Oct

13

Post-Mortem Park Avenue Bank, from Anatoly Veltman

October 13, 2010 | 1 Comment

The saga of Park Avenue Bank's Charles Antonucci is over. The bank president, who on March 15 was arrested on charges of engaging in a broad range of illegal conduct that contributed, in part, to the bank's demise, but most importantly to stealing $11 million from TARP. Well, tonight the FBI has just announced that Antonucci has formally admitted to and pled guilty to securities fraud relating to his attempt to fraudulently obtain more than $11 million worth of taxpayer rescue funds from the Troubled Asset Relief Program ("TARP"), bank bribery, embezzlement of bank funds, and participating in a $37.5 million scheme that left an Oklahoma insurance company in receivership.

The saga of Park Avenue Bank's Charles Antonucci is over. The bank president, who on March 15 was arrested on charges of engaging in a broad range of illegal conduct that contributed, in part, to the bank's demise, but most importantly to stealing $11 million from TARP. Well, tonight the FBI has just announced that Antonucci has formally admitted to and pled guilty to securities fraud relating to his attempt to fraudulently obtain more than $11 million worth of taxpayer rescue funds from the Troubled Asset Relief Program ("TARP"), bank bribery, embezzlement of bank funds, and participating in a $37.5 million scheme that left an Oklahoma insurance company in receivership.

Then again, this is what every other CEO in America is guilty of every single day. Which means that only thing Antonucci really pled guilty to was being a stupid enough to keep Park Avenue Bank Too Small To Succeed. As we all know the TBTF curtain is the only alibi many other criminals in the industry resort to when the congressional theater convenes.

Moral of the story: unless you can threaten the world with collapse, you will go to jail.

Oct

12

Are Utility Stocks Better Than 5-Year TIPS? from Rocky Humbert

October 12, 2010 | Leave a Comment

It's generally accepted that large electric utility stocks are interest rate sensitive. They also have earnings growth based on a regulator-sanctioned "acceptable return on capital." The stocks are considered cheap when they are trading near book value (not now), and also when their yields are relatively high versus treasuries and bonds (yes now). There's some economic sensitivity to electric demand of course– but the stocks are still very low beta.

I posit that at their current relative prices, a basket of quality utility stocks should outperform TIPS… with similar risk and reward. The reason is not that utility stocks are particularly cheap, but rather because many TIPS have trivial and/or negative real yields. In a rising inflation environment, utilities should be able to get regulator approval to raise prices [to maintain their statutory ROE]– and in the current status quo environment, the stock yields will exceed the TIP yield.

At this moment, the 5yr Treasury has a 1.1% nominal yield, the 5 year TIP has a -0.50 real yield, and the UTY has a 4.34% nominal yield.

What am I missing here? Other than regulatory risks, in what environment will the UTY significantly underperform a 5-year TIP held to maturity?

Mr Krisrock comments:

In his book on theory, Ray Dalio of Bridgewater theorized that "stress testing" an investment theme by asking other unsuspecting traders their views, in effect is a surreptitious poll, as we note here in this textbook case of pedestrian "street begging".

Rocky Humbert responds:

Perhaps Mr. Krisrock will be so kind as to put a penny in this beggar's cup with an insight using all of his over-sized frontal lobe (and not just the amygdala).

I thank the speclisters who kindly pointed out (offlist):

1) During the 1930's depression, utility stocks held their dividends… And people who paid their bills saw higher rates to compensate for the people who did not pay their bills.

2) The TIPS will return par at maturity — there is no similar guarantee for utility stocks.

3) Because TIPS are currently trading at a premium to par, outright deflation can be injurious to their returns.

4) Utilities are taxed as corporations — and are also subject to the risks of cap&trade etc. However, the state rate-setting boards may/may-not compensate for the increased costs of cap&trade with rate hikes.

The daily and weekly statistical correlations between utes and tips are quite poor. But as the attached chart shows, they do seem to move in the same directions.Perhaps foolishly, I'm least worried about technological innovation– because the primary motivation for investing in a regulated utility is that they set rates based on a statutory ROE….

