, and asked my assistant Linda to send him a copy of it tonight. Two hours later, as I looked through the jacket of my pink coat that I wore to my brother Roy's Halloween party, I found a playbill — Sunday in the Park with George. The 1 in 16 chance of five days' repeating each other like last Friday, makes me think of coincidences and the many times that I have had patterns with 25 of 25 correct predictions at the hand ready for use, only to find the 26th, in real life, totally wrong. The power of probabilities to make truly unlikely events when taken in isolation very probable, a variant of the birthday problem, is astonishing and if one was not a man of lack of faith, it would be eerie.

Michael Cook writes:

This makes me think of Ramsey Theory. The classic version of Ramsey's Theorem: in any collection of six people, either three mutually know each other, or three mutually do not know each other. The philosophy behind Ramsey Theory in general is: "a sufficiently large system, no matter how random, must contain highly organized subsystems."

This is very suggestive for markets.

Steve Humbert replies:

Ramsey Theory is fascinating, but other than as an analogue I'm not sure it has any predictive power in the markets. Note that Ramsey Theory does not reveal which people know each other and which do not (a bit like Ogilvy's famous lament that half of the money spent on advertising was wasted, but that he was never sure which half), and that in its binary, know-don't know, criterion, RT doesn't tell us anything about the strength of the connections. A passing acquaintance is treated the same as a life-long friendship (the market equivalent of treating a 1-tic and a 20-tic up move (or down) as equivalent, and only concerning oneself the binary up-down distinction.

Oct

26

Some Wonderments, from Victor Niederhoffer

October 26, 2008 | 1 Comment

I wonder what nature has to teach us about how it recovers from natural disasters vis a vis the current market decline. Does the process of recovery and change after fires and floods and earthquakes and hurricanes have anything to teach? I looked at the methods of seed dispersal at the Botanical Gardens recently and it made me think again that IPOs at times like this must be priced at implicit returns of 100% a year or more. I also wonder whether there are insights from the Stockholm Syndrome here with people who are the source of the disaster being greeted with love and votes and money? How does romance come into the picture? I return to the subject of catalysts in markets. Are there some agents that are sufficient to cause big changes in markets that come ahead of everything, e.g. a big move in oil that precedes a violent move in stocks? When will asset allocators begin to compare the returns of stocks versus bonds and find that their portfolios now have gone up by 20 percentage points from before in terms of their allocation to bonds? That's too much, other things being equal, even if the expected rate of returns were not changed. I can't help but think that Alan Greenspan's confession that his belief in free markets was wrong is an example of the "Old Man Syndrome" a la Cyril Burt's wanting to have the most identical twins in his study, combined with George Zachar's "your own man said you were out." Does the average politician really believe that raising the rate of contribution to the Service will raise revenues or or is just an example of rent seeking and public choice theory at work where they look out for their own personna above all, and to what extent is the likely increase in this contribution under the now 10 to 1 favored new administration a major contributing cause to the current past meltdown? What is the cause of those fantastic moves at the close that are so ephemeral and dysfunctional to all who are not properly capitalized and money-managed? Most of all, I wonder what my mentors at the University of Chicago, Jim Lorie and George Stigler, would say about the current carnage. Would it undermine their faith in markets?

