Jan

2

Thoughts on EUR for January 2023, from Alex Castaldo

January 2, 2023 | 2 Comments

I do not focus on foreign currencies in my trading. And there are people here, such as Mr. John Floyd, who are far more knowledgeable about FX. So some of you may find these thoughts a bit simplistic; keep in mind I am an amateur!

I believe that a factor that makes a country's currency attractive to investors is the success (or lack thereof) that foreign investors have investing in the country in question. We can gauge this success by using ETF's that specialize in particular countries. For example SPY measures the performance of stock investors in the US, while EZU tracks investing in Eurozone stock markets.

What do we see? In recent months EZU has been performing better than SPY. For example in the last 6 months of 2022 SPY had a total return of 2.03% and EZU 9.56%. For 2022 as a whole SPY -18.38% and EZU -16.67%, two ugly numbers, but EZU did better. (These numbers will change between now and Dec 31, but not by much).

In my view this kind of comparison (especially given that Europe did poorly the previous few years, so it's a remarkable turnaround) will attract additional US investors to Europe, strengthening the currency. That is why I am bullish on EURUSD for the month of January 2023.

Bud Conrad responds:

Your logic is that if the stock market of a country rises, the currency of that country will rise in exchange rate. In the early days of this Speclist, the chair would ask me if I had "counted" the historical experience, which you cite for the last six months and year, but usually you need something like three cycles of inflection to get confidence.

The more usual comparison for currency strength are the Interest Rate Parity, using the futures market expected exchange rate and the difference in Interest rates.

And there the International Fisher Effect, also described here.

Often international traders look at trade balances for the country that has a trade surplus to be more attractive so the currency might rise. Trade surpluses mean they are a lender and not in debt to other countries. The US is the world's largest debtor, but the currency has been doing well.

John Floyd writes:

Doc makes the broadest, cleanest, and most accurate point about what drives currencies: what are expectations for return by BOTH domestic and foreign participants, and how does that drive investment flows into equities, FI, FDI, etc, which shows up in the BOP and Capital Account - on the other side of the ledge is the Current Account and the Errors and Omissions.

Admittedly I don’t know much about currencies and this is the area I know least about, but flow data is well researched and document by many at banks, independent research firms, IIF, IMF, BIS, etc. One challenge is it is often very much lagged, so Doc’s idea of looking at actual market instruments makes sense, and this is often particularly useful for emerging markets.

Capital account flows can fund a current account deficit for a very long period of time. Look at the US now or look at the Asian Currencies pre the crisis: errors and omissions become important given capital flight, particularly EM. Think Russia pre ’98 and Swiss bank accounts, etc.

As Doc well knows infinitely better than me, we need some more data and this can all be tested.

More broadly, outside of equity flows, Bud’s point of interest differentials will drive some capital flows. Also consider FDI from Europe to North America to diversify dependence on European energy costs and to friend shore manufacturing capacity.

And I would be remiss to not mention Italy (sorry Doc). Italy is in a Euro straightjacket that not even Houdini could get of. ECB is tightening with inflation at 10%, Italy 150% debt to GDP, Italian per capita GDP is barely higher than when joined Euro in 1999, Italy needs circa $250 billion in funding in 2023, 10 year yields in Italy up from 1 to 4.5%, all Italy issuance past few years was essentially bought by the ECB. This is not politically sustainable. Just look at the evolution of recent German politics. The ECB’s TPI is there but is intended for temporary dislocations and will require Italian political concessions. Oh and Italy is 10x Greece and the world’s 3rd largest sovereign debt market behind the US and Japan.

Read the full discussion here with additional contributors and charts.

Jul

9

what could make it go up? real wages? repatriation of companies? a better modus operandi how employees are treated? those graphs should be on a front page of WSJ and not how to send more arms to Ukraine.

A reader writes:

How about ending or at least curtailing the welfare state. It is mind boggling to count all the handouts and public assistance that otherwise middleclass people drink up. Look at various housing assistance programs, prescription drug benefits, free breakfasts and lunches. It has gone from helping the truly misfortunate to subsidizing at least half the country.

Alex Forshaw comments:

What's the issue? It went from 63.5% to 62.5% in 7 years. Probably entirely explained by avg age / boomers (who stick around longer than priors) finally aging out.

Nils Poertner responds:

why? there is monster public and private debt plus tons of entitlements…and then we are at the beginning of a long rise in yields (nominal and real) - so better to have a high participation rate. same as in Europe.

Zubin Al Genubi writes:

Its demographics and those are hard to change. Immigration would help, as would education.

George Zachar clarifies:

please only look at the PRIME AGE labor force participation rate, ages 25-54.

Larry Williams offers:

Prime age rate looks strong:

Bud Conrad asks:

So now what does this mean? The almost pre pandemic participation level suggests that the populace is finding jobs, and that the economy is not in such bad shape.

But I see:

- Inflation wiping out savings, Real wages declining from inflation, Rising Rates changing basic discount rates making stocks vulnerable, Demand destruction from rising prices. Import prices rising faster than US CPI, (CPI is cooked books lower than reality closer to 20% per year), Deglobalization.

- Many of the bubbles popping in the last six months: Stocks, Bonds, Cryptos, High yield debt, Housing starting down, and the reaction of collapsing Consumer confidence, Earnings in contraction.

- Debt overhang indicating generational Sovereign Debt collapse (Over 100% of GDP in US).

- Failure of Fed and its sham of fixing inflation, which it can't. Probable Fed "pivot" this fall and returning to money creation to fund the government deficits. Displeasure with the government.

- Tax receipt decline from less income (Bill Rafter's detailed work). International conflict, (Russia, China).

Is the participation rate more important or a better indicator or more predictive than all the other problems?

George Zachar adds:

and the cleanest measure imnsho is the prime age employment/population ratio, which sidesteps the issue of who is technically counted as being in the 'labor force'.

the labor market is quite healthy. otoh, pmi new orders are collapsing. the former lags, the latter leads.

Aug

10

Is Turkey a good buying opportunity now for holding 5 years?

August 10, 2021 | Leave a Comment

Leo Jia asks:

Any thoughts on the prospect of Turkish economy? Is Turkey a good buying opportunity now for holding 5 years?

Larry Williams clarifies:

Is the Turkish economy about the same as the Turkish stock market?

Some references:

The CIA World Factbook: Turkey/economy

iShares MSCI Turkey ETF (symbol: TUR)

Nils Poertner responds:

as we know from other EM countries, listed equity can be really a good play - even with fx tanking. see Latam and many Asian countries. a vast "play" on the USD (as lots of banks are financed in USD - and EUR) and a bet on the faith in the current regime. cap controls an issue.

understanding EM requires study of previous bull-and bear mtks for EM mkts itself- doing the tedious work - building implicit knowledge over time, cycles, mass psychology, whateever it takes - it is worth it, Jia and a lot of fun - as one learns from it and can share with others.

John Floyd writes:

Larry has somewhat taken the words out of my mouth on the economy and stocks in Turkey. I would expand on that somewhat given the unorthodox nature of the current Turkish administration and the expanding Taliban presence and thus likely growing chance of further friction with the US, following recent and historical comments by the head of Turkey on the topic.

As economy and FX it does sure have the potential to get things right and turn for the better. But, the odds of that happening and the headwinds against it seem rather large at the moment. The current path is one of further unorthodoxy in policy and leadership combined with expanding debt that will likely lead to a default or restructuring and FX going from 8.6 north of 10.

Reserves are tenuous at best, local capital outflows a perennial risk, and the need to continue to pump up the economy through credit, tourism headwinds given COVID, current account deficit of 5%, etc…

Given the circa near -20% returns for the Turkish indices there may be some gems within the them with careful selection, as is needed in China given the P-like oligarch crackdown there as the aim by X is to stay in power for life and control data and tech to do so.

James Lackey suggests:

As John clearly said the news risk..what about the derivative of the big Mac index and or the hot dog stand.

If I'm forced to value a stock on foreign exchange correctly, I'd go to Turkey, rent a flat, and open a food stand and sell Harley Davidson T Shirts. The McDs index of brands is HOG. I can sell merchandise like a roadie at a show and let's use the most recognized brands in the world.

