Jan

31

Market Completeness, from Vinh Tu

January 31, 2008 | 2 Comments

"…Left off the balance sheet is the value of the asset that Gary Becker, Nobel Laureate in Economics, calls human capital. Professor Becker says that the skills and experience of our people are worth more than half a million dollars per person. By this calculation, traditional assets comprise less than 25 percent of the national balance sheet, which means that true U.S. assets exceed $180 trillion…" Mike Milken

I haven't had my morning coffee yet but here's an attempt at arithmetic along Beckerian lines:

A recent FT article put Japanese assets at 75% of its GDP. Pulling a totally random number out of nowhere, if the return on assets is 5%,

GDP = 5%*(total assets)

GDP = 5%*75%*GDP+5%*humancapital

19.25*GDP = humancapital

Looking at World Bank statistics

World GDP 2006 = 48.2 trillion

World financial assets = 170 trillion

Return on assets = 5% (can someone give me a better number?)

Return on financial assets = 8.5 trillion

Return on human capital = 39.7 trillion

Human capital = 794 trillion

population = 6.6 billion

Average human capital per capita (hheh..) = 120303.3

Anyway, very rough calculations with numbers plucked from the ether, but the order of magnitude at least is in line with Prof. Becker.

(Also, I left out something important - GDP is not just a return on capital (even human capital) because human ingenuity produces excess profits and increases the value of the capital. So you'd have to adjust the calculation of human capital to account for growing return. And risk adjustments. Etc. etc.)

Any real macro economists care to point me in the direction of more accuracy?

Phil McDonnell replies:

Rather than pulling an imaginary growth rate out of our … armpit, perhaps a better approach can be found. GDP is the goods and services produced by a society. However much of that is consumed as well. The number we are really seeking is the net 'profit' figure that can be carried forward into the next year. It is good to remember that any 'profit' carried over must be held in the form of an asset. Thus a reasonable measure of the rate of return would be the net increase in total assets year over year.

Yishen Kuik counters:

Maybe I'm too classical, but I've always thought that GDP is a flow measure of all the goods and services we produce, of which one portion is consumed to give us present utility and the remaining portion is invested to enhance our ability to increase GDP in the next period.

Presumably all goods have some aspect of both utility and investment ("school is fun and you learn something" or "bridges are beautiful and enable transportation"), but we can think of the investment portion of GDP as flowing into a stock of accumulated capital.

The stock of capital deteriorates over time, so some of that flow is just running to keep still. Part of the stock is human, part of it is physical plant, and part of it is institutional arrangement of society (courts, laws etc). The dollar figure we attach to capital stock is just a very rough attempt at measurement, and doesn't take into account the importance of having the right arrangement of the 3 kinds of capital stock. The right arrangement catalyzes a $100mm investment to return 15%, while the wrong arrangement will have no such catalyzing effect. That is why $100mm produces such different results when invested in America versus Africa.

I think it is this accumulated capital stock (human/physical/institutional) which is the right place to discuss big picture returns on investment. Unfortunately much of it is unquantified and unquantifiable.

Adi Schnytzer brings up the stock market aspect:

Surely the real issue here is that, however, we define GDP, it's notoriously unpredictable? After all, why has the market been shooting up and down so furiously lately? In part it's because every one has been wondering whether or not the US economy is moving into a recession. Well, if we could agree on a way to to measure and predict GDP, we'd have solved that issue for the market pretty quickly, wouldn't we?

Derek Gard dissents:

This assumes the market moves based on GDP at all.

From 1950 to 1960 GDP went from 1696.765 to 2517.365 (48%) and the DJIA went from 198.89 to 679.06 (241%)

From 1960 to 1970 GDP went from 2517.365 to 3759.997 (49%) and the DJIA went from 679.06 to 809.2 (19%)

From 1970 to 1980 GDP went from 3759.997 to 5221.253 (39%) and the DJIA went from 809.2 to 824.57 (2%)

From 1980 to 1990 GDP went from 5221.253 to 7112.100 (36%) and the DJIA went from 824.57 to 2810.15 (240%)

From 1990 to 2000 GDP went from 7112.100 to 9695.631 (36%) and the DJIA went from 2810.15 to 11357.01 (304%)

GDP during the 60s was higher than the 50s and yet the market barely budged. And GDP during the 60s and 70s surpassed the growth rates of the 80s and 90s, yet what decades saw the greatest gains in stocks? Stock market moves do not correlate well with actual GDP data over decades or even years, let alone the daily thoughts and musings of financial pundits.

To say stocks move on GDP data, or confusion thereof, is not supported by raw data. This is the same logic that says, "Stocks rose on a drop in oil prices" one day and then the very next day says, "Stocks fall despite a decline in oil prices." It is a fallacy promulgated by the same people who earned 3.5% per year in stocks during the 80s and 90s when the market was earning more than triple that.

Adi Schnytzer replies:

My argument was not that the market moves in line with GDP, rather that lately the market has been reacting to news suggesting either an imminent recession or not. To measure the relevance of this assertion you need to check whether or not the market falls some months before a recession (thus anticipating it) and not whether over a long period the market tracks GDP.

Nigel Davies opines:

As a simple chess player I must admit to being confused by the apparent

implication (seen everywhere right now) that positive GDP is good and

negative GDP is bad. In my own admitedly primitive pursuit one rarely

gets the opportunity to play expansive moves on a continuous basis,

there are periods when one must regroup in order to increase the

potential energy of a position.

So if I were an economist I would not be looking for answers in simple

linear relationships. Instead I'd try to study the interplay between

'potential energy' (one might try to define this in many ways, for

example by defining debt in 'real' terms) and GDP. And I'd hypothesise

that one of the most bullish economic times would be during a recession

in which personal debt was being reduced.

Vinh Tu tries to sum up and conclude:

Whether more GDP is "good" or "bad" is a normative judgment. To an

economist, however, since GDP by definition refers to the production of

"goods", it has to be good. (It is generally assumed that utility is

monotonically increasing with goods.) Whether the increase in goods

produced corresponds to an increase in share prices is an entirely

different matter. A share represents a claim on assets which, in turn,

yield a stream of goods (or money which can be exchanged for goods.)

Whether an increase in GDP is beneficial for share prices has

everything to do with where that increase comes from. An increase in

efficiency, whereby the return on existing assets increases, would

probably increase share prices, all else being equal. On the other

hand, the creation of new capital assets would not increase the value

of pre-existing assets if it resulted in the assets being less

efficient.

Jan

31

Risk Management, from “R.S.”

January 31, 2008 | 2 Comments

Risk Management

(for the French)

.

The flowers must be fresh,

The wine and food superb,

And dont forget to,

Bring a nice trinket or two,

For a fine lady whos not afraid of

Playing both sides.

.

Forget everything she told you

Remember everything left unsaid

And dont forget to,

Give a kind word or two,

For a fine lady whos not afraid of

Playing both sides.

.

She'll flirt with disaster,

She'll lay with a brute,

Lest you forget to,

Alter the vases water,

For a fine lady whos not afraid of

Playing both sides.

.

She'll love your soft pillows,

Dont let'em comfort you,

Lest you forget the

Hunger a row under

For a fine lady whos not afraid of

Playing both sides.

.

Jan

31

Wrongly Accused of Sportmanship, by Nigel Davies

January 31, 2008 | 3 Comments

Last Sunday I was accused of 'sportsmanship'. Frankly I felt like a mug. What happened was that in a crucial tournament game in a rapidplay event the minute hand on my opponent's clock stopped moving when he had 5 minutes left. This meant that he effectively had unlimited time and I saw a better position and time advantage evaporate into a loss. Immediately after the game it was established that this had indeed been a defective clock but that my resignation had to stand. I didn't kick up a fuss because then I stood to lose more than just the point. This is why my 'sportsmanship' later got praised.

