Nov

5

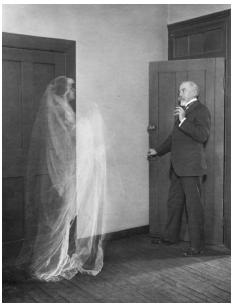

The Professor and the Pathological Leverage, Richard Owen

November 5, 2012 | 1 Comment

One sigma daily, two sigma occasionally, three sigma rarely, six sigma never.

One sigma daily, two sigma occasionally, three sigma rarely, six sigma never.

High sharpe always. The Professor smiled to himself. He looked at the drawdown, sortino. Beautiful.

Months of work. Days away. He flicked off the monitor, stood up, letting all the stored aches shoot up his hamstrings, into his back.

He glanced at the clock. 1.05. Traipsing across the floor, he pulled off his shirt, rolled onto the bed and closed his eyes. Bliss. Everything was ready for presentation to the team. All the numbers were checked. The initial framework was there. New. Perfect. Months of hard work lay ahead, but the core was ready.

For a minute he pondered. Would he run it for the endowment? Sell it up to Man Group? Perhaps get some capital from Stanley Fink.

He'd dreamt up the core years ago. But he needed markets to meet him halfway. To get there technologically. For the high frequency guys to put in the infrastructure. For the futures brokers to cannibalize each others spreads down to nil. His edge was niche, specialised. Skilfully risk managed. The leverage needed to get it humming at 600 over T-Bills wasn't even that high. Most of it was embedded in the contract terms. And it was scalable. Give it fives years and every corporate treasurer in the country was going to push their actuaries to get in on this thing.

He yawned and lay back. The pillow was fresh. It was one of those moments, all was right and in equilibrium. Just as it should be. The Professor sighed, stretched and slowly drifted off to sleep.

§

Urgh. The Professor startled up. "Hello, what!" he cried reflexively. He shot backwards, square to the headboard. As his eyes adjusted, the outlines of a ghostly body appeared in front of him.

Pulling his hands to his face, he squirmed, rubbed his eyes and cheeks, and looked again. "What is this?"

"Hello Professor," said the apparition.

"Oh god. What is this, what's going on?" The Professor span round to look at the radio clock. Half three. He glanced at the Restoril bottle next to it. None had been taken last night, right? Wait. All the late nights had got to him. The sleeping pills were sending him loopy. Slapping his face a few times, he sat up straight and looked forward again.

"Professor, I need to speak with you about your model," the apparition said calmly.

"Oh god. Still there," the Professor mouthed, sub silento. Just engage with it. Let the hallucination happen and then ring Dr. Green. Give him a bloody earful in the morning and get switched over to Klonopin. That was the best way to get this over with. Let it happen. "Okay, so my imagination has created you. What do you want?" the Professor said cockilly.

The apparition smirked. "Your model. Quit now."

"W-what?"

"Publish, sure. But then give it up. No good can come of it."

"What are you talking about?"

"Your model. Quit now!" the apparition repeated.

It clicked, suddenly. The Professor remembered his psych classes. This was the Restoril bringing out his superego. Anthropomorphising his inner fears. Just a matter of self-control. His taut muscles relaxed.

"Our work is revolutionary," the Professor objected, feeling faintly bemused at what his mind was having him engage in. At least it was another sign that he was a budding genius. To imagine this at half three. Gotta be smart, he concluded smugly.

"Revolutionary? So was Leland and Rubinstein, so was Black, Scholes."

"Who? What? That's old news."

"Have you spoken to anyone from the real world about it, Professor?"

"Sure I have. I went over the fundamentals with my buddy at the B-School the other week."

"The B-School? The B-School?! What, the same colleague who wrote up the case on the petrodollar merger? Said it was down to pioneering EVA analysis and infrastructure considerations?"

"Yes."

"The same colleague who forgot to mention that the VP for MENA Corporate was doling out back handed favours to every reserve-toting, sinecure cashing, oligarch-connected dolt who came through Heathrow?"