I wonder what nature has to teach us about how it recovers from natural disasters vis a vis the current market decline. Does the process of recovery and change after fires and floods and earthquakes and hurricanes have anything to teach? I looked at the methods of seed dispersal at the Botanical Gardens recently and it made me think again that IPOs at times like this must be priced at implicit returns of 100% a year or more. I also wonder whether there are insights from the Stockholm Syndrome here with people who are the source of the disaster being greeted with love and votes and money? How does romance come into the picture? I return to the subject of catalysts in markets. Are there some agents that are sufficient to cause big changes in markets that come ahead of everything, e.g. a big move in oil that precedes a violent move in stocks? When will asset allocators begin to compare the returns of stocks versus bonds and find that their portfolios now have gone up by 20 percentage points from before in terms of their allocation to bonds? That's too much, other things being equal, even if the expected rate of returns were not changed. I can't help but think that Alan Greenspan's confession that his belief in free markets was wrong is an example of the "Old Man Syndrome" a la Cyril Burt's wanting to have the most identical twins in his study, combined with George Zachar's "your own man said you were out." Does the average politician really believe that raising the rate of contribution to the Service will raise revenues or or is just an example of rent seeking and public choice theory at work where they look out for their own personna above all, and to what extent is the likely increase in this contribution under the now 10 to 1 favored new administration a major contributing cause to the current past meltdown? What is the cause of those fantastic moves at the close that are so ephemeral and dysfunctional to all who are not properly capitalized and money-managed? Most of all, I wonder what my mentors at the University of Chicago, Jim Lorie and George Stigler, would say about the current carnage. Would it undermine their faith in markets?

Sam Marx writes:

Something I noticed about market that I tried to avoid when I had traders working for me is that the market rewards and penalizes on a continuous basis, but "employed" traders and executives are usually rewarded on a yearly basis.

Dick Fuld of Lehman, Stanley O'Neil of Merrill, Frank Raines of Fannie, et. al., received yearly bonuses, so their goal was maximizing the yearly profit while neglecting the carry-forward risks. If they had to leave a large portion of their bonuses or profits in escrow, as did my traders, to be carried over from year to year, they wouldn't take excessive risks and the market would be more stable.

Alex Castaldo adds:

The study of how nature recovers from natural disasters such as forest fires or floods is called the theory of succession and was developed by one H. C. Cowles. Wouldn't it be a strange coincidence if he was related to the Alfred Cowles III who studied stock market forecasting.

Oct

26

Roubini on Bloomberg, from Paolo Pezzuti

October 26, 2008 | 4 Comments

In a recent Bloomberg interview, Roubini says that markets are dysfunctional, there are no natural buyers, markets are in a situation of deleveraging, capitulation and total panic. He says to stay away from the US dollar, which appreciated too much. Stock prices will plunge another 20-30%. Relative economic, political, geostrategic power of the US over time will be eroded and reduced. It is likely we will experience a L shaped recession with long term economic stagnation. Not really an optimistic view I must say. Sen. Obama has a clearer idea of how to solve the crisis. He said a laissez-faire approach at this time cannot work. I was skeptical when I heard him speak at the beginning of this year and then the economy and markets spiraled down as he predicted.

In a recent Bloomberg interview, Roubini says that markets are dysfunctional, there are no natural buyers, markets are in a situation of deleveraging, capitulation and total panic. He says to stay away from the US dollar, which appreciated too much. Stock prices will plunge another 20-30%. Relative economic, political, geostrategic power of the US over time will be eroded and reduced. It is likely we will experience a L shaped recession with long term economic stagnation. Not really an optimistic view I must say. Sen. Obama has a clearer idea of how to solve the crisis. He said a laissez-faire approach at this time cannot work. I was skeptical when I heard him speak at the beginning of this year and then the economy and markets spiraled down as he predicted.

I do not have enough information or the crystal ball to assess whether he is right or not, however, his "predictions" are quite scary. But are we really able to predict how this crisis is going to evolve? Being optimistic may sound silly at this point. The crisis is spreading to East Europe, smaller governments may default, there may be a currency crisis. The speed of this meltdown in the past weeks has been impressive. Are there any positive points? For the moment I do not see many, unless you believe that market forces will start again to price assets orderly and investors will see good value for money at these prices sooner or later. I believe, however, that we may see even a long rebound, but this crisis will have a long term effect. If you look at the charts, e.g. the Nasdaq, you can see that the bear market has actually started in 2000. The uptrend between 2002 and 2007 was only a long rebound. The long term bear trend has now resumed to print a C Elliot wave for the "secular" optimists or a wave 3 for the chronic bears.