Naturally I've been thinking about what I should have done, this was the first time I've had this situation. It's difficult to know because calling the arbiter means losing concentration and thinking time, not to mention the fact that you're in the lap of the gods once officials are involved. One could simply ask for a new clock, providing there's someone there to hear this request. But given the potential for argument a better approach may be to knock the clock to the floor, by 'accident' of course. Hopefully the thing will more obviously break and at the very least you can ask for a new clock 'just in case'.

Shouldn't the organisers have ensure that all the clocks were working? In theory, yes of course. But this is the kind of naive attitude that means you always get shafted. It's better to leave 'challenging authority' out of the battle plan.

A Trader from NYC adds:

It is difficult to know what to do. This happens in real trading situations all of the time, and I've been on both sides. There have been many times where I've seen a trader at a Nice Yokel Scum Exchange appear to not honor a posted market. Do I take time out from my trading to call surveillance and have it tracked down, knowing that they are inclined to take the other guy's side?

As a market-maker I've been on the other side too. On the ARCA options exchange, for example, a customer has 30 minutes, I think, to ask for a trade-break on an "obvious" error. The exchange would then look at it, then make a ruling, then call me. So 45 minutes or so after a trade, I get call on something that has already been hedged, on an option that has been up 50% and down 50% in value on the day. I then have to decide do I lose yet more time fighting the ruling, knowing I'm going to lose but that precedent matters, or just eat it? Of course, these customers challenging are never Grandma from Des Moines, but usually a "customer" account at Large Hedge Fund or Mega-Bucks Bank. They buy an option at the market on the open in something that just had earnings. ARCA is electronic, and they take whatever offer I'm sending. Being a good-little liquidity provider, I'm providing liquidity at the moment of the opening in an event-driven stock. 25 minutes later, the initial euphoria is over, volatility is in 50%, and the call they paid $2.50 for is now offered @$0.75. They call to bust the trade because the price is "obviously" an error. The cynic would say they are just taking a free look on the open, but I, of course, would never accuse LHF or MBB of such tactics. I did ask ARCA what they would do if I opened Free Look Trading, a division of Customer Capital…

Jan

31

Hero Trading, from Kim Zussman

January 31, 2008 | Leave a Comment

He hoped to be a hero

One day atop the hill

Surviving all the bullets

Expert at the kill

.

But then one day he noticed

How they all try and die

The sacrifice was futile

Objective was a lie

.

The experts at the killing

Drop them one and all

Friend, foe, and family

One by one they fall

.

Until the hill is barren

Adobe red with blood

The hero stands alone there

Above the boiling mud

.

The lady sits in waiting

A dark and empty home

Her face the mirror changing

Her hair pulled in the comb

.

Her gallant lads are fighting

A war without an end

Will it be reversing

Or is this now a trend

.

All the men who loved her

soldiers through and through

Killed in the great battle

Wet skin all grey and blue

.

He couldn't be a killer

And didn't run too fast

They noticed he was thinking

So saved his shot for last

.

His final thoughts ran from him

Fanning into space

The last thing he would ever see

Was her lovely face

Jan

30

Basketball and Markets, from Victor Niederhoffer

January 30, 2008 | 12 Comments

It's been a long time since I considered what we might learn from basketball . Like most former Knick fans, I was so turned off by the surly and ugly play of Patrick Ewing, including his bumping of teammates when they didn't give him the ball for the crucial shorts, his inability to get a rebound after a shot, and the depth from the basket he shot from , that when he didnt accept my proposal to trade places with "Doc Greenspan", I called it a day.

It's been a long time since I considered what we might learn from basketball . Like most former Knick fans, I was so turned off by the surly and ugly play of Patrick Ewing, including his bumping of teammates when they didn't give him the ball for the crucial shorts, his inability to get a rebound after a shot, and the depth from the basket he shot from , that when he didnt accept my proposal to trade places with "Doc Greenspan", I called it a day.

But I recently tuned in to a few Knick games to see the structure of what makes a team that bad, with their record 14 wins of 44, as if they're that bad you might learn from them in other fields. I found that there is a general air of malaise that surrounds the team. They like to come out to the scorer's table en masse as if for a gang rumble, and q loves to pick fights with people twice his size, the coach likes to bump referees, and if you beat them too bad they threaten you with a locker room brawl, to say nothing of the elbows. This general air of viciousness always leads to losses in basketball or markets.

The Knicks on paper, man for man are a good team. But as Clyde says, they pick the wrong time to take their shots. They fire from 100 feet out when the opposing team is sure to get the rebound, and the game is on the edge. They run around madly trying to find an isolated player from Downtown with no inside game. The movement to high risk trades to bail one out at the close is sure to lose.

There is no rudder to the team. The big men are fighting with each other and the coach. When Curry scores, he doesn't bother to go back to defend. They chew each other out in public with the coach shaming the players, and vice versa. A movement from one market to another, from day trading to long term, from big margin to low margin is sure to cause the same results as the Knicks.

The off court antics of the Knicks show that they are deeply disturbed. They seem to hang on to each other for fear that word about their shortcoming might lead to wholesale losses in litigation say in the harassment front. The fans are admonished to go crazy at the games, but when they berate the coach, they are thrown out. The inability to accept censure and to get feedback from what you're doing wrong is a sure sign of failure.

They use up their energy with fruitless movements and attempts to improvise plays while their opponents conserve theirs while waiting for the tried an true that is part of their game plan. Indeed, the Knicks seem to have no steady game plan, even to the point of not knowing who they are going to put in the game at any time. When they do score an unusual short, like Balkman's three against Los Angeles, they get so excited they use up all their energy in congratulating themselves. Anyone who talks about their great wins in speculation is like the Knicks and destined to fade like a shooting star.

The woe of the Knicks is typified by their captain. He's a man paid a few hundred thou a game, but after being out for 4/5 of the season, and paid, he's suing for the one game he didnt show up for after a heated converse with the coach where the coach may or may not have told him he didn't care if he showed up or some such. Like Ewing, the captain is an egomaniac, as typified by his remarks to the intern about whether or not she was going to go into the truck, immediately, and his wild shooting from outside with no rhyme or reason to it.

Any team that has a loose cannon like that for a captain who takes shots that are so non-percentage because they disrupt the flow of the whole team, is designed to slip into the nether world.

They have a tendency to fall apart at crucial moments which is typical of a team that has a flimsy foundation. Time and time again, they can bring the game close, but when the other team tried harder near the end, the Knicks fall apart and lose by a few points. The market that can't make it big by near the end of the period is likely to move the other way.

I don't know too much about basketball, never having been good at using the left of the jump, so I would appreciate more erudite analyses of the technical aspects of what's wrong with the Knicks and how it can teach us what not to do

Jan

29

Parasites, Markets and Host Behavior, from Victor Niederhoffer

January 29, 2008 | 8 Comments

The parasite T. Gondii lives in rats but must get transmitted to cats to complete its life cycle. It does this by changing the rat brain so that it seeks out cats. When the cat eats the rat, the parasite gets transmitted through droppings to other mice and humans. The incidence of schizophenia in humans is about 25% higher in those 7% of the human population that have contracted the parasite than the rest of the population.

This parasite and other parasites play a large role in determining the behavior of their hosts. For example the fluke d. dendriticum changes the behavior of ants so that instead of spending time in its nest, it climbs on top of a blade of grass, so that it will eaten by a grazing aminmal. Other flukes cause fish to jump up so that predators will eat them. And hairworms cause grasshopers to drown themelves, transmitting the worms through water as they die.

Parasites attack the body without the host knowing it, and the virulence of their attack is related to their method of transmission. Factors that determine their activity include their ability to reproduce, the mobility of their host, the costs of dying and the costs of sickness. In general, if the probability of transmission is high as it is in crowded conditions, for example in foxholes or planes, then then severity of the illness increases. Where the parasite needs a mobile host who sneezes, or has sex with induced increased frequency then the parasite becomes relatively mild in its impact, especially during the first stage of its impact, so that it has more time to reproduce and survive.