Sell shirts for 6 weeks and my guess is you're going to learn exactly what's going on.

Larry Williams adds:

Bring lots of NIKE stuff to sell.

Jayson Pifer provides local insight:

Fwiw, I can offer some boots on the ground perspective. I spend a few weeks a year in Turkey and have done so for the past 15 years, missing last summer due to covid however please take the below comments with an appropriate amount of salt. Each time the conversations come up on investing in real estate there. And each year, I come away boggled at the lack of progress and steadfast in keeping money away.

If I were to hazard why the Turkish economy isn't more than it could be, I would suggest that it is the general absence of faith in any of the government constructs. Without commenting much on their current 'populist' leadership, I mean to say that the average person has little faith in the police, courts, and laws and work around or without them. (plied with a bit of scotch and I could relate some Keeleyesque tales of my encounters there with these systems ![]() )

)

Absent true legal financial recourse, trust stays in small personal circles that are difficult and slow to grow and this has various and deep side effects. As an example, if one were to meet a VP of a bank in the US or UK, you might assume they had interviewed for the role from a range of candidates and/or had been in the role for a while and knew the business and their area. One would likely be correct in those assumptions. In Turkey, you do not have that assurance as they will probably have gotten their role through a circle of acquaintances. They may be qualified or not, but they are almost certainly in somebody's inner circle.

The low trust and inner circle workings are seen in both the political and business environments. When new leadership comes in, it is typical and considered normal to bring in their trusted group, reward them for their loyalty and displace anyone they do not trust. Partisanship there compounds the issue, similar to the partisan wars in Google but with more serious consequences if one supports an out of favor party (eg. non-AKP).

Wrt the stock market, my impression is that it's a lottery. There is money to be made, for sure, by smarter and luckier people than me. But the risks are real.

I don't have numbers, but my anecdata shows a worsening brain drain with talented turks leaving the country and those that have returned are struggling.

Taking a further step back for the five year horizon posed originally, my impression like Mr. Floyd's is that Turkey has headwinds and not much to stop it from falling. My questions are what could change to reverse this trend? A change in leadership is often cited, but it would not create an overnight increase in trust. I could barely speculate how long it might take, but would guess decades if all went well. While it's not exactly fair and I'm out of my historical depth, I compare it with Iran when it went down the path of Islamic leadership in '79. How will Turkey not fall into the same trap?

Theodosis Athanasiadis comments:

Historically real exchange rates have been a good predictor of emerging market economies and equities through the mechanism of cheap exports, labor, external investments etc. they are a form of valuation for the whole economy. I see them currently at multi-year lows which has been bullish for equities in Turkish lira for the long term.

John Floyd responds

Yes, on real rates in Turkey that is true and can be seen in the standard OECD PPP, but that has been like that for ages and you need the positive catalyst for change…..move to orthodoxy one way or another….monetary, fiscal, and geopolitics…should gradually grow confidence in varying degrees and speeds and drive capital flows in a positive fashion if it occurs and given valuations you can find some gems I am sure…perhaps on well capitalized companies that can benefit from the inflows and cheaper FX…plenty of meals for a lifetime if you look at Argy, Venny, Russia, SA, Zimbabwe, etc…

If anyone is bored, I did an interview on Turkey last August - it somehow has gotten just under 20k views that highlights both contemporaneous points at the time and some of these longer term issues.

Alex Forshaw writes:

Erdogan is in bed with the asset heavy industrial elite of Turkey… this is China but with very ineffective capital controls (mainland Chinese stock performance has been terrible for 12+ years btw, altho indices don't include juicy dividend yields). They're all massively overleveraged, and basically long and wrong The only way is devaluation / financial repression (forcing inflation >> cost of capital) until they deleverage… but Erdogan can't really let them deleverage because the economy would implode, Turkey is poor, the opposition is highly organized with high recourse to violence (Kurds), so Erdogan would be dead. So they just keep building and building, but who's going to come?

Seems to me that Turkey is uninvestable until Erdogan is gone…but he's a de facto dictator…so he can't go.

Leo Jia offers more data:

New home sales are down lately, which may be caused by the pandemic:

Turkey: new home sales

But existing home sales shot up sharply in recent years:

Turkey: existing home sales

Nov

6

My Main Inquiries, Coming Out of This Election

November 6, 2020 | Leave a Comment

Alex Forshaw writes:

1. Is it possible to determine what % of dead people (alt'y, what % of people over 110 years old) voted for Biden over Trump, where they live, and when they last voted? AFAICT, so far, the dead demo is 100 percent for Biden, and turnout was up at least 100 percent over 2016/2012. This was a devastating rebuke to 160 years of shameless GOP voter suppression.

2. More dead voters have voted for Biden than have shown up for all of Biden's campaign rallies, combined. Outstanding GOTV by the Biden campaign here, especially considering that they had no GOTV for most, if not all, other demos.

3. Dead Lives Matter! Just from sampling social media, dead voters are clearly the fastest-growing demographic in the United States, and Biden's outreach to this underserved minority was amazing. What policies & voter outreach should GOP'ers consider in order to compete for this underserved demographic?

K.K. Law writes:

If there is a way to quantify voter frauds such as dead people's votes, illegal people's votes and people casting votes multiple times and destroying GOP votes, that would be great. I am sure all these happen but just don't know the magnitude.

Oct

21

Howard Jarvis is Rolling Over in His Grave

October 21, 2020 | Leave a Comment

Alex Forshaw writes:

CA's property tax system is idiotic and the most dysfunctional in the country.

Property taxes are assessed on purchased basis, not on assessed value. So somebody who bought a home 30 years ago for $10,000 could pay 1/10th (or less) the property tax of someone in an identical house next door.

It has placed a huge relative tax burden on recent home buyers. It has subsidized the aging hippies who bought into CA 30 years ago, who have subsequently voted to throttle housing supply in the name of environmentalism for their own benefit

Kim Zussman writes:

Your thesis is based on commonality with losers and supplicants. The only ones subsidized, ever and always, are the socialist organizers.

Check back with us when you're at the end of your earning years. Without 13 those who always know better would squeeze you out of your house when you are old and useless to them. Even if you followed the rules, paid your taxes, and paid off the mortgage, there is always marketable pathos in the unending supply of hungry mouths to feed.

Alex Forshaw writes:

I'm a raging conservative and I think taxes suck. But if you're going to buy into the idea of a property tax, levy it in a way that's transparent and affects people on a logical and consistent basis. The CA property tax system charges nothing to people who bought 30-50 years ago (who are sitting on gigantic paper gains) and does the opposite to new buyers. It's totally inequitable, capricious, and creates lots of terrible incentives, more so than any other vanilla state tax that I can think of.

Larry W writes:

Howards point, and success of prop13, was the unfairness to people that had lived/worked in homes for year and could not afford the tax hike until they sold those gains are illusory until sold and the state was taxing a value the owner never pocketed

BTW Howard was pretty amazing ball of energy, perhaps I’ll share some stories of being on the campaign trail with him one of these days

Mar

15

People Are Out and About, from Tyler McClellan

March 15, 2020 | 1 Comment

I live in NYC and the idea that everyone has dramatically changed their lives is…simply not what I observe. People are out and about in all the restaurants bars and shops.

Alex Forshaw writes:

The same is true in the Bay Area Although in the past week, Uber/Lyft drivers bookings are -50% week on week as WFH has taken hold.

Jan

22

Dysfunctional San Francisco Grist, from Alex Forshaw

January 22, 2020 | 4 Comments

I moved to SF with my wife and baby 7 months ago from NYC. My wife is a member of local online mothers' club, Golden Gate Mothers' Group (GGMG), in which local moms pay $75/year to access a forum to share notes around good restaurants / neighborhoods / sites / activities / etc, and generally help each other out.

I moved to SF with my wife and baby 7 months ago from NYC. My wife is a member of local online mothers' club, Golden Gate Mothers' Group (GGMG), in which local moms pay $75/year to access a forum to share notes around good restaurants / neighborhoods / sites / activities / etc, and generally help each other out.

