Letters to the Editors

October 2006

Write to us at:![]() (not clickable).

(not clickable).

Please include your full name, and omit attachments

|

Daily Speculations |

|

| |

Letters to the Editors Write to us at: | |

Notice from the Editors: Competition for Contributions

Daily Speculations is dedicated to the scientific method, free markets, ballyhoo deflation, value creation and laughter. The material on this Web site is provided free by us and our readers. Because incentives work better than no incentives, each month we reward the best contribution or letter to the editor with $1,000 to encourage good thinking about the market and augment the mutual benefits of participating in the Daily Speculations forum. Prizes are awarded at the end of each month by the Chair and the Collab. Past winners30-Oct-2006

"Dessert", from Bruno Ombreux

Optimal Trading Strategies from Kissel and Glantz, contains interesting discussions about the trade-off between market impact and the opportunity cost of non-execution.

This NYSE paper about the limit-order book is interesting: I don't know what it is worth academically, but it is trying to validate TA through microstructure. A rare endeavor.

27-Oct-2006

A Fundamental Misunderstanding, by Donald Boudreaux

Editor, The New York Review of Books

To the Editor:

I've read few passages in your pages that are as mistaken as Bill McKibben's assertion that that "The technology we need most badly is the technology of community - the knowledge about how to cooperate to get things done.... We Americans haven't needed our neighbors for anything important" ("How Close to Catastrophe?" Nov. 16).

Each of us cooperates daily with countless others - neighbors, fellow citizens, foreigners - to ensure not only our prosperity but our very existence. My mind boggles at the number of people who cooperated to make available to me, for example, the shirt on my back. Cotton-growers in Egypt; fashion designers in Italy; textile workers in Malaysia; merchant marines from around the globe; investment bankers in Manhattan; insurers in Hartford; truck drivers along the east coast; department-store executives in Seattle; security guards and retail clerks in Virginia - these people and millions of others cooperated so that I might wear an ordinary shirt. Ditto for my house, my food, my subscription to The New York Review of Books.

For McKibben to say that "cheap fossil fuel has allowed us all to be come extremely individualized, even hyperindividualized" is to be blind to the amazing and vast system of cooperation that today spans the globe. Clearly, we have, in spades, "knowledge about how to cooperate to get things done."

Sincerely,

Donald J. Boudreaux

Chairman, Department of Economics

George Mason University

25-Oct-2006

Contributing to The Delinquence of Our Seniors, from Russell Sears

Every paycheck I am reminded of my ever growing contribution to the delinquency of the senior citizens of the USA.

I am not talking about their anti-social behavior. After all what more can you do to a generation that turned the romantical and socially acceptable "wine, women and song" into the brazen anti-social stance of "sex, drugs and rock and roll".

It is more about what they are becoming, a generation that is entitled to a drug to help them dream of sex, then another drug to have sex, and anti-social songs are becoming whines about the lost art of donut making, Krispy Kreme versus Dunkin Donuts, cream filled or jelly.

Who needs high priced mind numbing illegal drugs to corrupt the seniors, when the young can use high priced artery clogging donuts at donut chains full of social security collecting retirees.

The price of those little magical pills and that donut have less to do with BB and the price of oil than it does with SS slowly bleeding the productive.

Yesterday it was Greenspan's response to y2k and the twin towers, too easy money turning dream homes and 2nd luxury homes into inflated death traps for retirement saving.

Today, its BB turning demand shock in oils into high priced donuts, and no doubt more and higher priced drugs to wash the toxic donuts down.

While Friedman and the Feds may have shown that good monetary rather than fiscal policy can control inflation in the aggregate. Indeed reality has shown that it cannot control it for the specifics. And socialism paints the final ending bull's-eye of that inflation. Government subsidization of education, to medicare and Social Security ensures that the inflation that remains will be transformed and directed at the supposed citizen recipient of the Government generosity.

If you force me to give the seniors a dollar through the government. I will be able to ask the senior to pay me and extra dollar, since the governments dollar afterall was "free money". Then soon force the senior to pay 2 or 3 extra dollars, as the young play both sides of the street.

One dollar extra to appease the vocal youth full of resentment and couple extra dollars for the polictical supportive youth welling to buddy up to them and using their social leverage. Further, the government will soon only pass through 25 cents of that original dollar I gave them to give to the senior.