All this and much more is contained in the layman's book "Survival of the sickest" by Sharon Moalem. The basic thesis is that many diseases that we now have once served to help us survive when a short term solution like preventing freezing during an ice age or gaining energy during a famine were imperative. They served a function then, but now cause diseases like diabetes, Alzheimer, and cancer.

In looking at the recent disclosure of an 8 billion loss from a hidden agent in its Delta One unit, I found that the insights I gained from the study of infectious agents and their transmission method were very helpful. The agent was hidden in a hard to find part of the hosts structure, it stayed invisible for several years while it was acting with little impact, it acted mainly during the evenings, in anonymity, without alerting the immune system through margin calls, or seemingly unbalanced positions. Indeed, like many parasites, it had turned the host immune system against the host by copying the methods of healthy traders within the system. But most important of all, the parasite was finally expunged from the system, and this left the host, and the market it acted within in a much healthier state.

I would be interesting to consider what other parasites are acting upon the market system , and how they coevolve with their hosts.

Alston Mabry adds:

Attenborough's Trials of Life videotape series has incredible, and ghastly, footage of several of these parasites and their actions ontheir hosts.

Sushil Kedia writes in:

Separation of Corporate Management from Corporate Ownership that was hailed as a quantum progress in the management of businesses, heralding an era of objective decision making by profesisonal managers, has brought in its wake massive Agency Costs.

Regular earnings announcements every quarter were made mandatory to fulfill compliance with the agency relationship corporate managements have with the stakeholders. Over shorter periods the volatility in announcements is perhaps affecting the valuation of the stakeholders' equity.

Fundamental Valuation Research driven brokerage and investment banking services were initially celebrated to have brought greater professionalism to markets to only finally ending up in being forced to have Chinese Walls and arms length existence from their Research Divisions.

The Margining System when introduced to the Clearing Houses of Exchanges was a boon for their existence and sustenance. However, when catastrophic moves occur the Portfolio VaR shoots up because the benefit of diversification dwindles as asset correlations increase. The very same margins thus shoot up unexpectedly bringing down the trading & clearing system of exchanges.

Similarly, all of the risk management technology that has come up to manage risk within tolerable ranges ends up making it intolerable, even more so as risk goes out of the tolerable range.

Banks and Investment Banks were required to operate in different segments of financial services to keep the systemic risk under check. Finally, competition in risk taking brought about a necessity for banks and investment banks to be brought back into the same circle.

The Reflexivity perspective of markets itself is akin to a virus that was initially required for our progression but has started affecting the progression itself. Markets came into existence to help us allocate resources by anticipating future events. Now often times markets are shaping future events.

The law of Diminishing Utility of Returns itself operates as if there are viruses of the types Vic describes here, embedded within any pursuits inside the markets. A local maximum exists in the progression of each process in the market system. It is appealing to imagine that such viruses are perhaps Nature's way of making change the only permanent process.

Jan

29

Drug Research and Drug Stocks, From Bill Egan

January 29, 2008 | Leave a Comment

Gregg wrote a nice comment: "This NYT editorial story is not good for drug stocks which depend on revenues from cholesterol lowering drugs. That is good and bad. Good from a moral-philosophic point of view, bad for my portfolio."

Drug stocks will become much more volatile in the next 5 years. Many billion dollar patents are expiring and the pipelines are not there to replace them. Big pharma will downsize more and more in US/EU, and throw money at all biologicals as well as small molecules designed for cancer to fill pipelines, and shift research projects (and esp. regulatory testing) for small molecules to cheaper chemists in China/India. Why?

Labor costs. Wu Xi in China (WX on NYSE) a great example of the last. WX is also getting into cheaper regulatory/development testing. Many big pharmas opening R&D centers in China, too (Shanghai). Biologics are harder to make but easier to develop (usually less toxic). Small molecules for cancer are more likely to get approved. Big pharma has made billions on small molecule drugs for chronic conditions. Double whammy here - a) many good drugs coming off patent for those conditions, so unless the new drug is much superior, it has no chance cost-wise, b) FDA is now much tougher on the safety of drugs for chronic conditions, especially if the condition is not life-threatening. Cancer is still hard to treat and life-threatening.

VCs seem to be putting less money into traditional US small molecule startups. If I were a VC, I would move money to China/India, but also look for plays for pipeline fillers. Big pharma execs have to be seen "doing something" or lose their jobs.

Their real problem is the length of the R&D cycle. Research averages 5 years, clinical testing in humans averages 7 years, and FDA approval time is ~14 months. So 13 year cycle.

Fail rates are huge. Take 10 research projects. Each makes 2,000 molecules on average to produce a clinical candidate (drug to test in man). One of those ten projects will produce a drug. So about 1 in 20,000 molecules becomes a drug after 13 years. Why the fail rate is so huge is another essay.

Consequences are that big pharma execs reorganize alot and buy pipeline fillers while cutting costs and praying the pipeline gets better randomly (and they fire the research head, too). Changes made back in research may or may not affects the success rates. Doesn't matter much, either, from the CEO viewpoint. Even if a research process change/new technology tripled the success rate, you couldn't tell easily. 3x better means 1 in 6,667 molecules succeeding after 13 years… So big pharma execs "do something now" even if it has little chance of fundamentally changing the odds in order to save their own necks. Likely more shenanigans like hiding of bad data on Vioxx and new Vytorin ethics scandal.

This means lots of volatility. The problem is the high fail rates mean it is tough to tell which small companies are any good. Interesting times ahead.

Jan

29

Pulling Money from the Pit, from Jeff Watson

January 29, 2008 | 3 Comments

Having spent a considerable amount of time trading in the pit, I came up with many methods to wring out a little extra money, which meant the difference between winning and losing on many days. I earlier recounted the method of finding a loser and fading his trades. That was a great way to make a net average profit. I also alluded to mechanical methods that I used to make money. All of these methods required strict concentration and quick thinking.

Pit brokers are only human, and most of them are just tradesmen. When a pit broker would get an order, I'd carefully watch which direction his eyes moved as he read the order. As all paper orders were made in the same format, one could see if it was a buy or sell just by his eye movement. If he had a buy order, I'd bid at the market price, maybe even bid it up a quarter cent, just to see what he'd do. If he bid the price up in front of me, I'd turn around and sell him the wheat. I'd then offer wheat at that price, sometimes a pr etty large amount, just to try to get some more locals to offer it down a quarter cent, in which I'd buy it back. If the broker didn't do anything with the paper, I'd usually assume that it was a limit order, and was usually right. This was a good piece of information, as I knew that there would be a price where I could pitch out wheat at a certain price after he put the order in his deck. I'd memorize those price points with as many of the brokers as I could, and this greatly lowered my risk.

I learned the individual methods of brokers, such as the brokers that worked for hedging companies. As they were usually sellers, I would try to entice them to sell by offering in front of them in order to move the market. Many of those hedging brokers used to like to sell at 10 cent intervals, and I found that there would sometimes be selling pressure at the dime which was very useful. Back then, I found that there were many brokers that would just let us have the wheat at whatever pr ice we wanted…all they wanted to do was to fill the order, and they didn't really care at what price they filled it. I treated these guys like gold, sometimes giving them trades in distant months, just so they could fill the order. Of course, I'd immediately spread that month, and try to work it out later. All in all, I was a net loser on those trades, but considered it to be a cost of doing business. Some brokers wanted all of the money for themselves, and were very tight. I tried to avoid them like the plague. The brokers that represented the big commercials were very useful, as if you could figure what was in their deck, you could see what they were doing, and at what price. The big commercials did volume, and knowing what and where their order flow was going allowed me to put on sizable scalps with a good guesstimate as to where I could exit the trade, which would also limit risk. During my tenure in the pit, I learned how to read upside down, and to also read the writing through the orders if the light conditions were good. I used to watch brokers put unfilled orders in their decks, and if I had an idea of what price was on the order, and if it was a buy or sell, I could figure out their hand like a good gin rummy player does.