"T-they thought our model seemed practical," the Professor offered, defiantly.

"You don't get it. That Deutsche salesman with the piercing blue eyes, hot butt, and breathy tones? She didn't grab your port sheet whilst you were buying her a drink?"

"I've never even so much as been into a German bank, let alone done business with one!" The Professor reached out to his bedside table, grasping to touch his hardcopy of Hull. He needed some sort of anchor.

"You don't think your risk management framework hasn't been faxed all over town? That Eurotrash capco banker you've been courting hasn't already sold the system up to Rentech? They aren't already running it live? Think your PB lawyer hasn't slipped a special set of terms into the repo appendices just for you?" The apparition was beginning to talk forcefully.

"You're garbling nonsense at me."

The apparition fixed his eye right to the Professors, "I know, you shmuck. You're not getting this are you. God you're so… I bet you never even tried to bed one of your hot postgrads."

"That's it," the Professor fumed, "I'm calling Dr Green about these pills right now."

"You don't think every Merrill Lynch salesman in the country isn't already halfway down their client list, marketing your positions to every dentist and realtor they can get on speed dial? Samuelson's reforming CC, pulling back Kovner, sending Tudor the other side. Leitner and the BT boys are clubbing back together to grind out your spreads. Millennium is six deep into your positions. Izzy's got five guys in already, working over a book."

"We haven't even selected which asset classes to focus on yet!" the Professor yelled.

The apparition let out a curdling laugh. "You really believe Munger and Buffett haven't got your stops list in fifty inch bold font, searing from a three hundred hertz overhead onto their office walls? Einhorn is already buying your distressed claims. Riffing at a conference to a thousand adulatory guests about your liquidation."

"What stops list?" the Professor whimpered.

"You think your model code hasn't already been passed hand to hand in a battered attache from MI5 to Mossad to ISI. Travelled half the world in a diplomatic pouch."

"But… but I haven't written it yet. You're not making any sense."

"You don't think James Bond has had it injected into his forearm in microcode?"

"Bond doesn't exist you idiot," said the Professor, grasping.

"That a Bolivian drug mule hasn't got twenty thousand lines of Python code jammed up his backside on a capesize, on the Panama. He hasn't already sold it to the Zetas?"

"What?"

The apparition started to crescendo. "You don't think your positions are being taught in grade school, recited in church, presented on the ten o'clock news? Inserted into magazine centrefolds? Served free with coffee? Written on the back of cereal packets? You don't think everyone, everything. Everybody! They all know your position, your stops, your model, your approach?"

The Professors cheeks fell. His lips curled. "Everything you're saying. It is insane, ludacris, madness. Nobody knows my stops, nobody has my code. They're my ideas. You're talking like a madman. It's a work in process. It's great risk management. Revolutionary. It's going to change the way people invest. It's going to get me the Fields. Going to get me rich."

"And get you laid for once, I bet?" The apparition gracefully floated down and an ethereal hand emerged from the dark. "Let's shake on it," the apparition sniggered. As the Professor offered his hand, the apparition yanked him forward. "It's going to get you busted, you idiot." He released and shook his head. He'd seen it so many times before. "Goodnight Professor."

§

Sunlight. The Professor startled awake. His mouth burnt. Ah, so bright. He covered his face and circled the room with his eyes. He locked onto the bottle of Restoril. Smashing it with his hand, he let out a burst of anger, the remaining pills scattering across the floor. He shouldn't rely on these things. He knew they were a slippery slope. Addictions and emotions weren't for him. Cold numbers and analysis.

Then he remembered the dream. He shuddered. That's definitely it, he thought. Cold turkey on everything save for Aspirin.

Suddenly a burst of energy caught him, and he leapt up from the bed. Stretched his arms up and smiled. Today was the day. He was going to present his model.