Has the ability of creating wealth in our societies become a problem? If technology and innovation are not creating value in our economies, it may the bad sign of the shifting of geostrategic power to other powers of the world. The challenge is intellectual. We need to rethink if we want to tackle this challenge, and how our societies can re-organize and re-assess their life-style, their education, financial and industrial system.

Nigel Davies responds:

Quite a few people have predicted something like this, though they tend to differ on how it will play out. The big unknown is how we react to this crisis, for example it's a moot point about whether we should have tried to prop the thing up at all.

One very interesting feature to emerge from this is that the World's nations have come to a very sudden understanding that we're all linked economically. So hostile acts vis a vis oil, for example, end up rebounding. I wonder if this will be the great good that emerges from this crisis, an awareness of our shared predicament.

GM Davies is the author of Play 1 e4 e5: A Complete Repertoire for Black, Everyman, 2005

Oct

25

Souper Saturday, from Alan Millhone

October 25, 2008 | 1 Comment

Earlier today I was at Beechwood Presbyterian Church to help with "Souper Saturday" held the last Saturday of each month. The church opens up its kitchen and dining room and volunteers come from various churches in the area on a rotating basis to help serve those who come to dine. The tables were set for 60 and those chairs were all filled with people in the area who walk in for a monthly free meal. I also asked and found that 55 dinners were 'to go' and they ran out of food tonight or more dinners would have been packaged. As last time I helped, I worked the dessert table and it kept me busy serving cookies, cupcakes, and cutting various pies. I was in the back of the room and from my vantage point could tell that those who came were hungry and enjoyed a hot meal. A blessing was given before the meal and after that no other items of any religious nature were invoked. Those who came could come and eat and leave when they were finished. It did me good to help serve tonight and made me thankful for all I have in my life. I also noted that there were many more people tonight than the last time I helped as a volunteer.

Earlier today I was at Beechwood Presbyterian Church to help with "Souper Saturday" held the last Saturday of each month. The church opens up its kitchen and dining room and volunteers come from various churches in the area on a rotating basis to help serve those who come to dine. The tables were set for 60 and those chairs were all filled with people in the area who walk in for a monthly free meal. I also asked and found that 55 dinners were 'to go' and they ran out of food tonight or more dinners would have been packaged. As last time I helped, I worked the dessert table and it kept me busy serving cookies, cupcakes, and cutting various pies. I was in the back of the room and from my vantage point could tell that those who came were hungry and enjoyed a hot meal. A blessing was given before the meal and after that no other items of any religious nature were invoked. Those who came could come and eat and leave when they were finished. It did me good to help serve tonight and made me thankful for all I have in my life. I also noted that there were many more people tonight than the last time I helped as a volunteer.

Oct

25

My Favorite Doomster, from Nigel Davies

October 25, 2008 | Leave a Comment

Being a bit disappointed with Peter Schiff (in 'Crash Proof' he recommended that Americans borrow on their homes so as to buy 'foreign stocks', so as to emerge with a massive overplus when the US unilaterally collapsed) I've been thinking about the art of the doomster. My pick for being the greatest master of the art is Frazer from the ancient UK TV series, 'Dad's Army', a character who may not be known in the US: excerpt.

Being a bit disappointed with Peter Schiff (in 'Crash Proof' he recommended that Americans borrow on their homes so as to buy 'foreign stocks', so as to emerge with a massive overplus when the US unilaterally collapsed) I've been thinking about the art of the doomster. My pick for being the greatest master of the art is Frazer from the ancient UK TV series, 'Dad's Army', a character who may not be known in the US: excerpt.