Some brokers were very careless with their order decks, and would accidentally flash their order, much like a careless poker player accidentally flashes his cards. I found it advantageous to sometimes stand behind careless brokers, peeking over their shoulder. I learned to watch what all the players were doing, especially if the big commercials were trying to move a spread. They'd battle it out, and I'd pick up the scraps, some of which were pretty tasty. I had to learn the art of deception as a lot of locals would try to follow me. Sometimes, I had to put on positions through other brokers to disguise my intentions and strategy. In quiet times, if Chicago started moving a couple of cents, I'd sometimes try to fake a rally just to get people sucked in. Unfortunately for me, sometimes I'd start to believe the rally I faked was for real. That would cost me money in the long run. I found a real good indicator for market opens. If the market was poised to open higher, people would get into the pit 5-10 minutes early, whereas a lackluster or down opening would find people arriving at the pit at the last minute.

Unfortunately, as the electronic markets replace the pits, all of these mechanical techniques will be destined to the dustbin of history. I personally feel bad about the impending demise of the open outcry method, and often wonder what will happen to the electronic markets if there's ever a big internet shutdown.

Jan

29

Numerology, from Ken Smith

January 29, 2008 | Leave a Comment

With Biblical numerology 911 is a curious date.

The number of the Beast is crucial — 666:

Jan

29

A Brief History of Recession Time, From Stefan Jovanovich

January 29, 2008 | Leave a Comment

The first recession I remember was the one that came shortly after Dad had his first heart attack during Eisenhower's second term. Although it was relatively short, it was pretty severe. I remember several of my friends' fathers losing their jobs in the New York printing trade, which slumped badly and never really recovered.

There have been 7 more recessions since then (not counting the one which may or may not be officially happening now). The median decline in real GDP for the 8 slumps has been 1.91%; their average duration has been 10 1/2 months.

Aug.1957 - Apr. 1958 8 months -3.75%

Apr. 1960 - Feb. 1961 10 months -1.64%

Dec. 1969 - Nov. 1970 11 months -0.64%

Nov. 1973 - Mar 1975 16 months -3.10%

Jan 1980 - Jul 1980 6 months -2.18%

Jul 1981 - Nov 1982 16 months -2.87%

Jul 1990 - Mar 1991 8 months -1.26%

Mar 2001 - Nov 2001 8 months -0.17%

Jan

26

Bear Market? from Victor Niederhoffer

January 26, 2008 | 24 Comments

There has been much talk recently about the many bear markets that have been achieved. The way it's usually defined is that a market has declined 20% from a recent peak. There are many ways of quantifying that, but let's say the definition is that the current month's close is less than a monthly close in the last five years by more than 20%, and is also not more than 10% above a close preceding it in the last five years by 10%.

There has been much talk recently about the many bear markets that have been achieved. The way it's usually defined is that a market has declined 20% from a recent peak. There are many ways of quantifying that, but let's say the definition is that the current month's close is less than a monthly close in the last five years by more than 20%, and is also not more than 10% above a close preceding it in the last five years by 10%.

In November 1968 the S&P 500 closed at 108 and in January 1970 it closed at 85. Subsequently the S&P 500 rose, to 118 on December 1972, then fell continously to 64 in September 1974. It then rose continously to 1400 in December 1999 and then fell to 815 in September 2002.

During 1929 the market rose to 31 in August, then fell to 4.8 in June 1932. In June of 1921 there was a 40% drom from tge high of 10.2 in 1916. Those are the only major drops.

There are many questions. There were three declines of more than 40%. Were these offset by the many drops of 20% that bounced back? Have conditions changed since 1929 when the market dropped by 83%? What would proper exit and entry points be? What happens when the market drops by 20% within various periods? How does the interest rate environment affect it? Have declines associated with big drops in real estate been any different? is there such a thing as a bear market?

Rudolf Hauser adds:

I have always looked at the bear markets that ended in 1970 and 1974 as two distinct bear markets. What characterized both the major periods of down markets in the 1930s and 1970s were inappropriate monetary and other government policies. This is what appears to turn modest periods of market and economic setback into major ones. In the 1930s monetary policy was too restrictive and other government policies were also the absolute wrong way to go. Because these mistakes were on the downside of economic policy decision making, I have tended to view that as one protracted bear market interrupted by a rally. Following the 1970 episode the Fed was much too expansive, which compounded the underlying inflation problem. That in turn led to the 1973-1974 debacle and subsequent ones until this stop-go policy finally ended under Volcker and Reagan. The lesson seems to be that market downturns caused either by market (not just equity markets) imbalances and/or mistaken government policies may remain moderate unless further government mistakes in reacting to the events are badly mistaken ones. One just has to hope that the government and central bank have learned from past mistakes and do not stumble into some new variation of mistaken policies. If they can do that the prospects for the equity markets are much better. The low probability major downside risk I see here is the whole structure of derivatives and other new products that spread out risk to those willing to bear it. The problem comes if enough of those ultimate risk takers are not able to bear it and take down those who lent to them and those who were counting on their ability to pay up when the time comes. If this goes into major financial institutions that are not just short of liquidity but suffering from major negative equity positions that cannot be baled out without special government legislation, we could have a new version of mistake — one that perhaps cannot be blamed on government actions as opposed to inaction, unless one wants to place the blame on monetary policy that too expansive in the past for asset markets.

I have always looked at the bear markets that ended in 1970 and 1974 as two distinct bear markets. What characterized both the major periods of down markets in the 1930s and 1970s were inappropriate monetary and other government policies. This is what appears to turn modest periods of market and economic setback into major ones. In the 1930s monetary policy was too restrictive and other government policies were also the absolute wrong way to go. Because these mistakes were on the downside of economic policy decision making, I have tended to view that as one protracted bear market interrupted by a rally. Following the 1970 episode the Fed was much too expansive, which compounded the underlying inflation problem. That in turn led to the 1973-1974 debacle and subsequent ones until this stop-go policy finally ended under Volcker and Reagan. The lesson seems to be that market downturns caused either by market (not just equity markets) imbalances and/or mistaken government policies may remain moderate unless further government mistakes in reacting to the events are badly mistaken ones. One just has to hope that the government and central bank have learned from past mistakes and do not stumble into some new variation of mistaken policies. If they can do that the prospects for the equity markets are much better. The low probability major downside risk I see here is the whole structure of derivatives and other new products that spread out risk to those willing to bear it. The problem comes if enough of those ultimate risk takers are not able to bear it and take down those who lent to them and those who were counting on their ability to pay up when the time comes. If this goes into major financial institutions that are not just short of liquidity but suffering from major negative equity positions that cannot be baled out without special government legislation, we could have a new version of mistake — one that perhaps cannot be blamed on government actions as opposed to inaction, unless one wants to place the blame on monetary policy that too expansive in the past for asset markets.

Jim Sogi remarks:

There are many ways of quantifying a bear market.

There are many ways of quantifying a bear market.

For the sake of argument, let's call it a one or more down months. Looking at Dow monthly from 2/1945 to 11/2006, 309 months were down and 424 were up.

If we say two or more down months in a row is a bear market then we have the following count of consecutive up and down months. Under this definition we are 40% of the time in a bear market. Three down months are close to 40%.

Months in a row, down, up

2 39 50 3 21 32 4 4 11 5 2 3 6 4 6

If we look at first 360 months the situation is much darker with close to 50% of the time in a down market.

2 20 20 3 11 17 4 2 6 5 2 0 6 2 3 7 0 1 8 0 1 11 0 1 12 0 1

The last half is brighter, but there are a number of downdrafts.

2 19 30 3 10 15 4 2 5 5 0 3 6 2 3 7 0 1 8 0 1

So yes, there are bear markets. Lots of them.

As to magnitude: mean down month is -80.8, mean up is +84.2

This shows the drift, but also that the downs months can be bad. This study highlights the skew in the data.

Jan

26

Good as Gold, from Pitt T. Maner III

January 26, 2008 | 3 Comments

One of the best gold stories from the 1970s was when Arthur Ashe beat 19 year old Bjorn Borg in the WCT tournament in Dallas and won a solid gold tennis ball worth $33,000. Ashe kept it and it wasn't too long before gold was selling around $800 dollars an ounce and the ball was worth close to 1 million dollars.