26-Oct-2006

Scaling Volatility, by John DePalma

Last month you wrote: "the movements of prices relative to high and low in the day has always struck me as highly non-random. holbrook working had a test for the range of prices based on the individual tick moves and number of transactions based on simulation. I believe the gist of the problem is more that the market moves a lot to generate trades, and the ranges are much higher than they should be considering where they end up, and that a test based on this ecological fact would be more to the point." I'm currently reading Bill Gross on Investing and a chapter entitled "Selling the Noise" seemed parallel. Gross said: "[Fischer] Black coined the term 'noise,' which he he applied both to financial markets and financial market volatility. Noise, Black said, is to be contrasted with information ... Those who buy stocks or bonds on noise are typified by traders in the futures pits, who buy and sell constantly, based often on rumors, perceived trends, and news that may or may not be relevant. Trader's perceptions are injected into the markets in the form of intensified trading and wider price movements than would normally occur without them. Some of the price movements may have nothing to do with fundamental information at all but may simply reflect the game playing of traders in the pits as they seek to outmaneuver their competition ... 'Because of the market noise ... the short-term volatility of price will be greater than the short-term volatility of value,' he writes. If so, then money managers who use short-term volatility estimates for longer-term option valuation are systematically overvaluing option prices ... [I]t seems a legitimate objective to gear our strategy toward 'selling the noise.' ... "

And in a Bloomberg TV interview last week, Gross noted a preference for "selling volatility." He said, "We prefer basically to move on the assumption that you have mean reversion."

(In the book Gross also has a chapter called "The Plankton Theory" that reminds me of your metaphor of "pilot fish." Gross: "Logic would suggest, therefore, that in attempting to forecast the well-being of the Great White Whale, Jaws, or even Jaws II, one of the factors to consider would be the status and future outlook of the plankton." Though Gross' metaphor depicts the investor instead of the asset class.)

On a separate topic, an interesting allusion to Galton that I came across in wondering through the blogosphere today-- In the post Andrew Gelman suggests that the "actual distribution of men's heights is longer-tailed than normal." ("If height were truly distributed normally, the likelihood of a nine-footer would be far, far less than one in a trillion.")

Flashback to Taleb/Mandelbrot starting off with a reference to normally distributed heights before launching into their ode to power law distributions- "There are specific measurements where the bell curve approach works very well, such as weight, height, calories consumed, death by heart attacks or performance of a gambler at a casino. An individual that is a few million miles tall is not biologically possible, but an exception of equivalent scale cannot be ruled out with a different sort of variable, as we will see next."

25-Oct-2006

A Long Strange Trip, from Steve Humbert

Believe it or not. we just had our first 50 degree swing in temperature going from an all time high two days ago to an overnight low in the 40s. Sitting here in my living room, I was thinking of you guys in Connecticut. I just wanted to write and send long distance good cheer your way. I talked to someone the other day who recently was in CT and he commented on how beautiful the change of seasons is this fall for the Nutmeggers.

I also am reflecting on what a wild and unique life it is to work in the world of speculation and investing. I cannot think of a time when I did not think of the markets. Over 25 years of buying and selling things that really do not exist -- intangibles -- in anything other than a number on a statement or confirm can exact a toll on one's psyche. It can be a overwhelming challenge to remain grounded in the real world when we thrive in an unreal world.

I am reminded of the timeless words of the Grateful Dead: "What a long strange trip it has been."

23-Oct-2006

Follow-up to Mention of Religious Fundamentalism, from James P. Smyth, M.D.

I felt compelled to respond to to the thread opened by Ronald Weber in his letter to the Spec editor. His letter to the editor seemed to imply that religious fundamentalism, especially of the Catholic Christian variety, seemed to impede economic progress.

I heard shades of the argument of the Max Weber work (perhaps a relative?) that I read when I was an undergraduate at Columbia "The Protestant Work Ethic and the Spirit of Capitalism". I reject the idea that certain religious groups or peoples are more suited to capitalism. The main requirement for economic progress for any group of people is that the scoundrels get out of the way. My parents were emigrants to this country from Northern Ireland. Without delving too deeply into the religious and social pathologies that existed in that part of the world, it was not a place where enterprise or hard work was rewarded. My parents, both were forced to leave school at fourteen. They moved to this country, worked hard, and put four children through college, two of whom earned graduate degrees. My relatives back in Northern Ireland, who are a perfect control group, have not done nearly as well. My story is obviously not unique in an exceptional county such as this. People all over the world, from the most dysfunctional countries and societies in the world, excel and become among our most productive citizens when they move here. Scoundrels in different parts of the world have different ideologies: in some countries they are religious fundamentalists, in other counties they are socialists, in other countries economic nationalists, in others, just good old fashioned dictators.

