Aug

31

Speed and Longevity, from Victor Niederhoffer

August 31, 2008 | Leave a Comment

I have come across several conflicting ideas about the relation of speed and longevity recently. In Eric Sloane, the idea is that the slowest animals live the longest, but several studies show that that the fastest runners live the longest. I wonder how this would be resolved in the real world of markets. Speed and distance, and lifespan would seem to be helpful concepts to untwine.

I have come across several conflicting ideas about the relation of speed and longevity recently. In Eric Sloane, the idea is that the slowest animals live the longest, but several studies show that that the fastest runners live the longest. I wonder how this would be resolved in the real world of markets. Speed and distance, and lifespan would seem to be helpful concepts to untwine.

Dylan Distasio adds:

Typically, larger animals have longer natural lifespans. This is likely related to their lower base metabolic rates (a smaller mammal is going to have a faster metabolism to offset greater loss of body heat). The most obvious analogy would be market cap and the idea that larger companies are slower to shift course.

Another factor is how prodigious the species is at reproducing. High fecundity usually means a shorter lifespan. Is there an analogy to this in the markets? If we use our imaginations, perhaps. Maybe an area of the market with many competitive companies, and a low barrier for entry like the Internet space.

For those who are gluttons for punishment, there is scientific journal article on body size, metabolism and lifespan that may be worth untangling.

Scott Brooks recalls:

I saw a special on either Discovery Channel about heart rate. They did a comparison between many animals and the number of heart beats they had in a lifetime. The one that stick out in my mind was the difference between some kind of mouse and an elephant. The difference in life expectancy was quite substantial in terms of years, but the average number of total heart beats between birth and death was essentially equal.

This didn't hold up for all species, but there were some striking similarities between mammalian species and heart beats.

If this is true, then am I using up my "lifetime heartbeats" each time I work out?

I know that my family doesn't live particularly long, with most dying at or near average life expectancy. I also know that for my entire life, my resting heart rate has been in the upper 80s or low 90s. I've worked diligently to get it lower, but it doesn't come down. When I exercise, I get my heart rate up into the 160s or 170s — if I'm really working our hard, then I'll get it up into the 180s or 190s.

Am I using up my heartbeats?

Marion Dreyfus reassures:

When I worked for the giant ad agency J Walter Thompson, the physican onstaff, with whom I consulted about all of my copy, used to tell me: "I have grown old walking in the funeral corteges of those more fit than I."

Kim Zussman, on the other hand, enjoys frightening people:

Don't forget, the healthier your heart (and the longer you go without heart attack) — the more likely you are to die of cancer.

Low fat diet, exercise, contol of blood pressure/blood sugar, have much bigger effect in forestalling heart disease than cancer.

Aug

30

Briefly Speaking, from Victor Niederhoffer

August 30, 2008 | 3 Comments

Here's a composite of a typical season in a horse trader's life that will enable you to understand such things as why the market is bad when it looks good, why the value stocks are good when everyone wants the tech stocks, the importance of liquidity, the prevalence of deception, and the back and forth in the market during the day and year.

Here's a composite of a typical season in a horse trader's life that will enable you to understand such things as why the market is bad when it looks good, why the value stocks are good when everyone wants the tech stocks, the importance of liquidity, the prevalence of deception, and the back and forth in the market during the day and year.

Ben's usual technique when entering a new area like Mississippi is to sit at the long table in the hotel and flatter the locals "Of course I didn't hesitate to let them in on the fact that I was from Texas, and I didn't know too much about the farming business, that I'd made my living on a horse about all of my life. But I told them I had a high regard for the people that tilled the soil and fed the world and provided fiber that made the clothes, and I knew that this type of citizen was the salt of the earth. I said something about what a fertile land the Mississippi Valley was and how much of the rest of the world Miss could feed and clothe. I also dropped in that I knew the Miss Valley was stocked with some of the finest old Southern people in the nation because that wasn't going to hurt my case any either." How many times one is cajoled into some deal where it starts out that they flatter you to death thereby lowering your guard. "Our trader is thrilled at the opportunity to trade with you but begs that you go easy on him".

But this time, hoping to meet a better heeled citizen that could buy 60 mules that he couldn't sell for a dime worth 30 bucks a head, Ben Green stays at a fancy hotel where there are fewer mule men to sell at a proper price when he wishes to sell his mule. "I was just peeping out from under the brim of my Stetson and had my boot crossed over my knee so that everybody could for sure tell I was from way out West". The anxious seller always pretends that he's short on brains and the farthest thing from his mind is selling.

He sees a mark "He walked up in the lobby and stood looking into the dining room and I could tell for sure he was off his home range" (The best cons come spontaneously when the other side isn't expecting it.)

"I got up and moseyed up close to him to get acquainted because I knew I looked country enough that he would ask me whatever it was that he was trying to find out " . It might be that he wanted to buy some mules and the last thing that Ben wants him to know is that he might sell. (The salesman with tremendous urgency to unload bonds or stock is in conference, please call back later.)

Russ Sears applies the lesson:

The latest Investment Outlook from PIMCO's Mr. Gross paints a dire picture for Mortgage Backed Securities, perhaps because he is starting a new fund that plans to buy some of them mules.

Aug

30

More on Google and the Media, from Stefan Jovanovich

August 30, 2008 | Leave a Comment

One of the passengers I got to spy on during my time as Dad's designated driver for joy riding with actual and would-be authors was the renowned painter Thomas Hart Benton. Benton had hinted that he might want to publish his memoirs so Dad had me drive them up to the Cloisters when Benton visited New York. Benton said that he "missed the Depression" because Benton & Bowles was doing so well as one of the first independent advertising agencies that he never knew anything even close to hard times in his business. Google employees probably enjoyed a similar insulation until the price of GOOG common stock and their stock option mansions started going south, but I doubt there is much euphoria in the cubicles right now. Paid search is still the only business that Google has that makes money, and the extraordinary technical ingenuity of their employees may end up being like Xerox Parc — great for the country and the world, terrible for the company paying the bills. The "mainstream" journalists are accurately reflecting the general public's disenchantment (9% Congressional approval rating), and the financial press is pessimistic is for the same reason that most people living in the major media centers of the United States are in a sour mood: they have seen their principal assets — their homes — go literally in the tank.

One of the passengers I got to spy on during my time as Dad's designated driver for joy riding with actual and would-be authors was the renowned painter Thomas Hart Benton. Benton had hinted that he might want to publish his memoirs so Dad had me drive them up to the Cloisters when Benton visited New York. Benton said that he "missed the Depression" because Benton & Bowles was doing so well as one of the first independent advertising agencies that he never knew anything even close to hard times in his business. Google employees probably enjoyed a similar insulation until the price of GOOG common stock and their stock option mansions started going south, but I doubt there is much euphoria in the cubicles right now. Paid search is still the only business that Google has that makes money, and the extraordinary technical ingenuity of their employees may end up being like Xerox Parc — great for the country and the world, terrible for the company paying the bills. The "mainstream" journalists are accurately reflecting the general public's disenchantment (9% Congressional approval rating), and the financial press is pessimistic is for the same reason that most people living in the major media centers of the United States are in a sour mood: they have seen their principal assets — their homes — go literally in the tank.

I agree with Dr. McDonnell that paid search advertising has certainly had an effect on newspapers, but eBay, Yahoo, Craig's List, Amazon and the decline and fall of the department store have cumulatively had a greater effect. Radio has actually seen revenue growth, if you included the satellite broadcasters. Their profit problems have come from the fact that, like the movies, radio has become a hits business; it is no longer possible to be a low cost producer. As Dr. McDonnel says, general circulation magazines have become nearly obsolete, but their more important, if less noticed, cousins the trade magazines have held up very well and those publications are definitely not replacing their reporters with younger, prettier and cheaper talent. Quite the contrary, they are offering a refuge to the experienced print journalists who can actually produce 500 words in an hour that answer the basic questions of Who, What, When and Where.