Jeff Watson writes:

Wireless electrical power transfer has been around since Leyden, Franklin, van de Graaf, and Tesla, just to name a few. Radio waves are a wireless electrical transmission system….just ask me, as a ham radio operator I have gotten many very nasty RF burns when my system wasn't properly grounded, or I stood directly in front of a beam antenna when someone keyed up the transmitter putting 2KW through the antenna. Further back was the study of charged amber by the ancient Greeks and the ability to turn static electrical potential into kinetic energy. The thermoelectric effect has reputedly been described since the middle ages. Now, the newest commercial application of wireless electrical transfer is with those new cellphone and iPod chargers where you just lay them on the pad and it magically charges the batteries with no electrical circuit. One might expect for more practical applications as time goes by and the market demands the convenience.

Mr. Krisrock adds:

In India, for example, there are many rural areas without electricity or the likelihood of same. Some years ago we partnered with Reliance and built cell towers with solar panels that allowed locals to plug in their mobile phones into the cell towers to recharge them. Until we did this they had to send them back to the cell phone company to recharge them…clearly some pennies for the beggars cup….

Tyler Mclellan comments:

You're missing this. The future nominal rates are the sum of the short rates (at least to some point on the yield curve). If you finance the position at overnight money (which many marginal buyers do), you cannot lose money if the sum of the short rates is less than the yield. I repeat, no matter what happens to inflation etc…you cannot lose money so long as the short rates one finances at are less than the yield. Through one more iteration, TIPS work the same way.

So i suspect the answer to your question has to do with the nature of "return".

David Hillman adds:

Once we could not imagine a wheel nor a printing press nor telescopes nor electricity, nor steamships, nor the camera, nor the radio, nor the automobile, nor the incandescent light, nor telephones, nor submarines, nor television, nor computers, nor endoscopic surgery, nor nanotechnology.

The 4 ounce, 4.75"x2.5"x0.5" device clipped to my belt is a GPS, a voice recorder, an 8MP camera, a calendar, an alarm clock/stopwatch, a music/video/tv player, a language translator, a dictionary, an encyclopedia, a library, an internet browser, it allows remotely operating a computer half-way across the globe, it connects to gmail, to WiFi, it recognizes touch commands and voice commands, it will both convert the spoken word to text and vice versa, and oh, yes…..it's a telephone, too. The cost of entry is $99 + $55/mo. Such a device was not imaginable as recently as 20 years ago.

A world without a power grid depends upon a collective will to have it, vision, investment, R&D, innovation, efficient production, practicality, affordability, and profitability.There are many individuals moving "off the grid" now, some adopting current [no pun intended] technology, wind, solar, water, other renewable, that allows same, others eschewing that technology in favor of more basic passive and mechanical means, horsepower and elbow grease.

But while basic technology exists, instead of pursuing advancement in earnest, we persist in taking the easy, short-sighted, petroleum-based way out, screwing ourselves in the process.Still, given the history of technological advancement, one might suggest somewhat optimistically that, someday, we will will it and the question is less "could there be?" than it is "when?" Until then, we'll just plod along from crisis to crisis as we humans are wont to do. Plus ca change…..

Jeremy Smith comments:

You wrote, "It's generally accepted that large electric utility stocks are interest rate sensitive. They also have earnings growth bas…"

"Generally accepted" is statistically incorrect, at least since 1994, which is a long time. Correlation to bond prices is actually negative. Utility dividends also increase. They can estimate 3-4% increase for an index of these, more for the better companies. Of course the longer you hold a higer yielding stock with dividend growth, the more hopeless fixed income is by comparison, especially with regard to income generated. As income rises it forces higher the value of the instrument producing the income, all other things being equal.