One of the best gold stories from the 1970s was when Arthur Ashe beat 19 year old Bjorn Borg in the WCT tournament in Dallas and won a solid gold tennis ball worth $33,000. Ashe kept it and it wasn't too long before gold was selling around $800 dollars an ounce and the ball was worth close to 1 million dollars.

Jeff Watson reminisces:

I bought a lot of physical gold back in 1979-80 and my position has been underwater ever since. My gold-bug friend told me that I'm finally making money in the gold market, as it's taken out its old highs. I explained to him that with inflation, storage and cost of carry, I'd never get out from being underwater. Luckily, I still find looking at and feeling the actual gold to be rather invigorating.

Alan Millhone agrees:

Yep, nothing like feeling the heft of a roll of Maple Leafs in ones hand.. I knew an old barber years ago from Middleport, Ohio who went West every year to prospect on his vacation and made enough each trip to pay for his expenses and his vacation. He was a coin collector as well and he is long gone, as is his fine collection.

Jan

25

Market Moves, from Jim Sogi

January 25, 2008 | 6 Comments

I remember the 1960s through the 1970s (Chart). There were 50% price swings. Though I cannot test it, I hypothesize the recent 20 year sample won't be predictive in that 1960s out sample. In the 1970s and early 1980s apparently simple trend following strategies worked, but in the last several years such tactics have not worked. Successful trend followers became extinct. But today we are seeing 20% trend moves which might be defined as multiple 100 point moves without an equal bounce. Bollinger wondered whether old things might have their comeback. I do too. To quantify this, we have had a 200 points down with no 100 point bounce. In 2001-2002 there were several 300 point down moves without a bounce.

I remember the 1960s through the 1970s (Chart). There were 50% price swings. Though I cannot test it, I hypothesize the recent 20 year sample won't be predictive in that 1960s out sample. In the 1970s and early 1980s apparently simple trend following strategies worked, but in the last several years such tactics have not worked. Successful trend followers became extinct. But today we are seeing 20% trend moves which might be defined as multiple 100 point moves without an equal bounce. Bollinger wondered whether old things might have their comeback. I do too. To quantify this, we have had a 200 points down with no 100 point bounce. In 2001-2002 there were several 300 point down moves without a bounce.

In 2000 and 2001 mechanical day trading tactics worked. Strategies such as trailing stops, breakout/down buy/sell stops, buy prior x bar high breakouts, pyramiding etc. These have not worked well the last five years. Also note that ranges, gaps, absolute volatility are all non-significant for 15 years data. Today entries and exits almost had to have been at market to get in or out in time. There were no retracements on the runs up or or down runs. Today's 68 point bounce was the biggest up move open to close since 1994.

Referring back to our discussion of stop/no stop/leverage tactics, the no-stop method does not work well in a trending situation and one trend, whether random or not can hurt a no-stop leveraged account. Larry Williams is right on this. No stops may have been right before, but things have changed, again.

The non-significance of current moves indicates climatic changes. Only adaptability will prevent extinction. In evolution theory, fixed or slow moving characteristics or non-adapters were wiped out when climates or conditions changed rapidly. Even the mighty dinosaurs disappeared after ruling the earth for hundreds of millions of years. The question is, are the data becoming stale? Hurricanes build when energy is released. All this stimulus is going to keep these storms going strong. What about a 50% trading range like the 1960s-1980s? There were weird government maneuvers going on then too, price controls, the dollar off the gold standard, Vietnam, Savings and Loans, inflation pre-Volcker, assassination of presidents, impeachment, war, race riots. All very weird. I remember getting out of investments in October 2001 after some stiff losses thinking, things are changing. Glad I did. It saved me.

The non-significance of current moves indicates climatic changes. Only adaptability will prevent extinction. In evolution theory, fixed or slow moving characteristics or non-adapters were wiped out when climates or conditions changed rapidly. Even the mighty dinosaurs disappeared after ruling the earth for hundreds of millions of years. The question is, are the data becoming stale? Hurricanes build when energy is released. All this stimulus is going to keep these storms going strong. What about a 50% trading range like the 1960s-1980s? There were weird government maneuvers going on then too, price controls, the dollar off the gold standard, Vietnam, Savings and Loans, inflation pre-Volcker, assassination of presidents, impeachment, war, race riots. All very weird. I remember getting out of investments in October 2001 after some stiff losses thinking, things are changing. Glad I did. It saved me.

Paolo Pezzutti adds:

The market will come back eventually.

What is amazing is how quickly you can give back your hard gained money. Especially, what happens to small traders is that even if you do recognize situations like this one as buying opportunities you are under capitalized to enter the market. You are caught by surprise, when you consider selling it is too late, your gains have already gone, you decide to hold because it will go back up, but you are unable to profit from the "On Sale!" prices. You cannot participate in the party and you get only the crumbs. End of story.

When trading short-term you do not have these problems, you are in and out often, but the small trader, part time trader is not consistent, does not have time, has high commissions, may have a not-perfectly-tuned strategy and the results most of the times are at best underperforming.

In all these years, I have learned that when volatility is above a certain level, I have to stay out. One loss can be so big as to eat all the profits I made in two months. Normally volatility does not increase so abruptly that you cannot tell that the environment has changed.

Jan

25

Market Moves II, from Vince Fulco

January 25, 2008 | 1 Comment

Speaking of rarities, one of the issues I have been grappling with as the market decline continued is that this period reminds me of a combo of the 1989-1990 junk bond debacle and the Oct 2002 US accounting "crisis"; current conditions are worse than in the former case and better than in the latter. Mix them together and what do you have? I continue to search for the answer daily.

On the one hand, as the bond insurers are impacted by downgrades and fears of possible bankruptcy, billions and billions of previously AAA rated securities (thanks to bond insurance) now have to stand on their own merits. Who is to say what the average rating of many of these instruments is, BBB, BB? By default (no pun intended), the removal of insurance or ratings causes forced liquidations by parties which can only hold the highest rated paper. Given all the structured product created in say the last 3-5 years, where is the home for all this paper? It was one thing when the S and L's of old held Milken's junk and had to sell it without regard to price: there were adequately capitalized parties which could absorb the inventory with the proper markdowns. Will the newly downgraded structured products overwhelm even the vulture funds and opportunistic hedge funds' ability to buy? And are we seeing equities decline because the competition for return is swinging to the newly created fixed income opportunities with better implied ROR? I'm told plain vanilla junk is now trading around +1100 from +400 to +600 in the last few years; historically wide by most accounts but not at max spread to previous distress periods.

What reminds me of the accounting crisis period is the disgorging of US equities in buckets as we've witnessed the last few weeks; very little discernment of company by company fundamentals. I can remember at my old fund, in the height of the accounting debacle, seeing Kroger (KR) among many, many others, drift down from 23 to 15 in a matter of days and within 1 day trade "in the hole" to 10.75 briefly. Within 8 hours the stock was back to 14.50 and proceeded to drift back up to the low 20s within a few months. I mention this as an example because as I recall this was a single A issuer with NO accounting issues whatsoever, recession proof and a steady income stream trading at 5 to 7x EBITDA depending on where you marked it. I can look back and point to example after example of similar situations in that period. I'm sure many others can mention a laundry list of current stocks which should not be impacted by bond market turmoil other than that the equity risk premium is increasing "because it is". Aside from the realization that US and global GDP are slowing rapidly, these are some of the other ingredients for this manic depressive market.

I remain optimistic especially after the severe markdown we've had but the unique qualities of this period do give me pause. Would welcome any comments.

Jan

25

Complex Numbers, Risk Management and Poison, from Russ Sears

January 25, 2008 | 1 Comment

The fundamental theory of asset allocation/ risk management is that diversification (increasing the number of assets invested in) decreases the total risk. The amount of the decrease is generally reckoned solely based on the correlation of the new asset to the total portfolio and the weight given to the new asset. The specific risk is assumed to go to zero as you increase the assets.