The common thread is that when people are allowed to improve their own lives, they will do it on their own. The recent Nobel Peace Prize awarded to Muhummad Yunis for his work for the Gameen Bank captures this universal truth, and this idea is the greatest hope for progress against ignorance and poverty.

Ronald Weber replies:

Thanks for your reply. However, I didn't mean to imply any link whatsoever between religion and economic progress (this hypothesis can be easily refuted). Don't get me wrong, being bearish is more of an individual (or institutional) attitude and has nothing to do with personal (or national or regional) success whatsoever; Stephen Roach is certainly a very wealthy bear!

23-Oct-2006

Position Sizing and Bouyancy, from Jeff Burkey

Since everyone is talking about risk management in the face of some high profile hedge fund blowups and the fact that it is Fire Prevention Week, I thought I would touch on damage control.

Let's take a look at an example of excellent damage control. Navy ships are designed and constructed with extensive shipboard compartmentalization to limit both progressive flooding and the spread of fires. Britannica has a nice article on Naval Architecture: Buoyancy.I like to think of my trading account in the same manor. Let's say I have $100,000 in my account and my daily scan comes up with a signal in a $50 stock and a 'reasonable' stop is 48. As most of you know, a cardinal rule in trading is to never risk more than 1% to 2% per trade. So let's say we are more aggressive than most and want to risk 2% or $2,000. We can buy 1,000 shares costing $50,000. If the stock does drop to 48, we will be stopped out and end up losing $2,000 per our risk threshold.

Perfect, right?

Sure that is what will happen most of the time, but what about protecting against the worst case or 'highly unlikely' event. The above example involves a position size of 50% of overall capital. When trading equities this is absolutely reckless. You don't have to be trading long to have the distinct pleasure of owning a stock that gets cut in half on a nasty gap down open. Your $100,000 account goes to $75,000 overnight. Even if you have ice in your veins, you still have a lot of work to do before you get back to breakeven. If you happen to be trading for clients, you better check the fax machine for redemption notices!

A simple rule that all hedge fund managers can easily remember is 2/20; risk up to 2% per trade as long as overall position size does not exceed 20% of overall trading capital. These are maximum levels and a more conservative trader might consider 1/10.

Damage buoyancy and stability. Building a ship trading account that can be neither sunk nor capsized is beyond practicality, but a ship trading account can be designed to survive moderate damage and, if sinking is inevitable, to sink slowly and without capsizing in order to maximize the survival chances of the people aboard trader.

--Encyclopedia Britannica, Inc. (modifications are mine)

19-Oct-2006

In Remembrance of your Mother, from Nathan Jones

Dear Victor:

Today, October 19, is the birthday of my mother and your late mother. In each of your books, and the writing and metaphors I feel like part of her shines through you. I'm sure she shared your heartache and discomfort yet had to be so proud of your achievements. Perhaps, the best testament is how you have handled adversity. So the achievements or you and your brother are a tribute not just to you, but also to your mother. Perhaps the most admirable individuals in our society are those who are self made and you and your brother are both in that category. I think much of that can be attributed to your mother.

My Father died in March of this year and my mother still lives. Yet I know that someday she will also pass away. But today on her birthday, I remember her and your mother.

Your mother taught you. You taught others. I still enjoy your insights more than any other financial person because I know how competitive you are and yet you have also shared the ecstasy of triumph and the agony of defeat in the financial markets. Thank your for all of your writings and insights. Thanks for having such a wonderful mother.

Nathan E. Jones

18-Oct-2006

Commerce isn't Conquest, by Donald J. Boudreaux

Editor, New York Times

Dear Editor:

Public understanding of trade is sufficiently poor without you deepening the problem ("Not Coming Soon to a Lot Near You: Chinese Cars," Oct. 18). Contrary to your words, imports are not an "invasion," and foreign merchants who sell things to us neither "conquer" industries nor "flood markets." Invasion and conquest are done by armies using violence to force foreign populations to do the bidding of the conquerors. Floods are similarly unwelcome as they destroy people's lives and properties.

rade is the opposite. It's peaceful: no one is forced to buy imports. It's productive: consumers get more goods and services at lower prices. Ask New Orleanians today if they regard a Circuit City stocked with Chinese electronic goods to be a calamity on par with Katrina's floodwaters.