Nov

4

8 Things We Can Learn About Trading from Caesar, from Victor Niederhoffer

November 4, 2012 | 1 Comment

I have recently read several biographies of Caesar including Caesar by Colleen McCullough. I found this brief review on Wikipedia illuminating. While I am not very knowledgeable about military strategy or Roman History, I saw many examples of Caesar's genius that were applicable to trading. I thought it might be helpful to list 10 things that helped him rise to the top and win battles that extended Roman territory to the Rhine and English Channel, and conquered 3 million of enemies, killed or captured more than a million of them, and brought back vast wealth to Rome.

I have recently read several biographies of Caesar including Caesar by Colleen McCullough. I found this brief review on Wikipedia illuminating. While I am not very knowledgeable about military strategy or Roman History, I saw many examples of Caesar's genius that were applicable to trading. I thought it might be helpful to list 10 things that helped him rise to the top and win battles that extended Roman territory to the Rhine and English Channel, and conquered 3 million of enemies, killed or captured more than a million of them, and brought back vast wealth to Rome.

1. High Frequency Execution.

He used high frequency weapons. The soldier's weapons were much shorter and lighter than the enemies. His used the Javelin and a short sword called the Gladus. The enemies used two foot spears. The Romans got to wound the enemy much faster and were able to fight much longer and fresher because they carried lighter weapons.

2. The Roman Logistics.

Legionaires had much better logistics than their enemy. Caesar always paid greater attention to food and living arrangements than his enemy. His men were healthier and stronger for battle and were able to escape quicker when defeat was imminent. The importance of a proper foundation for trading is emphasized. Make sure you have proper equipment, capital, and infrastructure before you start trading.

3. Alliances.

He was a master of making alliances, no matter the virtues of his allies. He formed an alliance with Pompei when it was in his interest, married his daughter to him, established peace with hostile Germanic tribes to defeat the Helvetias and the Gauls.

4. Training in the trenches.

He fought as a common soldier from the age of 20. He lived with the soldiers, ate their food, and battled with them. He was captured by pirates and was able to talk his way out of capture with a ransom and then caught the pirate ship and executed them. He had down to earth habits in his food and living. A trader who wants to succeed can't rise to the top withouot trading himslef, and developing economical habits.

5. Engineering.

Caesar loved nothing more than a complicated engineering problem. When he coudn't pursue the Germans by land he built a bridge over the Rhine. He left enough space on the other side so that he couldn't be captured again. He was able to move his army over the Alps in two days to defeat Pompei in Spain. He was trained as a scientist before becoming a soldier and applied the disparate disciplines of engineering, medicine, and architecture to better prepare for battle. The best training for a trader comes from fields other than finance,— physics, ecology, biology, music.

6. Celerity.

He moved his Legionnaires faster than his enemies. They frequently marched 60 miles in a day. He made decisions quickly and brought his legionnaires into the fray quickly when it was time to rout the enemy.

7. Speculation.

Time and time again he gambled and took bold strokes. If you are going to be a speculator you have to speculate you can't grind like Pompei, a much more experienced commander, did.

8. Incentives.

The legionnaires and he were entitled to a % of captured lands, jewelry and slaves. Each hand had a share of the spoils and this made them fight harder. At the end of their stay in the legionnaires they were promised land for retirement and many remains of their homes and belongings show that they lived relatively as well then as retired military today.

Alston Mabry notes:

Twenty or 25 miles a day would be a substantial march, especially carrying all the gear they had.

In broad terms, the key to Roman battlefield success was their tactic of fighting in very close formations, even with overlapping shields. Essentially, they had more "swords per yard" at the front of a unit. This was very effective against enemies who fought in loose mobs, like the Gauls.

As for Caesar, an interesting topic of study is the battle of Alesia.

Phil McDonnell writes:

When I attended high school in NJ I had the pleasure of reading some of Caesar's writings in Latin. In particular I was struck by how he opened his account of the Gallic Wars. the opening three sentences were:

Veni. Vidi. Vici.

They translate as: I came. I saw. I conquered.