Here was a barely-surprising story related by one of the GGMG moms: We live on a very steep hill, where parking is perpendicular to the curb. Last Saturday night, we were at our neighbor's potluck party - well attended with lots of older folks and young kids, including my toddler and baby. We went home at 8 to put the kids to bed. Our car was parked in front of our house at the top of the hill. Around 10, I was asleep, but my husband heard a crash - didn't think much of it. The next day, we looked out to see my car parked at a 45-degree angle. I thought, Oh no, someone hit it. Yes, indeed. Some jerk totaled my car (which I just paid off last month). Damages are estimated to be $9,000 and the car's only worth $11K. Of course there wasn't a note. People suck. But then, the neighbors rallied and IDENTIFIED the car using security footage. A guy in an SUV was backing down the hill, rammed into my vehicle, switched drivers (probably drunk), and literally sped away back up the hill. An Uber was on the street at the same time and captured his license plate number. We filed a police report and included all this information, including the license plate number. The cop said the SF police force is understaffed, no one wants to work there, and yeah, they're not going to investigate. So this drunk driver, who totaled my car, who could have run down my children, can just go on enjoying life. So, please take note - if you hit a parked car (or a moving one, or even a pedestrian), don't worry. No one is ever coming after you. I hear this type of story a lot. "I was the victim of a property crime. I did the cops' job, tracking down who did it and collecting proof, all on my own. I presented a heap of evidence to the cops. The cops shrugged and very politely responded, 'F**k off.' AFTER I did their job for them!"

Part of SF's urban breakdown is surely due to the idiot politics of its elected officials. The SF police basically can't incarcerate anyone for anything short of attempted murder, especially after SF just elected Chesa Boudin (former Hugo Chavez speechwriter and adopted son of Bill Ayers / Bernadine Dohrn) as the new DA, whereupon he fired the 7 assistant DAs for incarcerating too many people. But the cops also just don't seem to care.

As far as I can tell, these policies and government are despised by 80%+ of working liberal San Franciscans, who strike me as fundamentally rational people, aside from attributing 90% of all weather readings to either global warming or, if it's a colder day, climate change.

But nothing changes and nobody expects anything to change.

If you live in SF, it sucks. But the moral of the story is, you couldn't dream of a better example (in the US) of the moral and intellectual bankruptcy of woke liberalism in action. Every Democrat presidential candidate outside of Biden and Bloomberg wants to do to the United States what the Democrats are doing to San Francisco. If one of the idiot Democrats wins the nomination, Trump should have a full-time staff based here to log all of the stupidity that SF puts its taxpayers through. They will come up with a very original, just shocking enough, 100%-true attack ad every week.

Jan

5

Book review: Why We Lost, by Daniel Bolger (Lt. Gen, ret.), from Alex Forshaw

January 5, 2020 | Leave a Comment

My main Christmas reading this year was Why We Lost, published in late 2014 by retired Lt. Gen. Daniel Bolger. Examining the ROI of US government spending has become a weird passion project of mine. What better place to start than the Afghan/Iraq campaigns, which have cost the US somewhere between $2.5 trillion (Pentagon) and $6.5 trillion (dedicated antiwar interest groups) over the past 17 years, all to turn Iraq into a restive Iranian satrapy?

My main Christmas reading this year was Why We Lost, published in late 2014 by retired Lt. Gen. Daniel Bolger. Examining the ROI of US government spending has become a weird passion project of mine. What better place to start than the Afghan/Iraq campaigns, which have cost the US somewhere between $2.5 trillion (Pentagon) and $6.5 trillion (dedicated antiwar interest groups) over the past 17 years, all to turn Iraq into a restive Iranian satrapy?

I picked this book for several very specific reasons. One, Bolger is a prolific author with no apparent career agenda (he retired in 2013), political ambitions, or axes to grind–a combination that's unheard of within this subgenre. Two, it would've been written for publication before ISIS had really put itself on the map (late 2014/early 2015), which recast the Iraq debate into a finger-pointing exercise at the expense of dispassionate analysis. And three, the book's mere title takes the intra-military debate over What Went Wrong to a place most men in uniform won't go.

The book is very readable, and gives the feel of being the middle of dozens of episodic life-or-death firefights, each of which illustrated a larger success or shortcoming of the American strategy. For me, this vivid episodic detail bolstered the author's authority, but grew repetitive after a while.

In his strategic analysis, Bolger is much more nuanced than the title suggests, comes to some interesting conclusions, and, along the way, highlights some very surprising facts. I was astounded to learn, for example, that "the US military did not torture anyone" at Abu Ghraib. (Bolger doesn't hesitate to highlight other episodes of US torture, intentional killing of civilians, etc.) US troops did photograph some prisoners in compromising positions, strip some of them naked, have some dogs bark at them, and intimidate them. In the most infamous case, a prisoner was put on a box with fake electrodes attached to his fingers, and was told they were real and he'd be electrocuted if he stepped off the box, but the electrodes were fake and nothing actually happened to that prisoner. All of these things would fit semiawkwardly into the US military's prescribed environmental manipulation for interrogating suspects without physically harming them or placing them under such duress that they'd say anything escape the situation. According to Bolger, the worst that could be said about what actually happened at Abu Ghraib was that some of these intimidation/degradation incidents weren't related to any specific interrogation.

Bolger also refuses to point fingers at the easy scapegoats. President Bush gets measured credit until the 2006 Iraq Surge, when every general who'd fought in the Iraq theater had told Bush to a) cut American losses and get out, or b) even if the US was to stay, in many respects the larger US footprint was becoming as much of a long term liability as much as it may be a short term asset. Bolger was ahead of his time in assessing the Surge to be both an impressive tactical success and a major strategic blunder. He's more critical still of Obama's subsequent "Afghanistan surge," which recycled the same mediocre Iraqi formula into a theater where it was even less effective, had no justifiable long-term value once bin Laden had been killed (May 2011), and was badly hamstrung by idiotically restrictive revisions to rules of engagement which, up to that point, had been generally OK.

Stan McChrystal's handling of the Afghan theater gets particularly terrible reviews: ridiculously restrictive rules of engagement; McChrystal holding himself/the Coalition hostage to a treacherously ungrateful Afghan president (Karzai) who never would've existed without American backup; and a blatant protection racket in which the US was getting extorted by every side of the Afghan conflict, worst of all by Karzai.

On the issue of Iraqi war rationales (terrorists vs. WMD), Bolger writes as if the military never took WMD seriously: everyone knew that Saddam had no real, functioning nuclear program, and while chem/bio weapons play well in Hollywood doomsday scenarios, in reality, they require circumstances far too specific and consistent (in terms of humidity, wind direction, extremely stable delivery or storage en route, etc.) to be really effective outside of massive artillery barrages of chemical weapons. In terms of capable terrorist organizations, on the other hand, Bolger repeatedly notes that Iraq hosted a genuine vipers' nest of capable, well-equipped Sunni terrorist groups which the Americans had largely liquidated by 2005.

With the benefit of hindsight, Bolger writes, the US had completed 99 percent of its job in the war on terror, at a fraction of the original cost, by 2004 (or even 2003, after the Taliban had been kicked out of major Afghan population centers). Al-Qaeda itself had been completely destroyed aside from bin Laden himself and a few couriers. Many separate groups did claim allegiance to al-Qaeda and attempt to imitate it, but they weren't operationally coordinated. Over time, the Coalition footprint became its own casus belli against the US. The Americans were always occupiers, regardless of how much money they threw around for victim compensation or reconstruction. This was compounded, in Bolger's view, by chronic Sunni Arab double-dealing (always shaking America's hand while stabbing it in the back) and Afghan cultural treachery, in the sense that honesty basically has no place in Afghan culture.