The worst is certainly not over for our business out here in LaLaLand. If I have still managed to make more money this year from buying and selling common stocks than from our "real" business, it is because the business's income has done a Margaret Hamilton over the past few months. In the end, Dr. McDonnell is right on the money. The valuations in the companies that I look at — those with belt, suspender and Velcro-cinched balance sheets — have become as compelling as they were five years ago. It is time to throw up in your own waste basket and buy.

Perry Metzger counters:

Trade magazines in electronics are a shadow of what they once were. Every issue of EE Times, the biggest trade rag in the electronics business, got smaller and smaller for a few years, but then they switched from tabloid format to magazine size to save additional money and that’s stopped for a little while. The size of the reporting staff has gone down, too. Same thing is true for almost all of the ad supported industry rags I’m familiar with.

Trade magazines in electronics are a shadow of what they once were. Every issue of EE Times, the biggest trade rag in the electronics business, got smaller and smaller for a few years, but then they switched from tabloid format to magazine size to save additional money and that’s stopped for a little while. The size of the reporting staff has gone down, too. Same thing is true for almost all of the ad supported industry rags I’m familiar with.

It is true that the only business at Google that makes money is paid advertising, but quite certainly not simply on search-based advertising. They own large web ad networks like DoubleClick that were profitable before Google bought them, and I suspect they make money on things like Gmail and Google Reader because of the advertising. They’re currently losing money on their video properties, but they’re starting to change that as well — they only began to attempt to monetize them in the last couple of months.

Aug

28

Blame It On Google, from Phil McDonnell

August 28, 2008 | 8 Comments

It seems every day for the past few months we heard another story about how bad the economy is. The mainstream media have had a monotonously lugubrious message about how bad it is. Against this backdrop we have today the salutary news that GDP rebounded at an adjusted annual rate of more than 3% in the second quarter. Simply put, the widely predicted recession never happened.

It seems every day for the past few months we heard another story about how bad the economy is. The mainstream media have had a monotonously lugubrious message about how bad it is. Against this backdrop we have today the salutary news that GDP rebounded at an adjusted annual rate of more than 3% in the second quarter. Simply put, the widely predicted recession never happened.

This still begs the very real question as to why the mainstream media are so bearish on the economy. There are several reasons for this but one is often overlooked. Part of the blame for the bearishness of the press can be placed on Google.

Clearly the people at Google are not sending out negative messages nor are they inherently pessimistic. In fact the opposite is true. Google is one of the most successful companies in history. Most of its employees are active participants in its success story. So the folks at Google are just short of euphoric on the economy. It is working very well for them. But that is exactly the problem. Google has a had enormous disruptive influence on other media companies. It has adversely impacted newspapers, magazines, radio, TV and pretty much every other advertising medium.

Across the board things are bad for almost all media companies who do not have a significant Internet presence. Sales are falling and consequently earnings have been decimated. No question, the media industry is in a Google-induced depression. So it should be no wonder that the mood in the financial press is depressed. They are losing their jobs wholesale. Over the last year many if not all senior columnists or reporters have been replaced in many companies. Typically they are being replaced by younger, prettier and, most importantly, cheaper talent. Many of these Young Turks have never seen a bear market. The guidance of the financial media has never been very good at its best, but this new generation may represent a new level of ineptitude. They are far too quick to hit the panic button.

However that is no reason that the rest of us need to panic. This time it is not different. Financial crises happen all the time and with a certain cyclical regularity. The GDP number tells us the worst is behind us and that the non-financial non-real-estate part of the economy is just fine. I believe stocks are more undervalued than at any time since 2003.

Dr. McDonnell is the author of Optimal Portfolio Modeling, Wiley, 2008

Aug

28

Evolution of Long Distance Running, from Russ Sears

August 28, 2008 | 3 Comments

Watching the Olympics, it was clear that distance running has moved up a notch from 1996. It was only 12 years ago that I thought with some hard work and perhaps a miraculous race of a lifetime one day I could make the USA marathon team. But what I watched this past year with the US team trials and then the Olympic marathon was a spectacle most amazing. I was left wondering how I ever thought I had a chance. What was I thinking? I don't know how to convey how good a 2:06 marathon is, especially in those hot conditions. It is something I think you can only feel, by running with those who have that capability. The only way to understand it is to feel the intensity of the competition, by keeping pace with those amazing talents for a few miles of such a marathon. You can only understand the inner strength of such athletes if you've tried to built up that strength brick by brick — if you knew intimately the effort necessary, and built up within you a magnificently strong structure and then felt it melt by the heat of their calm efforts.

Watching the Olympics, it was clear that distance running has moved up a notch from 1996. It was only 12 years ago that I thought with some hard work and perhaps a miraculous race of a lifetime one day I could make the USA marathon team. But what I watched this past year with the US team trials and then the Olympic marathon was a spectacle most amazing. I was left wondering how I ever thought I had a chance. What was I thinking? I don't know how to convey how good a 2:06 marathon is, especially in those hot conditions. It is something I think you can only feel, by running with those who have that capability. The only way to understand it is to feel the intensity of the competition, by keeping pace with those amazing talents for a few miles of such a marathon. You can only understand the inner strength of such athletes if you've tried to built up that strength brick by brick — if you knew intimately the effort necessary, and built up within you a magnificently strong structure and then felt it melt by the heat of their calm efforts.

But what I found most amazing was not the asymptotic curve of times as displayed by the 4:00 mile, or the swimming pool. The line gets moved downward as methods, coaching and even equipment improve. But what I found amazing was the great diversity of talent. Any of those top 10 marathoners could have won, given the right venue. But the diversity of talent ensured that even given a terrible venue, one would still shine.

It's impossible to say who would have been best, given today’s knowledge, methods, equipment and training using yesterday's top talent. Everybody responds differently to different methods, especially the extreme training you need to do to be competitive today. For example altitude-simulating chambers will give one guy a bigger edge than another.

Many have said that yesterday’s talent would never be the best today. And I know in my case, it is probably right; I wouldn’t have gone as far as I did in today’s deep field of youth and talent. But in general I disagree. It's not that they wouldn’t be the best, it's that they would be the best only under a much narrower set up of circumstances. It reminds me of the high school three sport athlete star who gets to college and has to decide which sport to play. Running today is more specialized, for example one marathoner may do better in heat, another in higher altitudes, another on hilly course, another on rougher roads. So it's not just survival of the fittest narrowing the field, but heightened competition responding to the need for more diversity.

Hence the market continually responds differently, not just because the competition is more cut-throat and getting tougher so all must learn new tricks, but because intense competition prepares for strenuous times by developing more diverse talents.

Scott Brooks adds:

If my math is correct, these runners are moving at a rate of ~12.5 mph to cover that distance in 2:06. They are running ~4:48/mile pace for all 26.21875 miles. That is a stunning pace! It makes me ask a question I've always wondered. What is the limit of human endurance? How much more time can we whittle of those numbers? Sure, I guess as time measurements get better we can break it down to the 1/10000th of a second someday to measure the difference between athletes. But when do the changes stop becoming meaningful? In 100 years from now, will marathoners be breaking the two hour barrier with regularity and how much will they break it by? What about 200 years from now?

Russ Sears replies:

The physics of the sport are more important than the time measurement accuracy. For example in measuring a marathon course, I believe it is officially 42,195 meters, then you must add 42 meters, because the course may shrink with temperature. So there maybe some truth to the joke, perhaps they needed to measure the distance of the cube again with so many records being broken. In about 1992, I read an article in Sports Illustrated claiming to analyze the Track and Field events for the physical limits of what is possible. All were well past the then current world record, but I believe that several have since been broken, such as the 10k time.