In many ways it is the height of confidence, even arrogance. Undoubtedly his confidence was one of his greatest aspects but it also lead to his hubris. One imagines that he was truly shocked when they assassinated him in the Senate chambers.

Nov

4

Let’s Go Fly a Kite, from Duncan Coker

November 4, 2012 | Leave a Comment

Should you find yourself in need of a kite for kite flying this weekend, I highly recommend a foil kite over traditional framed kites. A foil kite has a stitched honey comb design which inflates expanding the canvass to catch wind. They require no cross bars or frame. They are lighter, pack much smaller, require less wind to fly and can be stored in a backpack to be near when the kiting urge takes over. Premier is a good brand. Find a field, some wind, a small child, or child-like mood and enjoy the day.

Should you find yourself in need of a kite for kite flying this weekend, I highly recommend a foil kite over traditional framed kites. A foil kite has a stitched honey comb design which inflates expanding the canvass to catch wind. They require no cross bars or frame. They are lighter, pack much smaller, require less wind to fly and can be stored in a backpack to be near when the kiting urge takes over. Premier is a good brand. Find a field, some wind, a small child, or child-like mood and enjoy the day.

Jeff Watson writes:

I fly a lot of kites and use this purveyor Into the Wind. They have my good seal of housekeeping.

Craig Mee adds:

The Tao of Kiteflying: the dynamics of the tethered flight by Harm van Veenmuch is quite a good little book with a great foreword: "dedicated to all those who have not yet unlearned their sense of wonder about reality in general and the phenomena of kites in particular".

Easy enjoyment and also market lessons for all.

Nov

2

In the Parks Near Chinatown, from Victor Niederhoffer

November 2, 2012 | 1 Comment

In the parks near Chinatown you can see tables devoted to Go. The players are generally 80 to 95 years old although since all Chinese above 80 look similar, some centenarians might be there. Standing on all sides of the table are dozens of spectators who lean forward in tense poses waiting in perilous animation for the move of the masters.

In the parks near Chinatown you can see tables devoted to Go. The players are generally 80 to 95 years old although since all Chinese above 80 look similar, some centenarians might be there. Standing on all sides of the table are dozens of spectators who lean forward in tense poses waiting in perilous animation for the move of the masters.

One is reminded of this as everyone waits for the important number announcement moves like employment. Of course the numbers are distributed on a "need to know basis" to the president, and presumably to be fair to the challenger, and of course to the "central" and presumably their colleagues across the world say in Negara so that their crucial operations in the exchange market might not be disrupted (where is my challenger friend who has a bedroom here when I could interpret his body language). And one can imagine the give and take before the release from the circular office. "No that's too low, we got a lot of flack last time. Suzy might have let Jack out of the attic again. How about a little rise. But keep it below the round".

The centenarians perched precariously smile inwardly.

Nov

2

It’s Now Clear, from a former rackets player

November 2, 2012 | 1 Comment

It's now clear to me that everything Rogan said recently is right. There is a force, probably without memorialization wishing to keep the world state going. That force will do everything it can to keep the market up before the election. Shortly after or in conjunction with the wish fulfillment of the incumbent win, a revulsion will occur.

It's now clear to me that everything Rogan said recently is right. There is a force, probably without memorialization wishing to keep the world state going. That force will do everything it can to keep the market up before the election. Shortly after or in conjunction with the wish fulfillment of the incumbent win, a revulsion will occur.

Please help me with the timeline. It starts with the Roberts decision to allow medicare. Then the German decision to allow redistribution from Germany to Europe, then the GE 4 the cooling of Arab Spring protests so as not to embarrass their fellow traveler in the "circular" office, then the 7.8 % from a temporary head who lunches as agrarian party bashes with her kid.

Let us hope that the adversary does very well in cardinal events such as debates and polls in the interim so that massive European and central bank activities unlimited to support the stock market can be implemented in the remaining few weeks.

Alex Castaldo writes:

The next logical step would be a Nobel prize for Bernanke or one of his ilk.