Sincerely,

Donald J. Boudreaux

Chairman, Department of Economics

George Mason University

16-Oct-2006

Great News from Michael Strong, CEO of

FLOW, Inc.

Dear Friends in FLOW,

Last week our cause received a marvelous unforeseen boost, as Muhammad Yunus and Grameen Bank were awarded the 2006 Nobel Peace Prize. Clearly deserved and long overdue...and a profound affirmation of the power of "liberating the entrepreneurial spirit for good" for manifesting peace through commerce! In Yunus' words: "Lasting peace can not be achieved unless large population groups find ways in which to break out of poverty."

Several people associated with FLOW have worked closely with Yunus and Grameen Bank; in 2005 FLOW supporter Vidar Jorgensen arranged a private meeting between FLOW members and Yunus. In light of the obvious similarity between FLOW's cause of "liberating the entrepreneurial spirit for good" and Grameen's twenty-five year record of doing precisely that, I named Yunus the "grandfather of FLOW." He smiled, accepted the honor, and then graciously joked that he was a very young grandfather - I hadn't realized how young he was, or that I might have been committing a faux pas to suggest that he was an elder.

Among the anecdotes that he told us was one regarding the resistance he faced when he wanted to set up Bangladeshi women as cell phone ladies, micro-entrepreneurs who buy a cell phone and sell calls to other villagers by the minute. Everyone told him that those illiterate peasant women couldn't learn to use a cell phone. A few months later he visited a village and a cell phone lady proudly came up to him, closed her eyes, and asked him to give her a phone number. He did, and she proudly dialed it with her eyes closed.

Yunus has a marvelous stock of one wonderful surprise after another. One of the requirements of the Grameen Bank is that the villages must set up a latrine before Grameen will give them loans. In every case the villagers resist; why should they change centuries-old customs just to get loans? But Yunus insisted that this rule be followed despite the resistance. One day he was walking through a village and a woman came up and hugged him over and over again. He tried to remember if he had ever seen this woman, or had ever done anything for her, and couldn't place her. So he asked her why she was so grateful. And she replied, "For my entire life i had to wait until nightfall to relieve myself. Now I can go any time of the day with completely privacy!"

Grameen Bank is the first for-profit company ever to win a Nobel Peace Prize. As such, the award is a profound validation of FLOW's Peace through Commerce initiative.

For more information on this initiative, see our website, as well as the following two articles:

Understanding the Power of Economic Freedom to Create Peace

Peace,

Michael Strong

CEO and Chief Visionary Officer

FLOW, Inc.

P.S. See Yunus' autobiography Banker to the Poor for more wonderful stories about his work.

16-Oct-2006

A Few Thoughts on the Average in Humans and Stocks, from John DePalma

Vic wrote:

It's interesting to see how many average things he discovers and how many matches different people might have to them. But there is no validity or even justification for the goal of the book, which is to find the most average person. Instead what he comes up with is a person unique in fulfilling each of 140 criteria that each have, say, a one-third probability of failure. That indeed is a unique person, not an average person.

On can find a good visual illustration of the uniqueness of averageness in Tyler Cowen's blog. And a follow-up blog post notes that Galton is the intellectual progenitor of the notion:

A 1990 paper by Judith Langlois and Lori Roggman found that 'average' faces are judged to be more attractive than distinct faces. Specifically, digital composite portraits were described as more beautiful in proportion to the number of faces used in their construction, and the composite faces were more highly rated than nearly all of the individuals...

As the authors acknowledged, the idea behind composite photos was hardly new. In the 1870s, Sir Francis Galton, creator of statistical regression and correlation, came across a set of what we would today call police 'mug shots'. Galton, who also later pioneered the use of fingerprints in criminal investigations, hoped to identify physical traits that might predict unlawful behavior. He had been toying with the idea of creating composite portraits by superimposing photographic exposures, and the mug shots were perfectly suited for this project. After examining some early results, Galton noted, 'All composites are better looking than their components, because the averaged portrait of many persons is free from the irregularities that variously blemish the looks of each of them...