It's difficult for me to take some of this criticism seriously. Was the US supposed to call it quits in Afghanistan in 2003 without killing bin Laden or al-Zawahiri? Would al-Qaeda proper have remained infirm had the US stopped hunting him down? No way. At the same time, if not surging in Iraq in 2006, and getting out of Afghanistan in 2011, were strategically such obvious calls, where was the military criticism of Obama's Afghanistan strategy? Enlisted personnel couldn't make the criticism, but retired personnel could (and in the case of the Iraq surge, loudly did).

Anyway, I'd strongly recommend the book for students of contemporary US military history.

Stefan Jovanovich writes:

If one looks at American deployments for what they are - largely bloodless training exercises, then Winning and Losing has to be evaluated by what the wargaming produced. In the first Gulf War, the U.S. military capabilities were larger in scale but no greater in technology or ability to engage at the sharp end than the French or British. The victory in Kuwait was greeted almost with relief - see, the Americans can actually win something. Now? The distance between the actual warfighting abilities of the U.S. and the rest of the world is now a chasm. The only comparison that fits is Nelson's Navy. The French, Spanish and Danish navies were still capable of challenging the British in the Caribbean and Baltic in 1780 and even 1790. By 1810 the British Navy was the largest physical and financial enterprise on the planet by a factor of 10.

I am not saying this is a good thing; I am saying this is what happened. The U.S. can win the war in Afghanistan tomorrow, as the President has said; we would just have to turn the place into Carthage. That we don't says nothing more about "victory" than the fact that the British Navy chose not to destroy every American ship on the Atlantic in 1813 because there was still the little matter of Napoleon's continental empire to deal with. Britain spent the next half century enjoying the financial dominance that its Navy had won. The dollar is the world currency now in large part because the Americans have that same military monopoly that Nelson and the Admiralty had created.

Jul

8

Help for Fed Heretics, from Stefan Jovanovich

July 8, 2019 | Leave a Comment

I think Ms. Shelton's odds for surviving the attacks by CNBC et. al. will improve significantly if she adjusts her Lafferite theology. In a old C-SPAN interview I watched this morning I saw her making the same claim that Boris Johnson made this week on his hustings tour: "lowering taxes raises more revenue".

I think Ms. Shelton's odds for surviving the attacks by CNBC et. al. will improve significantly if she adjusts her Lafferite theology. In a old C-SPAN interview I watched this morning I saw her making the same claim that Boris Johnson made this week on his hustings tour: "lowering taxes raises more revenue".

Clearly, it doesn't; taxes are the government's revenue, and lowering them means that the government has less to spend. This confusion has been a chronic problem for "conservatives" ever since Professor Laffer first scribbled on his napkin. It seems to have created a fog even for Laffer. How else can one explain his support for a single tax rate across all income levels? As a policy and political platform "lowering taxes" is a pure folly equal only to the defense of "capitalism". (Ms. Shelton commits that sin as well; she is an advocate of "democratic capitalism" which is itself an oxymoron.)

Where the progressives are instinctively right is in their belief that the rates should increase as income brackets go up. Where the progressives are and always will be disastrously wrong is to believe that the fundamental purpose of a tax system is to inflict punishment on the rich, to be a collective act of revenge against those who make the most.

A flat tax rate ignores the common sense truth we all see around us: the successful are much better than the poor at making money and the rich are much better at making money on their money. All the babble about the American dream ignores the obvious fact that the power law applies to enterprise just as it applies to the ability to hit baseballs 400 ft. All of us who love the sport can play the game, but only a very few can make the All-Star Game roster. What produces more wealth for both the government and the people who pay taxes is the lowering of TAX RATES if you get the proper shape for the stair-step of brackets and rates. The current tax code has gone a long way towards achieving that result; that may explain the seemingly inexplicable–how both net wages and tax collections can continue to grow in the United States even as they flatten out elsewhere.

Rudolf Hauser writes:

The Laffer curve idea that lowering marginal tax rates increases revenues only works to the extend that it makes it cheaper to pay the tax than the costs and losses incurred in trying to avoid the high tax rates. In regard to the incentive impact on growth, it is best not to focus on how much the tax rate is reduced than on how much after tax income is increased. The incentive impact of reducing the tax rate five percentage points is a lot more important when the initial marginal rate is 90%, thereby increasing after tax income by 50%, than it is when the initial rate is 50 and the increase in after tax income is only 10%. When the cut applies to the capital gains tax rate, there might initially be a larger increase in tax revenues, as many long term investors might tax advantage to sell their stocks that they only held for so long because of the tax consequences of selling and/or to repurchase the shares to establish a higher cost base should the tax rate be increased again in the future.

But beyond that, there is a conflict of interest between the wealth of the nation and the wealth of the government. Lowering rates does increase the incentive for greater growth. But if the average tax rate is only 20%, the growth in the economy has to increase five-fold for the tax cut to result in more revenues. That is unlikely in most cases. It also has to be remembered that many people are by nature game players, that is they are very competitive and like to win. Why would a billionaire have any incentive to work hard? After all, he has more money than he could ever need to satisfy his consumption needs? It's because gaining the most money is like winning the most points in the game. So even when the government takes a large share of the gain, there is still the competition to have the most points, that is after tax profits and wealth, even with the reduced incentives. Naturally, that only applies to some people. Many will behave like the British aristocracy of old and become a leisure class. But it does explain why we were still able to have economic growth when marginal tax rates were so high in the 1950's, along with the fact that the various loopholes, etc. reduced the actual tax rates that were paid.

Stefan Jovanovich replies:

I hate to disagree with RH, especially this week when I am enjoying a biography of Gresham that I owe to his recommendation. My view may be distorted by my experiences as a low-rent criminal, both with and without a law license. My direct observation of both clients and customers is that they all followed the Gompers rule where taxes and penalties were concerned. ("What does labor want? We want more schoolhouses and less jails; more books and less arsenals; more learning and less vice; more leisure and less greed; more justice and less revenge; in fact, more of the opportunities to cultivate our better natures, to make manhood more noble, womanhood more beautiful, and childhood more happy and bright.") Taxpayers want to pay LESS at every possible rate. When rates are confiscatory - at the rates that Democrats have traditionally favored - taxpayers literally stop being taxpayers. They find ways to categorize their wealth and income so that it is not subject to any rate at all. They don't look for marginal reductions; they look for escape.

The ability to escape explains the seeming paradox of the 1950s when private incomes and wealth grew even though the legacy tax rates of WW II remained in place. Thanks to the magic of non-recourse debt financing, the effective tax rates paid in the 1950s were no higher than they were in the 1980s after Reagan's tax cut. The 1954 Tax Act became the bible of the 1950s whiz kids in Beverly Hills whom I was lucky enough to go to work for in the 1970s and it made their fortunes. (The reference is deliberate: Tex Thornton's Litton Industries offices were just down the block on Little Santa Monica.)

When Jerry Ford, the economic moron who succeeded those other economic morons Johnson and Nixon, signed the 1976 tax reform act, he not only did me out of a job (no more 8-1 write-offs on real estate, oil & gas and movie deals); he also raised the effective tax rates on the wealthy to where they had been in the late 1940s. It produced exactly the same kind of inflation that Truman's vetoes and price freezes had done. The Federal government collects roughly 21% of the national income. The individual income and employment tax share is about 17%. It is rumored that Kevin Hassett's magic calculator at CEA produced a Laffer ziggurat (it is never a curve) that begins at 5% and ends at 30% for all personal incomes; its output was 20% of the national income - 3% more than the current collections. The result was never published because it would be the ruin of the Republican Party.

Integrating Social Security and income taxes would be even worse than Bush's "privatization"; and they would never be able to get it through the Rich's brains that their loss of exemptions and carve-outs would be more than offset by a simple 30% top rate. But, to be fair to the Rich, they know - from long experience that a simple stair-step is a Congressional impossibility. What would Representatives do is they could not offer special rules for wool growers and weavers? Still, as a thought experiment, it is intriguing.

Alex Forshaw writes:

Getting back to Stefan's original post, I don't understand how anybody can take seriously someone who for tight money in 2011-13 who's simultaneously in favor of loose monetary policy today. (Stephen Moore, Shelton, others) You can be for one or the other but not both, unless you 'evolved' to a completely different philosophy… which rarely happens honestly in my observation.