Nov

2

How to Tell if You Are the Target of Bullies, from anonymous

November 2, 2012 | 3 Comments

Bullies, as adults, generally abuse their authority. If you stand for excellence and have some success you will attract the attention of bullies. It has been my experience that bullies hate a good success story but despise the successful more for the attention and admiration of others than their success. The heroes of myths, Bible stories, and legends are often victims of the drummed up accusations of bullies. Apparently, most ancient cultures were gravely concerned with bullies in everyday adult life.

Bullies, as adults, generally abuse their authority. If you stand for excellence and have some success you will attract the attention of bullies. It has been my experience that bullies hate a good success story but despise the successful more for the attention and admiration of others than their success. The heroes of myths, Bible stories, and legends are often victims of the drummed up accusations of bullies. Apparently, most ancient cultures were gravely concerned with bullies in everyday adult life.

Here are several tells that a bully's complaint against you is a witch hunt rather than legitimate complaint:

1. You are singled out after publicity.

2. Many interviews are held and are fishing expeditions of your weaknesses.

3. In these interviews, there are two types of witnesses, those that routinely support the bully and those that are intimidated and gladly rat out their neighbor to get the bully to leave their doorstep.

4. The interviews are one sided.

(It is widely known that the bully and their cohorts have immunity for much more corruption. Interrogations do not happen for them. Romance, money and power are often a triangular core. The bully often is a mistress of the ruler in the stories)

5. The bully often will intimidate and harasses the friends and family who would give the moral support to the victim.

6. It makes no financial sense for the bully to waste so many resources pointing out your minor faults.

It makes sense to do whatever it takes to rid yourself of an organization that allows one to be bullied.

I wonder if the moral implication of the ancient stories is correct, that rampant bullying is a subtle sign of an empire or emperors impending sudden chaotic demise…

Nov

2

The Origins of Credit, from Gary Rogan

November 2, 2012 | 2 Comments

The origins of credit are in the financing of trading voyages, specifically in Venice. That was basically a way to invest capital in productive enterprises, as of course is any other form of credit extended with the intention of finding a profit by creating value. Credit for consumption is arguably equivalent to the second oldest form of credit which is financing wars by the kings, and that came later once the credit making machinery got deeper and more geographically distributed following the trade it was financing.

The origins of credit are in the financing of trading voyages, specifically in Venice. That was basically a way to invest capital in productive enterprises, as of course is any other form of credit extended with the intention of finding a profit by creating value. Credit for consumption is arguably equivalent to the second oldest form of credit which is financing wars by the kings, and that came later once the credit making machinery got deeper and more geographically distributed following the trade it was financing.

Credit for consumption is almost always a Ponzi scheme of sorts relying on the incomes of the borrowers rising with time, but once in a while it's not when the borrowers pay back and the lenders cease and desist for some rare reason. But as history has demonstrated, sooner or later lending for consumption (or wars by the kings) ends badly because the income streams always start falling or disappear at some point if you wait long enough.

Nov

2

Koufax Facts, from Dan Grossman

November 2, 2012 | 1 Comment

I once saw Koufax pitch.

I once saw Koufax pitch.

In his honor, here are some tidbits:

He was signed by the Dodgers for a $14,000 bonus and $6,000 annual salary.

His career was, of course, before free agency. When he and Drysdale were at top of their careers and held out together (refused to report to Spring training for six weeks), he eventually settled for a $125,000 salary.

Inside baseball language in those days was not very PC (perhaps still isn't). In 1965, when big decision for first game of World Series was whether to start Koufax or Drydale, manager Walter Alston came into clubhouse and announced, "I'm going with the Jew."

Notwithstanding modest earnings, lack of endorsements and very limited TV career, he retired to Maine and seemed to live a distinguished, very private post-baseball life.

He married, and eventually divorced, a highly attractive daughter of actor Richard Widmark.

I was saddened to see that, through the advice of his childhood friend Mets-owner Fred Wilpon, Koufax lost a considerable amount investing with Bernie Madoff.

