Sep

9

More on High and Low Beta Stocks, from Charles Pennington

September 9, 2011 |

Here's more on risky vs non-risky (more precisely, high beta and low beta) stocks, following up on a previous post.

There is a very nice set of data on Eric Falkenstein's website www.betaarbitrage.com. The data gives monthly returns, going back to 1962, on stocks grouped according to beta. I've used that data along with data on market returns and interest rates from other sources.

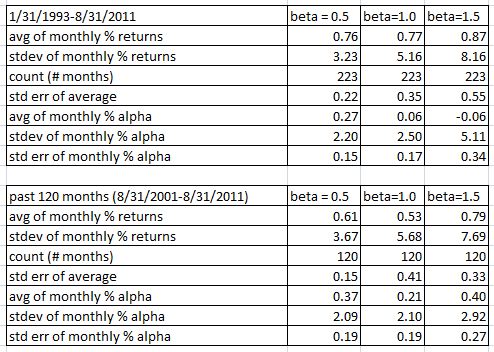

I looked at two (overlapping) date ranges. The first is from 1993 to present. That range was chosen since it coincides with the lifespan of the S&P 500 etf SPY. The other range chosen was the past 10 years / 120 months, from 8/31/2001-8/31/2011.

The results of this study are summarized in the following table.

There is only one fairly anomalous finding–a Lake Woebegone effect–in that all beta groupings had positive alpha and out-performed SPY. That is interesting, but is nothing more nor less than an artifact of the fact that the S&P "equal weight" 500 index outperformed the standard "cap weighted" index over these periods.

If we compare within the different beta groupings, we find a great big null result, a result consistent with expectations of the "Capital Asset Pricing Model". Neither low, medium, nor high beta stocks excelled or under-performed the others in any statistically significant way. For the past 120 months, the average monthly alphas of the beta=0.5, 1.0, and 1.5 groupings were, respectively, 0.37%, 0.21%, and 0.40%, each with standard error of about 0.2%. That's a tie in statistical terms.

For the 1993-present period, the alphas were 0.27%, 0.06%, and -0.06%, giving the edge to the low beta (beta=0.5) stocks, but with standard errors in the readings that are comparable with the differences, so again it's a statistical tie.

Reiterating points that I made in a previous post, I think that the returns of risky stocks get a bad rap. First, it's not appropriate to use geometric average returns, which unfairly penalize volatile stocks. A real-world investor can re-balance his portfolio periodically if he feels his market exposure is too big or too small. Second, with risky stocks, you don't need to invest as much money to get the same market exposure, so risky stocks should be credited in some way for the interest on the money that you didn't need to invest. The Capital Asset Pricing Model term "alpha" takes care of these problems in an elegant and logical way.

Technical details:

–Monthly returns data are taken from Eric Falkenstein's site www.betaarbitrage.com, specifically from the "beta=0.5", "beta=1.0" and "beta=1.5" portfolio data supplied here.

Eric writes: "The beta portfolios here target a forward looking beta. Using historical daily data, for the most recent period, but monthly for data prior to 1998, I create portfolios filled with stocks that have the betas closest to 0.5, 1.0, and 1.5."

–Monthly alphas are calculated as follows: alpha = (return - return_riskfree) - beta*(return_s&p - return_riskfree)

–For return_s&p I used the monthly total returns, taken from MarketQA, of the S&P ETF ticker SPY.

–For return_riskfree I used the 13-week treasury bill index (ticker ^IRX on Yahoo Finance) as measured at the start of each month.

Comments

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- Older Archives

Resources & Links

- The Letters Prize

- Pre-2007 Victor Niederhoffer Posts

- Vic’s NYC Junto

- Reading List

- Programming in 60 Seconds

- The Objectivist Center

- Foundation for Economic Education

- Tigerchess

- Dick Sears' G.T. Index

- Pre-2007 Daily Speculations

- Laurel & Vics' Worldly Investor Articles

{kind=link}