Also, Keynes' interest in knowing about average people in order to play the stock market game:

Or, to change the metaphor slightly, professional investment may be likened to those newspaper competitions in which the competitors have to pick out the six prettiest faces from a hundred photographs, the prize being awarded to the competitor whose choice most nearly corresponds to the average preferences of the competitors as a whole; so that each competitor has to pick, not those faces which he himself finds prettiest, but those which he thinks likeliest to catch the fancy of the other competitors, all of whom are looking at the problem from the same point of view. It is not a case of choosing those which, to the best of one's judgment, are really the prettiest, nor even those which average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practise the fourth, fifth and higher degrees.

13-Oct-2006

On the Current Political Campaigns, by Donald J. Boudreaux

Editor, The Wall Street Journal

Dear Editor:

Re the current political campaigns: Every day I'm bombarded with e- mails, supposedly from Africa, written by strangers promising to make me rich while at the same time enabling me to serve a worthy cause. These messages drip with mock-sincerity and faux familiarity, each writer assuring me that I can trust him or her fully. All I need do is to give these correspondents ready access to my wealth by sending them my bank-account number.

Of course, I wouldn't dream of trusting such people. And for the same reason I wouldn't dream of trusting a similar gaggle of glib strangers who, at this time of year especially, assure me that if they have access to my wallet (and my liberties) they will make me richer while they also make the world a better place. Unfortunately, unlike with the first set of scoundrels, I can't easily hit a 'delete' button to rid my life of politicians.

Sincerely,

Donald J. Boudreaux

Chairman, Department of Economics

George Mason University

10-Oct-2006

Mind versus Heart (Aristotle Debunked), from Ed Gross

The human mind is what differentiates man from the rest of the species on earth as noted by Aristotle in his Nicomicethean Ethics and other works. It is proven because man dominates the earth despite it being lower than many other creatures in speed, dexterity, strength and many somewhat noble virtues of the animals, such as monogamy and an unwillingness to kill one's own.

Detroit was the heart. the Yanks the brains. Yes, pitching wins baseball, but Detroit's pitching hasn't beaten the Yankees over the history of their matches. Although Torre made the right move to move A-rod. As the expression goes have a heart! He could have discretely put him in the two spot and not humiliated him, and given the Tigers confidence. Then they might think it was just a move to balance out the team or balance Giambi's injury... His mind was in the right place, but his heart failed him, and the Yankees heart failed altogether. No love amongst the team, only dissension, jealousy and diarrhea of the mouth.

Rationally they were the best, but the heartland dreams of America conquered the minds of the New York aristocrats. I tip my hat to Leland and Detroit!

04-Oct-2006

Some Thoughts Regarding Bears, from Ronald Weber

There may be two additional explanations for the bear virus: 1) System Complexity and 2) Religion (as strange as it may seem!). I am confident about Nr. 1), whereas Nr. 2) is really more of an essay!

System Complexity

Our modern economy is a an abstract and complex system that takes years and years of thinking, mental modeling, many false directions and much frustration to finally get a grasp of it (I am still far from having reached that point!). With the working mechanisms of modern capitalism far beyond the reach of many commentators, some have come up with an ingenuous way to solve the problem: simple mental shortcuts.

In doing so, the world appears nicely packaged in a way that does not require too much qualitative thinking, and in a flavor that is easier and more pleasant to communicate (simple explanations are always more popular than complex explanations). So if the dollar weakens, then it must be because of the "deficit", if there is a deficit it must be because of "globalization", if gold and oil go up it must be because China and India are driving demand, and so on.

As my space on this website is limited to further elaborate on each point, I will instead recommend to these commentators the following books to start with: The Misunderstood Economy: What counts and how to count it (by Robert Eisner) for issues regarding the deficit; Paul Krugman's Pop Internationalism for globalization; and finally for the Gold bulls, Bernanke's essays on the great Depression.

Religion

As I said, this is maybe a "long shot", but I will give it a try! The idea emerged as it turned out that many of the "end-of-the-world" bears I confronted tended to be Christians Catholics (I am a Protestant). The sample is too small to have any scientific relevance, and should be tested on a larger population across religions, but it is still worth thinking about the idea.

