Aug

31

Oh, the Burdens of Management, by Alston Mabry

August 31, 2007 | Leave a Comment

I've been meeting with some folks who do a lot of training and development work with big companies. Recently, these T&D consultants have been hearing about a new problem their clients' managers are dealing with, and it involves their new, young employees from Generation Y (or Z), i.e., the ones fresh out of college. The clients want some sort of training program for their managers to learn how to handle this new problem. What is this new problem? When the Gen Y subs do poorly or are disciplined, the managers are getting irate phone calls from the young sub's parents.

I've been meeting with some folks who do a lot of training and development work with big companies. Recently, these T&D consultants have been hearing about a new problem their clients' managers are dealing with, and it involves their new, young employees from Generation Y (or Z), i.e., the ones fresh out of college. The clients want some sort of training program for their managers to learn how to handle this new problem. What is this new problem? When the Gen Y subs do poorly or are disciplined, the managers are getting irate phone calls from the young sub's parents.

Alex Forshaw replies:

The WSJ ran an article about this some time ago. Helicopter parenting is making its predictable transition from high school, to college, and now to the workplace.

Baby boomer parents are obsessive about building an invulnerable system of guideposts in life (get >2200 SAT, be a co-editor of the high-school paper, which gets your kid into a top 20 college, which gets your kid into 90th percentile of starting workforce, which gets your kid into a top x%ile grad school) and they are simply incandescent when their "children" encounter any speed bumps along the way.

You have to wonder if this huge swathe of baby-boomer upper crust-dom was ever exposed to pain resulting from mistakes, or if they ever took any real risks in life.

Aug

31

Nature’s Bounty, from Alston Mabry

August 31, 2007 | Leave a Comment

This is grillin', not BBQ, but I just had to pass it on anyway. A friend here in British California got himself a nice, new, giant Weber "Genesis" grill. Given the size, it ought to be called the "Missouri" or the "Invincible". It plugs right into an outside gas line, so no external tank needed.

This is grillin', not BBQ, but I just had to pass it on anyway. A friend here in British California got himself a nice, new, giant Weber "Genesis" grill. Given the size, it ought to be called the "Missouri" or the "Invincible". It plugs right into an outside gas line, so no external tank needed.

One of his specialities is to put a bunch of sun dried tomatoes, parsley, garlic and herbs in a food processor, whip it into a pesto, and then spread it in a thick layer on the skinless side of a properly prepared (i.e., de-boned) slab of fresh-caught salmon. Then he puts the salmon skin-side down on that Weber and cooks it until it's just firming up but still juicy. Meanwhile, he's tossed big chunks of onion, mushrooms, peppers and squash in olive oil, added salt and pepper, and roasted them in a veggie tray, also in the Weber.

Throw in a bottle of Rigamorole (blended Riesling and Gewurtz) from the Okanagan, and fresh blueberries for dessert, and it's one of the best meals I've had in a long time.

Greg Calvin adds:

I have put one of these Webers to good use after obtaining it through the certified pre-owned program. The Genesis is a well-constructed grill that provides for even distribution of heat throughout the chamber, making it ideal for when you don't want to flip the food. The design is flare-up resistant, and higher models generally have more stainless steel.

This grill is not perfect for BBQ as the burners run side-to-side, but this is a minor gripe. The Summit line provides front-to-back burners as well as other accessories at a substantial jump in price. Weber's customer service is even better than its grills.

Some simple equipment lessons learned:

If you're using propane, get a spare tank. It's a minor cost, and eliminates some 'uh oh' bbq moments. Keep the grate clean, keep it oiled, or seasoned. Finally, get a second opinion — Check the built-in thermometer with a good oven thermometer. This is especially important for BBQ and roasting.

John Bollinger writes:

Get some swordfish steaks, one per person. Wipe 'em and spread one side thickly with a mixture of Dijon mustard, a little good olive oil, a bit of sea salt and a few good cranks on the pepper mill with a mix of peppercorns. Let 'em sit while you fire up your grill. Grill 'em mustard side up, without turning. The heat cooks 'em from the bottom up and the acid cooks 'em from the top down. Five to seven minutes should be right depending on the thickness of the steaks and the temperature of the grill.

Webers: I have three, a little Smokey Joe, an 18" One Touch and an old 22", so I always have the right tool for the job. They sit in a line like the three bears. Use hardwood charcoal if you can get it. Mesquite charcoal is cheap and plentiful here. My local liquor emporium sells it in 50 pound sacks for the cost of a 20 pound sack of the standard toxic oil-refinery briquettes.

Aug

31

Outsourcing, from Henry Carstens

August 31, 2007 | Leave a Comment

I just had some code written to setup and process a workflow. The code is all Python so I can maintain/expand it. The problem, of course, is that it's taken me a week of learning obscure (chmod, source, PATH) Unix commands just to test the darn thing. It is kind of cool, though.

I subbed out the code work on Guru.com. It's a beautiful bunch of code modules, lots of features, all documented and well-written. Even has file locks. Will work locally or on a server. My cost? $120 (and some Unix pain).

Aug

31

Ozymandias, noticed by East Sider

August 31, 2007 | Leave a Comment

The $64,000 Entreaty for a Portrait of the Chairman

By Mary Ann Akers, Thursday, August 30, 2007; Page A19

He's been chairman for only eight months, but already Rep. Charles Rangel (D-N.Y.) is more than daydreaming about what his official Ways and Means Committee portrait will look like. He knows one thing: It'll be top of the line.

In perhaps the most thorough and earnest letter ever written on the subject of a member of Congress's portrait, Rangel's campaign attorney sent a letter to the Federal Election Commission asking permission to use either campaign or leadership political action committee money to pay for the chairman's grand portrait.

Aug

31

Bo Keely, from Ken Smith

August 31, 2007 | Leave a Comment

Bo Keely has moved into the Oasis Motel in Blythe CA and has begun new job as substitute teacher in local high school. His first call to work to sub was yesterday.

His vision of life on the road has been modified, I believe. Maybe temporary, because Bo has a lust for the road, is of restless character. Yet strange things happen in this universe. He may settle down, and should, in my thinking, because he has a lot to offer students in the way of life experience, is cunning, with creative methods in teaching.

Maybe we will see Bo move out of his desert retreat, take a steady job, set himself up in a Blythe condo with swimming pool, get a business suit, start eating in upscale establishments instead of the free food kitchen.

Riz Din adds:

I found a handful of old YouTube shorts on Bo and collected them.

Aug

30

The Best Place in the USA, from Bruno Ombreux

August 30, 2007 | Leave a Comment

I'll give you my foreigner's viewpoint on the best place in the USA. It is always interesting to have a fresh and candid opinion from an outsider. This is one of the reasons why companies hire management consultants.

I'll give you my foreigner's viewpoint on the best place in the USA. It is always interesting to have a fresh and candid opinion from an outsider. This is one of the reasons why companies hire management consultants.

My credentials as a European expert on the USA are: I was married with a girl from Boston MA, then I had a girlfriend from Santa Barbara CA for eight years, then a girlfriend from New Fairfield CT for three years. And I traveled for business to places like Los Angeles, Houston, Cleveland. The only really famous American town I don't know is New York, which is odd because that's the city Europeans usually visit first.

In my expert opinion, the best place in the USA is Jacksonville FL. My friends in Boston say that my friends in Jacksonville are trash and I am not associating with the best America has to offer, but I don't agree. The people I know there are marvelous. They are simple, honest, welcoming people. They are not intellectuals like the Bostonians, but who needs intellectuals to barbecue and have a keg party? The Saint John's River is a great river and a sight to behold. Climate is great. Never too warm, never too cold. Food is of the utmost quality.

Charles Pennington adds:

Good things about Jacksonville:

- Plentiful, easy-to-find barbecue

- Hot weather, yes, but frequent sea breezes

- People are sensible and use air conditioning

- Ponte Vedra Beach Resorts, a great spot, with beautiful beaches, great food and great tennis

- Real estate away from the coast isn't too expensive

I love Jacksonville.