Stefan Jovanovich writes:

Let's go back to RH's point as well. If monetarists think that "money supply" is both the fulcrum and the lever for Archimedesian economics, we taxistas tend to have the same certainty that tax rates move everything. They don't.

For me Ms. Shelton's heresy is the belief that legal tender in any form can be a "store of value". I also find her giving Jefferson and Madison credit for putting the U.S. dollar on "the gold standard" the worst kind of Ron Paul historical fiction. If credit is to be given to Virginia Presidents for fixing the dollar by weight and measure, it has to go to the first and last of the Founders - Washington and Monroe.

Rudolf Hauser writes:

The monetarist point is simply that an excess of money ( the accepted means of exchange and those liquid assets held that are considered reasonable means of quickly obtaining the means of exchange at minimal cost) results in an attempt to dispose of the excess, which initially results in more nominal purchases of other assets and goods and services and subsequently inflation as the sellers of those goods and services realize that the increased production was not really economical. When there is a deficit of such liquidity, the opposite happens. If income and nominal wealth gains go to those who have a low propensity to consume, the increase may mainly be reflected in higher prices of existing asset, both physical and those financial claims behind such assets. If monetary policy is erratic and causing erratic inflation, the increased uncertainty as to the future might deter future real economic growth potential. Aside from that, monetary policy has negligible impact, if any, on real growth potential. Another mechanism is the increase in money driving up prices of financial assets, thereby lowering interest rates. That in turn can shift some purchases of durable goods financed on credit and investments likewise financed on credit to be shifted forward, whereas a deficiency of money can work in the opposite direction. Stefan believes that the central bank can control interest rates. But a central bank can only keep interest rates low when it has created an inflationary situation by continuing to accelerate the rate of monetary growth. When that stops or the public expectations catch up with what is really happening, those interest rate will rise. As the central bank is not the only creator of near forms of money, the demand for money created by the banking system can change for numerous reasons such as opportunity costs, the speed of transaction settlements, inflation expectations, and financial uncertainty. One impact of financial uncertainty is reduced access to quick credit and less confidence in the ability to convert such assets as commercial paper into money that can be used to settle transactions quickly and at minimal cost is diminished. Shifts in the demand for money depend on public desires for the amount of money they wish to hold and are not well understood or necessarily constant.

In contrast the main impact of tax policy is on economic growth potential. There are both temporary shifts as changes and expectation of changes in tax policy can drive income recognition forward or backward and the far more important permanent effects. To the extend producers try to pass on tax increases to consumers, it might have some inflationary impact as industry shifts the tax burden on to consumers, but since the income of consumers is not increased, eventually it should mainly have a real impact on the purchases of goods and services.

Mar

24

It Doesn’t Get Any Easier Than This, from Ralph Vince

March 24, 2019 | 4 Comments

"If the best horse always won, this stuff would be so easy," the Old Frenchman used to tell me.

But it sure helps when the best horse is running against a field of nags. Similarly, I don't recall, in forty years, what appears to be a easier setup than right now in equities.

Not even close. Ever.

Let's start with the backdrop, which is decidedly negative at least in terms of recent news - global slowing, yield curve inverting, earnings trailing off etc.

Great.

Now, let's just look at the reality. In terms of what's going on with rates–a contrived situation on the short end, entirely inconsistent with quality spreads which have narrowed in the past couple of months, considerably, even with respect to junk.

Whatever global slowing was going on in 2018 has decidedly and abruptly turned. Since the first of the year, Shanghai is up 24%, Oil is up 27%. Global Slowdown?

To think we're still in a slowdown period is to miss what's already going on.

Employment in the US is very strong, evidenced again by this past week's jobless claims, and should be evermore evident after the next monthly jobs number where it should become clear the February number was a shutdown-induced aberration.

In fact, the basic indicator I keep (and many others do, of essentially the same thing, in various forms) of commodities prices relative to employment has again turned up–and at already high levels. This is very strong.

Earnings, here we are, end of Q1 and month-on-month S&P earnings are still growing. That;s right, despite the 21 1/2% growth in earnings on the S&P 500 last year, and the fact that they were to be contracting by now, are STILL growing, month-on-month.

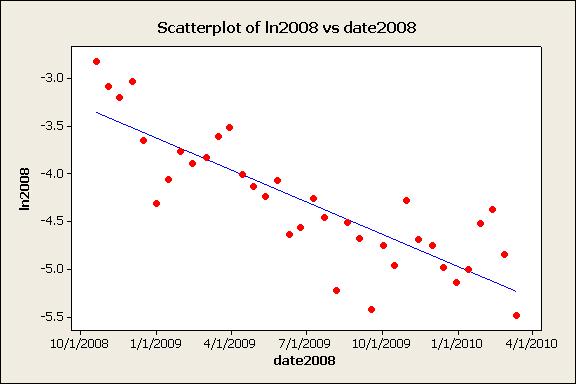

The sentiment is still quite negative, and there are actually people out there who, for whatever natural-glass-half-empty they harbor, think the December lows will be challenged here. In December, we saw sentiment readings in surveys, in the press, in put/call ratios and in VIX futures that were negative along the lines of what we saw in late 2008! Such readings occur, typically, before protracted gains, bull runs that last many months. The following chart shows the 13 week rate-of-change of the S&P, as percentage, as of this Friday's close.

We haven't seen a move this vigorous, up and outta here, since 2009 Q2. Does this look like a market about to roll over? All of this backdrop, historically, set the stage for a prolonged bull run–which we are again in the early throes of it would appear.

"Roy's Red" –the six week coefficient of variance (I call it that after my late friend and fellow trader, Roy Klopper, who cooked it up with me years ago trading value line futures on hourly data) has again dipped below .10, indicating an imminent move (i.e. we're coming up and out of this congestion we've been in the past month or so–a congestion which has had an upward bias, indicative of strength coming when we break up out of it). The last time we had a reading this low in Roy's Red, this imminent of a move, of an impending and imminent trending move, was in early October last year.

The volume bars of Friday (tight, profitable-quarter-ending-stops being played) indicate one should be a buyer on weakness Monday - even if things collapse Monday, you gotta be a buyer. ESPECIALLY if you can be a buyer below Friday's close (I don't know if we'll get this chance, or if Monday is a further collapse, on heavier volume–I doubt it, the setup is such that Friday should be made up and then some in the coming week). Even if things work a little lower, the bigger picture is so strong right now, that backdrop story so counter to what's actually going on in the numbers, and the forecast so strong here, and the daily so set up for a buy I just don't recall things ever being easier than right now.

Could I be more unequivocal?

Alex Forshaw replies:

Ralph,

A few devil's advocate arguments:

1. Shanghai composite was trading at 10x forward earnings 3-4 months ago with aggressive supply side government stimulus. that has historically always been a good time for a trading bounce. There hasn't been a material shift in on the ground economic fundamentals in China.

2. By my math the SPX is trading at 17x 12m forward EPS. The range has been 15-18x in the past 3 years. The SPX traded over 18x forward earnings 4 times in the last 100 years — 1929, 1936, 1999, and january 2018. In each of those occasions, the SPX's sharpe ratio for the following 12-36 months ranged from quite bad to historically atrocious. so unless there's a massive expansion in earnings in the near term, the SPX is not valued attractively right now.

3. Earnings season just ended. There won't be material movement in the "E" for another month.

4. While the yield curve doesn't historically correlate with fwd 12m equity returns, how do forward 12-month returns look when we are at least 6 years into an economic expansion and the yield curve has flattened? It's one thing for the yield curve to flatten 2 or 3 years into a bull market. but 10 years? Seems like the context is materially different from a lot of the past contexts around this statistic, although I haven't studied it closely.

5. Employment is a coincident to very slightly leading economic indicator, but hasn't it decelerated very markedly recently?

6. Europe is clearly slowing down dramatically again. China has had a valuation bounce but economic activity there is still quite weak judging from company earnings reports and anecdotal. The US has managed 3.1% GDP growth with a 5% deficit/GDP that dwarfs the OECD average.