Phil McDonnell comments:

I do not think that it is generally accepted that utilities are negatively correlated with bonds but that appears to be the case. I picked idu for utils, tlt for 20+ treasuries and shy 1 yr treasury. For last 105 days of daily net changes we have the following co-terminal correlations:

idu tlt idu

tlt -59

shy - 54 74

Perhaps the utility– interest rate connection is more complicated than upon first reflection. 1. They are heavy borrowers for their capital equipment financing so one would think they are hurt by higher rates. 2. Their are regulated, so when their regulators are convinced that rates have risen they will often give them rate relief which means higher rates are eventually mitigate. 3. The stocks sell in competition for investment dollars with other income producing assets such as bonds etc. So they must be priced to yield competitive returns.

Steve Ellison writes:

Could it be that there is little interest rate sensitivity when rates are very low? Or that the correlation was arbed away when everybody knew about it? Last year, I noted a similar regime change in the correlation of stock prices and interest rates.

Tyler McLellan writes:

Look, stocks and bonds have been Correlated negatively in price terms since 1999/2000, I would bet that utilities have been correlated enough to the market as a whole that they've been at least partially along for the ride.

One reason to suspect this? Maybe if equity price are set my marginal preferences of equity investors if tech stock a goes down and that makes people want to sell some ute b to buy more, it might not matter that bonds are twenty bps lower, especially when the bond buyers don't care about either.

Rocky Humbert writes:

I played with the data a bit more, and it looks like the Tyler and Steve's observations account for most of the the regime change. The Ute's stock market beta/correlation dwarf their bond market beta/correlation (notwithstanding the low stock mkt beta of Utes.) Since stocks versus bonds have gone their separate ways over the past 12 years– the ute's regime change riddle is mostly solved.

There is one last data point worthy of mention: more than 65% of the UTE's total return is due to their dividends…and the attached chart graphically illustrates investor preference for utility dividends versus bond market dividends. This chart highlights the fact that the mean dividend yield for utes is 69% of the bond yield … and we are currently 3 sigma cheap…on a yield comparison basis. But that's true of many stocks…

My intuition remains that Ute's will probably outperform 5-year TIPS from these relative prices, but it appears that this intuition is a restatement of my bias that stocks overall should outperform bonds from these relative prices. If Ute's get whacked because of a hike in dividend tax rates, this may provide an attractive entry point for Ute's on their own absolute-return merits.

I'd like to thank everyone for contributing their thoughts (especially when they disagree with my thesis). It's a pleasure and privilege to interact with a group of such intelligent, independent-thinking people.

Jim Sogi comments:

Undistributed power using local generation, solar, wind, battery, water will be what undermines the monopoly just as cell phone undermined the phone land grid.

Stefan Jovanovich replies:

I think it is an exaggeration to argue that the cell phone has "undermined" the phone land grid. The "land" grid is, in fact, the backbone that now connects all the cell towers; if wireless were truly able to handle the data rates, the towers would be off the grid. They are not; and the "wholesale" wireless technology– microwave– has been the greatest single casualty so far during this wireless revolution.

Oct

12

Technical Break or Momentum Gaining, from Craig Mee

October 12, 2010 | Leave a Comment

Watching (and trading) GBPUSD today brings up a few interesting oberservations. As cloudy skies enveloped Tokyo and the Nikkei started to get hosed, S&P futures fell easily to carve through the bid. Gold struggling, Crude off ok, specie longs on the QE train booking. Will it turn the USD position?

Watching (and trading) GBPUSD today brings up a few interesting oberservations. As cloudy skies enveloped Tokyo and the Nikkei started to get hosed, S&P futures fell easily to carve through the bid. Gold struggling, Crude off ok, specie longs on the QE train booking. Will it turn the USD position?

GBPUSD…bid early… easing easing, bang, through 158.60, and straight to 1.5790 …stops …trendline break…not sure but Europe had been in for 3 hrs, and had good time to look at day's Asian events before acceleration took hold.

Who knows whether technicals are worthy, or if it's just a momentum play, and a flip of the coin…but the break on the day seemed long overdue.