Aug

30

Rugby World Cup, from Aaron Krizik

August 30, 2007 | 1 Comment

The IRB Rugby World Cup, the greatest venue for the sport, begins in eight days. I am rooting for the USA Eagles, but my favorite team is the South Africa Springboks, a team with absolutely no flair or tactical nuance in their game. Their "strategy" has been described pejoratively as "subdue and penetrate." They are the most physically aggressive side in any sport I have ever seen — and have been that way for a century. They fight you, they tackle you to oblivion, they run over you, but they rarely (defined as "no more than any other team" since rugby is incredibly violent) play dirty.

The IRB Rugby World Cup, the greatest venue for the sport, begins in eight days. I am rooting for the USA Eagles, but my favorite team is the South Africa Springboks, a team with absolutely no flair or tactical nuance in their game. Their "strategy" has been described pejoratively as "subdue and penetrate." They are the most physically aggressive side in any sport I have ever seen — and have been that way for a century. They fight you, they tackle you to oblivion, they run over you, but they rarely (defined as "no more than any other team" since rugby is incredibly violent) play dirty.

Of the sports I have played, rugby most reminds me of the game of life. It is a constant grind and struggle. Physical, mental, and emotional pain are around every corner. I was once blindsided on the side of the face during a match, which both hurt physically and offended my sense of fairness. But you have to focus and hope your teammates can kindly point out the transgressor for suitable retaliation. There is simply no time to become offended or to take things personally. It is too fast a game for that, and diverting your attention to a petty offense dramatically reduces your effectiveness.

You must communicate with your teammates constantly, you must defend them when they are punched, gouged, and cleated at the bottom of a ruck. You cannot be intimidated by foul play or hostile words, or become frustrated when someone bumps into you after the official stops play. It's all gamesmanship.

At the end of the game, all is forgiven. Everyone understands that temperaments during conflict become warped. The person who punched me later walked up to me, bought me a beer, and apologized with sincerity. It's a great sport, filled with incredibly tough and skillful athletes, and a joy to watch.

Ian Brakspear adds:

Rugby is the ultimate in physical challenge. I played for the national team in Rhodesia, then played for five years in South Africa, including two years in one of the hardest competitions in the world, the Currie Cup.

There is a position in the game for everyone, no matter what his physique, size or speed. Back-line players require a lot of speed, especially the wings; fullbacks and fly-halves must be good under the high ball, good in defense and be able to counterattack from turnovers — thus the need to think and size up the game in a split-second as well as the ability to kick the ball prodigious distances.

Tight-forwards come in all shapes and sizes but must be physically strong both with ball in hand, on defense and in the ruck and maul. The front row are usually short and very stocky and are some of the heaviest men on the field and the locks are always tall (at least 6'6")and well-built.

Loose-forwards' physical requirements are somewhere between the backs and the tight five; they lack the speed of the backs and yet are faster than the tight five but not as big or heavy –- their tackle count in the game must be higher than any other player's on the field to be considered effective for their position. Some countries play with a genuine fetcher (for instance, New Zealand's Richie McCaw) but others don't.

Today's games are won on defense, yet the only team to have won the World Cup twice, the Australians, won with their attacking play.

As for the Springboks' (South Africa) chances, I hope we win, but we lack a quality fly-halve, don't have a genuine fetcher in the loose-forwards playing in our "A" side, our rush defense from set-pieces is stale now and teams have figured out ways to beat this. We lack the ability to score from set-pieces and are forced to include some third-rate players — those our government refers to as the "previously disadvantaged." But in our favor we have the best lineout forwards in the world, our defense lines are amongst the best in second phase play, and we can score tries from broken play.

The coach of South Africa, Jake White, is a good friend and was my training partner for a long time. But Jake lacks that "something special" to win this, the fourth most viewed sporting event in the world, as he has never played rugby at a high level, not even club rugby, after winning the Tri-Nations in his first year, 2004 — his winning percentages have gone down every year since. Jake and I have had many late-night debates about strategy and tactics.

Aug

29

Right and Wrong, from David Lamb

August 29, 2007 | Leave a Comment

What's right with the world? Paul Potts is rewarded for a true talent after years of struggle.

What's right with the world? Paul Potts is rewarded for a true talent after years of struggle.

What's wrong with the world? Lauren Upton is rewarded almost immediately from the womb based on physical appearance, but receives her just deserts when forced to demonstrate more than that one "talent."

James Lackey replies:

Why is born smart different than born beautiful? If one is born smart and works to refine his natural talent into ability, we call that hard work. But if a beautiful girl works to refine her natural ability, beauty, we chime in with "what is wrong with this world?"

Michael Brush remarks:

The poor girl, give her a break. Have you ever spoken before a large crowd? I have. It is terrifying. This young lady had an audience of several million and she is only 17. It may be fun, but it is heartless to ridicule her for being nervous. I'd like to see you try speaking on national TV for the first time.

David Lamb replies:

If Paul Potts had her looks, or if Miss Teen had Paul Potts's looks, would their stories be the same? My point was that pageants look at skin first, than talent. And, perhaps, Potts didn't get much of a chance in the opera ring due to his looks, or lack of refinement. What is right about the world is that a show like that was able to place a person like Potts on center stage, in front of millions, to have them accept him or not, after he demonstrated his talent. There aren't many venues in this world that offer such an opportunity.

On the other hand, place a plain girl into a Miss Teen pageant and she won't even make it past the first interview, even though she may be able to give the correct answers without a moment's hesitation.

Steve Leslie remarks:

What is wrong with this world is people who get a sordid pleasure and a wicked delight out of tearing others down. Schadenfreude. Who try to start a controversy where there is none.

What is right with this world is those who exercise their inalienable right to pursue their own interests.

We are told by the greatest of teachers that he who is without sin may cast the first stone. And that he who is exalted shall be abased.

Aug

29

End of an Era, from Jason Thompson

August 29, 2007 | 2 Comments

With the merger of the CBOT and the CME, a physical consolidation of the two exchanges' trading floors will take place with the Merc floor being shuttered. As a result some current open outcry pits will move exclusively to the screen, a move that will likely mean the death of the product in certain cases. Oh Frozen Pork Bellies, how we knew thee.

With the merger of the CBOT and the CME, a physical consolidation of the two exchanges' trading floors will take place with the Merc floor being shuttered. As a result some current open outcry pits will move exclusively to the screen, a move that will likely mean the death of the product in certain cases. Oh Frozen Pork Bellies, how we knew thee.

Ryan Carlson writes:

On Monday, bellies traded only 148 contracts, all in the pit, with an open interest of 710. Not a huge loss for the floor crew.

The meats are funny at the Merc because it's such an old-school crew down there. Walking down to those pits, everyone will eyeball anyone new. Also, they've been trying to push the meats to the screen but they won't go. I've been told that no one will trade with you if you wear a headset (computer trader on other end). Also, I've been told that unless you know people down there, they won't trade with you either.

The power of the CME always flowed from the meat pits, so I've done my best to align my interests with theirs.

Aug

28

Wealth and Poverty, from Roger Arnold

August 28, 2007 | 5 Comments

Washington Suburbs Lure Federal Work to Top New York's Wealth

Forget those swanky Connecticut addresses, lakeside Chicago suburbs and Silicon Valley millionaire enclaves. Loudoun and the next two wealthiest U.S. counties lie just outside Washington — the traditional home of government workers — and have median household incomes rising to almost $100,000, the latest Census Bureau figures show.

I have stated on the radio for years that if the taxpayers had any idea how disconnected government pay had become from the private sector pay, they would burn down Washington. It is not uncommon for two government workers to marry, each with a bachelors degree, and each attain a $100,000+ salary inside of five years and live in a million dollar home in the DC burbs. I live here and can tell you it is truly surreal.

During the housing crunch of the 1930s, in many suburban and rural areas, where most of the banks failed, government employees moved in and bought up the land cheap from the taxpayers who had gone under. I kid you not.