GM Davies is the author of Play 1 e4 e5: A Complete Repertoire for Black, Everyman, 2005

Oct

25

Stocks for the Long Run, part II, from Kim Zussman

October 25, 2008 | 1 Comment

(Or what the boring do on Saturday morning)

Curious about investor dispositions over time, I used DJIA monthly closes 1928-present (w/o dividends) to calculate a rolling compounded 10 year return. At the end of each month, plotted the product of this and the prior 119 month's return vs date (see attached - dark blue line) defined:

{kind=link}

Month return = (this month close) / (prior month close) = "M"

10y compound rolling return = {M * M(t-1) *…… *M(t-120)}

Also plotted in pink is ln(DOW) - 4 (to scale with 10y compound rolling return)

Assuming October ends about where it is now, the 10y compound rolling return is currently just under 1 (0.975), which hasn't happened since 1982. The last time 10y compound rolling return dipped below 1 was 1974, and it hovered around this level for 8 years. The the prior sub-1 regime was in the 1930's, so the wait was about 40 years. There is about the same wait between 10y compound rolling return peaks -from 1959 to the most recent in 2000.

While there are few inferences to be made when N=2 (but how often do we get markets like the current one…), this could be evidence for cycles of over–and under–enthusiasm for stocks on the timescale of human-investable-years.

Oct

25

Pointillism and Speculation, from Jeff Watson

October 25, 2008 | 4 Comments

Back in my grad school days, I'd stroll down Michigan Avenue to go over to the Art Institute in Chicago whenever I had some free time.. Although I had covered the entire museum about a hundred times, one painting kept me coming back view every visit, without exception. The painting was Georges Seurat's Post-Impressionist "Sunday Afternoon on the Island of la Grand Jatte." Since Seurat was an early adopter of pointillism, his paintings took on an ethereal quality. Pointillism was a technique that used very small dots of primary colors closely arranged, almost overlapping, that would create the illusion of a variety of secondary colors when observed from a distance. Seurat was probably the second painter, after DaVinci, that melded art with science, except that Seurat took his techniques to a level never before seen in art. He combined the science of such scholars as Chevreul, Newton, Helmholtz, and all of the Neoimpressionists, and was able to reproduce their theories on canvas brilliantly. His ideas were that one could use color to create harmony in a painting, much like a composer could use certain devices to create harmony in music. Seurat said that applying colors to a canvas follow the natural laws of science, much like Newton postulated his law of gravitation from the observation of a falling object.

Back in my grad school days, I'd stroll down Michigan Avenue to go over to the Art Institute in Chicago whenever I had some free time.. Although I had covered the entire museum about a hundred times, one painting kept me coming back view every visit, without exception. The painting was Georges Seurat's Post-Impressionist "Sunday Afternoon on the Island of la Grand Jatte." Since Seurat was an early adopter of pointillism, his paintings took on an ethereal quality. Pointillism was a technique that used very small dots of primary colors closely arranged, almost overlapping, that would create the illusion of a variety of secondary colors when observed from a distance. Seurat was probably the second painter, after DaVinci, that melded art with science, except that Seurat took his techniques to a level never before seen in art. He combined the science of such scholars as Chevreul, Newton, Helmholtz, and all of the Neoimpressionists, and was able to reproduce their theories on canvas brilliantly. His ideas were that one could use color to create harmony in a painting, much like a composer could use certain devices to create harmony in music. Seurat said that applying colors to a canvas follow the natural laws of science, much like Newton postulated his law of gravitation from the observation of a falling object.

I borrowed this passage from Wikipedia regarding Seurat's theories.

They said, "Seurat's theories can be summarized as follows: The emotion of gaiety can be achieved by the domination of luminous hues, by the predominance of warm colors, and by the use of lines directed upward. Calm is achieved through an equivalence/balance of the use of the light and the dark, by the balance of warm and cold colors, and by lines that are horizontal. Sadness is achieved by using dark and cold colors and by lines pointing downwards"

Looking at a work like Seurat's "Sunday Afternoon" can be an emotionally uplifting, beautiful, moving experience. One can get very close up and see the individual points of color, gently dabbed in a very painstaking way. Looking at the very close level makes one appreciate the sheer genius and talent that went into such a masterpiece. Moving 15 feet from the painting, and one is swept away by the magnificence of the entire drama and is allowed to see the entire picture. The whole painting is an illusion, created by nothing more than dots.