However, what if the asset added is poison… such as subprime? What happens is risk is raised not lowered no matter how small the amount added. Its total negative risk. or: The vol rather than lowering is raised, or the square root of -1 cancels the negative to positive.

Likewise for time, in most instances Vol(2t) = 2^1/2 x Vol(t). It is less than 2 X Vol(t) since the autocorrelation is assumed zero.

But what if the vol of one of the time periods is poison, such as on Rogue MLK Monday. The Vol adds to, not decreases, proportionally to time.

I will leave it to the reader to deduce what determines a "poison" time period and asset class… but I would suggest fraud seems to me to be the reoccuring theme, in both my examples.

Jan

25

Sleeping, Dreaming and Trading, from Riz Din

January 25, 2008 | Leave a Comment

If anyone is passing through London over the coming weeks, I urge a visit to the 'Sleep & Dreaming' exhibition by the Wellcome Trust , just outside Euston Station. The exhibition looks at our understanding of sleeping and dreaming through the ages from a scientific, social, and artistic perspective, and as with many of the museums and galleries in London, admission is free.

Here are some take-aways from my visit:

- Doing without sleep: In 1959, radio DJ Peter Tripp managed to go 201 hours without sleep. However, Tripp suffered from hallucinations and paranoia, and perhaps even brain damage as a result. The record was beaten in 1963-64 by Randy Gardner, who went a full 11 days without sleep and had no lasting side effects. I've read that this record was since beaten by Tony Wright from the UK in 2007 and that David Blaine is also planning to break the record as his next feat of endurance.

- There exists a rare genetic condition called fatal familial insomnia, in which the patient develops incurable insomnia usually in their middle age and dies as a result.

- Drivers of vehicles often suffer from microsleep, when they dose off for a few seconds at the wheel or start day dreaming. Car manufacturers are working on technologies that monitor blink patterns and alert drivers when they are too tired. I imagine such a technology would be useful to day traders working double shifts.

- On dreaming: We dream while we are sleeping, not only during the rapid-eye-movement stage of sleep (there are five stages of sleep and the whole sleep cycle lasts about ninety minutes before repeating). Listening to audio tapes while sleeping does not appear to be effective but sleeping and dreaming seems to play a crucial role in the formation of the days memories and knowledge: an experiment was conducted on rats whereby the rats were placed in a maze and their brain activity monitored as they worked their way around. It was found that the same parts of the rats brains kept firing away while they were asleep, supporting the idea that 'sleeping on it' really helps. Human studies have had similar results, supporting the idea that sleep is a kind of revision. Some suggest that the days knowledge not only gets remembered but that it consolidates with other knowledge. For traders, this could be particularly important. Indeed, with the market see-sawing all over the place I imagine many traders view sleep time as 'dead time' when they could be doing something productive. as for me, I'm off to sleep.

Jan

25

Predator vs. Prey, from Greg Calvin

January 25, 2008 | 1 Comment

An observation from watching the Kruger Battle is the difference in speed and resolve of predators vs prey. The lions, and the alligator for that matter, move in fast for the kill. The predators may wait hours or days, but when attack is decided upon, it happens in the blink of an eye.

Note in contrast the fits and sputtering attempts of the herd to defend its offspring. Even the largest bulls are hesitant and fearful initially to confront the predators, but only lunge in here and there, risking life it seems when fully engaging a lion with physical contact, as the vulnerable head and neck of the bull are in such close proximity to those deadly horns. The defense of the calf takes time, as the courage of individual bulls emboldens others, and the lions one by one get the message.

Movie Fan reminisces:

From Jaws:

"Quint: Y'all know me. Know how I earn a livin'. I'll catch this bird for you, but it ain't gonna be easy. Bad fish. Not like going down to the pond and chasing bluegills and tommycocks. This shark, swallow you whole. No shakin', no tenderizin', down you go. And we gotta do it quick, that'll bring back your tourists, put all your businesses on a payin' basis. But it's not gonna be pleasant. I value my neck a lot more than three thousand bucks, chief. I'll find him for three, but I'll catch him, and kill him, for ten. But you've gotta make up your minds. If you want to stay alive, then ante up. If you want to play it cheap, be on welfare the whole winter. I don't want no volunteers, I don't want no mates, there's too many captains on this island. Ten thousand dollars for me by myself. For that you get the head, the tail, the whole damn thing. "

Jan

25

Another Rant, from James Lackey

January 25, 2008 | 1 Comment

One good up day… One reversal day… One "good date" night and an "O" sure does not make up for all the reprehensible behavior in the markets… Price fixing, rigged deals… Fed emergency rate cuts… It does remind me of all of the old books about 19th century financial markets…

Hey, on Monday night let's say 3am when we were limit down… who do you think was in there buying? Yes and .25 off the limit I am sitting there long too much, thinking am I really this nuts to hope or think we really are going to get an emergency Fed cut? What the hell kinda trader is that?

No that is not why I bought… But why I sold… I had no idea how much lower it would have gone once the limit came off later in the day, maybe not much at all, 10 SNP points for a joke on the Stop Boys. Yet, what I do know is we all should have had that opportunity to find out… the limit down deprived us of that.

If it falls below 1255.30 later this year… every point it does falls below, all the pain you take, blame the Feds for the bailouts, not me. If they let it fall this time, the next time we start buying before the old low and "hope" for a panic or a new low to buy more from the stops. No, next time down I'll be there commenting… "where is your bailout now. Don't ask the traders for help."

It wasn't this time that upset me so much… Hades we are down 20% in a few weeks. I am long anyways. Yet for the past many months how many stupid plans and bailouts have we had? You all know damn well years from now we are all going to look back and say, that wasn't good.

TODAY: MBIA, Ambac Likely to Get Bailout, UniCredit Says

MBIA Inc. and Ambac Financial Group Inc., the biggest bond insurers, are likely to be bailed out to avert worsening credit-market turmoil, according to analysts at UniCredit SpA.

AIG Bails Out $2.2 Billion Nightingale Finance SIV

American International Group Inc., the world's biggest insurer by assets, will bail out its Nightingale Finance structured investment vehicle, according to Moody's Investors Service.

Bank of America Plans $6 Billion Preferred Offering

Fed 75BPS Emergency rate cut more to come next week (yea, right!) Bernanke to Cut Rates Further, Faster to Buoy Growth

Citigroup Trial May Double Enron Creditors' Payout

Don't forget the 150-200 billion stimulus package!

And don't forget the treasury department Super SIV.

And Subprime mortgage reform and price fixing!

Jan

23

The Bulls and the Bears, from Craig Mee

January 23, 2008 | 5 Comments

I get the feeling on days like we have seen recently, that it is a total battle between the bulls and the bears, ie who is going to win on the day, with this being signified by being on the positive side of unchanged or the negative side at the close. Coming back from a strong deficit will not be seen as win for the bulls unless they make it over the line- and vice versa. The acceleration of the market into unchanged and away from unchanged throughout the sessions is brutal on the turn.

Vince Fulco ponders:

One wonders what the approximate level of blended Treasury rate is that is low enough to bring out the asset re(allocators). I don't think pension funds can meet long term liabilities with a 3.45% ten year!

Jan

22

The Battle of Ramree Island, from James Bitumen

January 22, 2008 | 16 Comments

Today is one of those tremendous days in the market that reminds me of the Battle of Ramree Island that took place in Burma between January and February of 1945.

Today is one of those tremendous days in the market that reminds me of the Battle of Ramree Island that took place in Burma between January and February of 1945.

I have not seen a first half of month decline in the market this severe for many years. Vic and Laurel have frequently discussed symmetry and V-shaped recoveries, and I'd add that I have never seen an earnings season beginning with a decline that has not been met with a sharp recovery.

The above picture shows what the shorts, like the fighters at Ramree Island, are going to face very soon.