I also advise reading Thomas Woods Jr.'s new book 33 Questions About American History You're Not Supposed To Ask, which is the follow-on to his previous book, The Politically Incorrect Guide to American History.

Mark Meredith remarks:

Wealthy DC suburbs are not the land of government workers, but of corporate lobbyists and consultants. Nearly every government worker I've known in DC made much more money when he left for the private sector.

Aug

28

Markets and Oceans, by Paolo Pezzutti

August 28, 2007 | 1 Comment

Markets develop impulses which displays some similarities with what you experience at sea. After a big anomalous wave you can expect a period of lower waves. That is when you want to change the course of your ship because it is easier to turn. A second series of waves will then challenge your ship; they can be weaker than the first series or bring a renovated impulse to mounting seas. We have experienced in the market a first big impulse to the downside with increased volatility, followed by a rebound characterised by lower ranges and volume. A good opportunity to exit the market in the short term. The second series of waves has now started toward the downside. It remains to be seen whether it has less strength than the first and it will not reach or only test previous lows. Or it will surge higher and bring the market to print new lows.

Aug

28

Travel Tips for Europe, from GM Nigel Davies

August 28, 2007 | 1 Comment

What I've found with most cities is that there's an unspoken two-tier system of cost — one for the locals and one for foreigners. Which tier someone chooses is entirely voluntary but preys on feelings of insecurity and ignorance about his destination.

Here are some travel tips for visiting any city inexpensively, and getting to know it much better too:

a) Dress down, and that doesn't mean new/garish casual clothes. By blending in with the locals you'll feel more comfortable living as they live.

b) Use inexpensive luggage - less chance of its being stolen and you don't present yourself as a turkey waiting to be plucked.

c) Make an effort to learn local customs and language, and that includes English. Blending in gives you better access to less expensive services and makes the locals more willing to help you.

d) Don't assume that everywhere has areas that are as bad as your home town or that muggers are waiting round every street corner. In the UK, for example, very few criminals have guns so the very worst they'll do is pull a knife. If you're really nervous about this, carry a personal alarm, or big stick, or be prepared to hand your wallet over. This helps give you access to less expensive areas.

e) Don't take taxis as a reflex. Get the appropriate maps (which are usually free) and investigate the local underground and buses. With trains, check if there are expensive times to travel and find out what deals are offered with travel cards and contracts.

f) If you're visiting the capital consider staying in a nice suburb (where the locals live) and commuting in. This guarantees much better value on hotel rates and just about everything else. Traveling light helps.

g) Consider visiting places outside the capital, even if they reduce bragging rights (I 'did' London/Paris/Rome). I personally have no idea why anyone would want to visit London when there are cities like Chester and Durham available.

h) Get as much inside knowledge as you can about your destination. With London, for example, Southall is a dirt cheap but great place to go for a curry and offers the best value outside of McDonalds.

i) Find out what level gratuities are appropriate. In London 10% is plenty and if you stay in a place without a bellboy you don't need to tip.

Paying more than you want to is a simple product of laziness.

Aug

28

Spec Party Highlights, from Jim Sogi

August 28, 2007 | 1 Comment

Left to right: GM Nigel Davies, Dr. Phil McDonnell, Prof. Gordon Haave

Left to right: GM Nigel Davies, Dr. Phil McDonnell, Prof. Gordon Haave

This year's Spec Party had a different feel than other years', a more mature, more focused, a more comfortable, intimate feel. We had specs from all around the world: India, Ireland, Scandinavia, Zurich, France, Italy, London, Hawaii, California, Nevada, Tennessee, Georgia, Delaware. A truly remarkable international diverse experience. The depth of knowledge, expertise, and perspective was simply mind boggling. Though there were fewer, the group was more intense, more hardcore quantitatively philosophically naturalistic in the Niederhoffer/Kenner tradition.

We spoke of survival of volatility, diversity, adversity, ecologies, as we strolled from jungle environment to desert environments at the Haught Conservatory Greenhouse at the New York Botanical gardens bringing to mind the radical and swift regime changes and the necessary adaptations in nature and the markets.

We rode out to Shea Stadium to see the Mets play Florida. Baseball has so many parallels to the market. The long periods of hard effort with no score. The long innings of playing from behind, the maximum effort required while in a losing position. The rapid reversals as the Mets lost the game to a home run in the bottom of the 8th. All lessons valuable to the specs who braved adverse windy wet conditions, an anomaly in an otherwise sunny, warm, beautiful New York summer.

We went back in time to the 60s and 70s in a nostalgic trip out to quaint Coney Island, near Brighton Beach where Victor grew up, per the stories from Ed Spec. We swam in the ocean, discussed waves, rode the Ferris wheel and had a wonderful day in the sun. I had a very nice discussion about India with Sushil Kedia, and a lengthy discussion about chess, strategy, and markets with Grandmaster Davies on the way back.

The Dinner at Delmonico's was the highlight of the weekend, with a great collection of specs celebrating with Victor and Laurel in the tradition of the giants from the history of Wall Street. I can imagine that years in the future a Wall Street legend will tell of how Niederhoffer threw lavish parties and took over the whole restaurant for his friends. The food was delicious and the tap dancing and Hula from the traveling Von Sogis of Hawaii added to the fun of the evening. Among the likes of David Wren-Hardin, Bill Egan, Chris Cooper, Dan Grossman, Andy Moe, Tim Humbert, Easan Katir, John Floyd were fascinating discussions about cutting edge microstructural theories, fundamental considerations in currencies, statistical chemistry and the drug industry, and the creation of unintended toxins. But the evening was just starting; next was the Tim Melvin pub crawl to the usual midtown Irish bar where many a very tall trading tale was retold with flourish and where Melvin was characteristically seen in the arms of three beautiful blondes at once. James Goldcamp was heard to have had a really good time.

The weekend ended up with a serious and quite profound and relevant discussion of current market conditions at the Rose Garden in Central Park under beautiful blue skies and cool weather, with raccoons scurrying in the lush green arbors as Victor and Laurel espoused their theory of the markets as the mechanism that mediates between government and the the populace, and the need of the financial ecology to support its overhead and extract the maximum amount from the weak, causing not only the obvious capital allocation but also buffering the power of government to protect the needs of the populace through price and capital demands. It is a novel theory that I have never heard discussed anywhere else. The market itself is the mechanism that effects large scale-social and political change through changes in incentives, attitudes and demand, and is more than merely shuffling money. Understanding the markets as a social and political driver can lead to long term trading strategies and keep the trader on the right course.

New York was vibrant, alive, clean, young, safe, friendly. New York has a noticeably disproportionate number of young people, and slim attractive young women dressed nicely compared to other areas, something Galton himself was known to count. Even Dr. Zussman noticed this anomaly. At many clubs and bars large groups of attractive women attended, and late at night there were more women out and about than men. The taxi drivers, restaurateurs, hoteliers, and people about town, subway riders, citizens, restaurant-goers, theater-goers, were all courteous, friendly, intent and focused on discharging their social obligations and expectations. I saw no antisocial behavior, no arguments, no outbursts of anger, almost no vagrancy or homelessness. The subways were clean, very clean, well lit, and uncrowded. Even the traffic had less hornblowing and argumentation. To me, who grew up in the bad era of the 70s in the city, a real low point when the city was on the verge of bankruptcy and crime and vagrancy were rampant, it was a remarkable and enjoyable weekend in a magic kingdom.

For these wonderful and life-changing experiences and lessons in life and markets, available in no other forum, and for the creation of this unique, international, eclectic, esoteric, erudite group, and for their huge contribution of expense and time in the midst of tumultuous market conditions, we have the true genius, generosity and broad thinking of Victor and Laurel to thank. I extend my heartfelt thanks and love to them both for a truly wonderful weekend I will cherish my whole life.