Bill Egan writes:

Gold and dollar even more extended now in model space with values consistent with a reversal; by analogy a couple of springs pulled too far…looking forward to seeing whether this will be a mild pause or rush back.

Oct

12

Exiting Trades, from Craig Mee

October 12, 2010 | Leave a Comment

Exiting trades is always the toughest part of the game for me on a speculative basis, especially wanting to book trades to protect P and L, after taking a few hits. But what I find interesting is some trades are easier to let run than others with the same risk on the board. And it will come as no surprise to all that these are the low volatility plays… but what is it? Realistically the high volatility are the trader's saviors, and can turn a 3 bagger into a 8 bagger in a heartbeat. These are precisely the ones we should be putting on the risk and shutting down the screen. But hey the risk of scratching in a heartbeat is only too real as well, and there lies the trade off.

Exiting trades is always the toughest part of the game for me on a speculative basis, especially wanting to book trades to protect P and L, after taking a few hits. But what I find interesting is some trades are easier to let run than others with the same risk on the board. And it will come as no surprise to all that these are the low volatility plays… but what is it? Realistically the high volatility are the trader's saviors, and can turn a 3 bagger into a 8 bagger in a heartbeat. These are precisely the ones we should be putting on the risk and shutting down the screen. But hey the risk of scratching in a heartbeat is only too real as well, and there lies the trade off.

Alan Millhone writes:

The late Tom Wiswell said, "keep the draw in sight" at the Checker board. Knowing when to execute a trade at the board certainly carriers over to stock trading and knowing when to liquidate your position on the board or at the big board.

I spent this past week in Medina,Ohio as referee for a world title "Free Style" Checker match of 24 games between reigning Champion , Ron "Suki" King of Barbados and challenger Dr. Richard Beckwith of Ohio. I know a little about Checkers and watching these two Grandmasters all week was quite a treat.

Games one through twelve were all drawn and the players knew when to liquidate their position and make effective trades to exist the game. Suki "changed up" in game 13 and won as Dr. Beckwith stuck around too long and got into trouble by not having an effective exit strategy and lost.

I sat and witnessed game 22 as Dr. Beckwith improved on an ending that Suki and the late Derek Oldbury of England played off another opening that transposed into the line of play that was used in game 22. After 4 hours and 22 minutes Dr. Beckwith emerged as the victor after a hard fought ending that Suki could not escape. Dr. Beckwith had previously studied this ending that arose in game 22 and knew how to win the ending. Hand held notes as the Chair admonishes at the Checker board or the big board are critical to survive.

Suki drew game 22 and won the final game with an odd line of the "Tillcoultry" opening that Dr. Beckwith failed to meet correctly and did not trade out early enough and lost on a ending bind that he could not escape.

"Knowledge is power" on both boards. I was a first hand eye witness to this all last week watching these two greats do battle over the checkered squares.

As Chair points out, there are direct correlations to board games and stock trading and stock exit strategies that will help keep you unscathed.

Phil McDonnell writes:

One strategy I use with certain option spreads is something I call stop profit exit. I talked about it in my book. For strategies such as butterflies and calendar spreads the profit peaks out at a certain definable point relative to the underlying asset. For many ratio spreads there is a peak profit but that point changes dynamically with time. The point is that deciding to get out at the peak profit is a no brainer. Once it hits that point you will give money back if it goes up or down from there. The exit can and should be should be mechanical.

The probability of touching a price target is governed by our old favorite the arc sine distribution. Because of the Reflection Principle the probability of the target being touched is twice that of it being above (or below) that target at the end of a given time period.

Oct

12

The Heck With “Wall Street”, from Alan Millhone

October 12, 2010 | Leave a Comment

Headed to the Sundance Film Festival is the movie King Me, a documentary on the game of Checkers and players from around the globe.

Film producer Geoff Yaw of Think Media of Mayfield Heights, Ohio has a running blog at King Me that can be found by Googleing.