Caroline Valetkevitch notices:

NEW YORK (January 23, 2007. Reuters) - The Dow and the S&P 500 rose late on Wednesday, rebounding from earlier losses of more than 2 percent each, as investors bought back shares they had bet against and the banking sector gained. "It looks like it's short-covering and also all financials are really, really running right now," said Todd Clark, managing director of stock trading at Nollenberger Capital Partners in San Francisco.

Jan

21

Leather Jacket, from Ken Smith

January 21, 2008 | Leave a Comment

Bo Keely wrote me once when I made a comment about an expensive leather jacket that I intended to wear to my trip to his little village in the desert. Keely admonished me, saying upscale dress was a good way to get mugged when traveling.

Bo Keely wrote me once when I made a comment about an expensive leather jacket that I intended to wear to my trip to his little village in the desert. Keely admonished me, saying upscale dress was a good way to get mugged when traveling.

Of course if you are traveling first class, staying in five-star hotels, using limos to shuttle between airport and hotel, taxi to shuttle from event to event, then the journey is safe. But I can't travel first class, I stay in motels not hotels, I walk around to avoid taxi charges, I use public transportation systems.

So I took Keely's advice — put the leather jacket back on the closet hanger. I have two fine leather jackets — except one is pigskin, made in China. I do not like pig, did not think of what animal the jacket skin might be when I bought it on sale — just thought of the price, was a steal; except it is pig.

The other jacket is tailored, fits like an Eisenhower. Maybe off a Kentucky Derby animal. Bought it at Nordstrom 30 years ago and it's a grand style to wear. Only thing about it is I wore it to an AA meeting once and a recovering female alcoholic commented "Jesus, we don't need another leather jacket in this group." I guess she was making a statement about gay dress, seeing the style for gays at that time was to dress in leather.

Steve Leslie remarks:

In the movie American Gangster there is a scene where Denzel Washington, who plays the gangster Frank Lucas, wears a mink coat with a mink hat to Madison Square Garden for a heavyweight boxing match. Detective Richie Roberts, played by Russell Crowe, takes pictures of people in the front rows around the ring. This helps Crowe in identifying Denzel as the drug kingpin that he is looking for. Up to this point, Denzel had always kept a low profile, thus allowing him to fly beneath the radar of the police. This one gaffe ultimately leads to a subsequent investigation, arrest and conviction.

Riz Din adds:

In addition to its functional role, clothing clearly acts as a signaling mechanism. Another place where it is may be better to dress down is when taking one's car to the garage for repairs; dressing smartly signals a wealthy person who probably doesn't know his manifold sprocket from his flux capacitor.

Bruno Ombreux extends:

This is a very European attitude. In France, there is a saying: "pour vivre heureux, vivons cachés." That is: to live happily, live stealthly. I had a great aunt which had a lot of money. She dressed so poorly that one day she went to place Vendôme to one of those luxury jewelers with the intention of buying some trinkets. She was denied entrance by the bouncer: "Sorry Madam, we don't think you can afford the merchandise in this place".

In England, really old blue-blooded money consider it a lack of taste to display wealth. They'll go as far as having domestics wear their new clothes so that the clothes acquire quickly the aged patina that makes them wearable to the wealthy.

Jan

20

Two Thumbs Down, from Scott Brooks

January 20, 2008 | 1 Comment

I watched a couple of movies last week up at the farm. Since I was alone for a couple of days, I decided to rent some movies that my wife wouldn't want to watch, but that were also off the beaten path of mainstream video fare.

I watched a couple of movies last week up at the farm. Since I was alone for a couple of days, I decided to rent some movies that my wife wouldn't want to watch, but that were also off the beaten path of mainstream video fare.

The first movie was Shoot'em Up starring Clive Owen and Paul Giamatti. I had not heard of this movie prior to seeing it on the shelf, but I have enjoyed both Owen and Giamatti in the past and decided to take a flyer on it.

It wasted no time jumping into action. And it was constant action from the moment it started till the moment it ended. The plot was completely beyond belief, the actors were endowed with superhuman capabilities, performing feats of strength that defied the laws of physic. The s-xuality of the movie was so overdone as to make it nearly soft-psychological porn. The gore and violence factor was a high 10.

But the premise of the plot was utterly and completely awful, mixed with a message that guns are bad and guns do bad things and people that make guns are bad people only out for blood.

This movie looks like it was torn from the pages of a comic book directed towards s-xually frustrated adolescent losers who probably fit the profile of growing up to be a serial killer living in mom's basement.

There was not a single redeeming quality to this movie. It was completely and utterly without any redeeming value. A complete and total waste of 90 minutes.

The second movie that I rented was Tracks . The premise is that a group of friends who drink too much, smoke too much dope, live on the fringes of society in their lower class neighborhood and suffer from more than their fair share of teenage angst are bored one day, and flip the switching mechanism on a commuter train track in NJ. The result is a train wreck that kills the conductor. The boys are sentenced as adults and sent to prison.

The second movie that I rented was Tracks . The premise is that a group of friends who drink too much, smoke too much dope, live on the fringes of society in their lower class neighborhood and suffer from more than their fair share of teenage angst are bored one day, and flip the switching mechanism on a commuter train track in NJ. The result is a train wreck that kills the conductor. The boys are sentenced as adults and sent to prison.

The focus of the movie is one young man and what he goes through. There are flashbacks to his troubled past, as well as glimpses here and there into his life outside of prison. The main focus is time in prison and its trials and tribulations. He tries to push away those that love him. Why these people love him (except his mother) is not made clear. He's a loser, a troubled young man, with a history of violence and a bad attitude and is disrespectful to most around him. He goes through some difficult times in prison, as would be expected of a 17 year old boy in adult prison. He makes friends with one guard (played by Ice-T), who gives him some guidance. But Ice-T is a painfully bad actor and his plastic strained performance in the flick further cements his inability to act.

The young man finally achieves parole and ends up in a halfway house for a short stay, only to end up back in prison after earning his first day pass and failing to follow the very simple rules (call to check in every hour).

The plotline surronding this young man is very conflicted, as if the director couldn't decide if he wanted to portray this young man in a sympathetic light or as the troubled hoodlum moron that he ended up coming across as.

In one scene he's portrayed as a smart kid helping the prison guard (Ice-T) with his junior-college homework. In the next scene, we see the young man behaving like a total and complete loser making absoutely awful decisions, the kind of bad decisions that make you feel no sense of compassion for him.

The ending of the movie was extremely disappointing and left me hanging. Now, don't get me wrong, I don't expect every movie to end like a nice neat package all wrapped up. But this movie just ended. It left me completely hanging.

I found myself just not caring about the main character. He was a real loser with real problems and there was nothing about him to like. I didn't hate him. I didn't like him. I simply didn't care! He had no redeeming qualities and I was never able to connect with him . Maybe it's because I knew too many guys like him in my youth and I know how the vast majority of them turned out (most are still losers and the ones that aren't are most likely dead). Regardless, this movie left me with a void.

I can't say anything nice about the movie. The bad stuff I could say is pretty run of the mill. It was bad, but not awful (Shoot'em Up was utterly awful). This movie left me feeling like I wasted 90 minutes. I didn't gain a thing from watching, but most importantly, it was simply was not an entertaining movie.

Tracks is chooked full of violence, nudity, s-xual content, and vulgar language. Don't waste your time with this one, either.

Jan

20

Diversity, from Stefan Jovanovich

January 20, 2008 | 1 Comment

During the run-up to a crash, population diversity falls. Agents begin to use very similar trading strategies as their common good performance begins to self-reinforce. This makes the population very brittle, in that a small reduction in the demand for shares could have a strong destabilizing impact on the market. The economic mechanism here is clear. Traders have a hard time finding anyone to sell to in a falling market since everyone else is following very similar strategies. In the Walrasian setup used here, this forces the price to drop by a large magnitude to clear the market. The population homogeneity translates into a reduction in market liquidity.