But for every ten innovations that shave a 1/10th of a second per mile you get one innovation that shaves a full second. Perhaps eventually you reach the point where for every 100 innovations you get 1/100 and one you get 1/10th but you never know if the 1 millionth innovation shaves that full second off again. But what I think you are seeing is that rather than just the talent and training, controlling the conditions of the event starts to mean more than the control of the talent/training. Hence on any given day one can beat the others.

Adam Robinson predicts:

The marathon world record will be under two hours in the year 2023, according to my projections, though it could be broken earlier with superior terrain and weather conditions.

The equation I fit was:

Marathon post WWII times (in minutes) = 159 - .00044 * (world pop.)^0.5

Nigel Davies queries:

Are you sure this will be linear? Training methods and superior equipment may be part of the equation but other factors could include things like human height (with a direct effect on stride length) and population size (increasing or decreasing competition). And it seems there's a cyclical element to human height at least; it declined in the late 19th and increased in the 20th century.

Adam Robinson replies:

There's no way to model training method improvements, and I assume in something like the marathon that technique and training is probably close to asymptotically perfected as we're likely to see, unlike shorter events where a better start or something might shave off a significant fraction of time.

But note that the relationship is not linear, it's based on the square root of the world's population, which is how the bell curve of talent will disperse, so the model's based on the very simple assumption that the fastest time will improve simply because the sample size has gotten larger.

I did this quickly, back-of-the-envelope, when in fact a better model would have been the world record as a function of the accumulated population of the world. But as a rough (90% accurate) prediction, it's not bad.

Clive Burlin says it all depends on incentives:

Idolize and pay huge sums of money to marathon winners and sub two hours will be broken long before 2023.

Why would anyone but a narcissist endure all that pain when you can go out on a field, catch a ball, run a few yards and make 20 million a year?

When marathon runners start making mad Benjamins, more will come out to train and break records.

Stefan Jovanovich rectifies:

There has only been one baseball player paid $20 million/year; and, as Yankee fans know, Mr. Rodriguez is not being paid for his glove work. As for running backs, none is paid $20 million a year or anything close to it. One of the great successes of the NFL — compared to baseball and basketball — is that the spread between the publicly-announced salaries and the net cash received by players is 50% or more; it was one of Gene Upshaw's many burdens that the NFL Player's Unions strikes were not nearly as effective as the baseball and basketball player unions "job actions" have been. (Anyone have any idea why?)

Compared to what they made even ten years ago, track and field athletes have made remarkable gains; there are now several thousand professionals who actually make a living from their pains. In Carl Lewis' heyday the number was fewer than one hundred. There may be more than narcissism motivating those guys in Mexico City who train in the smog every day.

One of the fascinating ironies of the Olympics regarding money and sports was that the Russian women's basketball team won the bronze medal by having the American Becky Hammon as a ringer. When one of the newsies complained that she has playing for the U.S. cold war enemy, she pointed out that the U.S. team did not invite her to play (itself puzzling since she is the best pure shooter in the history of U.S. women's professional basketball). She also pointed out that she makes far more money playing for the Moscow team in the Russian professional basketball league than she makes playing for San Antonio in the WNBA.

Aug

27

The Most Amazing Thing, from Victor Niederhoffer

August 27, 2008 | 7 Comments

The most amazing thing about markets to me is that no matter how many previous instances I have, I can never find days that are anywhere near the ones we are currently having. The S&P is moving from x day highs to y day lows with impunity and alacrity and then hanging on the balance scale at the end of day when Zeus decides who will win.

Peter Earle replies:

I remember reading a book several years ago about Roger Bannister and his breaking of the four minute mile in 1954. At the time there were any number of physicians who predicted that the record was physically impossible to break; one predicted that Bannister's heart would explode in accomplishing such a feat.

I was reminded of this in both watching (and hearing) that, once again, in a seemingly inexorable march of highs (and lows), world records were broken throughout the Olympics in Beijing.

It bears mentioning that the events themselves have changed greatly from year to year: not only in the rise of professional Olympians, undistracted from a training (indeed, a living) regimen by employment, formal education or social duties, but as well in the structure of the events themselves. Engineered swimsuits, deeper pools, vacated end lanes, and other such changes in swimming events alone have contributed to the aforementioned increase of extremes.

So too, in the markets: that the year-over-year outdoing of previous records in extremes have as much, if not more, to do with the character, fragmentation and specialization of market venues; the "democratization" of access to various markets, bringing millions of additional opinions and hundreds of billions more dollars in; the rise of electronic, in particular algorithmic trading; better/faster processing speeds in technology; and the like, ad infinitum — than of any intrinsic quality of markets.

Kim Zussman ponders:

Like global warming, it is hard to measure whether the market becomes progressively and durably more efficient, or just temporarily stations in an efficient regime. Presumably the proportion of outperforming trader/investors who persist over long periods must go down if markets get more efficient, but that number ought to be hard to get, in that widespread knowledge could discourage the hopeful machine.

Anatoly Veltman adds:

I'll give you another factoid: TY (10-y Treasury futures) lost 10% of Open Interest on the Fri, Aug 22 drop. We just found out that FV (5-y Treasury futures) gained almost 10% of Open Interest in Tue, Aug 26 slow trade. Any connection to the recent abandonment of 10-y as the benchmark?

Aug

25

What is Art?, from Scott Brooks

August 25, 2008 | 18 Comments

I have never gotten art. I can't determine what is and isn't a great work of art, or even define what constitutes a great work of art.

Kim Zussman replies:

Scott, in my experience art is very personal communication - between the artist and the viewer, and between the viewers.

Yes, there is much scholarship on the subject: what was innovative, what changed the world. But good pieces talk if you listen carefully. And great pieces will never leave you.

Even modern art.

For example, take this web site's favorite subject of barbecue: There have been many descriptions of delicious smoked ribs, dripping sausages, saucy pulled pork. When you savor this food, you taste something of the life and the love of the cooks - as well as friends who find it important enough to recommend. A common experience, which feels unique, and pre-dates you by thousands of years and will continue to live beyond.

Isn't it wonderful to share food loved by all? That's art - because it is talking to you - and many others. You are connected to past and future. It talks without words and within it you speak loud in silence. If you cannot hear then you are not listening or it is not talking.

Beautiful women are art. Yes, they are up to something, and indeed they are programmed functionaries. But if her flashing eyes unsettle you, or the fine hair on her arm or the particular curve of her breast, this is art (as well they know). That they don't realize the extent of their role is art.

Even not-beautiful women are art. Sometimes the best kind of art.

Art debilitates. And it's funny.

We cannot seek it - it will come for us. And raise us up, by the neck for just long enough to allow the taste of life and the understanding that others can taste it too.

Aug

25

Distribution of Absolute Value of Half Hourly Changes for S&P Futures, from Victor Niederhoffer

August 25, 2008 | 1 Comment

The recent distribution is as follows:

. 8 22 8 21 8 20 8 19 8 18 . 10 + 7.5 - 10.0 1 5.0 - 7.5 5 1 2.5 - 5.0 5 2 5 2 3 . 0 - 2.5 9 11 4 12 9

The distribution of changes has many interesting implications. But to me it highlights the aburdity of going down a googol on PPI and up a googol on Bernanke's comments that inflation numbers should be better in the future.

Aug

25

Anecdotal Evidence from a Cruise Ship, from Russ Sears

August 25, 2008 | 1 Comment

There has been much talk lately of how everybody except big oil is in a major downturn. Housing stinks, Wall Street geniuses are looking for work and while some manufacturing is up, you better be prepared to get a new job if you work for a domestic auto company and our import/export deficit can't keep up with the long term price of oil. And how will the consumer keep up, now that the housing ATM is shut-off?

Yet, my vacation found a much brighter picture. There is a buzz around the farm communities that hasn't been there for years. Commodity prices are swinging, but most have locked in healthy profits. There finally is money in the bank, or at least a healthy balance sheet, to upgrade the house, buy those acres the old neighbor's son had been renting to them or buying the equipment that they needed. Single mansion sized houses are going up in a sea of corn. Much of the heartland is springing back to life.