In the markets, we're sometimes hypnotized by watching every movement, tick by tick. The ticks, the inside market, can be compared to Seurats' individual tiny dots of primary color. Taken alone in a small sample, they have little meaning, but observed from a distance, a different time frame perhaps, they begin to show the complete picture. The market always tells you what it is doing at any given time, and sometimes even gives you a hint of what it is going to do. It is up to the speculators to connect the dots…pardon my pun.

Oct

25

Multi-Graphics Card Setup in Debian, from Vince Fulco

October 25, 2008 | Leave a Comment

Having just wrestled over the weekend with a multi-monitor, multi-graphics card setup in Debian, found a comment posted today on OneUnified to be useful. hope it saves some folks a few hours.

Oct

24

Five Year Lows, from Scott Brooks

October 24, 2008 | 4 Comments

I firmly believe that cash flow will be king in the coming decade. Buying companies with a solid cash flow that do well in difficult times will allow the prudent investor to have the capital available to make purchases of other companies (and acquire their talent either thru acquisition or hiring them after they are laid off) during this depressed time.

I firmly believe that cash flow will be king in the coming decade. Buying companies with a solid cash flow that do well in difficult times will allow the prudent investor to have the capital available to make purchases of other companies (and acquire their talent either thru acquisition or hiring them after they are laid off) during this depressed time.

Cash flow = money in the bank to buy depressed companies…..depressed companies that offer (what I believe to be) the great growth opportunity of the coming decade.

Kim Zussman writes:

I keep trying to remember why my folks weren't buying stocks in the early 1970's: "cash flow" (used to be called money, like consumers were once citizens) was needed for things like mortgage, cars, food after coupons, and thread for mom to repair our clothes.

Darn socks - damn stocks

Alston Mabry adds:

Given the DS comment on the new cash flow ("I firmly believe that cash flow will be king in the coming decade."), I have the temerity to re-post this link of mine from 2006.

Oct

24

Econ 252 Financial Markets Midterm, Part 2, from Kim Zussman

October 24, 2008 | 2 Comments

2. A market mystery is that crashes are prone to Fridays and Mondays. A certain Friday opens limit-down, but bobs up a bit during the day. What will traders do at the end of the day? Choose the best answer:

A. Fearing a Monday massacre, they sell heavily to the close. You buy because now there is no "portfolio insurance", and a 1987-type crash cannot happen. Plus it's a good way to get a date on Friday night.

B. Traders are horny, so they run the close up. You short or hedge because the lack of fear makes a Monday crash more likely, plus you already had a date on Thursday (meow).

C. Trader is finally listening to the pleas of radical Islam .

Oct

24

War, from Andrea Ravano

October 24, 2008 | 3 Comments

I have the privilege of being born in Western Europe in 1958, and I don't know what being shot at means. On a day like this though, I get the feeling of looking at my city being shelled, in ruins. I do remember two days after the Monday October 19 1987 we were waiting for the 14:30 CET Economic data from the US. Not a noise could be heard. Telephones as well as mouths were shut. The figures for the balance of payments came out much better than expected and the market came back to life. Very few of us were aware at that moment that the market had changed direction. The general manager of the bank had started buying the US market the very same day of the crash. Some executions came in by late Friday due to the massive volume traded on the NYSE. Most purchases were already very profitable by the time the booking was done. As I write I relive some of the feelings of those days, fear, hope, dismay and disbelief are running around in my brain (Dillinger "Cocaine" late 70's). The contract futures limit down early on Friday October 24 2008 are a pretty good sign the forced sales are almost over.