Nov

2

Conrad Black, from Dan Grossman

November 2, 2012 | 4 Comments

I have followed Conrad Black and highly recommend his recent book, A Matter of Principle . The latter half of the book — on his conviction, incarceration, successful appeal to the Supreme Court, but then his re-sentencing (for one count out of some 16 dismissed or overturned) — is very compelling, and more interesting than the first half of the book, an over-detailed account of his business activities, although they seemed highly successful and convincingly non-criminal to me.

I have followed Conrad Black and highly recommend his recent book, A Matter of Principle . The latter half of the book — on his conviction, incarceration, successful appeal to the Supreme Court, but then his re-sentencing (for one count out of some 16 dismissed or overturned) — is very compelling, and more interesting than the first half of the book, an over-detailed account of his business activities, although they seemed highly successful and convincingly non-criminal to me.

He presents a brave account (despite great pressure to apologize to the Court in order to receive a lesser sentence, he always refused to do so) and he writes with grace, humor, and a refusal to feel sorry for himself.

Very good on the nature of the US criminal justice system, the legal profession, and the alacrity with which famous friends immediately desert him or even work against him when he is charged with a crime (Henry Kissinger is prominent in this regard).

As I say, highly recommended. It's a compelling example that when the government decides it wants to convict you, it is 99% successful in being able to do so.

(The law Black was convicted under, in its latest iteration, was authored by now-VP Joe Biden. At the Supreme Court hearing, Justice Breyer — probably the justice who most upholds the government — commented that the way the law was written, probably 80% of the business executives in the US could be convicted under it.)

Nov

1

The Question Arises, from Victor Niederhoffer

November 1, 2012 | 2 Comments

The question arises, "who can you trust as you get along in life" and "how can you teach your kids or your wife to take care of their financial lives when you are gone" and "how many spouses and family have been victimized when the person that controls considerable wealth is seduced by a much younger and more sexual personage with the intention of relieving him and the family of their wealth"?

an anonymous commenter writes in:

My friend recommended The Sociopath Next Door a few days ago. Here is a great quote:

My friend recommended The Sociopath Next Door a few days ago. Here is a great quote:

"Maybe you are someone who craves money and power, and though you have no vestige of conscience, you do have a magnificent IQ. You have the driving nature and the intellectual capacity to pursue tremendous wealth and influence, and you are in no way moved by the nagging voice of conscience that prevents other people from doing everything and anything they have to do to succeed. You choose business, politics, the law, banking, or international development, or any of a broad array of other power professions, and you pursue your career with a cold passion that tolerates none of the usual moral or legal incumbrances. When it is expedient, you doctor the accounting and shred the evidence, you stab your employees and your clients (or your constituency) in the back, marry for money, tell lethal premeditated lies to people who trust you, attempt to ruin colleagues who are powerful or eloquent, and simply steamroll over groups who are dependent and voiceless. And all of this you do with the exquisite freedom that results from having no conscience whatsoever. You become unimaginably, unassailably, and maybe even globally successful. Why not? With your big brain, and no conscience to rein in your schemes, you can do anything at all."

Ken's book suggests 1 in 25 have the personality type. Sociopath's seem to be an overweight in the business sphere. And Sociopath's organizations echo their personality traits. Thus identifying them would seem to be essential. Unfortunately, there's the chicken and egg issue: by the time you have foreknowledge, it's often too late.

The only ready indicators I've felt: a general feeling that somethings not quite right when you meet them; something about the eyes that is a bit vacant (but as distinct from meeting an introvert).

But I do not claim any success in this measure.

I think the Rockefeller approach of cheating your own sons perhaps has sense. Similarly, I think you need to meet some truly ruthless people to get a sense of them. You might seemingly want to protect children from these sorts of experiences, but perhaps it ultimately costs more later? Unfortunately, ruthless people are not always in ready supply until you are on the battlefield, so to speak.

Jeff Watson writes:

The sociopaths in the S&P pit in the late 80's were legendary. Any

time I would get a trade down, even my own firm's broker stole from me.