On the ship to Alaska there were many Aussie, Asians and Canadians aboard. Still plenty of free spending USA citizens. To get the best views at supper you would request to sit with other couples or families. Each on hearing my profession, asked my opinion on the subprime mess and when the banks would recover. However, each talked glowingly about their local economies and jobs. In no particular order I meet a nurse that coordinates Canadian health care, a retired merchant marine, a retired naval man, a retired dock worker, a Las Vegas golf course lawn care pro, a semi-retired air force pilot, a director of a drug rehab facility, a couple of tax preparers, a personal trainer/rehab for a nursing home, a nurse, a ski resort masseuse, a few small business owners. Not only did their jobs seem to be in high growth economic areas, their communities invariably did also.

It may have been that this was my first vacation starting from a west coast cruise, but I only meet one guy that sheepishly admitted that he was a stock broker during the early hay-days of the 90's before starting his own business. The makeup of who are taking these luxury vacations seems to have completely changed from the 90's. While there where many foreigners it seemed that their make-up has changed to much more European. There also were considerable more Asian. They too seemed to be a different group than the technology smart group, hip youth who planned on making USA their permanent home. Now many foreign tourists seem to be much more broad professionals group, with family in tow. All seemed willing to spend freely.

The staff was composed of almost all foreigners. It appeared that the ship was able to pick the cream of the crop. And on talking with the staff, reinforced this assumption. From the lowest cabin maid to the first mate besides being well groomed, they were bright, spoke great English, eager to please and were very friendly. Many nationalities where represented. From First World to Third World all seemed glad to be on a vessel touring the USA.

While such a census may be simply be descriptive, not predictive, sometimes carefully watching for who is prospering and inferring the future paths can be helpful. It would seem the old definitions hold: recession — when your neighbor loses his livelihood; depression — when you do.

Aug

25

The Lies, Liars and Con-men of the Klondike Gold Rush, from Russ Sears

August 25, 2008 | Leave a Comment

Wherever there are rational people responding to instinct, doing foolish and irrational things, you will find a swarm of lies and deception. Mark Twain's story of the Duke and the King with its parody of the Shakespeare play shows how the lie and liars work in such a situation. It starts with the lure: the promoter telling the truth, but not the whole truth. The victims of the lure turn to pathological lying; rather than admitting a mistake, they allow themselves to become strong supporters of the promoter. And finally you find the con-men each stepping over the others to take advantage of the swarm.

The Klondike gold rush was born of instinct. Great wealth and dangerous conditions ensured that greed, fear and folly were sure to follow.

A. The Truth but not the Whole truth.

First came the media and marketer alliance created to oversell its wares. This group often prides itself on technically telling the truth, but practices deliberate deception by creating an illusion to promote their agenda. Perhaps chief amongst them was Erastus Brainerd, a Harvard educated newspaper man, editor of the Seattle Times. He is noted for fueling the rush into a frenzy. He sent out over 70,000 pamphlets to every US post office and to libraries, besides promoting the Seattle through news reports. The "reports" are now regarded as little more than thin guises, advertising Seattle. His efforts won Seattle a role as the trail-head of the gold rush, mainly because his map to riches started in Seattle. This created a boom town monopoly for supplying the prospectors.

If there is any doubt that the prospectors felt duped, consider the complaints against W. D. Wood. Wood, on hearing the news of the gold, promptly resigned as mayor of Seattle to run a steamboat business for the eager prospectors. He was almost lynched by his customers when they saw he left much of their newly acquired gear on the dock because he overbooked his ship. However, in true politician fashion he was able to talk his way off the gallows by returning the ship to pick-up the gear.

I was conversing with some descendants of a rusher, granddaughters and great grand kids, who also toured Skagway, Alaska, gateway to the Klondike. They were taking the tour still trying to understand what could have possessed their bright forefather to have made such a foolhardy expedition. With such clear signs, in hindsight, that the efforts were clearly doomed to failure they are still questioning such a costly mistake. The success of the deceptions below should be studied by all trying to get rich. The promoters created the rush by:

1. Creating a bottle neck. Most simply choose Seattle for the starting place to load up simply because Brainerd's map showed this as the start of exploration. Actually several cities to the north (in Canada) or south would have expedited the trip.

2. Old news is still actionable. Reporting on how to plan an expedition implied that the reader was receiving up to date news relevant for decision making.

3. Creating a rush. Downplaying the crowds, the impossible odds for all but the front line and those with the best organized efforts and reporting of how an individual would go about prospecting as if this was the most rational choice.

4. Targeting the educated, wealthy; planting "reports" in libraries. Most of the prospectors were professionals. Emphasizing the need to plan, and the expense, ensured the prospectors would have money to burn.

5. Under-reporting the corruption, organized scamming and organized crime. Implying just hard effort and brains would win. No need to be on guard, questioning everything. Especially don't question the truth of reporting.

6. Ramping up the lies with questionable sources. The Seattle papers had a steady stream of reporters going to and from Skagway. The "expert's" stories of success largely came from two sources. The collaborators, fellow promoters whose success, like the reporter success, came from successful crowd herding. Many needed cheap laborers, and many needed gulible people to dupe. Also many tales of prospecting success from clear failure and pathological liars- a group that has trouble distinguishing reality from what they wished were reality. The lies got bigger, with the "reporters" were looking for "sources" that were simply willing to outdo the last one.

7. Appeal to the adventure, versus the cold hard truth of death and total ruin. If there were any "balance" in the piece it still did not convey the odds, or give a clear picture of the risk. Many smart, strong, prepared men were doomed to die by sheer bad luck.

8. Needing the crowd, promoters reassure the crowd that so many can't all be wrong, when a few moments thoughts would reveal the opposite: that following the crowd ensures all fail. What I found interesting was that much of the tourist trade by the Alaska inner passage still heavily relies on such crowd herding devices to pad the wallets.

B. The second liar is the pathological liar. The harsh reality of the task of prospecting, the insurmountable odds of the Klondik, made many a former honest man into such a liar. Pathological liars, lie about everything, from what they ate for breakfast to their net worth and physical and mental abilities.

Clearly, as Twain's story shows, one person can be all three, a promoter, con-man and pathological liar. But what separates a pathological liar from the other two is this need to live in an alternate reality. They need to live in a world, very similar to reality, but slightly altered so that their folly and gut instincts become genius. Most stories contain some truth, and the reason the liar can appear to actually believe in the lies, is in his opinion, it could have easily happened that way, just need a slight reallignment of reality. The purpose of every "story" is to believe if luck had simply smiled on me, I would be successful. Implying as luck changes I will be fine. However, the only effort these liars put forth, so there luck could change, was to create a pyramid scheme fueled by their lies. But often these are given strength by the promoter's organization, and their need to distance themselves from the lie, but support the lie.

The gateway town to the Klondike was full of such men: men who were once town leaders, the most educated doctors and lawyers; men who had given up, men that had known those that struck it rich, men that were trapped into a position of either admitting their mistake and going home or living the life of a pawn and liar.

C. Finally, the con-man: What distinguishes a con-man is his deceptions go directly for your wallet. Perhaps the best known and most sucessful con-man of the era was Soapy-Smith. Soapy got his name from his Colorado days when he and his gang would sell soap by holding rigged lotteries, in which he would place large dollar bills, $10, $20, $50, and $100. The crowds would start buying, when they saw someone unwrap a $10 and yell "I won $10!". Then same with the $20, and $50. And after that he would turn them into a wild mob when he announced, Nobody has picked the $100 dollars winner yet. This funded his was to Alaska, where he and his cohorts bought a tavern and brothel. Soon he had many other businesses, a telegraph office, with wires that ended just outside of town. Skagway did not get an actual telegraph until 2 year after his death. Here are a few observation to perhaps helps spot such a con-man:

1. He kept politicians on his payroll. Hosting the Governor four days before his death. He owned the town police and government. Many a fool would be taken in by underestimating the scope of his operations.