7. Why would you pay 17x ftm eps for 3-5% estimated earnings growth? 17x for 20% eps growth (12% organic), a la 1h18, is one thing…

8. Given the volume of corp borrowing and debt issuance, and the peaking of the current rate cycle, why wouldn't the next downturn be much worse than the 2008 one? I think the "next downturn" risk is maybe 20% in next 6-9 months, but even if it's 20%, why would you pay 17x for that?

Ralph Vince writes:

Alex,

All good points.

I'm considering valuations with respect to competing assets more so than historically, the notion being the investment dollars move someplace. Is the the "right" way to asses these? I don't know, it's how I usually try to look at it, but time will tell.)

Consider the long bond which is selling at a "multiple" of about 35 here vs the S&P 500 (whose earnings, as I say, are STILL rising; actual earnings, not future prognostications of events which have not transpired) of 21.48 (S&P500 PEs were riding above the long bond "multiple," dipped down and touched it around 88 and again in 95, by mid '05 the S&P500 PE dipped below the bond multiple, and has remained there ever since save for a period in 08-9 where the PE for stocks went haywire for several months. So one cannot say that the bond multiple naturally belongs above stock PEs, but they have for nearly a decade and half).

That's with the VERY rich US yields, relative to the rest of the world. The Bund, of course….a different animal here. Investment dollars flow someplace, the US, with earnings still gaining (despite the incredible gains of the past 14 months or so) look very attractive by comparison.

Employment is extremely healthy, so much so that wage pressure is finally returning. By my measures, last month was an aberration caused by the shutdown. A more accurate assessment, a proprietary one with respect to equities prices reveals: We're not even close to a sell by my employment measures.

On the more near-term, the next few weeks should see an end to this congestion we've been in for a month or a little longer in equities prices, per Roy's Red. Whereas it COULD be to the downside, I don't see it, the technicals (and sentiment) are acting far more lie 2009 Q2 here. Further, the pattern of volume (which is no different than how one might have read the tape 35, 40 years ago or before– only now we have the benefit of seeing bigger swaths of time, e.g. I look at yearly, monthly, weekly volumes as well) are ALL bullish here, all buy any weakness here. If I had to rely on jut one indicator, this would be it.

Alex Forshaw writes:

To me, the S&P 500 is trading at almost the same valuation as it was in January 2018, except

1) S&P estimated earnings growth is 3-5%, instead of 20%

2) the 1yr/10yr spread (the most predictive of all the yield curve spreads) is slightly negative today, vs +80bps a year ago

3) all macro fundamentals have decelerated everywhere, and the rate of negative surprise has dramatically accelerated

4) SPX earnings yield minus 10 year yield (attached) is inline with its average over the past 10ish years, although if you go back further, it looks more favorable

5) there is no prospect of further policy stimulus until after the 2020 election, which remains a complete wild card, and seems like a "lose/no-win" coin toss for investors (the possible outcomes being untethered socialist idiocy or the dysfunctionally mediocre status quo)

In my experience, stocks-vs-bonds valuation logic is not very useful when stock valuations are rich by their own historical standards. It would have said to be aggressively buying through 2017/1h18 (if you were looking at the past 20 years of data) and the sharpe ratio would have been quite poor. It only takes 1 bad stretch to seriously derail one's financial career…

Ralph Vince writes:

Re: "there is no prospect of further policy stimulus"

The transportation bill, likely to be proposed very soon, and highly stimulative. Think QE5. Giant barrel of uncooked pork.

China, among other things, agreeing to buy 500bln/yr ag and etc over next 6 years(my cheap seats guess), highly, HIGHLY stimulative (2 1/2% yr on a 20 trln economy, before any kind of a multiplier, which is at least 2, as that is just export, but goes into either consumption or investment 1x over 12 months, and that accumulates going forward).

Effects of "New Nafta" not yet felt online. We could go on and on hereon these various recent changes all of which are stimulative.

If you take away energy, and go back to our being a net importer of oil, and take away the repatriation effect of the recent tax bill (and AAPL agreeing to invest 350 bln, and Foxcon, and etc) , we would likely be at a GDP deficit here. Things haven't really gotten going yet is my point, but these are real numbers coming online. I don't for the life of me understand Atlanta Fed GDP projection.

Steve Ellison writes:

Since 2010, the S&P 500 has not strayed too far in either direction from the level implied by a 2% dividend yield (see attached chart). From this perspective, the S&P got a little ahead of itself in 2017, and the 2018 correction overshot. In fourth quarter 2018, there was a plausible argument that the required dividend yield ought to adjust higher (implying the trend line should be pushed down lower), but the recent move in 10-year yields to multi-month lows seems to have taken that possibility off the table for now.

Dividends have been growing at roughly 8% per year recently.

Oct

19

Polling Report, from Kim Zussman

October 19, 2018 | Leave a Comment

They say the market is upset about the jump in bond yields but maybe she's anticipating a premature return to socialism

Stefan Jovanovich writes:

If I thought there was any reliable direct connection between elections and speculations, I would be tempted to join LW and you other clever traders and bet my "system" - which does better than average at guessing political horse races. I don't because, if there were any such link, I would not be able to pretend to be an expert in such company. You guys would already know the odds down to the precinct levels if that mattered.

I think, in fact, you all do know what matters regarding politics and money. Now that I am 60% of the way through the House "swing" districts, I are learning what the markets have already predicted: Jim Jordan is going to be the new Speaker of the House of Representatives. When that happens, the Federal budget and the Treasury's operations are going to be subject to the approval of the 21st century successor to John Sherman; and the shock is going to be that the national debt will be brought home. The taxpayers are going to become the Federal bond holders just as they did during and after the Civil War; and they are going to want tariffs and "sound" money to protect their investments, even as Confederate paper (aka Chicago municipal bonds) is allowed to evaporate.

Larry Williams writes:

If the new speaker shrinks debt stocks will get hit hard. Deficits are very bullish for equities.

Alex Forshaw asks:

Larry, why do you say that/how do you strip out correlation vs causation in this? The blowoff 1998-2000 top occurred among budget surplus and deficits are inherently counter cyclical i.e. generally low in late cycle/high in early cycle (deficit as % of GDP biggest in 1981-83, during/after 2 recessions or 1 severe recession; 1991-93 after a fairly deep recession; 2002-03 after a recession; 2009-10 after a severe recession.) To the extent that the deficit is high adjusted for its place in the economic cycle (2012, 2018 ytd) it doesn't seem bullish. To the extent that deficits are unusually low cyclically adjusted (late 90s, 2007 arguably, 2015 arguably) it definitely does not seem bearish.

Larry Williams replies:

I don't think it is correlation but causation. Large deficits means lots of money floating around the hood. That translates to expansion, building–which translates to jobs, and that to consumer spending, and that to corporate profits. I'm traveling so lack data. The "one and only" Mr Vince may wade into this with data.

Ralph Vince responds:

25+ years ago I bought the Commerce Dept Database of 900 data items, and set u p a program (that would take two months to run, with a math coprocessor no less!) to examine each pairwise data set, and for each pairwise data set, to skew them +12/9/6/3/0…/-12 months, and record only those dataskew pairs with absolute value of correlation > some value (I forget which, but it was quite high).

One of the (many) dataskew pairs that filtered through very highly was that of federal deficits and economic growth (and broadly, we can stipulate that ROC of economic growth correlates to equity returns). The greater the deficits, the greater the market gains.

There were periods that did not fit this pattern, of course, it was not absolute (one out-of-sample period being the Robt Rubin era which was yet to transpire).

My guess is like the Senator's here; greater money floating around menas greater economic activity. I think it;s even a deeper causation than that. I would define it by saying that debt needs be repayed only once (if ever, it can also be perpetually rolled — the "problematic" nature of this is solely a function of rates. If manageable due to rates, it is virtually nothing. Further, even if rates become problematic, the yield curve itself provides an avenue of release — cue Rubin again), whereas the borrowed dollar can circulate multiple times.

So there is the multiplier effect of borrowed money vs the borrower's asset which is a one-time shot

If it weren't for borrowing, in particular the fractional banking system, we'd be in the year 1,000.