The strength of modern capitalism over the past 200 years to overcome so many obstacles, wars, bubbles, crises, deflation ,inflation, combined with the idea that your life will improve thanks to better technology and productivity (and many other things as well) does not seem to be compatible with the Christian Catholic "business model". Good times that last too long can be interpreted as a "sin", and may deprive the Church of its role as "savior-of-last-resort" when redemption finally comes. Moreover, the history of capitalism is very much linked with the Protestant work ethic and culture, having found its roots in the U.K. before flourishing on a larger scale in the U.S. ...

Please feel free to refute, elaborate, critique or disregard!

Gordon Haave comments:

I think his sample is biased. In my observations when I lived in CT., I would have agreed with the author. Now, in Oklahoma, it is definitely fundamentalist protestants and not Catholics who tend to hold the end of world view.

It seems to me that the end of world view is held by the most fundamentalist group in any one area. In the Northeast, there are very few fundamentalist Protestants, leaving the top of the fundamentalism rankings to Certain Catholics.

R.S. adds:

Having grown up with my Dad a fundamentalist preacher, I must agree with Gordon on a pure count basis. However, the doomsdayist fundies tend to be the saddest lot of the bunch. Depression and poverty and their belief in justice through judgement lead them to their scenarios. In other words things did not work out for them despite their righteousness. The wickedness of the world is to blame, God will fix it.

So perhaps if the count is weighted by money the doomsdayists control, perhaps Catholics still are the more influential of the doomsdayists. But I have not mixed enough with them to tell.

04-Oct-2006

Nice to See the Hubris Returning, from A Prudent Bear

So soon we forget about May 10th?! Ahhh a new month, 401k money is just about done being put to work while crude oil loses 4% (nat. gas up over 3% shhh) and those stubborn bond buyers happily lock in a 2.75% return after inflation for the next 30 years. No matter, CNBS has their headline and all is right with the world!

Maybe you enlightened Quants can tell me what happens when the advance/decline issues and volume make lower highs and lower lows for a week straight as an index makes a new high?

03-Oct-2006

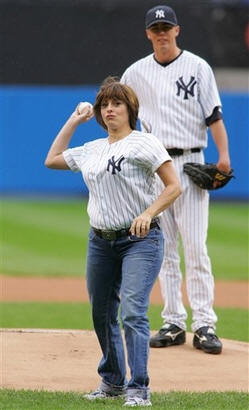

A letter on Maria Bartiromo, from Steve Leslie

The ubiquitous Ms. Bartiromo threw out the first pitch on Saturday September 30th for the baseball game between the New York Yankees and Toronto Blue Jays. The Yankees went on to honor Ms. Bartiromo by subsequently dumping the afternoon game to the Jays in an uninspiring 6-5 loss.

It appears the former "Money Honey" and "Econo Babe" named as such by floor traders for her resemblance to Sophia Loren needs to resume her Pilates training regiment or cut back on the carbohydrates. Years sitting behind her desk at MSNBC is beginning to take its toll on her once curvaceous figure.

Perhaps the selection of Dungarees was not the best of choices for this event. One must wonder out loud as to who her fashion consultant is. Suffice it to say at least in this instance it was not Vera Wang but perhaps more like Dickies work clothes.

In viewing the photo image of Ms. Bartiromo and how she blindsided the Federal Reserve Chairman recently quoting him in an off-the-record discussion, I am reminded of a famous quotation from Maureen Dowd, Pulitzer prize winning journalist from the New York Times as she described her profession.

"Wooing the press is an exercise roughly akin to picnicking with a tiger. You might enjoy the meal, but the tiger always eats last."

Ms. Bartiromo appears to be eating very regularly.

03-Oct-2006

Prohibition 2006, from Mr. Attorney

All in all this action by Congress is egregiously indefensible.

02-Oct-2006

Paolo Pezzutti on S&P Earnings

How to explain that while the operating earnings at more than 10% per year the Index is still well below its 2000 highs. Note also that in 2000 with the S&P at 1320.28, earnings were 52.00 (3.94%). In 2005 the Earnings Yield was 5.47%.

S&P 500 Operating Earnings:

2003 54,69 P/E 20,33

2004 67,67 P/E 17,93

2005 76,44 %CHANGE 13,0% P/E 16,33

2006 86,59 %CHANGE 13,3% P/E 15,32 (estimate)

2007 97,46 %CHANGE 12,6% P/E 13,61 (estimate)

From this perspective, it seems that the S&P is undervalued. There might be other reasons why money is not going toward stocks. During the past years the flow of investments might have found higher returns in different activities.