I have the privilege of being born in Western Europe in 1958, and I don't know what being shot at means. On a day like this though, I get the feeling of looking at my city being shelled, in ruins. I do remember two days after the Monday October 19 1987 we were waiting for the 14:30 CET Economic data from the US. Not a noise could be heard. Telephones as well as mouths were shut. The figures for the balance of payments came out much better than expected and the market came back to life. Very few of us were aware at that moment that the market had changed direction. The general manager of the bank had started buying the US market the very same day of the crash. Some executions came in by late Friday due to the massive volume traded on the NYSE. Most purchases were already very profitable by the time the booking was done. As I write I relive some of the feelings of those days, fear, hope, dismay and disbelief are running around in my brain (Dillinger "Cocaine" late 70's). The contract futures limit down early on Friday October 24 2008 are a pretty good sign the forced sales are almost over.

Oct

24

The Old Man and the Sea, from Shui Kage

October 24, 2008 | 3 Comments

Nice time to read The Education of a Speculator.

Nice time to read The Education of a Speculator.

The Yen is making an explosive move against both the Dollar and the Euro, not because the Japanese economy is doing comparatively better than US nor EU, but it is useful to make money. After all, all of the currency traders and investors want profits in their own currency, i. e Americans eventually want US$, Europeans want Euro and Japanese want yen. Soon as the game is over, the Yen will lose its popularity. There is no reason for Yen to be this popular for so long. My special best wishes to Victor and Laurel for good Yen trading. It is almost time for me to buy US$ and sell my Yen.

Oct

23

Arnold, from Steve Leslie

October 23, 2008 | 11 Comments

What are the odds? A man who excels in the obscure sport of bodybuilding, hails from Austria, can't speak English, moves to America, makes an obscure Hercules movie. Now he starts to make movies about a mythical character named Conan. He becomes the biggest box office draw in the world, marries into one of the most powerful political families in America, is elected Governor of the largest state in America and lives a fantasy that we can usually read about only in fairy tales.

Do you think you could learn something from such a man?

Oct

23

A Shocking Consilience, from Victor Niederhoffer

October 23, 2008 | 3 Comments

date level change date level change

fri 10-10 891 -21 fri 10 17 933 -08

mon 10 13 1017 26 mon 10 20 990 57

tue 10 14 1002 -24 tue 10 21 959 -41

wed 10 15 903 -09 wed 10 22 903 -56

thu 10 16 941 38 thu 10 23 915 12

I dare not put the change for 10 17 up except to say that my two year old played heads with the market, and beat me.

Alex Castaldo updates:

The streak continues. Friday of this week was again in the same direction as Friday of last week (down).

Oct

23

Differentials, from Vince Fulco

October 23, 2008 | Leave a Comment

Institutional investors now have a decade of no return. With some detailed credit work they can get 15-20%+ annualized from more senior securities and meet long term liabilities. Why subject oneself to the vol of equities when all your peers are moving to liability management policies and many are way behind the curve? The word on the street is hedgefund managers ( those still in existence) are blowing out their equity teams under the banner, "debt is the place to be for the next decade." Granted equities are undervalued by many historical measure but can stay so for a lengthy amount of time and the recent moves can be lethal if not careful.

Victor Niederhoffer asks:

Given that it would be possible to make 10% on senior debt, what would the required return on equities be at this level? That's my point about VIX and the required a priori rate of return.

Tim Melvin replies:

I would humbly suggest two times the level of senior debt rates.

Phil McDonnell ventures:

One reasonable and quantifiable approach might be to assume the market demands comparable Sharpe ratios from various asset classes. Consequently the ratio of the observed or estimated standard deviations of stocks to bonds may be the same as the ratio of the required expected returns.

Dr. McDonnell is the author of Optimal Portfolio Modeling, Wiley, 2008

Oct

23

An Interesting Parallel, from Nigel Davies

October 23, 2008 | 4 Comments

"Alan Greenspan, the former Federal Reserve chairman once considered the infallible maestro of the financial system, admitted on Thursday that he “made a mistake” in trusting that free markets could regulate themselves without government oversight…. But in a tense exchange with Representative Henry A. Waxman, the California Democrat who is chairman of the committee, Mr. Greenspan conceded a more serious flaw in his own philosophy that unfettered free markets sit at the root of a superior economy."