Jan

21

Short Interest, from Alex Forshaw

January 21, 2014 | Leave a Comment

The problem with Short Interest is that the data from the exchanges tend to be out of date. Right now the latest data I have is from December 31. - A Reader.

There are at least 2 services that plug into the back ends of 100+ HF's and basically derive a short interest with a 3 day lag (the time it takes to settle a trade).

Jun

17

Notes From China, from Alex Forshaw

June 17, 2012 | 1 Comment

It only takes 3 months (if that) to lurch from a bullish supermajority to a bearish supermajority as far as China is concerned. From a sentiment perspective it doesn’t get much more bearish than this. On our TMT buy side trip, there was 1 bullish contrarian. The most bearish person in our entire group was the analyst from CIC, the Chinese sovereign wealth fund.

It only takes 3 months (if that) to lurch from a bullish supermajority to a bearish supermajority as far as China is concerned. From a sentiment perspective it doesn’t get much more bearish than this. On our TMT buy side trip, there was 1 bullish contrarian. The most bearish person in our entire group was the analyst from CIC, the Chinese sovereign wealth fund.

The “policy cycle” promises to be much weaker now than before. The Chinese view the 2009-10 stimulus as a disaster and don’t want it repeated (or so they insist; after power has been transferred, incentives will change, and policy will no doubt follow.)

Chinese real estate transaction volumes have been recovering for two months. However, developers are not buying more land from city governments to replenish liquidated inventory.

The more connected a given investor happens to be with Chinese princelings and elites, the more bearish he seems. Nobody, and I mean nobody, knows how political power will be apportioned when the power transfer happens later this year. The Hu Jintao-Wen Jiabao “liberals” (to the extent that any Chinese faction has any accurate ideological label) seem to hold almost most, if not all of the cards, and the only question is how far they will press their advantage. The corrupt wealth accumulated by the underlings of Bo Xilai, Zhou Yongkang, Zeng Qinghong, and their many underlings, wants and needs to escape China ASAP, before the late-2012/early-2013 change of power.

The American EB-5 visa program, the fastest and most expensive route to a green card, is going nuts. (An EB-5 requires $500k of investment and 10 American jobs.) Canadian citizenship was considered highly preferable before, because it’s much easier to obtain, and Canada doesn’t tax non-Canadian income. But that door seems to have closed.

It seems like the “liberals” have compromised with the devil (the PLA) to determine the composure of the next Standing Committee. Over time the PLA, which has historically been underrepresented in political decision making bodies relative to the raw muscle at its disposal, took the side of the Bo Xilai-Zhou Yongkang nationalist-socialists in the factionalism within the Standing Committee. When Bo Xilai was in political limbo in late February, the PLA’s loyalty was judged extremely uncertain by Hu and Wen (resulting in an avalanche of headlines in People’s Daily and other organs, reminding PLA cadres of their allegiance to “the Central Military Commission *headed by Hu Jintao*”), giving way to a sense of imminent instability among Chinese elites.

The sense of imminent instability in early March is now gone, but the medium term power structure remains completely uncertain. Meanwhile, there is a growing sense amongst many Chinese elites that their the PRC’s system of governance is completely unsustainable. One of my friends, a Mainlander who went to the US for college, worked for a hedge fund, and now works for one of China’s largest internet VCs firms, bounced John Hempton’s “The Chinese Kleptocracy Is Like Nothing Seen in Human History” article around her Beijing office. Pretty much all of her Chinese friends – Mainlanders – agreed with it: the country is being looted; nobody has the power to stop it; anybody who tries to stop it is firstly a hypocrite, and secondly, on the cusp of political suicide.

Chinese people are also more skeptical than ever of everything, if that’s even possible. The Chinese wife of a Beijing-based American insisted that Bo Xilai is a hero and was an instinctive democrat, and all official accusations and “leaks” against Bo (11 murders; US$6bn laundered out of the country; wiretapping the entire Chinese Politburo) are fabrications. A very plugged-in American-born Chinese person was also sympathetic to Bo, believes Bo was no worse than average – and believes most of what has been reported about him.

Still others, also very politically attuned and connected, believe that although Bo’s liquidation was a very political power play, not only are the officially documented crimes real, but the true extent of his crimes has been significantly understated – the CCP has already lost a huge amount of credibility over the rumors which have leaked out and nobody has any interest in this spinning further out of control.

Most people shrug, say it’s none of their business, and go on with their lives.

Cheers,

Alex

Apr

23

The Bo Xilai Case, from Alex Forshaw

April 23, 2012 | 3 Comments

There are some intriguing financial aspects of the Bo Xilai case.

1. Bo Xilai racked up $26bn USD of debt while he was mayor of Chongqing. He supposedly ran the city's budget at 150 percent of revenues - *net of *the massive "sing red smash black" campaign which looted billions of private assets from the city. He is accused of moving $1.3bn overseas just for himself, most of which came during his Chongqing tenure.

2. Bo was definitely at the gangsterist extreme in terms of how violent he was (he and his wife are now accused of nine murders between them, and massive use of torture in Chongqing. These reports did not all suddenly emerge post-scandal to humiliate him - the FT and others have been running articles on the subject for months.) However, Bo was able to do this with a very large amount of protection within the Chinese government for a very long period of time, in both Dalian and Chongqing. None of Chongqing's debt was classified as at-risk. (In fairness to the PRC, you could make an identical argument against the one-third-ish of American muni bonds which aren't backed by a specific revenue stream like a toll road or utility fees

…)

Chinese people, imho, have known that stuff like this has been going on for a very long period of time (at nowhere near this level of organization or sophistication, however). I think this is a huge driver in Chinese capital flight - rich Chinese people hear scattered stories of insane corruption (well beyond any ethical pale) and simply do not feel safe at all, and export capital at a massive rate. If the best-informed insiders are selling so much stock in PRC Inc, why should anybody else be buying?

3. Bo Xilai's close business crony, Xu Ming, was president of the Dalian Shide conglomerate. He has vanished in PRC detention for a month and his business empire is unraveling.

According to the dissident site Boxun that has been leading the news cycle on this whole scandal, Dalian Shide's core business - petrochemicals manufacture - has been unprofitable for a very long period of time. The stock-speculation side of the business has been successful, and the conglomerate also engaged in a lot of land permit arbitrage (using the commercial nature of its business, plus close government connections, to gain land and land permits very cheaply. The overall financial status of the conglomerate is very murky, but appears to have required enormous amounts of debt in order to stay functional, and the debt recall has blown the firm up.

38 lenders had exposure to Dalian Shide. Before this scandal occurred, not a single loan to DLSD was classified as non-performing, even though many of the loans had no realistic prospect of being paid back. imo, this is a blunt example of why NPLs in the PRC are massively understated.

4. Even before the Bo blowup, DLSD's Hong Kong subsidiary, Gaoden, was trying very hard to access liquidity thru HSBC, RBS, and others in Hong Kong. So the house of cards was in some trouble even before its political risk premium exploded.

Sep

7

No Email Say Docs, from Dan Grossman

September 7, 2011 | Leave a Comment

In a survey of doctors on a website I follow, 80% of responding doctors answered no way would they allow their patients to email them.

In a survey of doctors on a website I follow, 80% of responding doctors answered no way would they allow their patients to email them.

This was the response I posted:

To the 80% of responding docs who say "No way": If you wonder why many patients develop major hostility to doctors' office procedures and to doctors themselves, and why the public is happy to stay silently on the sidelines while the government and insurance companies take over control of doctors' working lives, could it be that doctors (who for 100 years had control of their practices and refused to make them patient-friendly and efficient) have failed to enter into the 21st century? And regard it as perfectly acceptable to impose inefficiency, frustration and wasted time on patients by not letting them communicate with the doctor but requiring them to make an office appointment (probably 3 or 4 hours with travel to and fro, long office waits, etc) for every question or matter?