2. He gave generously to all churches. And he would set up "charities" to expand his kingdom such as "finding" owners for the "orphaned sled dogs". Influence was as important to him as wealth.

3. After conning many out of their money in his gambling establishments, he would instruct his workers to send them to his telegraph office… where he could ask someone at home for more money. Of course without a real telegraph, no money would come. He would instruct the telegraph office to send the lost soul to him, where he would give them the fare, to leave town.

4. He generously donated and took up a collection for the widow after one of

his men shot a local man in a argument over change.

5. Even with such measures to eliminate enemies and mobs, when the government turned a blind eye, the legitimate businesses and town people gouped against him. His demise came when a group of his men out-right stole several thousand of dollars of gold dust from a prospector unwilling to gamble, knowing he would be swindled. The locals had a gunfight in which he died. His gang fled town quickly and he was buried in a paupers grave, with nobody attending his funeral.

There are many more Klondike characters to research.

Aug

22

Following My Passion, from Daniel Flam

August 22, 2008 | 11 Comments

I know it's way off topic - I am passionate about going into an automated trading strategy oriented position, I have been following this web site for many years now and I have developed quite a lot of interesting strategies all automated, and some profitable on paper. I am a top programmer [C, C++, R, WealthLab, NinjaTrader and scripting languages like PHP, Perl etc.] with a wide variety of skills including leveraging my home network as a Beowolf cluster to calculate complex R simulations on 3000 equities ("dad, why is guitar hero running slowly?"). I constantly read material on mathematical techniques and can present some really interesting and novel ideas. I wrote some really interesting code reading poker cards off the screen and working out Bayesian odds - with (positively) surprising results. It is really my passion and I would think this is the place to find someone who shares this passion for the markets now that I am looking for a new position.

Aug

21

Q. What provision does the value investor make for an error in his estimation of the "true" value?

Q. What provision does the value investor make for an error in his estimation of the "true" value?

A. Investing is not a precise science, a fair value is an estimate. That estimate is as good as the assumptions that went into it. I detest the precision of many sell side analysts when they estimate the value of the company (i.e. we believe this company is worth $10.75 thus at $10.10 it is 6% undervalued). I suggest to tamper with assumptions to arrive to ranges of estimate (i.e. change discount rate, sales growth, profit margins etc., tinker with them to figure out the impact they have on the fair value. Also playing with these variables will help you to understand which ones have the most impact on the value of the firm and thus you can spend your time focusing on things that really matter).

In my analysis the required margin of safety is a function of two variables: company's quality (the higher the quality the less margin of safety I need); and fundamental return (earnings growth and dividends), the lower the fundamental return the higher margin of safety I'll require as I need to be compensated for the stock turning into dead money. In other words when you own a company that doesn't grow earnings or pay a dividends, a time is not on your side, thus you want to make sure that you are compensated for that by a larger discount to fair value.

Q. What of Keynes's warning about the tenacity of the market's irrationality outlasting one's funds or investment horizon. How do you deal with that?

A. Great question!

The point I made above answers this question somewhat, but I'll repeat. If I own companies that pay dividends and grow earnings I'm compensated for the wait. Dividends provide a real time payments, where earnings growth makes companies more and more valuable, compressing the P/E under the stock.

This is a reason why I don't use leverage. Leverage compresses the time of your bet. Even if you are right on undervaluation, leverage may kick you out of the position before your proven right. To some degree this is what happened to LTCM, they were right on the arbitrage but because of the high leverage they did not survive to see themselves being proven right.

Q. Also, at what point does the value investor exit on the upside, assuming that the market "wises up" to the "true" value of the stock and starts bidding it up? When the price reaches value, or when it overshoots it by some predetermined amount, or what?

A. I suggest figuring out the sell price or sell P/E (I prefer P/E) at the time of purchase. This way you have not developed the psychological attachment to the company. I discuss selling in my book in depth (Active Value Investing: Making Money in Range-Bound Markets). The sell price will be close to the fair value point.

Q. Finally, can't the stock price itself affect "the fundamentals" in a Sorosian fashion (e.g., cost of capital, certain loan provision triggers, ability to make acquisitions, attractiveness as an employer, etc)?

A. I try not to own companies that rely heavily on external financing or their P/E staying high so they can make "accretive" acquisitions. This point you touched upon is so true with banks in today's environment; they have to issue stock because their capital is destroyed, but their stock is down. But let me give you the opposite side of this: I own UNH , WLP, NOK and Microsoft , these companies have couple things in common, they have incredible balance sheets (NOK and MSFT have no net debt and billions of cash), lower stock prices will provide these companies an opportunity to buy their stock on the cheap.

Q. The bedrock premises of value investing have always left me slightly puzzled, as if I'm missing something.

A. I guess the idea behind value investing is to find companies that market misprices (often for psychological reasons) and sell them when market recognizes the error.

Aug

21

Double Pump, from Jim Sogi

August 21, 2008 | 1 Comment

Did you ever see Michael Jordan floating through the air doing the double pump fake out shot as two or three blockers got faked out by his feints?

Today's [August 20, 2008] S&P looks like a double pump after a quick dip under the basket. Looks like it was a fake out. Took a bit of travel and not a three pointer, but point was made.

Aug

20

The Tao of Poker, reviewed by Vince Fulco

August 20, 2008 | 5 Comments

A colleague recently mentioned The Tao of Poker by Larry Phillips. What an excellent find and addition to one's inner game library. Some of it reminds me of the wisdom Vic and Laurel have imparted over the years.

A colleague recently mentioned The Tao of Poker by Larry Phillips. What an excellent find and addition to one's inner game library. Some of it reminds me of the wisdom Vic and Laurel have imparted over the years.

The author documents 285 rules for playing. The first couple are right up there with trading truisms-

1) Don't dig yourself into a hole when you first sit down.

2) If you think you are beat, get out.

3) Start with premium hands. When you get them, bet them. If the hand starts to deteriorate, get away from the hand.

4) If you don't think your hand is good enough, it probably isn't.

5) If you do make a mistake, correct it as soon as you can.

6) It's important that a player starts seeing "staying too long on marginal hands" as where the money goes.

7) The money you don't lose from staying too long in a hand and the money another player does lose from doing this is often the profit you go home with.

8) The hand you really want to spend your money on may be right around the corner.

I was also touched by the dedication which is one of the most heartfelt and genuine ones I've read in years. And of course strikes at the core of the trading experience.

""To Mandius…This book is dedicated to my grandson, Mandius, and the poker players of the future. As a friend once observed: They'll be a lot like we were– and they'll go through all the same things. They'll gather around the same green felt tables, suffer the same bad beats, and experience the same agonies of seeing an opponent hit a two-outer. They'll know the feeling of being down to their last dollar as the light comes up in the dawn, as well as the exhilaration of dragging in a mountain of chips on days when the angels hover around them. They'll experience high drama and low drama, hear great stories, experience laughter, and free food.

They'll meet people they otherwise would not have met–great people from every walk of life–some of the best people, it will turn out, they will probably ever know in life. If, as James Earl Jones once said, ' Children are a message we send to a time and place we will never see,' then these are our ambassadors to a poker future yet unseen. Accept this note of well-wishes from those who went before you– a message from the past.

Aug

19

BBQ, from Jim Sogi

August 19, 2008 | 3 Comments

Some fancy BBQ: Squab (breast, sliced), lightly seared, mushroom or Bearnaise sauce on top of some fried Foie Gras, on top of shitake mushrooms chopped, sauteed and seasoned; all on top of a toasted and seasoned French bread slice ala Brochette style, with Raptor Ridge Pinot Noir from Oregon 2006. As we say in Hawaii, "Broke da mouth" (tastes so good).