"Alan Greenspan, the former Federal Reserve chairman once considered the infallible maestro of the financial system, admitted on Thursday that he “made a mistake” in trusting that free markets could regulate themselves without government oversight…. But in a tense exchange with Representative Henry A. Waxman, the California Democrat who is chairman of the committee, Mr. Greenspan conceded a more serious flaw in his own philosophy that unfettered free markets sit at the root of a superior economy."

"Citizen judges, I want to tell [you] how a man who spent thirty years in the party and worked a great deal, stumbled [and] fell … I have committed heinous crimes. I realize this. It is hard to live after such crimes . . . But it is terrible to die with such a stigma. Even from behind bars I would like to see the further flour-ishings of the country I betrayed." Genrikh Yagoda

"… I confirm the admission of my monstrous crimes . . . We were preparing for a coup d'etat, we organized kulak insurrections and terrorist groups … I would like those who have not yet been exposed and have not yet laid down their arms to do so immediately . . . Their only salvation lies in helping the party." Alexei Rykov

GM Davies is the author of Play 1 e4 e5: A Complete Repertoire for Black, Everyman, 2005

Kim Zussman replies:

I doubt Mr Greenspan has as much at stake as the bolsheviks did, though the interesting parallel does illustrate the easy job inquisitors have.

Given government ownership of assets and increased regulation decrease the risk premium, keeping risky assets at a durably lower price level?

Oct

23

Observations, from Victor Niederhoffer

October 23, 2008 | 6 Comments

I always find Mr. Caravaggio's writings very thoughtful and insightful. However, I don't agree that it was a bubble. Prices were and will be completely justified. What was wrong was that the financial companies were leveraged to debt of 30 times their net worth. When the value of their assets which to a first approximation equaled their debt declined by 3%, their net worth was wiped out. The problem was that they made their money by making 1% more than their debt for a long time, and when the negative news had its day on home prices, it was enough to temporarily mark their assets down by 10 to 20 percent or so, without regard to subsequent return. What a former colleague insightfully would call "selling premium." Ouch. Okay, the banks erred. That doesn't mean that they will err again or that cycles will repeat or that the economy will not be resilient. Regions come back much stronger after natural disasters. Things have been worse. The banks were given say 100 billion of money from the rest of us to recoup their bad debt. They're happy. The process of recovery will occur. Proper money management and adherence to economic principles is called for now. The difference between the returns on equities and debt and the required rate of return a priori which is equal to the actual realized return on average, and the average non-understatement of earnings estimates is paramount. Let the bygones be bygones.

I always find Mr. Caravaggio's writings very thoughtful and insightful. However, I don't agree that it was a bubble. Prices were and will be completely justified. What was wrong was that the financial companies were leveraged to debt of 30 times their net worth. When the value of their assets which to a first approximation equaled their debt declined by 3%, their net worth was wiped out. The problem was that they made their money by making 1% more than their debt for a long time, and when the negative news had its day on home prices, it was enough to temporarily mark their assets down by 10 to 20 percent or so, without regard to subsequent return. What a former colleague insightfully would call "selling premium." Ouch. Okay, the banks erred. That doesn't mean that they will err again or that cycles will repeat or that the economy will not be resilient. Regions come back much stronger after natural disasters. Things have been worse. The banks were given say 100 billion of money from the rest of us to recoup their bad debt. They're happy. The process of recovery will occur. Proper money management and adherence to economic principles is called for now. The difference between the returns on equities and debt and the required rate of return a priori which is equal to the actual realized return on average, and the average non-understatement of earnings estimates is paramount. Let the bygones be bygones.

Vince Fulco adds:

Institutional investors now have a decade of no return. With some detailed credit work they can get 15-20%+ annualized from more senior securities and meet long term liabilities. Why subject oneself to the vol of equities when all your peers are moving to liability management policies and many are way behind the curve? The word on the street is hedgefund managers (those still in existence) are blowing out their equity teams under the banner, "debt is the place to be for the next decade." Granted equities are undervalued by many historical measure but can stay so for a lengthy amount of time and the recent moves can be lethal if not careful.