He was busted for it in 1989.

Kim Zussman writes:

We trust friends and family based on incomplete information, or empirically based on a sample of trials from which we conclude trust or not. This is true because we can never get into minds of others to understand their true motives and intentions (and even if we could, their motives may be indecipherable as they are invisible to themselves).

Thus it is logical, when presented with unexpected criminal evidence, to question the original basis of friendship or kinship.

Put another way, when should countervailing evidence out-weigh personal connection?

Nov

1

NYC Junto, from Victor Niederhoffer

November 1, 2012 | 1 Comment

The NYC Junto will still be meeting at the usual place, the Mechanics Institute, 20 West 44th Street New York, NY, at 7pm Thursday November 1, 2012 with Mr. Greg Rehmke delivering a talk on evolution of economic behavior.

The NYC Junto will still be meeting at the usual place, the Mechanics Institute, 20 West 44th Street New York, NY, at 7pm Thursday November 1, 2012 with Mr. Greg Rehmke delivering a talk on evolution of economic behavior.

Hope to see you all there!

Sincerely,

Victor Niederhoffer and Dailyspec

Nov

1

Inside the Investors Studio, from Richard Owen

November 1, 2012 | 1 Comment

Recently, I've been enjoying a nightly course of steroids (ROIDS!) which has immobilized me for a half hour or so. This has provided a perfect opportunity to catch-up on junk TV.

Recently, I've been enjoying a nightly course of steroids (ROIDS!) which has immobilized me for a half hour or so. This has provided a perfect opportunity to catch-up on junk TV.

Thankfully, I have discovered Inside The Actors Studio. It is my first encounter, albeit a long running series probably long since known to all those in the USA.

There are quite some similarities between the field of movie stardom and investing. Both are fickle industries where talent and determination are necessary, but not sufficient, conditions for success. A favorable tailwind helps. Intelligent, trusting partners matter perhaps more. Room for some failure is essential to survive. Low barriers to entry, high barriers to success.

The Studio focuses on interviewing the big stars. Some consistent themes come out in their personas, that might be familiar:

- All are highly inspired by their craft. They seem like they could talk endlessly and enthusiastically about it.

- Upbeat personalities seem a given.

- Many went through a long apprenticeship, constantly revising their core model until perfected. Others seemed blessed by the Hand of God from day one.

- Focus on process and love of the art seems to matter almost as much as the outcome. Which is good, because often others are going to hate it.

- The media of both industries has it's similarities; they're gonna puff you up one minute and deflate the next. Spine is a requisite.

- There's constant reference to precedents and pioneers in the industry; everyone's looking to to see what the other is doing.

- Mimicry and plagiarism are rife.

Some more niche analogies can be made:

- Eddie Murphy is the model trader, focused on the short term. He's got his system down cold and is constantly trying to tweak his market (the audience) for eighths and quarters (laughs). His only issue is if times change and his tastes become outmoded. The persona is so embedded, it's going to be an upheaval to adjust.

- Sean Penn and Francis Ford Copola are maybe the maverick strategists. Perhaps Jim Rogers. Brilliant, mercurial, coming up with leftfield views nobody else anticipated; always with initial backlash. Eventual vindication and celebration await. But sometimes being so far from consensus takes its toll, and turns them a little wild. They wouldn't have it any other way.

- Tom Cruise is Warren Buffett. Economics have been maximized in the principals favor. Intensive research goes into each project; this is how they de-risk. Cruise invested countless hours into Japanese history before even discussing The Last Samurai with the director. Their favored asset is the big ticket, no-nonsense production. Risk is capped, but with big upside potential.

- Pacino is Soros. He's got the full package; attacking from all angles and styles; pulling in other big guns where needed. But with an underlying dedication to craft. Occasionally he'll use sheer force of personality to get the trade or film over with.