Aug

18

Olympic Lessons, from Russell Sears

August 18, 2008 | 9 Comments

The Summer Olympics is the one time that I watch way too much TV and so far there have been many lessons for life and trading.

The Summer Olympics is the one time that I watch way too much TV and so far there have been many lessons for life and trading.

Phelps in general:

1. Stating a goal publicly leads to personal commitment to keep it.

2. Families that support each other go further individually.

3. Use others' antagonism as motivation.

4. If you are passionate, dedicated and talented about something, people will find you fascinating even though you are singleminded about something most people consider dull.

5. Give credit to those who helped you. Never forgetting to thank your coach, especially after a tough win.

Phelps miracle touch win:

1. Stay focused on what you can do, not what success others are having

2. Momentum or Acceleration/Deceleration are very deceptive to predict, but in hindsight can have dramatic results. On second thought everybody "knew" he would come through. Remember, even the experts called it wrong immediately after the race and before the results, even his Mom.

3. Keep your head down, don't raise your head in victory, until it's done.

4. The biggest of kingdoms may occasionally be lost by want of a nail, but the biggest of kingdoms usually got there by always having that spare nail to draw on when needed.

The Chinese Dominance of Gymnastics and Diving

1. A country that is authoritarian and values rules above the individual can excel in a sport that has strict rules, close adherence to "the system" and where perfection is based judges' acceptance. But it has difficulty excelling in the non-arbitrary judged and purer individual athletic sports. You will get the results that match the way you rule your people.

2. Success of such an authoritarian system is terribly inefficient despite its new found embrace of "competition".

3. The USA 1, 2 in womens gymnastics, was a sharp contrast for their artistry and exuberance, to the rigorous and painful to watch approach of the young Chinese. Implying you can't demand passion and love.

4. Extreme youth and their resilience can bear such a system only for awhile. In contrast to the now 33 year old German medalist who continued in the sport winning a medal for the love of her western womens coach who saved her son from leukemia. But in such a harsh system the youth dreams quickly turn to being the authority rather than the producer.

The medal count China versus USA, China many Gold few silver very few bronze. USA more bronze than silver, or gold:

1. While the west, capitalism, especially the USA version, are accused of the

unhealthy "win at all cost" attitude., it would appear to me that USA values the individuals more who clearly tried despite not winning.

2. Making their women's gymnasts age an officially sanctioned lie shows that the system "win" is the goal, not the sport. Again long term such a system will

crumble due to inefficiency.

The emergence of Jamaica as the new fastest country:

1. Talent with increased opportunity gives results. The more competitive and

global USA college coaching system has given both.

2. The same with many more high caliber meets and more global competition. The more competitve the system, the more chances to win and the more winners the system can support. This makes picking the best harder, but making the best better.

3. Even with raw talent, great coaching or standing on the shoulders of the experts of the past is necessary.

The 38 year old Romanian Women's Marathon gold medalist:

1. She was a surprise gold medalist by making a gutsy daring surge on miles

12-16 gaining about a minute lead on the crowded "lead pack". When the

conditions are brutal, often the biggest risk is taking no risk and playing it safe.

2. Sticking to your plan, despite others' reaction, if built on study and understanding of the problem, is best.

3. While in the long run anything can happen, it doesn't happen unless you

train and sweat for many years, believing with conviction, "anything can happen" if I put my mind to it.

And now I have to go back to NBC, and perhaps more insights on these and other events.

Nigel Davies comments:

This is an interesting post, but I think it may be overly simple to define China's approach to sport as just 'authoritarian' given its millenia old culture and long standing traditions of personal cultivation. As Bronstein once wrote, we already know that one horse can run faster than another. So is it really surprising that China doesn't 'get' 'competition' in quite the same way that the West does?

This doesn't, however, mean that its athletes are merely acting out of obedience. Having hung out with lots of former Soviet chess players I learned that there are very strong incentives to succeed at sport in a communist country. Add to that the fact that national pride is much stronger in China than it ever was in the artificial entity that was Soviet Union and you have a potent mix. Sure they may lack 'joy' and 'passion', but these things didn't stop surly Soviet chess players kicking our joyful asses for decades.

It would be interesting to get expert insight on this, but the Chinese seem to have promoted some sports more heavily than others. For example they became utterly dominant in table-tennis without showing too much elsewhere but have recently branched out. Now they're the top nation in women's chess and look like they could soon dominate the male game too. And just like the Soviets they never crack a smile.

Aug

18

WSJ Calls Inside Buyers Ignorant, from Steve Ellison

August 18, 2008 | 2 Comments

Throughout Wall Street history, insiders have earned superior returns on purchases and sales of their companies' stocks. H. Neyjat Seyhun wrote a book in 1998, "Investment Intelligence from Insider Trading", detailing an exhaustive study of insider transactions. Seyhun found that stocks in which insiders were net buyers outperformed stocks in which insiders were net sellers by an average of 8% in the following 12 months.

Throughout Wall Street history, insiders have earned superior returns on purchases and sales of their companies' stocks. H. Neyjat Seyhun wrote a book in 1998, "Investment Intelligence from Insider Trading", detailing an exhaustive study of insider transactions. Seyhun found that stocks in which insiders were net buyers outperformed stocks in which insiders were net sellers by an average of 8% in the following 12 months.

The Wall Street Journal is well aware of this outperformance and regularly reports on insider transactions. I was quite surprised, therefore, by today's Heard on the Street column. David Reilly suggests that investors would be foolish to follow the lead of financial company executives, whose net purchases of their companies' shares in July were the highest in 10 years.

Excerpt : [subscription required for link to full article].

"Company executives clearly have better information than the average investor. But it doesn't always pay to follow their buying cues.

Like plenty of other investors, executives at financial firms haven't been good at calling bottoms during the credit crunch. In the third quarter of 2007, executives and directors of diversified financial companies — brokers, big banks and exchange operators, among others — bought more stock in their own companies than at any other time since the third quarter of 2002, according to data from Gradient Analytics.

The trade didn't work. The third quarter of 2007 was anything but the bottom for financial stocks …

Today, financial executives are back buying. Since the end of June, the value of purchases, when compared with share sales, has reached its highest level in a decade."

Kim Zussman replies:

It would seem difficult to believe in changing cycles (dissipation of knowable patterns), and not suspect that insider buying has been gamed - by insiders who are informed of the literature and seek (for not unselfish reasons) to align with shareholder objectives.

Whether Seyhun's alpha persists will be answered in time, but like others which are well-known, expect it to run through a period of great disfavor before flying again.

Victor Niederhoffer comments:

It's ridiculous to assume that because in one quarter insiders were wrong, this disproves studies based on hundreds of thousands of trades. Of course it doesn't work, some quarters — like the beaten favorite Federer: that's when he's going to win the doubles for sure.

[Dr. Niederhoffer is the author of "Predictive and Statistical Properties of Insider Trading", The Journal of Law and Economics XI (April 1968): 35-53.]

Aug

18

Sports and Markets, from Victor Niederhoffer

August 18, 2008 | 2 Comments

That Little Extra

That Little Extra

There are so many market lessons that one can learn from the Olympics. To me the most important was that that little extra is the difference between success and failure. This was most apparent in the two big 0.01 second differential swimming races involving Phelps and Torres. In one case, Phelps said it was the difference of a "shaved finger" and in the second Torres said "I shouldn't have filed my nails." The former apparently referred to better streamlining and the latter to extra reach. Phelps had broken his wrist in 2007 and the extra kicking training he did helped him on the last reach, creating the winning margin. He stated that when he practices it's like a bank deposit. So often during the year, during a career, one decision, one wrong practice can mean the difference between success and failure. It underlines the importance of total concentration at all times, and constant practice.