Ken Smith writes:

Glad the Specs had a pleasurable weekend. I couldn't be in New York. It's a 6,000 mile round trip for me. Anyway, I do not talk sports, don't care about politics, played golf only once in my life, can't remember who the current boxing champ is, have forgotten books I've read, don't remember any poetry, can't read music or play an instrument, have no bragging to do since I never got anywhere, can't remember names of people I meet for as long as even five seconds, hate chit chat, small talk, and big talk, and daydream during conversations, all of which makes me a poor guest at a dinner table.

Aug

28

Big Mac Indicator, from Jason Thompson

August 28, 2007 | Leave a Comment

My wife and I just returned from a dozen days in the UK, including a visit to Caledonia and its stately capital, Edinburgh. London prices verge on the absurd; the average Londoner must be living a far inferior life as compared to someone of a similar station here in Chicago. For instance, public transport costs 50% to 200% more than the CTA on a per ride basis, taxis are roughly 300% more per mile, a TESCO food bill 35% more. My tip of the hat to the Economist comes in my notations of the cost of a Big Mac Meal (medium size) at McDonald's whenever I travel. In London I saw 3.69 pounds as the cheapest, on High Street across from Kensington Tube station, with prices in Edinburgh and Inverness ranging from 2.99 to 3.19. This compares to a local price of $4.70, about 2.35 pounds.

My wife and I just returned from a dozen days in the UK, including a visit to Caledonia and its stately capital, Edinburgh. London prices verge on the absurd; the average Londoner must be living a far inferior life as compared to someone of a similar station here in Chicago. For instance, public transport costs 50% to 200% more than the CTA on a per ride basis, taxis are roughly 300% more per mile, a TESCO food bill 35% more. My tip of the hat to the Economist comes in my notations of the cost of a Big Mac Meal (medium size) at McDonald's whenever I travel. In London I saw 3.69 pounds as the cheapest, on High Street across from Kensington Tube station, with prices in Edinburgh and Inverness ranging from 2.99 to 3.19. This compares to a local price of $4.70, about 2.35 pounds.

Aug

27

Market Efficiency, from Paolo Pezzutti

August 27, 2007 | 1 Comment

Market efficiency assumes that at any given time prices fully reflect all available information and the market comprises a large number of rational investors. According to this approach no investor has an advantage in predicting a return on an asset. There are three forms in which the hypothesis is stated: weak; semi-strong; and strong. In various degrees it emerges that no excess returns can be earned using technical analysis, historical prices, or other data.

Market efficiency assumes that at any given time prices fully reflect all available information and the market comprises a large number of rational investors. According to this approach no investor has an advantage in predicting a return on an asset. There are three forms in which the hypothesis is stated: weak; semi-strong; and strong. In various degrees it emerges that no excess returns can be earned using technical analysis, historical prices, or other data.

Speculators will try to exploit anomalies until they disappear. Predictable pattern of price movements eventually will not be traded because transactions costs outweigh benefits. Large and liquid markets where information is widely available should be more efficient. In order to implement investment strategies based on the exploitation of these inefficiencies, transaction costs have to be lower than the expected profits.

Inefficiencies come and go; some may remain for longer periods. Anomalies exist and will continue to exist because investors do not always behave rationally. I believe that in certain markets the main players adopt similar strategies and influence market behavior, leaving niches to be exploited by more flexible and fast traders. This should be a driver when trying to identify new anomalies.

Aug

27

Most Fearless, from Joe Gogolak

August 27, 2007 | Leave a Comment

This is from the "Weird But True" page in the New York Post today:

Two zoologists have helped save the world's "most fearless animal" - which will eat virtually anything - from angry beekeepers.

Keith and Colleen Begg of South Africa found that the beekeepers had been hunting and trapping endangered creatures called honey badgers because the animals were destroying hives while feasting on eggs, larvae and pupae.

The solution? Have the beekeepers raise their hives a mere three feet off the ground, where the badgers can't reach them. The Guinness Book of World Records lists the honey badger as the "most fearless animal" because it will eat anything from a scorpion to a python to a young polecat.

After reading so many articles with animal/investor analogies on this site, the first thing that popped into my mind was, "Which investors would be deemed 'most fearless' and 'eat' any type of smaller investor or in any market condition?" Adaptability and versatility are great tools to have in the arsenal of successful investing.

Aug

27

Mother Teresa, from Ken Smith

August 27, 2007 | 2 Comments

NEW YORK (AFP) - Mother Teresa, who is one step short of being made a Catholic saint, suffered crises of faith for most of her life and even doubted God's existence, according to a set of newly published letters.

Probably every saint, and we are all saints if Catholic, all of us have a dark night of the soul, descend into the underground of spirits, feel angst in every molecule of spirit, and some are never able to climb out of the darkness.

To write about this nun as if having doubt makes her less deserving of recognition is part of what goes on in human life, a drive to take away her prestige so others will not follow her saintliness.

David Lamb remarks:

This reminds me of Newton's manuscripts housed in Jerusalem wherein he kept secret all his life of his disbelief in Christianity's central doctrine, the Trinity. He was a minister at the time. He read the bible in numerous languages and concluded that this doctrine was not true. Denying the Trinity was illegal so he kept quiet.

James Lackey writes:

I lived most of my life in Chicagoland and Florida, and after a year in Tennessee, people from NY, CHI or LA have no clue how much of the so called bible belt really is full blown, full time, church-going, non-cussing, non-drinking patriotic Americans.

Many think people From TN, KY, NC, SC, GA, AL and southern Indiana and Illinois are from a different world. Yet people from here, unless they are newsmen or bible-salesmen who preach against society's ills, really don't give much care, thought, time or concern to what people in LA think. The joke around here is: stars from LA talk about the poverty and war in Africa and Iraq. People from here are in Africa doing the mission work for the church or in the 101st Airborne, just back from Iraq.

Aug

27

Outliers, Randomness and Red Bandanas, from Larry Williams

August 27, 2007 | Leave a Comment

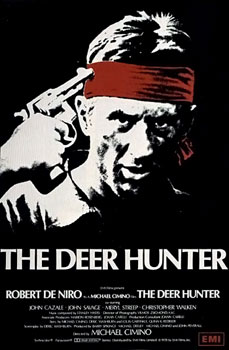

The best movie ever on outliers, randomness and red bandanas is The Deer Hunter.

The best movie ever on outliers, randomness and red bandanas is The Deer Hunter.

I "have worn that red bandana of speculation" and late at night miss it –not unlike the Kingston Trio's refrain "once you hear the whistle blow, you can't come back."

Nothing is like the rush being long "too many contracts" whether they go with you or against you. Every second vibrates — it becomes a hundred yard dash and you are the fastest man on the planet, totally in the flow, winning or losing. An altered state.

In that state I encounter speculative Nirvana, and found it is a most dangerous place to visit, winning or losing, because it is so addictive. Either way the endorphins surge, mainlined into the larger vessels. Life is just one heartbeat. There is nothing else.

Not unlike your first bareback ride, getting in the chute, settling down on the horse, then giving that nod, the gate swings open and life begins or ends. Addicted to danger: what a great way to live and love.

Ken Smith replies:

I know that feeling. For three or four years I have not used realtime data, trading on marco information and end of day charts. Today I began using real time again and the experience brought me to life. Realtime boosted my spirits and the lift aroused my motivation to get to work. A good day to be alive.

Aug

27

A Great Guy to Fade, from Larry Williams

August 27, 2007 | 1 Comment

Jim Jubak of MSN Money is the guy who never gets the chair when the music stops — he's a bottle of ketch-up. But Singapore has so much going for it: the meeting and banking point between China and India. Lots of action there and the best, by far, crab dinner in the world, Singapore Pepper Crab. To die for.

Jim Jubak of MSN Money is the guy who never gets the chair when the music stops — he's a bottle of ketch-up. But Singapore has so much going for it: the meeting and banking point between China and India. Lots of action there and the best, by far, crab dinner in the world, Singapore Pepper Crab. To die for.

Aug

27

UK Interest Rates, from Riz Din

August 27, 2007 | Leave a Comment

Interest rates in the UK are higher than Germany’s and the rental yields are much lower.