I see nothing wrong with a doc charging for email or telephone time. Those patients wishing to use email or telephone should be willing to pay the time charge, regardless of whether such charge is covered by insurance. But if our profession continues to lord it over patients by refusing to allow them what every other profession and all of modern life does, doctors will deserve what they get in the way of government and insurance oversight and regulation.

Charles Pennington writes:

Chiming in, that is a pet peeve of mine. What other profession won't take email? Lawyers, dentists, accountants, etc. all communicate by email, of course. Doctors make it even worse by making you communicate with them only via a voice-mail maze that begins with "If you are a physician, press 1; otherwise, your call is very important to us so please remain on the line…"

Russ Herrold comments:

I'm with the doc's here.

When the tears are flowing, everyone says they are willing to pay, but without getting into the business of FIRST AND AT THE ONSET, having a Retainer Agreement, unilateral right to draw it down upon presentation of statement, Mandatory Arbitration clause, deposit for fees in the Trust Account, all one does is lay a background for a fee dispute complaint or malpractice counterclaim to a suit to collect those fees. It's not gonna happen as a general practice. The doc is caught between the rocks of patient desire for immediacy and convenience; the professional obligation 'not to miss' something that in hindsight seemed obvious; and the fact that insurer reimbursement for web and email oriented 'treatment' lag.

Having had poor service (breaches of patient confidentiality, outright prevarication by nursing staff, and failures of delivery of test results repeatedly and after specific instruction) in the care of a wound, all since May of this year, from the standpoint of the patient, I want there to be a formal paper trail (not email; not call center notes in some database, forgotten and closed; not some other ephemeral media) … a well drafted letter explaining the issue, a file CC, and a cc to the supervising agency (hospital system privacy officer, nursing board, 'authorized provider' certification entity), and an equally formal response (or in its absence, proper escalation on my part).

Unreasonable, I know, but progress is made on the backs of unreasonable people.

The same goes for lawyering. If a client cannot keep and will not pay for an office visit, or meeting at other venue of their choice, to permit the open-ended probing that proper representation requires, they won't be MY client very much longer, as I cannot properly represent them.

Alex Forshaw writes:

The fact stands that interacting with doctors is a pain in the ass from the second you enter the door. They do not face nearly enough competition. There is no bigger beneficiary of protectionism in the entire country. The lack of competition has meant they face no evolutionary pressure. I hate "socialized medicine" as much as anyone but US doctors are as much culprits in their own demise as the tort bar and all of doctors' other favorite bogeymen.

George Zachar adds:

In my conversations with doctors, I've been told the potential legal and regulatory liabilities risked by patient email contact are vague and large, leading them to simply shun the practice.

Phil McDonnell writes:

Regular email is not a secure medium. Privacy regs hamper a Doc's ability to use email. Most will call you on the phone and/or write a letter with results. That is why expensive software with encryption is required that often the smaller practices cannot afford.

Gordan Haave responds:

Sure that's what they say. But it's BS. How is the fax or telephone somehow more secure than email?

If the issue is confidentiality, why is it that Lawyers will email you but not Doctors?

There is one other group that won't send emails: The IRS.

I am in the middle of a personal and business audit, and you can't email the IRS. It's very inefficient.

To me this is just further proof that Dr's collectively are not the saints they claim to be, but rather just a cartel that uses wildly inefficient systems to extract rent's from consumers.

Dan Grossman writes:

I am surprised that a few otherwise highly astute Speclisters so easily accept doctors' excuses for refusing to permit email. As a service to the medical profession and to our country (and in time for inclusion in the President's speech tonight as a new regulation under the Patient Protection and Affordable Care Act), I have drafted and present below a few simple groundrules that a doctor can require a patient to accept as a prerequisite for emailing him.

"A Patient wishing to email Doctor must indicate his acceptance of the following:

1. Complex or detailed matters require an office visit. This email is for minor procedural, scheduling and prescription renewal matters.

2. Doctor will attempt to look at reasonable numbers of emails as time permits but because of his busy schedule cannot commit to read or deal with every email. Any information Patient wishes to convey with certainty must be conveyed by other means.

3. Emails are not secure and should not include sensitive personal information. They will not necessarily be presevered or included in Patient's medical file or record.

4. Patient agrees to pay $20.00 for each ten minutes or part thereof Doctor spends reading or dealing with emails from Patient, regardless of whether the amount is reimbursable to Patient by his insurer. Medicare and Medicaid Patients unfortunately are not eligible to use this email since such programs do not permit email charges. (Doctor regrets this and asks that you please take up such inefficiency with the Government rather than with him.)"

With regard to 3, doctors or their office assistants can instead spend 15 minutes setting up free encryption, as others on the List have already pointed out.

Cheers,

Dan

Aug

29

The Fed at Jackson Hole, from Alex Forshaw

August 29, 2011 | Leave a Comment

This purpose of this post is to help me think out loud more than anything else, and as always, I would love anyone's feedback/discussion on any points mentioned here.

This purpose of this post is to help me think out loud more than anything else, and as always, I would love anyone's feedback/discussion on any points mentioned here.

Going into the Jackson Hole meeting, the market had a range of expectations around A) to what extent is Bernanke a "dove" and how urgent another round of stimulus would e; and B) to the extent that Bernanke's trigger finger is itching on the next printer cartridge, what political constraints might force Bernanke to stimulate less than what he'd prefer, given his extremely dovish writings, speeches, and policy history — and the surrounding context of 58 percent Greek government bond yields, negative Tbill rates, BNY offering negative interest rates on institutional cash deposits, and Italian government bonds beginning to trade lower despite the ECB's recent intervention?

The market sees Bernanke as an ideological dove, driven by a zeal to correct the great imbalances of the "global savings glut" (FX surpluses, and trade and employment deficits, spawned by artificially cheap Chinese currency). He can correct that imbalance by devaluing the USD; but quantitative easing is the only tool available to him to devalue the USD. The level of USD devaluation required to normalize China's balance of trade is extremely large (over 20 percent), and would require larger and larger successive iterations of QE to accomplish.

Since Bernanke believes a significantly cheaper USD is in the long-run interest of the country, and QEs of larger size devalue the USD more than smaller-size QEs, Bernanke wants to pursue QE only at such times when the political environment will grant him the most sweeping authority possible, to implement the largest QEx possible, to devalue the USD as much as possible. In other words, to seek further iterations of QE only at the points of maximum panic among the financial and political establishment. This strategy worked somewhat effectively in March 2009 and August 2010.

Having established a framework that Bernanke is ideologically extremely dovish, several events curtailed Bernanke's political latitude going into Jackson Hole 2011.

First, less than a month ago, the Republican frontrunner for president said it would be "treasonous" for Bernanke to enact a third round of quantitative easing. No Fed chairman has ever served in office against the wishes of the sitting President, and the Fed would lose market credibility if it were seen as not having the confidence of the President — or a realistic potential future President. Bernanke cannot simply ignore that comment. Even if it was a 'rookie comment' by a relative newcomer to the Republican race, the candidate (Rick Perry) was playing to a very strong strain of anti-Fed, anti-Wall Street, anti-financial establishment sentiment among the lower/lower middle class of the country, especially the white lower middle class that is the Republican Party's political backbone. Bernanke can't ignore that constituency, at least not indefinitely. Second, the Fed did announce a mini-QE by pledging low rates until mid-2013. However, that had little effect on the market when it was announced — suggesting the market would be unmoved by non-drastic Fed action. Thus, Bernanke would have had to do something drastic — further testing the Fed's political limits — to enact a policy that would suitably impress the market. Third, industrial commodity prices (oil, food, etc) remain relatively high, despite the recent hot money de-risking across all asset classes. Fourth, despite the -10% August, there is not a sense of panic, fear, or clamor for action from American investors outside of Wall Street. In 2010 the situation was arguably different — there was a more acute bear market in the aftermath of the flash crash. Fifth, Narayana Kocherlakota, whom the market perceived as a moderate dove, joined Fed hawks Fisher and Plosser in dissenting from the Fed's pledge to keep short rates near zero for another 2 years. The Fed has not had 3 dissents since the early 90's. This marked a high in terms of dissent against Bernanke's dovish inclinations.