The Blake/Gonzales match

Much has been written concerning the sportsmanship involved in the Blake semifinal. Right after the match in a press conference Blake remarked that his father would never have let him do it, and would have taken him out of the tournament. Jack Kramer has a similar remark in Ed Spec about his father's breaking his racket in a similar moment of poor sportsmanship and presumably Blake knew of this instance which is tennis lore, although I have found that among tennis players Kramer is derided for his treatment of Pancho. However, the key to me was that Blake must have been brooding about the incident from 5-5 in order to come up with such a lengthy exegesis right after the match. The brooding probably caused a lack of focus that led to loss. I had a similar revelation in my career when, at an early age, I used to complain about all the bad calls the refs made in squash. I subsequently realized that the complaining did me more harm than good. It not only took away my subsequent energy, but gave the infractor the advantage of seeing how much misery his misdeed caused. I stopped complaining during the last 10 years of playing and it was very helpful. Time and again I won when I would have lost if I had stuck up for my rights on the point. The same is always true with bad fills. By the time I've complained about bad fills, or bad equipment, or bad treatment by a counterpart… By the time I've complained about it, and taking into consideration the extra costs involved and the missed subsequent opportunities, it's over. The legal system is such that on all matters involving less than 10 figures the costs are greater than the differences at issue. So that avenue never pays.

Putting it all together, one learns never to distract oneself worrying about the other side's problems and to concentrate on improving oneself and playing harder to compensate for the wrongdoing.

Denis Vako replies:

I can't define what "shaved finger" margin is, or unshaved for that matter, that is surely a joke, but in swimming hitting the wall makes the great difference for the result; as when one swims his body/hands/legs are doing cyclical movements and ability to break this cycle or accelerate it, to cut time on touching the wall, will win the race at the finish. In other words, when race is short, i.e. 50m or 100m, among equal sportsmen (as almost always the case), it is the touching of the wall which will determine the winner.

Different strategies there are, depending on the distance; when it is 50m race it is about how you jump into the water, how long you spend gliding under it and on the distance that left one must exhaust all his reserves before promptly touching the wall. While in a 200m or 400m race, one has more margin for error and strategy is more or less to "swim with the pack" and then to have an ability to explode the last 10-25% of the distance.

Stefan Jovanovitch writes:

It wasn't the finger; it was the half stroke before the final full one that gave Phelps the acceleration to touch out Cavic. Cavic's technique was the right one except he looked up a fraction before he touched. That lift of the neck and the added drag is probably what cost him the race. These are not my opinions but those of daughter, who — before her back injury — was good enough to be one of the field horses in Natalie Coughlin's 14-18 year old races at our County swim meet. Whether Cavic's looking up was a failure of character or just the inexperience that comes with being in a big race for the first time is also a question I leave to those who can read others' minds and souls.

Reid Wientge adds:

Athletes "letting up" at the finish line seems to be endemic. It's in baseball and can be found almost every game. In the Olympics, I watched a German lose in one man paddling (the paddler kneels in the boat) because he slackened his pace just before the finish line. And I do mean just — he had the Gold in his canoe but his opponent, who had been challenging for more than half the race, pulled hard all the way to the line and won by a fraction of a bow.

Jordan Low extends:

We should trade by following our models, and constant meddling, i.e., looking up, while a trade is still in play, causes drag. Trading is like competitive swimming: there are many factors that you have to perfect, from the stroke to the turn, etc.

Nigel Davies replies:

I believe that Stefan is right in implying this goes much deeper. Trying to compensate for what seem to be the errors ('looking up' or 'not sticking to systems') tends to do little other than consume the attention after which a thousand other small errors appear.

So instead of vowing never to look up again, the guy should seek out the small vanity that distracted him with the thought of medals and glory. But this is somewhere most people won't go; it's easier on the ego to find some other excuse.

Jeff Watson writes:

Back in my old days at the Mid America Commodity Exchange, the weekend before my trading debut, I remember practicing hand signals in the mirror for hours and hours on end. I wanted to hard wire them into my brain so they would come out effortlessly, with 100% accuracy. Anything less than perfect might end up with my having bought 20,000 bushels of March wheat at 3/4, when I meant to sell 20,000 bushels of May at 1/2. Vic and Laurel understand the value of practice, and know exactly what the fruits of practice will bear. Even though it's the oldest cliche in the book, "Practice makes perfect" is still an integral path in the road to success.

Ian Brakspear corrects:

"Practice makes permanent" — each time you repeat something incorrectly you are making the mistake more ingrained in your mind. It is crucial to have the right program/instruction before you start.

Aug

17

Preparing for a Hurricane, from Jeff Watson

August 17, 2008 | 1 Comment

The National Weather Service has issued many different models for Tropical Storm (soon to be Hurricane) Fay, most of which head in my direction, right on top of my head. The expert meteorologists say that the storm will make landfall on Tuesday, somewhere between Ft. Myers and Tampa, with my neighborhood right in the middle. Since I've been through this a few times, I know the drill. This morning I shuttered my house in about 90 minutes. Since I have a long term view of being prepared for an emergency, our generator is topped off, we have food and water for 35 days, and we don't have to panic. I ran over to the grocery store this morning for some donuts, and saw the madding crowd. Everyone was stripping the shelves, buying all the water, batteries, and staple items like there was no tomorrow. Tempers were flaring and people were pushing and shoving, much like the guys in the wheat pit when some bad news comes out. I'm sure that Lowe's and Home Depot are experiencing the same thing with plywood for windows. Preparedness for a hurricane is similar to preparing for a market event. Have a plan, stick to it, and modify it as conditions require. One can ensure personal safety through proper planning, much as one can reduce market losses through proper planning. Our plan is to always have on hand enough supplies to get through any disruption in the supply chain. One thing about a catastrophic event in nature or the market, once the damage has been done, the growth can resume. Four years ago, Hurricane Charlie missed us by a mere 30 miles. The beachfront residents to the south of me were 60% wiped out. Today, that area is back, bigger and better than ever. Markets in 1907-08, 1929, 1932, 1972, 1987, 2001-02 were all catastrophic events in those times, and all more than recovered, completely. Nature, like the markets, sometimes must wash things away so growth can continue. Nature and the markets both deserve respect because if taken lightly, they can do serious damage to your health and your bankroll.

The National Weather Service has issued many different models for Tropical Storm (soon to be Hurricane) Fay, most of which head in my direction, right on top of my head. The expert meteorologists say that the storm will make landfall on Tuesday, somewhere between Ft. Myers and Tampa, with my neighborhood right in the middle. Since I've been through this a few times, I know the drill. This morning I shuttered my house in about 90 minutes. Since I have a long term view of being prepared for an emergency, our generator is topped off, we have food and water for 35 days, and we don't have to panic. I ran over to the grocery store this morning for some donuts, and saw the madding crowd. Everyone was stripping the shelves, buying all the water, batteries, and staple items like there was no tomorrow. Tempers were flaring and people were pushing and shoving, much like the guys in the wheat pit when some bad news comes out. I'm sure that Lowe's and Home Depot are experiencing the same thing with plywood for windows. Preparedness for a hurricane is similar to preparing for a market event. Have a plan, stick to it, and modify it as conditions require. One can ensure personal safety through proper planning, much as one can reduce market losses through proper planning. Our plan is to always have on hand enough supplies to get through any disruption in the supply chain. One thing about a catastrophic event in nature or the market, once the damage has been done, the growth can resume. Four years ago, Hurricane Charlie missed us by a mere 30 miles. The beachfront residents to the south of me were 60% wiped out. Today, that area is back, bigger and better than ever. Markets in 1907-08, 1929, 1932, 1972, 1987, 2001-02 were all catastrophic events in those times, and all more than recovered, completely. Nature, like the markets, sometimes must wash things away so growth can continue. Nature and the markets both deserve respect because if taken lightly, they can do serious damage to your health and your bankroll.