- Woody Allen [ed: not yet on actors studio] is Marty Whitman. He's gonna grind it out; never levering up into one trade. But he's also going to concentrate his resources; finding high quality at low cost themes, producing a great risk adjusted return. His following is loyal. All this lets him sleep well at night.

- Spielberg and James Cameron are Peter Lynch. Only the Toniest product goes into the portfolio. Everything is visionary and of highest production value, but in a way that uniquely channels mainstream, not maverick tastes. Ten-baggers a plenty. And for the occasional busted asset - well they're the big dogs and can take it on the chin.

Nov

1

50 Billion to Repair the NY Subway System, from Victor Niederhoffer

November 1, 2012 | 1 Comment

I see an estimate of 50 billion to repair the NY subway system. "Many of the suppliers of equipment have been out of business for 50 years". All equipment damaged by salt water basically must be replaced. The loss of wealth from the flooding and the 3 million homes without power must represent enormous opportunity cost to the economy. At least 50 billion above and beyond the subway. The total goods that an economy produces represents the amount available to be divided up and would seem to be a good measure to total utility. These total goods are 100 billion less than they would have been. They say that one of the causes of the 1907 October crash was the San Francisco earthquake of April 1906. Big destructions in other floods and tsunamis would seem to have lagged negative impacts also. Total reductions in wealth like this have to be big negatives for the long term despite the tendency of calamitous events to have a negative impact the first day and bounce back by end of week.

I see an estimate of 50 billion to repair the NY subway system. "Many of the suppliers of equipment have been out of business for 50 years". All equipment damaged by salt water basically must be replaced. The loss of wealth from the flooding and the 3 million homes without power must represent enormous opportunity cost to the economy. At least 50 billion above and beyond the subway. The total goods that an economy produces represents the amount available to be divided up and would seem to be a good measure to total utility. These total goods are 100 billion less than they would have been. They say that one of the causes of the 1907 October crash was the San Francisco earthquake of April 1906. Big destructions in other floods and tsunamis would seem to have lagged negative impacts also. Total reductions in wealth like this have to be big negatives for the long term despite the tendency of calamitous events to have a negative impact the first day and bounce back by end of week.

Ken Drees writes:

I like the reference to San Fran in scope and lag. Let's say it costs 200 billion to repair–it will be the only QE that cannot be afforded. A sad reality.

Nov

1

Flood Insurance, from Alan Millhone

November 1, 2012 | 1 Comment

I wonder how many homes are not covered due to lack of flood insurance or not being able to get coverage on Jersey Shores etc. ?

I wonder how many homes are not covered due to lack of flood insurance or not being able to get coverage on Jersey Shores etc. ?

Anonymous writes:

Flood insurance is easy to get. There is a "basic" version and an add-on. The basic version on our Jersey Seashore house cost $20 per $100k of coverage and the add-on was an extra $47, PER YEAR. It is subsidized by the Federal government, which is why it is so cheap. Only an idiot would not have it. And yes, there are idiots out there. If you are in a flood-prone area, you want as much insurance as you can get.

If you are not in the defined "flood plain" it can be difficult to get flood insurance because the Feds do not subsidize it. We also had a lakefront property that somehow managed to be out of the designated flood plain. Coverage for that property was about 3 times that of the beach house. And that property did have some minor flood damage, although I chose not to submit it.

Bill Herrmann adds:

Federally subsidized flood insurance is a very good example of government incentives pushing the economy in the wrong direction. Just as “Too Big to Fail” encourages some institutions to take larger risks then they would otherwise, federal subsidized flood insurance encourages building in the flood plain. (Which is generally not a good idea.)

« go back —

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- Older Archives

Resources & Links

- The Letters Prize

- Pre-2007 Victor Niederhoffer Posts

- Vic’s NYC Junto

- Reading List

- Programming in 60 Seconds

- The Objectivist Center

- Foundation for Economic Education

- Tigerchess

- Dick Sears' G.T. Index

- Pre-2007 Daily Speculations

- Laurel & Vics' Worldly Investor Articles

{kind=link}