For several years now, I thought UK property was grossly overvalued and primed for a fall. However, using a gross simplification I have recently formed a new model of the UK housing market. My thinking is quite simple.

Over the long-term, house prices seem to keep up with inflation (let's say two to three percent per year). Current net yields in the UK are around four percent.

As a long-term investment, it may make sense to accept a low yield on the rental because of the long-term inflation hedge component. Thus the rental yield should perhaps be compared to the real interest rate, not the nominal rate. On this basis, houses in the UK may be fairly valued. I wonder whether Joe Public is walking around with such a model in his head?

Aug

26

Long/Short Equity, from Bruno Ombreux

August 26, 2007 | Leave a Comment

Everybody is developing new factors. Look at me, I am small fry, and I have been investing based on factors. I thought I was alone but recent hedge-fund problems have made it clear that the whole world was doing the same thing. In the world of low-frequency finance, everybody has access to the same data, is using similar tools, hence everybody is getting the same results, which are to buy certain stocks with certain risk exposures and sell some others if you fancy being long/short.

Everybody is developing new factors. Look at me, I am small fry, and I have been investing based on factors. I thought I was alone but recent hedge-fund problems have made it clear that the whole world was doing the same thing. In the world of low-frequency finance, everybody has access to the same data, is using similar tools, hence everybody is getting the same results, which are to buy certain stocks with certain risk exposures and sell some others if you fancy being long/short.

This raises the possibility that we were not paid to perform the economic function of taking risk and collecting risk premia, but merely noise investors in a crowd, with ever more money going to funds investing in the same type of stocks, then going to these stocks, increasing factor returns, confirming historical numbers, increasing allocated money, and increasing fund returns in an upward spiral.

Just riding the wave of a Ponzi scheme is not a pleasant perspective. So of course everybody is reassessing factor models.

To be fair, everybody knew he would fail in a liquidity crisis. Quoting the 2004 Wiley book, Pairs Trading, by Ganapathy Vidyamurthy:

A scenario-altering, huge macroeconomic event, for instance, relating to interest rates … typically manifests itself in the form of a liquidity crisis. In these situations, the covariance structure breaks down, leading to the breakdown of the model.

Aug

25

The pain in real estate land is increasing. Some of my developer cronies are hurting; taking 30 cents on the dollar loans against raw land they hold in reserve, with 90-day buy backs, to get cash to service ongoing projects because their credit lines are getting pulled. Brutal.

The pain in real estate land is increasing. Some of my developer cronies are hurting; taking 30 cents on the dollar loans against raw land they hold in reserve, with 90-day buy backs, to get cash to service ongoing projects because their credit lines are getting pulled. Brutal.

Many won't be able to meet the 90-day buy back unless, ironically, they come up with a development plan for that land that the hard money guys will fund. The scramble is on and the domino effect may begin soon as it did in the early 90s, the last time I saw this. Then I watched guys worth 100 million on their balance sheets go broke in 12 months.

Stefan Jovanovich adds:

The prices here in the Bay Area generally seem to have held up far better than they have in San Diego, Los Angeles and Orange County. What has slumped is the demand for home improvement services. The roofers, remodeling contractors, plumbers, and other local people in the building trades whom I know here in Contra Costa County have seen their backlogs disappear. They are still busy, but they no longer have pending projects beyond the job scheduled after the one they are currently working on.

Only a few months ago most they had half a year's work lined up; now they have three to four weeks’. It is now the best time since the early 90s to fix up a house in terms of cost, scheduling and improvement in building materials. Plywood has become expensive and crappy but resin board is now better and cheaper. HVAC equipment is vastly improved. Water heaters now have internal insulation and flameless ignition. Roofing underlayments have gone far beyond impregnated paper, and composite shingles now come in reflective "cool" shades that reduce heating loads by 30+%.

Tools have also improved. Nail guns, for example, are now much lighter yet actually stronger because of the use of composites. Building standards have also improved. Twenty years ago my friend George was considered "weird" because of his insistence on strapping tanks and adding plywood panels to house foundations for shear strength. Now earthquake reinforcement is taken for granted. What the people in the trades are wondering is whether people will take advantage of the opportunity. What the people in the trades themselves are doing is hiring each other to fix up their own primary and vacation homes. Whether that is a vote of confidence in the future or a sign that many intend to retire (most are in their late 40s or early 50s - which is "old" for the building trades) is the $64 question.

Dan Sturzenbecker writes:

I watched a recent episode of a popular reality TV show featuring investors who purchase fixer-uppers, make quick upgrades, and flip them back onto the market for purportedly large profits. A beach home was purchased in 2005 for $1.2 million. After $250,000 in repairs over a two week period, a "realtor" at the end of the show pronounced the home worth $2.4 million. The investors threw a party in the home and the episode faded to a close with much laughing and back-slapping in celebration of their investing genius. After a bit of research on the Internet, I discovered the home is still on the market with an asking price of $1.675 million.

Aug

25

Book Review, from Tom Ryan

August 25, 2007 | Leave a Comment

A History of the Vikings, by Gwyn Jones, is a keeper. It was originally published in 1968. This is not a history-light book that is all too common these days, but rather a comprehensive and thorough disposition on a rather complex society over the course of five or six centuries.

A History of the Vikings, by Gwyn Jones, is a keeper. It was originally published in 1968. This is not a history-light book that is all too common these days, but rather a comprehensive and thorough disposition on a rather complex society over the course of five or six centuries.

The book, if nothing else, dispels many of the negative stereotypes of the culture as being hell-bent on raping and pillaging everything they came into contact with (note the current movie Pathfinder). That's not to say that the Vikings did not raid their neighbors, fight wars against other cultures and take slaves. They did. But so did the Gauls, Angles, Saxons and Jutes, and the Goths, Vandals, and Celts before them.

Primarily the story of the Vikings is a story about trade; these people were first and foremost traders, and their expansion was driven by economics. Rather than raiding and relying on plunder, the Vikings set up a system of trading outposts where they traded for goods with the local populations. The Vikings had what was at the time the most sophisticated and sound monetary system in Europe. It utilized silver and gold coinage as well as precious metal and base metal beads. They had insurance contracts. They provided security and protection to shippers to protect goods from piracy.

At the pinnacle of Viking culture in the 9th and 10th centuries, the Viking trade system extended from Iceland all the way to Persia, which is why some of the most important information we have about the Viking culture comes from accounts from other cultures including Arabic and Byzantine traders. The Byzantine emperor hired the Vikings for his personal bodyguard (the Varangian Guard) and they used this position to further extend their trade network. The geographic span of this culture (Greenland to Byzantium, Portugal to the Urals) is amazing given the period and especially when you consider the state of technology at the time.

Clearly this was a risk-taking culture and it just goes to show how a bit of egalitarian politics (the Vikings although feudal, were not as hierarchical as the other tribal groups at the time), a sound monetary system, a focus on technology (Viking weaponry and ships were at the time the best in Europe by far), can create a potent cultural force.

Aug

25

Thoughts on Insider Trading Paper, from Stephen Schneider

August 25, 2007 | Leave a Comment

I recently found Victor's paper on (legal) insider trading, "Predictive and Statistical Properties of Insider Trading" incorporated into a book on the subject, How You Can Use the Wall Street Insiders, by Perry Wysong.

Victor's foresight about the potential use of this information, and his efforts to make strict quantitative use of it so early in his career, is particularly interesting to me. I wonder if Victor and Laurel have done any additional research in this area that might be available to individual investors?

So far as I can tell, although he is hardly mentioned at all today, Perry Wysong was the primary newsletter writer of the time (1960s-1970s) for insider trading. From his book, it appears Wysong used insider trading with relative strength measures to select stocks, but he does not say precisely how he measures relative strength.

Since Wysong was an insurance actuary prior to becoming an investment newsletter writer, I presume he must have known a reasonable amount about statistics. Do you have any insights about how he selected stocks?

Daily Speculations is an excellent resource, by the way. I admire Victor and Laurel's honesty and spirit of inquiry. It's a great inspiration to me, and, I imagine, to many other individual investors.