Regards,

Alan Millhone

President American Checker Federation

Oct

12

Time is greater than Money, from Kim Zussman

October 12, 2010 | Leave a Comment

The psychology of time in trading/investing may attribute in part to

The psychology of time in trading/investing may attribute in part to

the fact that money is more fungible than time; lost money can be made

back but not lost time. Similarly, is time lost attending to markets

compensated adequately? :

"The results of five field and laboratory experiments reveal a "time versus money effect" whereby activating time (vs. money) leads to a favorable shift in product attitudes and decisions. Because time increases focus on product experience, activating time (vs. money) augments one's personal connection with the product, thereby boosting attitudes and decisions. However, because money increases the focus on product possession, the reverse effect can occur in cases where merely owning the product reflects the self (i.e., for prestige possessions or for highly materialistic consumers). The time versus money effect proves robust across implicit and explicit methods of construct activation."

For example, which wine is more appealing:

"The greatest wine Quiot has ever made in my opinion, this wine shows a dense ruby/purple color and a gorgeous nose of camphor, blackberry, kirsch, some roast beef and Provencal herbs. Full-bodied with great intensity, beautiful purity, a multi-dimensional mouthfeel, and a spectacular finish of close to a minute, this is a fabulous effort from Quiot and should drink well for close to two decades" (Robert Parker)

or

"An expensive French wine at a reasonable price"

(Domaine Du Vieux Lazaret Chateauneuf du Pape Cuvee Exceptionnelle 2005)

Oct

11

Thoughts on Wall Street II, from Jeff Watson

October 11, 2010 | 5 Comments

I would love to hear comments from you all if you've seen Oliver Stone's new Wall Street II. Yesterday, my companion and I went to see the movie and nearly walked out after 15 minutes, it was that bad. Blaming speculators for the "Crisis," irrelevant discussion of "Moral Hazard," the Lehman and Bear Sterns references, heroic yet cutthroat actions of the bankers, artful cutouts of the talking heads of CNBC, the Oracle of Omaha, the improbable plot line, the horrible dialogue, Michael Douglas' insufferability, the resurrection of the corpse of Eli Wallach, the Phoenix like rise of Gordon Gekko, the tangled plot line!!!

I would love to hear comments from you all if you've seen Oliver Stone's new Wall Street II. Yesterday, my companion and I went to see the movie and nearly walked out after 15 minutes, it was that bad. Blaming speculators for the "Crisis," irrelevant discussion of "Moral Hazard," the Lehman and Bear Sterns references, heroic yet cutthroat actions of the bankers, artful cutouts of the talking heads of CNBC, the Oracle of Omaha, the improbable plot line, the horrible dialogue, Michael Douglas' insufferability, the resurrection of the corpse of Eli Wallach, the Phoenix like rise of Gordon Gekko, the tangled plot line!!!

I could go on and on. Does anyone else agree with me or am I overreacting? Frankly, instead of wasting my money on this horrible movie, I wish I would have sat home watching the local Spanish Channel watching my favorite telenovela, where the passion is real, and the revenge is sweet…and believable.

Sushil Kedia writes:

I attended the movie too. One good thing was the movie hall, the seats were extra comfortable, and it had a really good ambiance. Some things in India have changed for the better, in such measure.

But that's not all. Michael Doulgas resembled someone too popular on Wall Street. Someone whose name reads backwards and forwards the same kept coming to mind on the facial lines and contours that Douglas exuded effortlessly. The flinch, the long deep gaze, so many other things were all pretending to mimick the famous name. Was it a flawed make up design or a purposeful resemblance created for getting "eyeballs"?!

As a movie making exercise, this seems to me an outright fraud. But then again, I did witness such fraud pass by in the form of a movie effortlessly. The crowds in India may not have noticed it, really.

In the same vein, my two humble cents submitted herewith are that for non Wall Streeters the movie could well be a good entertaining account of so many things relating to lives on the Wall Street. A movie is after all an illusion and an entertainment. For those from the Street and around it, of course the real stuff is so much more real that forget Oliver Stone, any other movie maker will find it difficult to please us and to get close to portrayals of genuine resemblance.