– Blake LeBaron, "Financial Market Efficiency in a Coevolutionary Environment," Proceedings of the Workshop on Simulation of Social Agents: Architectures and Institutions, Argonne National Laboratory and University of Chicago, October 2000, Argonne 2001, 50.

Riz Din remarks:

Reminds me of the extreme robustness of the naturally diverse rainforest, and of how relatively small changes can destroy single crop plantations.

George Parkanyi writes:

I'm not so sure that's as true anymore. There are many new instruments such as commodity and short ETFs that create more possibilities for risk mitigation and alternative strategies. Perfect opposite correlation is an asset-allocator's dream. I would think most trading volume comes from mutual and pension funds. If they change their charters, or simply interpret short ETFs to be another asset class, then the herd mentality may dissipate somewhat as there is now less reason to sell in a panic. Hedge funds and individual investors already have the bi-directional option available to them. For example, I recently used short ETFs to blunt the decline of the past couple of weeks. I felt less pressure to sell my stocks that did go down — in fact I bought more — because I had money working in the other direction. I'm theorizing that markets will tend to become more choppy and less smoothly trending, even in a broad decline, for this reason.

Jan

20

Risk Control in Trading, from Kim Zussman

January 20, 2008 | 5 Comments

In light of current market behaviour, what are some ideas on risk control? Someone is going to say Optimal F, or related, but here I was more thinking about what you do when flying by the seat of pants as always.

You can reduce risk by:

1. Staying out of market more (always?)

2. Setting stops (which get triggered right before huge rallies and increase probability of losses)

3. Trading small (too small to ever recoup losses)

4. Staying in only for prescribed short intervals (ensuring the miss of the rally a day later)

Ken Smith replies:

I once concluded I should take the first option suggested by Dr. Zussman: stay out.

I once concluded I should take the first option suggested by Dr. Zussman: stay out.

My idea was if I cannot predict then do not trade. But I often fool myself, thinking myself a magician, prognosticator of great moment. Under the sway of this illusion/delusion, I do not stay out and frequently prove myself wrong.

But the problem is I am frequently right. The balance between right and wrong has played out on the positive side for some time now.

You should know I do not have money to trade. I am advising without compensation, under a tacit marital contract. So when I am wrong I suffer emotionally more than if this coin of the market were out of my own pocket.

I suppose those knowledgeable about psychology, behaviorism, that sort of thing, will recognize this pattern as typical of some concept developed by the profession.

For me it means I have to risk going into the fog under steam and do so without radar, only a whistle blow to sound out what's ahead. Primitive tool.

George Parkanyi writes:

According to Ken Fisher, the first 2/3 of bear markets are relatively mild. Typically the last 1/3 (about 6-8 months generally) is the brutal bit. If you think this is a bear market, we have approximately 12-18 months to go, with the worst yet to come. But is it a bear market? The nature of Dr. Zussman's question suggests uncertainty. If his anxiety has increased, then a good rule-of-thumb is reduce exposure (position sizes) until something more compelling, or some clarity, presents itself. He can always scale back up if the market suddenly starts going his way. No matter what the conditions, certain fundamentals and the tape should offer a few tradeable ideas in either direction. I think the risk-mitigation strategy should be whatever his methodology generally calls for. If his risk management approach is contingent on the type of market that he is in, by definition he's going to have to market-time successfully all the time or run the risk of a large hit. Best to have one consistent risk management approach for all seasons.

According to Ken Fisher, the first 2/3 of bear markets are relatively mild. Typically the last 1/3 (about 6-8 months generally) is the brutal bit. If you think this is a bear market, we have approximately 12-18 months to go, with the worst yet to come. But is it a bear market? The nature of Dr. Zussman's question suggests uncertainty. If his anxiety has increased, then a good rule-of-thumb is reduce exposure (position sizes) until something more compelling, or some clarity, presents itself. He can always scale back up if the market suddenly starts going his way. No matter what the conditions, certain fundamentals and the tape should offer a few tradeable ideas in either direction. I think the risk-mitigation strategy should be whatever his methodology generally calls for. If his risk management approach is contingent on the type of market that he is in, by definition he's going to have to market-time successfully all the time or run the risk of a large hit. Best to have one consistent risk management approach for all seasons.

Jan

20

“Cloverfield” Haiku-Reviews, from George Zachar

January 20, 2008 | 1 Comment

Alien re-done

in New York. Artsy, but lacks

Sigourney Weaver.

The monsters invade

Manhattan. How did they know

not to touch Brooklyn?

Jan

19

Thoughts on Bobby Fischer, from John Floyd

January 19, 2008 | 4 Comments

We have read a fair number anecdotes, biographies and controversies, but perhaps another way to look at Bobby Fischer is to think about what we can learn from him in terms of both life and any applications of his life and chess as they apply to the markets.

We have read a fair number anecdotes, biographies and controversies, but perhaps another way to look at Bobby Fischer is to think about what we can learn from him in terms of both life and any applications of his life and chess as they apply to the markets.

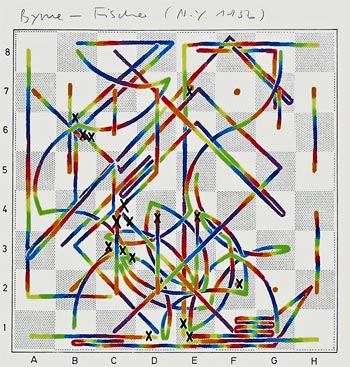

Independent thinking and willingness and adaptability to live in any number of places: Iceland, Japan, Philippines, and Hungary. Having been to or lived in all of them I can attest to the fact they are all vastly different. Fischer also demonstrated his ability and the longevity of his talents by making a comeback, on his own terms, as in his match with Boris Spassky in 1992. Or, when it seems as victory is improbable to make a dramatic and hard fought comeback as in his 1972 match against Spassky. How many times does the market make us question our own abilities and how needed it is to focus on ones methods and talents while still evolving and improving to achieve success? The need to be aggressive at all times whether it is attacking or using subterfuge as seems to be the case in his match against the grandmaster Robert Byrne.

This is not a suggestion to disregard or ignore his many faults but rather so that we can focus and learn from many of his positive attributes as well. Fischer's almost single-mindedness on Chess and his many transfers and incarnations also seem to have limited the scope of his achievements and therefore what could have been learned from him. As in nature when a tree grows, or is transplanted, it needs the root structure to support a broadening of the branch material and growth above.

Not being an expert on chess or Fischer, or life, I welcome all other suggestions and observations.

Laurence Glazier adds:

An icon of my youth gone, and the same applies for many of us.

It's a big question what to do about great artists who became antisemitic. Most notably in music, Wagner; and there is an open debate in Israel whether to hear his music.

I was never a fan of the recently late Karlheinz Stockhausen, but I listened to him no more after he psychopathically described 9-11 as a great work of art.

We have to take a broader view. Should we deprive ourselves of the works of DH Lawrence and TS Elliot because they were tainted as children with pervasive cultural prejudice? To boycott all literature by antisemitic English authors pre 1950 would leave very few (George Orwell a notable exception).

Bobby Fischer?

Probably not an Icarus, more a Narcissus who, lacking a mentor to grab his shoulder, fell - ever unaware - through the squared pool into muddy waters.

GM Nigel Davies adds:

I think there are many things to be learned from Fischer. Here's what comes to my mind:

1) Work rate: Fischer's 'remarkable' comeback becomes more comprehensible when one realises that all he ever did during his 20 year break was to study chess. I heard stories about his time in Hungary, that anyone seeking an audience was well advised to send in some of the latest chess books and magazines as a peace offering.

If you read 'Bobby Fischer goes to War' the comparison with the Russians becomes clear. In their training camps they studied a little chess in the mornings and then got the cards and booze out at midday.

2) Ascetic Lifestyle: Bent Larsen told me a funny story once about how he had to rescue a bottle of cognac from Fischer when the latter was intent on pouring it down the sink. Fischer also took a lot of exercise during his best years, mainly swimming I understand.