Aug

25

New Orleans, from Anthony Tadlock

August 25, 2007 | Leave a Comment

I just returned from a short vacation in New Orleans. Despite what the media imply, it is not a dying city, nor dangerous for visitors. The French Quarter is still beautiful and vibrant, although less crowded. Restaurants are generally keeping pre-Katrina hours and the food is as good as ever. Residents, shopkeepers, tour guides, and wait staff are gracious and eager to help, without being servile.

I just returned from a short vacation in New Orleans. Despite what the media imply, it is not a dying city, nor dangerous for visitors. The French Quarter is still beautiful and vibrant, although less crowded. Restaurants are generally keeping pre-Katrina hours and the food is as good as ever. Residents, shopkeepers, tour guides, and wait staff are gracious and eager to help, without being servile.

Unlike in many struggling tourist spots, I didn't feel like a "walking wallet." If the recent market turmoil has left you frazzled and confused, get flat in your speculative positions and go long Nola!

Aug

24

Ten Percent, from Jeff Sasmor

August 24, 2007 | Leave a Comment

Doesn't this whole 'yes, we've had the long-awaited 10.00% correction so now it's time for the market to go up again' seem very, well, scripted, for lack of a better word? Just seems all too pat.

Doesn't this whole 'yes, we've had the long-awaited 10.00% correction so now it's time for the market to go up again' seem very, well, scripted, for lack of a better word? Just seems all too pat.

It's like watching a TV crime drama, where it's the character you see for a few seconds near the beginning of the show who turns out to be the bad guy in a 'surprise' twist at the ending.

If you take the tack that it's the person who's somewhat invisible in the plot, but who was actually shown, even if only for a moment, then you can usually guess the culprit before the first half of the program is over.

Somehow I think that's what's going on here.

Aug

24

The Calendar, a Query from Jeff Rollert

August 24, 2007 | 1 Comment

What's the likelihood of folks' "painting the tape" on a very illiquid Friday 8/31? This applies less to liquid securities than equities or index futures. As an example, I have seen it done in high yield — or at least it appeared to have been done. Call reports and other mark-to-market/model issues will be interesting to watch, especially TRACE.

Larry Williams replies:

You believe in that? I never did. Suspect it's an old wives’ tail. But I’ve never been that close to the fire. If they paint the tape, buy to drive prices up, they have increased their longer term exposure for a momentary gain.

Aug

24

Book Review from Bruno Ombreux

August 24, 2007 | Leave a Comment

I just finished reading, How to Lie with Statistics, from Darrell Huff. This is a short book and a very pleasant read with a quaint charm. It was written in the 1950s when everybody was smoking, as attested by numerous illustrations dotting the pages.

I just finished reading, How to Lie with Statistics, from Darrell Huff. This is a short book and a very pleasant read with a quaint charm. It was written in the 1950s when everybody was smoking, as attested by numerous illustrations dotting the pages.

It is targeting a mainstream readership, the "average man," as they called him back then, not the scholar at ease with numbers, trained at avoiding bias. It is about spotting the lie whenever someone is presenting statistics to support a sales pitch, be it from Madison Avenue or Capitol Road. This can be extended to Wall Street and whatever thoroughfare is traversing the Cambridge, Berkeley or Stanford thin air academic publication hubs.

This book is best summarized by its last chapter, which provides a checklist for finding lies in statistics:

- Who says so?

- How does he know?

- What's missing?

- Did anybody change the subject?

- Does it make sense?

Who says so?

If a toothpaste manufacturer is showing numbers about how great his toothpaste is compared to competition, they may not be as reliable as the same numbers from an independent assessor.

How does he know?

This is about how numbers were collected. Sample bias. The author makes an interesting point that I haven't read very often: a poll is subject to three biases. There is the classical population bias; there is also a bias in the poll questions, which are a sample of possible questions about the subject; and there is a bias in the answers, which are but a sample of the possible opinions of the person answering the poll.

What's missing?

Very often it is the denominator. We keep hearing about how huge the US debt is. It is huge in absolute terms. Divide it by GDP, and it is not as frightening in line with other countries.

Did somebody change the subject?

A statistical non sequitur. The price of rice in Africa has been going up; this is a sure sign of inflation in the USA.

Does it make sense?

I read recently that four percent of French males and one percent of French females were switchers.

Steve Ellison adds:

On the topic of books, I recently spent a couple of hours in the investing section of a Borders bookstore trying to get a sense of the dominant memes that might be influencing the "public play", as Bacon put it.

Three themes, each of which I saw in multiple books, were:

- Trend following is the path to profits

- A disastrous day of reckoning is coming

- Commodities are better investments than stocks

Aug

23

Interesting Architechture, from Rich Bubb

August 23, 2007 | Leave a Comment

After last year's Sunday morning Stock Talk in Central Park, my wife and I decided to visit the NYC Guggenheim Museum. We had no idea they were exhibiting Zaha Hadid's brilliant works. After seeing her work for five seconds, I thought she was the 22nd century literal reincarnation of Frank Lloyd Wright.

Today I was cruising through her website and found language and building designs.

Aug

23

Newspapers, a Query from Monty Humbert

August 23, 2007 | 2 Comments

What newspapers and periodicals are helpful and useful from an investing and speculation perspective? My favorite reads include WSJ, Barrons, Economist, and Investors Business Daily.

Larry Williams replies:

Mother Jones, Foreign Affairs, National Enquirer.

And, never forget what Mark Twain said:

If you don't read newspapers you are uninformed. If you do read newspapers you are misinformed.

Alan Millhone adds:

Alan Millhone adds:

On a related topic, I have several newspaper stamps in my stamp collection, some of which will fill the palm of your hand. They were made in 1865 by the National Bank Note Company — there are eight of them and luckily I have all eight in my collection. In 1875 the size was greatly reduced and printing was done by the Continental Bank Note Company, the American Bank Note Company and then later by the Bureau of Printing and Engraving. The face value of each stamp runs from a few cents to sixty dollars, but as collectors' items they are obviously much more valuable now.

Aug

22

Changing Cycles, from James Sogi

August 22, 2007 | Leave a Comment

The cycles are changing. The Fed cycles are switching to an accommodating and easing stance. This has many predictive implications.

The cycles are changing. The Fed cycles are switching to an accommodating and easing stance. This has many predictive implications.

The Fed has started rate-cutting programs 10 times since World War II (11 times, if you include Friday's rate reduction.) In the six-month period after the first cut, the Standard & Poor's 500-stock index advanced by an average of 11.0%, two percentage points better than the average 9.0% price increase in all years since 1945. 12 months after the first rate cut, the S&P 500 gained an average of 18.6% and posted an increase in nine of 10 cases. (source Business Week 8/21/07).

The lowered discount rate seems to have stemmed the tsunami. Just as the recent hurricane dissipated just before hitting my island, the down swing of the last month seems to have run its course, and the T and S action is back to the steady up-tick without last week's wild swings. The airdrops of liquidity are being bid after less than one percent. Bidding depth is returning along with new daily highs. Execution and trade style needs to accommodate the swing.

While volatility clusters it cannot survive too long without dissipating; like the hurricane as it is caused by imbalance. Nature abhors an imbalance. The volatility measures like the VIC are dropping fast. Weather and markets have much in common and oddly seem to correlate in time. Witness Katrina and current weather anomalies such as tornadoes and floods in Brooklyn.

Changes afoot in the yen carry with yen over .87. Perceptions about China, Europe, and real estate seem to be occurring. There must be many more signs of the changing cycles.

Aug

22

Toxic Waste, from Alan Millhone

August 22, 2007 | Leave a Comment

I just looked over the state-by-state list and noted many former landfills are now golf courses. The average person in the US throws away 3.5 lbs. of garbage a day. I visit my local Waste Management landfill in Parkersburg, WV with regularity with construction debris from my jobs and am charged $34.05 per ton for dumping, plus a fee for being "out of watershed" because I cross the Ohio River from Ohio to dump there.