Riz Din replies:

Lack of returns is a problem for this generation but when I hear of the 'death of equities' I can't help but to think of past messages such as 'death of inflation' and 'death of cheap oil' and how they turned out.

Rocky Humbert remarks:

I'm watching for an inflection point on the number of Google hits for "Nouriel Roubini" as an important signal for a persistent rally in all risk assets.

Oct

23

Swap Spread Madness, from Jeffrey Emanuel

October 23, 2008 | 5 Comments

See chart showing the relation between 30 yr swap spreads and 5 yr swap spread going back to 1994.

{kind=link}

The current situation seems incredibly absurd to me– can any readers offer some insight into the economic/financial implications of this? It seems to me that the 30-yr swap spread is utterly out of whack (the 5-yr swap spread is also pretty darn low considering the distress in the banking sector; see this for more on why I think that. In fact, the 30-yr swap spread recently turned negative! (it's now hovering above zero). Consider for a moment what a negative 30-yr swap spread implies. For one, it is saying that the full faith and credit of the US Treasury isn't as good as an unsecured obligation of some shaky banks. But going beyond that, suppose the 30yr swap spread remains near zero. That would means that, if I had a $1b floating rate loan at say, 50 over libor, someone would be willing to lock me into a fixed rate for 30 years, and the rate I could lock it in at is the yield on the 30 yr treasury bond. Now, as we all know, treasuries are pretty expensive at the moment — flight to quality and all that. This statement is of course more applicable to short maturity Treasuries, but it is still the same underlying credit for the 30 yr. Now, I don't know about you guys, but with the way the fed has been printing money lately (see Federal Reserve release, +$245b in a week, and it's much worse, because as you can see, in that last week they sold a bunch of treasuries and replaced them with… crappy assets from banks), I can easily see Libor getting up to very high single digits over the next 10 years.

So what's going on here? What has caused this dislocation? Let's see what the fixed income mavens have to say about this.

Convergence trade anyone? Would be easy to put on — just pay fixed on a 30 yr interest rate swap, and then receive fixed on a 5 yr swap. You could lever it up pretty ridiculously too, as long as you had some cash put aside so you could stay in the game if this madness got even worse.

Oct

23

Econ 252 Financial Markets Midterm, from Kim Zussman

October 23, 2008 | Leave a Comment

1. Risk appetite is to (__________) as (__________) is to (__________)

A. The trader, tunnel of love, cute amusement parks

B. The US capitalist system, egg, matzo-brei

C. Dead generals, never to be written chapters, history books

D. The male black widow, leverage, market liquidity

Oct

23

Bennis on Wisdom and Leadership [$], from Mark Goulston

October 23, 2008 | Leave a Comment

Normally we try to stick to education and not commerce on this site, but one of our members has insights and asked us to post this for him . As Horatio Bump said of Davey Crockett "I believe that Dr. Goulston is a man of integrity and insight". Vic.

Mark Goulston announces:

Sadly there is much more brightness (how to turn nothing into something) and smartness (how to turn something into everything) in this world than wisdom (knowing what is important and worth fighting for and what's not). If you want to bathe yourself in the wisdom of one of the wisest people you will ever listen to, you and your teams should attend the live webinar:

Move from Managing to Leading, with Warren Bennis

Warren Bennis, the foremost authority on leadership in the world, will be interviewed by Dr. Mark Goulston, one of our Daily Speculations contributors on Oct. 28 from 9:30-11 AM PST/11:30-2 PM EST. The forementioned link will enable you to receive a discount on this [$] event.

Oct

23

More on Volatility: the Cost of (In)decision, from Sushil Kedia

October 23, 2008 | Leave a Comment

Andrew McCauley says, "Volatility itself can be a decision: Long or short volatility."

Andrew McCauley says, "Volatility itself can be a decision: Long or short volatility."