But then, how could Douglas be made to resemble the big name so well. Accident? Design? Transferred Epithet?

The human touch, the daughter, the fetus, the tears all came in to show that the street does have living beings. Huh! I would say the guy scripting the story forecasted the depressing markets would be lasting until the 3rd quarter of 2010 and settle with a simpler way of reasoning why the movie is what it is: It wasn't made for educating this universe about what Wall Street is. It was made for making money while the makers forecasted the Street would still be not making any. Bad forecast, that's all. Else the movie being a movie is fine.

Jeff Watson writes:

Did you notice the photo-shopped picture on the fireplace mantle of Josh Brolin with his character and the Palindrome? I got a kick out of that one.

Oct

11

The Pendulum Swings, from Rocky Humbert

October 11, 2010 | Leave a Comment

Every weekend I read through some classic papers from another era. With inflation expectations percolating, this weekend's reading were the many papers which pondered the failure of stocks to perform according to common sense during the inflation of the last secular cycle. (One suspects that the bear market of 2000- ? will give rise to a crop of similar articles that will provide amusement comparable to reading a Sears Roebuck catalog from the 1930s ….)

Every weekend I read through some classic papers from another era. With inflation expectations percolating, this weekend's reading were the many papers which pondered the failure of stocks to perform according to common sense during the inflation of the last secular cycle. (One suspects that the bear market of 2000- ? will give rise to a crop of similar articles that will provide amusement comparable to reading a Sears Roebuck catalog from the 1930s ….)

The Alpine Knock-About Fedora Hat for $0.69 and the silk ladies Clever Collar for $.29 reminds one of: R. Geske & R. Roll (J. Finance, March 1983) "The Fiscal and Monetary Linkager between Stock Returns and Inflation"

Abstract:

Contrary to economic theory and common sense, stock returns are negatively related to both expected and unexpected inflation. We argue that this puzzling empirical phenomenon does not indicate causality. Instead, stock returns are negatively related to contemporaneous changes in expected inflation because they signal a chain of events which results in a higher rate of monetary expansion. Exogenous shocks in real output, signaled by the stock market, induce changes in tax revenue, in the deficit, in Treasury borrowing and in Federal Reserve "monetization" of the increased debt. Rational bond and stock market investors realize this will happen. They adjust prices (and interest rates) accordingly and without delay.

Although expected inflation seems to have a negative effect on subsequent stock returns, this could be an empirical illusion, since a spurious causality is induced by a combination of (a) reversed adaptive inflation expectations model and (b) a reversed money growth/stock returns model. If the real interest rate is not a constant, using nominal interest proxies for expected inflation is dangerous, since small changes in real rates can cause large and opposite percentage changes in stock prices.

Finally, one notes that the real interest rate is currently -0.81% for cash, and 1.40% for the ten-year. Both are at 2-sigma lows. Where can they go but up? And is this bullish or bearish for stocks and bonds? Hmmm.

Vince Fulco writes:

One notes the newspaper boy hat has been creeping into Minneapolis clothing trends for the last 6 months. Some guys even wearing them in the height of summer. I guess what comes next is "a chicken in every pot" meme…

Kim Zussman writes:

Checked this using BLS monthly CPI data and SP500 returns. Here is regression of stock returns vs contemporaneous CPI change:

Regression Analysis: mo ret versus chg cpi

The regression equation is mo ret = 0.00935 - 0.00906 chg cpi

Predictor Coef SE Coef T P

Constant 0.009345 0.002033 4.60 0.000

chg cpi -0.009058 0.004278 -2.12 0.035

S = 0.0419261 R-Sq = 0.6% R-Sq(adj) = 0.5%

As they say, the correlation is significant and negative (though RSQ is small and thus CPI explains little of monthly stock return).