I just looked over the state-by-state list and noted many former landfills are now golf courses. The average person in the US throws away 3.5 lbs. of garbage a day. I visit my local Waste Management landfill in Parkersburg, WV with regularity with construction debris from my jobs and am charged $34.05 per ton for dumping, plus a fee for being "out of watershed" because I cross the Ohio River from Ohio to dump there.

It is unreal what you see dumped. One time I backed my dump beside a Dept. of Natural Resources truck that was loaded with dead deer. Really nice to be there on a hot August day!

Aug

22

Magic, Misdirection, and Markets, from Easan Katir

August 22, 2007 | 1 Comment

I find myself in Las Vegas having just finished a four-hour lunch with a master sleight of hand artist, Armando Lucero. After the dessert dishes were cleared, he showed us — not 30 feet away on a stage, but 30 inches in front of our noses, illusions that strained my belief. The climax was when he found a card in a clever way that anyone at our table has only thought of.

I find myself in Las Vegas having just finished a four-hour lunch with a master sleight of hand artist, Armando Lucero. After the dessert dishes were cleared, he showed us — not 30 feet away on a stage, but 30 inches in front of our noses, illusions that strained my belief. The climax was when he found a card in a clever way that anyone at our table has only thought of.

If one man with a deck of cards can baffle so completely, what massive and incalculable deception might be afoot in the armies of traders with their teraflopping supercomputers?

Aug

21

Sleights of Mind, noticed by Clive Burlin

August 21, 2007 | Leave a Comment

The following is an excerpt from a New York Times article:

Secretive as they are about specifics, the magicians were as eager as the scientists when it came to discussing the cognitive illusions that masquerade as magic: disguising one action as another, implying data that aren’t there, taking advantage of how the brain fills in gaps - making assumptions, as The Amazing Randi put it, and mistaking them for facts.

Sounding more like a professor than a comedian and magician, Teller described how a good conjuror exploits the human compulsion to find patterns, and to impose them when they aren't really there.

"In real life if you see something done again and again, you study it and you gradually pick up a pattern," he said as he walked onstage holding a brass bucket in his left hand. "If you do that with a magician, it's sometimes a big mistake."

Aug

21

Flight to Quality, from Chris Cooper

August 21, 2007 | 2 Comments

I have noticed that my trading systems suffer whenever there is a so-called "flight to quality". By this I mean not simply that the stock market is down, but that all "risky" assets are suffering uniformly as funds are redeployed toward safer instruments. When everything starts to trend is when I get in trouble.

What is a good list of indications that we are in such a regime? I would like to recognize this within the day, not days after it has begun. I can think of a few possibilities for what I would call an FTQ indicator:

- Simultaneous rise in strong currencies, such as CHF and perhaps a couple of EUR, GBP, JPY.

- Change in the spread between government bills, notes, and bonds, and the equivalent duration commercial paper.

- Large jump in intraday correlation between interest rate instruments and currencies.

- Dramatic sector rotation in equities.

FTQ happens when some market participants start to panic. I guess what I am looking for is an early-warning panic indicator.

Philip J. McDonnell writes:

To Mr. Cooper's list I would add:

1. The VIX

2. The VIC (increased range in the SnP)

3. Large positive correlation between diverse assets possibly due to margin calls even if the swoon starts with alt a debt it spreads to S&P, silver and soybeans because of cross market liquidations

4. The ratio between the S&P (quality) and the Russell 2000 (lesser quality)

5. The SPY (stocks) / TLT (bonds) ratio

Aug

21

Wall of Worry, from James Sogi

August 21, 2007 | 2 Comments

Worry is in the air. Concern over financial collapse is in the news. The sky is falling. Markets are down. The circle of life and markets needs a period of reconstruction, of regrowth. Thirty percent more bidders are joining the queue.

Worry is in the air. Concern over financial collapse is in the news. The sky is falling. Markets are down. The circle of life and markets needs a period of reconstruction, of regrowth. Thirty percent more bidders are joining the queue.

The year is positive. The market is almost six percent off its lows of last week. It is difficult to hold. Many worry whether the rally will last. What are the mechanics of the wall of worry? The Rose Garden Theory provides that markets are the social adjustment mechanism and prevent excess of politicians in upcoming election from giving clues as to timing. The idea that the market must provide for its own upkeep by the powers that be shows how knocking price down provides a profit by year end for the strong.

The timing during the summer holiday gives time for the process over several months and to accomplish the maximum haircut when players are out of the office and vulnerable. The current rally is the flip side of the "weak longs" bailing out. Only the strong are left to reap the harvest. As the markets rise additional players jump on board. As old highs approach, those that bailed try to get back on so as not to miss, but again at the wrong time, behind the form. The maximum pain trade, buying at point of maximum pain, seems to have been a reflection and antidote to the common natural reaction. Avoiding the herd down and up is always very hard for social creatures. It’s like walking up stairs during rush hour in the New York subway.

The formulae for Sharpe ratio, Black Scholes, Fed model have a risk-free factor keyed to the risk-free rates. The risk-free yields have dropped affecting the pricing of options, Sharpe ratio, and Fed model, all in favor of equities and giving equities a higher future expectation. What does all this subprime credit stuff have to do with equities anyway?

Larry Williams remarks:

"The quants froze" is what one of the most successful presidents of a hedgefund told me regarding what happened at his firm at the recent low. He had to step in for his traders — they just locked up. Great indicator!

Aug

21

Put it on the Train, from Todd Tracy

August 21, 2007 | 1 Comment

"Put it on the train; see if it gets off at Westport" is an old saying on Madison Ave. told to me by an editor at the Princeton University Press. My Father did just that for decades, get off the train there that is.

"Put it on the train; see if it gets off at Westport" is an old saying on Madison Ave. told to me by an editor at the Princeton University Press. My Father did just that for decades, get off the train there that is.

Westport in the 70s didn't have its commercial flare. Now mansions are cultivated where apple orchards and strawberry fields once were. The downtown where George Washington dismounted was home to a certain cigar smoking American woman of German ancestry by the name of Sigrid Schultz.

Today a plaque rests at the approximate spot where Washington relaxed in a little tavern. Behind the Episcopal church where this tavern once stood was a ramshackle home covered over with weeds and shrubbery. Bowing limbs shielded from view the little white house exempt from the Westport tax roles. Before I was born Sigrid had cut a deal with the town that upon her death they could make the property a parking lot but that until that day she would pay no property taxes. They hadn't counted on her living for so long. After all, the crippling effect of Nazi bullets had begun to take its toll upon her once ravenous beauty. Just as she had outsmarted Hitler, so too this suitably located hamlet.

Sigrid had written a book in the 30s which she was very proud of. She was proud of being the first women Chief of Central Europe for the Chicago Tribune. There was a network in the Berlin of the 30s that included my biological Grandfather. Officially employed by the U.S. Treasury Dept., my Grandfather was part of that clique of Americans milling about Berlin during the buildup. He made haste for Paris and eventually shipped back to the States. Sigrid stayed on to report the battles under another name and date.

Now, the full circle of coincidence. My mother, being an investigative reporter and political editor for the Hartford Courant, would run errands for Sigrid as the arthritis had confined her to bed. More often than not I was schlepped along for the ride. My mother had her hands full with armored car heists, suspicious murders, provocative human-interest stories (for which she was nominated for a Pulitzer) and dinners with Ella, another cigar smoking woman who happened to be the Governor of Connecticut at the time. My Mother didn't smoke cigars, however she thought it was cool.

A couple of times per week my mom would bring me to see Sigrid, as she was my mother's mentor. We had a good laugh when we realized the namesake as Sigrid recalled stories of the war and a woman's role in a man's world. That biological relation had been a friend many years before. There are coincidences in this world.

I was rather precocious at the age of ten and would invariably skip out of the house, say hello to Clarence, Sigrid's minder, and wander over to the river, past the old Westport Library on the corner of Post and Main. At that very corner there was a park bench where heroin addicts would nod out. It was called Needle Park and yes times have changed.