Aug

17

Let’s Debate Bank Stocks, from J. T. Holley

August 17, 2008 | 4 Comments

Sometimes I think that all these banks with brokerages attached are issuing 8%-9% preferred while simultaneously driving down their own common to be able to buy back their own stock later on the cheap and ride it back up gaining momentum until the 2013 call dates on all these preferred where they'll do secondary offerings pay off the preferred and the beat goes on! I know it ain't that simple but it sure looks like that is what is going on to me. I mean the real probability of a bank run has what been elevated from what, 2%, to 2.5% probability? Similar to foreclosure rate going up and everyone already assigning in their heads a permanent straight line to 100% foreclosure, heck the White House might have to be foreclosed on in that picture accordin' to many.

Sometimes I think that all these banks with brokerages attached are issuing 8%-9% preferred while simultaneously driving down their own common to be able to buy back their own stock later on the cheap and ride it back up gaining momentum until the 2013 call dates on all these preferred where they'll do secondary offerings pay off the preferred and the beat goes on! I know it ain't that simple but it sure looks like that is what is going on to me. I mean the real probability of a bank run has what been elevated from what, 2%, to 2.5% probability? Similar to foreclosure rate going up and everyone already assigning in their heads a permanent straight line to 100% foreclosure, heck the White House might have to be foreclosed on in that picture accordin' to many.

Y'all think Ms. Whitney seems to have all the answers [22 minute video dated May 27 2008, Transcript]?

Value investor Tim Melvin replies:

Read the FDIC website, it is worse than you think.

Read the various statistical reports… loan loss reserves and net chargeoffs continue to grow and credit is getting tighter by the day.

J. T. Holley replies:

There are over 8000 banks under the FDIC umbrealla; if 2% failed that would be 160 or more banks. Right now on the list it’s only 11 with close to 20 shutting down in the ’00-’03 recession. So we could be possibly over halfway done for all you know?

Tim Melvin is not amused:

Fine, buy 'em all… especially if the NPA's are over 2% and climbing. It will be fine.

Ignore the rising charge offs, foreclosures and loan loss reserves. Derivative exposure means nothing. Just buy 'em all.

Equity to assets failing? No worries it's bullish. Consent letter signed? Buy it up.

Halfway done implies another 40% drop in valuation so, yeah, maybe we are halfway done.

J. T. Holley answers:

I certainly understand your feelings and am not ambivalent to the situation at hand but a very good analogy is my experience in the Navy with crabs and most venereal diseases. When a sailor ports his mind is on usually two things that being booze and the opposite sex. This led this middle class white boy from Virginia to experience things that had never been a part of the spectrum of my life. When a sailor contracted something and was revealed once we set sail he was avoided and condemned. Kwell was passed out and penicillin was on hand. Everyone had a sense of cleanliness that wasn’t felt ever in my life. Toilet lids were swiped four to five times. Contact was avoided at all costs. Mattresses were burned and/or thrown overboard into the ocean (this was 1990). After a while the exiled was allowed back amongst the population and normalcy came.

The banking sector has crabs/vd. Not all banks are bad. Not all of them are going to go under. Yes, they all are playing defense right now to dress up the pig with lipstick. I never said no worries, just not fear of economic nuclear winter that seems ever so present. I didn’t even say buy ‘em, buy ‘em all? I just simply wanted to say that it ain’t as bad as it seems. Feelings seem to be dominating way too much. I know before you get to 160 you have to pass through 10, 11, 12, 13, 14 and such but geez I’d rather see negative PE’s across the board (no such thing) and 80 banks gone under or merged before I’d feel the fear that most feel right now?

Aug

15

Tension and Release, from Victor Niederhoffer

August 15, 2008 | 1 Comment

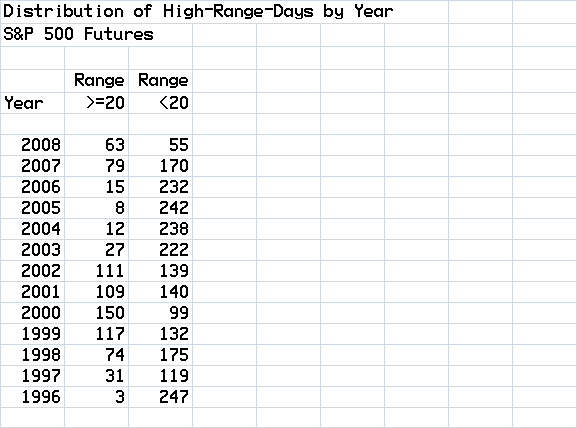

I note that today's range in S&P of 11.2 was a 40 day low, the lowest since Monday, June 23. Such a low range fits in with music theory that talks about how certain intervals such as the 3, 4, 5, 6, are particularly flowery, while others, especially the 2 and 7, are hollow and bitter. I note that after the low ranges of 12 or less the standard deviations the next two days are about 2/3 as great as after the above 12 range days. Around the third day, there seems to be some new music in each case.

I note that today's range in S&P of 11.2 was a 40 day low, the lowest since Monday, June 23. Such a low range fits in with music theory that talks about how certain intervals such as the 3, 4, 5, 6, are particularly flowery, while others, especially the 2 and 7, are hollow and bitter. I note that after the low ranges of 12 or less the standard deviations the next two days are about 2/3 as great as after the above 12 range days. Around the third day, there seems to be some new music in each case.

Aug

15

Free Style World Checkers Championship, from Alan Millhone

August 15, 2008 | 1 Comment

September 8th to 13th in Medina, Ohio I will have the privilege of being the Match Referee for a 20 game match between two fine gentlemen of color, for the "Free Style" World's Checker Title (held by Tommie Wiswell of Brooklyn, N.Y. for many years till he retired from the game and relinquished his title). Ron 'Suki' King of Barbados has held this coveted title for 19 years now. His opponent is from Port Elizabeth, South Africa by the name of Lubabalo Kondlo, who through the sponsorship of Vic and Laurel was able to come to Vegas twice last year to first win the ACF National Championship and then come back and win the WCDF World Qualifier and the right to issue a challenge to Mr. King.

September 8th to 13th in Medina, Ohio I will have the privilege of being the Match Referee for a 20 game match between two fine gentlemen of color, for the "Free Style" World's Checker Title (held by Tommie Wiswell of Brooklyn, N.Y. for many years till he retired from the game and relinquished his title). Ron 'Suki' King of Barbados has held this coveted title for 19 years now. His opponent is from Port Elizabeth, South Africa by the name of Lubabalo Kondlo, who through the sponsorship of Vic and Laurel was able to come to Vegas twice last year to first win the ACF National Championship and then come back and win the WCDF World Qualifier and the right to issue a challenge to Mr. King.

While these two men play each other for the week I will watch the clock they use and will record the moves they make. Both men exhibit the highest level of sportsmanship and make my job almost unnecessary! Lubabalo will arrive in Columbus, Ohio a week before the match and will be a guest in my home and will have access to my Checker library and be able to relax and sleep off any jet lag.

Lubabalo emailed me today and will be on national TV in South Africa before he leaves for America. He has no computer nor Internet (too poor) and walks 10 miles each way to a Somalian grocery store once a week to use the Internet cafe' there to keep in touch with me.

And you thought you have it tough at times! LOL

Aug

15

Biotech, from Tom Marks

August 15, 2008 | 2 Comments

A good friend from the Comex metals pits told me about a year ago he wanted to eschew the violent volatility in those markets. Recently at one point, silver had dropped about 5 1/2 bucks the last month alone, $27,500/contract.

A good friend from the Comex metals pits told me about a year ago he wanted to eschew the violent volatility in those markets. Recently at one point, silver had dropped about 5 1/2 bucks the last month alone, $27,500/contract.

Looking for a more placid pastime, went eyeing individual stocks. Amongst others, recently some of the biotech persuasion. Out of the frying pan, into the fire. Oops.

Bought 5000 Elan at $24, quickly went over $37. Analysts were saying eventually over $70. Clinical results come out, a few patients got sick out of 31,800 on the new drug.