Checked also whether this month's change in CPI predicts next month in stocks (with the usual answer, no):

Regression Analysis: M ret versus M-1 cpi chg

The regression equation is M ret = 0.00811 - 0.00503 M-1 cpi chg

Predictor Coef SE Coef T P

Constant 0.008108 0.002040 3.97 0.000

M-1 cpi chg -0.005026 0.004291 -1.17 0.242

S = 0.0420445 R-Sq = 0.2% R-Sq(adj) = 0.1%

To see how this has evolved over time, checked correlation between chg cpi and SP500 ret for non-overlapping 60-month periods:

Year corr 60 avg cpi

2010 0.12 0.18

2005 -0.17 0.22

2000 -0.04 0.20

1995 -0.25 0.24

1990 -0.15 0.33

1985 -0.22 0.44

1980 -0.12 0.71

1975 -0.32 0.55

1970 -0.18 0.35

1965 -0.07 0.10

1960 0.25 0.17

1955 0.02 0.17

As shown on the attached graph of data above, most of the negative correlation between cpi and stocks occurred in the good old days of high-cpi (70's-80's), when certain parties where whipping inflation now.

What will they whip next?

Oct

11

Horse Tradin’, from Chris Tucker

October 11, 2010 | Leave a Comment

Just in the middle of Ben Green's fabulous Horse Tradin' and came across this gem. One of many:

However he led you to believe– in fact, he was ready to confess– that he was a gentleman of the highest order and horsemanship and horses were not a business with him but a love; a part of his life that he couldn't do without. That was the real reason for his being in the horse business, and not because of any money that might be connected with the running of a livery stable and the buying, selling, and trading of horses. This kind of angle on things was sort of a a new breed of animal with me. I thought horse people were in the horse business because they had to be or because they wanted to be, and since I was a small boy I've more or less considered the horse business not a business but a disease. The thing a horseman ought to do was to learn all he could about the disease, so he could live with it without its totally ruining him, financially and otherwise.

Oct

11

Bulls Party, from Victor Niederhoffer

October 11, 2010 | 1 Comment

With S&P, Crude, Naz, Dow, Euro, Bund, gold, Yen, Dax, Estox, Silver, corn, wheat, soybeans, oats, and hundreds of individual stocks at 1 month highs, it is interesting to reflect how long a bull move can last and how far it can go, when fueled by all the wealth that other bulls have and helped along by expansionary policies by the central banks.

With S&P, Crude, Naz, Dow, Euro, Bund, gold, Yen, Dax, Estox, Silver, corn, wheat, soybeans, oats, and hundreds of individual stocks at 1 month highs, it is interesting to reflect how long a bull move can last and how far it can go, when fueled by all the wealth that other bulls have and helped along by expansionary policies by the central banks.

Ken Drees comments:

Since QE is the direct stock and bond market impetus at the moment through indirect likely promises of a recent fed statement and made very pseudo real by the never interviewed but very smart and successful David Tepper on CNBC who basically spelled it out for everyone that the markets are indeed going higher, I say that this rally lasts at least into election day and into the fed meeting where rumor/fact becomes real. All other momo markets are induced as well to grow since the QE feeds them too as collateral liquidity buckets.

As long as I read and hear topaganda I lean bullish.

Gary Rogan writes:

Wow, that was an interesting thought. On Friday I bought something for the first time in 1.5 years, and the first thing ever that wasn't a stock, and that was UNG. I just figured the risks over the next year which is the shortest period of time I intend to hold it are not that high. And for somebody who only buys at 52 week lows the chart looked like the most beautiful thing in the world.

Jeff Sasmor comments:

Just be aware of how UNG has to roll the underlying position once a month. I happen to be in this one too– but it can grind lower and lower on you. And once a month it's gamed when it rolls to the next month. The effect has been discussed to death in many venues. So it's tricky to hold it for a long time if it stays in a range.

Craig Mee adds:

Certainly might drive the speculators out, (or clobber them if they fade it), as runaway markets present less and less opportunities if one isn't in and sitting tight.