Walking across Jesup Green where the hippies were sprawled out mingling with the black leather clad bikers, I would skip up the little hill overlooking the Saugatuck River to the spot where the new Library now stands. It was a landfill back then and the funny thing is that they had a magazine section even then. A huge metal container filled with thousands upon thousands of discarded magazines. At ten years old there was only one kind of magazine that I was looking for.

Now 30 years later I make the journey in reverse. I have a workshop across the street from the old landfill, next to the site of the Yankee Doodle Fair (100 years and counting). I cross a little bridge from the fairgrounds over to the library parking lot. I do a quick scan of the printed headlines in the magazine section. I stroll across Jesup Green, no bikers. Pass by Needle Park, entrance to Guess Jeans (good tenant). I make my way into the old library building for a Starbucks. I stride along the river behind main street, over to and across the parking lot where Sigrid had her house and gardens right up to an adjacent lot behind the church where I manage residential modernizations to the only house in Westport with five legal kitchens.

In the most important ways, Westport is still the same. Train to NY, good schools and low crime. Not having movie theaters downtown has changed the dynamic along with the fact that most moms and pops are gone. But there were always women's clothing stores on Main Street.

Aug

21

Panics and Bubbles and the Wisdom of a Crowd, from Russell Sears

August 21, 2007 | 2 Comments

To paraphrase from an interesting article, the jelly bean in a jar experiment and predictive markets prove that the power of the crowd will beat even the experts, hence the markets generally are efficient. The exception is when the experts are given too much air time biasing the crowds opinion distorting the cancellation of error in divergent opinions.

To paraphrase from an interesting article, the jelly bean in a jar experiment and predictive markets prove that the power of the crowd will beat even the experts, hence the markets generally are efficient. The exception is when the experts are given too much air time biasing the crowds opinion distorting the cancellation of error in divergent opinions.

Two things this teaches:

1. We should value all opinions

2. The more we know the humbler we should be to this

Adam Robinson contends:

With respect to the esteemed Mr. Sears, guessing stock prices is nothing like guessing jelly beans.

In the first place, there's a risk associated with markets that does not exist with jelly beans. But more important, in markets the "guesses" of participants influence each other, with all sorts of feedback loops that do not exist at state fairs guessing jelly beans.

It would be interesting to see whether this second factor can be tested in the field: run the counting contest but post each of the guesses, in ranked order, along with high guess, low guess, median guess, average guess for easy overview, and see whether that information influences participants' guesses (for comparison, two groups could be tested, one with access to the information and one without).

A prize and a penalty could also be attached to guesses, and for a further dimension, see whether and how much participants would be willing to have access to the "market" information.

Russell Sears notes:

The predictive markets (the markets that predict things like election results, winners of Oscars, etc) do run very close to the proposed modification of the jelly bean test, with the added bonus that the "bettor" must be willing to lose and hence think he has an edge, like the stock markets.

One example is of a multiple choice of one out of four listing of the one not being in the old music group The Monkees. If 7% know all, 5% know two, and 5% know one, and rest don’t have a clue. With all votes random, besides the choices eliminated due to knowledge, it takes a fairly small number of players to get it right. This would work even if the "expert" did not have perfect knowledge, such as the Oscars, or the stock market.

Aug

20

Mastery of the Game of Checkers and the Market, from Alan Millhone

August 20, 2007 | Leave a Comment

I’ve been reading with interest the definition of the word "master" in many situations. Looking through my checker library I found two books of interest and will make some observations. In 1909, William Timothy Call wrote his Vocabulary of Checkers. It is a small hardbound book that has become quite scarce. I decided to find the word 'master' in it and was surprised not to find that word listed, but the word 'expert' was instead.

I’ve been reading with interest the definition of the word "master" in many situations. Looking through my checker library I found two books of interest and will make some observations. In 1909, William Timothy Call wrote his Vocabulary of Checkers. It is a small hardbound book that has become quite scarce. I decided to find the word 'master' in it and was surprised not to find that word listed, but the word 'expert' was instead.

But on the first page of his book is found the word “abecedarian.” Maybe it’s a new Scrabble word for many of you. Call’s definition: One who is learning the rudiments of the game; a new beginner. The stage of advancement are: abecedarian, beginner, novice, student, advanced player, expert, champion. I note the obvious absence of the word “master.”

Call says about the beginner on page 16 of his work: One who has started to learn something about the game as a science. The abecedarian becomes a beginner, then a novice, then a student.

Novice according to Call: An advanced beginner who has not had much experience in the game as a scientific diversion, no matter he may have indulged in it as an amusing pastime.

Thumbing through the book I find a term I have heard on some occasion: “scrub.” It is a colloquialism to designate the large class of adroit players who are not rated as experts. Tyro: A beginner or novice.

On page 190 of Learn Checkers Fast, we find the word “master.” Comparatively few players ever reach this high station in the game. Actually, the name is misleading, as no expert has ever really mastered the game to the extent he was immune to defeat. The author lists the following classifications of checker players: novice, amateur, near expert, expert, junior master, master and grandmaster.

Student: One who occupies an intermediate position between the novice and the expert class, particularly one who follows new play (lines of published checker play) with a critical eye.

My observation: I can see where beginners in the market (as myself) would begin at the bottom of the list and hopefully through study, listening to others, making mistakes, keeping a hand written manuscript, etc., would gain knowledge and put that knowledge to proper use in the market.

Aug

20

Time Cover: The Genius Problem, from Steve Ellison

August 20, 2007 | 5 Comments

Time magazine's cover story is about the Davidson Academy, where my son and daughter are students.

Any sensible culture would know what to do with Annalisee Brasil. The 14-year-old not only has the looks of a South American model but is also one of the brightest kids of her generation. When Annalisee was three, her mother noticed that she was stringing together word cards composed not simply into short phrases but into complete, grammatically correct sentences.

After the girl turned six her mother took her for an IQ test. Annalisee found the exercises so easy that she played jokes on the testers. In one case she not only put blocks in the correct order but did it backward, too. Angi doesn't want her daughter's IQ published, but it is comfortably above 145, placing the girl in the top 0.1% of the population. Annalisee is also a gifted singer. Last year she won a regional high school competition conducted by the National Association of Teachers of Singing.

Annalisee should be the star pupil at a school in her hometown of Longview, Texas.While it would be too much to ask for a smart kid to be popular too, Annalisee is witty and pretty, and it's easy to imagine she would get along well at school. But until last year, Annalisee's parents, Angi, a 53-year-old university assistant, and Marcelo, 63, who recently retired from his job at a Caterpillar dealership, couldn't find a school willing to take their daughter unless she enrolled with her age-mates. None of the schools in Longview, nor even as far away as the Dallas area, were willing to let Annalisee skip more than two grades. She needed to skip at least three as she was doing sixth-grade work at age 7.

What's needed is a new model for gifted education, an urgent sense that prodigious intellectual talents are a threatened resource. That's the idea behind the Davidson Academy of Nevada, in Reno, which was founded by a wealthy couple, Janice and Robert Davidson, but chartered by the state legislature as a public, tuition-free school. The academy will begin its second year Aug. 27, and while it will have just 45 students, they are 45 of the nation's smartest children. They are kids from age 11 to 16 who are taking classes at least three years beyond their grade level (and in some cases much more; two of the school's prodigies have virtually exhausted the undergraduate math curriculum at the University of Nevada, Reno, whose campus hosts the academy).

Among Davidson's students are a former state chess champion, a girl who was a semifinalist in the Discovery Channel Young Scientist Challenge at age 11 (the competition is open to kids as old as 14) and a boy who placed fourth in both the Nevada spelling and geography bees even though he was a 12-year-old competing against kids as old as 15. And last year the school enrolled another talented kid from a town 1,700 miles away. Annalisee’s mother moved with her to Reno so she could attend the school (her father was working in Longview at the time).

Aug

20

What Causes Economic Growth? from Denis Vako

August 20, 2007 | Leave a Comment