Kim Zussman writes:

About the only asset class that hasn't been goosed limit up is real estate. A big up-move in house prices would be very useful, driving LTV down, reducing foreclosures, and re-priming the dual wealth effects of McMansion braggadocio and cash-out refinancing. Not to mention fulfilling the campaign promise of re-establishment of the American Dream.

Oct

8

Smart Swarms, from Jim Sogi

October 8, 2010 | 1 Comment

The Smart Swarm by Peter Miller analyses crowd decision making by looking at ants, bees, locusts, and then humans. He discusses various heuristics making delayed response decision making difficult. The thermostat game and the beer game are good examples of difficulties in making decisions where the results are delayed. It usually ends up in a boom bust cycle. The cure is to reverse against the trend earlier. Experiments show that decisions made by 3 average persons are better than those made by the smartest person due to diversity of information. This is the Slumdog Millionaire phenomenon where the crowds answer tends to outperform the experts. Analysis of ants and bees show how the swarms make decisions: they simply follow those next to them. The remarkable aspect is how this information travels across large groups almost instantaneously and how this information is more than any of the individuals would have access.

The Smart Swarm by Peter Miller analyses crowd decision making by looking at ants, bees, locusts, and then humans. He discusses various heuristics making delayed response decision making difficult. The thermostat game and the beer game are good examples of difficulties in making decisions where the results are delayed. It usually ends up in a boom bust cycle. The cure is to reverse against the trend earlier. Experiments show that decisions made by 3 average persons are better than those made by the smartest person due to diversity of information. This is the Slumdog Millionaire phenomenon where the crowds answer tends to outperform the experts. Analysis of ants and bees show how the swarms make decisions: they simply follow those next to them. The remarkable aspect is how this information travels across large groups almost instantaneously and how this information is more than any of the individuals would have access.

Phase transition is the point at which the entire crowd or swarm behavior changes. Birds, locusts, fish, people in crowds, and even inert molecules can all instantly change phase. Markets seem to as well. Computer modeling requires quantification, and interestingly as Wolfram posited, simple rules create complex behavior and learning that arrive at group solutions which are not preprogrammed in. This differs and improves upon statistical analysis in its adaptability to change and new information. This recalls Wolfram's thesis where simple rules create complex patterns and reverse engineering is hard. Miller looks at the process of reverse engineering crowd decisions. Analysis of crowd stampedes in Mecca show waves in pilgrims backing up before the stampede. Traffic shows similar waves in traffic jams. Analysis of locusts show the rapid change in behavior of the locusts when crowded. One of the beauties of the market is the plethora of data and the platforms to deliver and analyze it. Half the problems the scientists faced was data collection. The question is what are the precursors and triggers to phase change in markets? There is a tipping point to every change in direction, of which there have been many recently. There are precursors, triggers and the phase change. These conditions when identified might give good signals. Pit traders seem to have worked out the dynamic in the pit, but what are the electronic signals? If ants and bees can work this out, can't traders?

Pitt T. Maner III comments:

Now that almost everyone has a smartphone, iPhone, etc, the potential for "super swarms" to develop amongst groups of people seems ever more heightened. One can imagine interesting collaborative efforts forming inside and outside of company boundaries. Swarmanomics. Or in negative cases, mobocracy—mobile vulgus.

It is reminiscent of the bee returning to the hive and doing a little dance to give the direction, distance, and quality of potential food.

One such network is Foursquare, where you can become a virtual "mayor" by being a habitue and boulevardier and a potential director of traffic (or dare say, wallets) to locations. Status and prestige are bestowed to the tireless, individual "worker bee". Where is the party today? Will not "killer" bees and killer apps be soon to follow? Facebook has entered this arena too. Marketing on steroids.

The head of Foursquare states his idea of the future here:

Crowley also offered a glimpse of his vision of Foursquare's long-term future. "In the future, I want Foursquare to be able to tell people where to go wherever they are in the world, based on their previous visiting habits, likes and dislikes and the time of day…We want to be able to push venue suggestions to you. That's what I am pushing towards as we develop Foursquare's tools and how we use our data," he explained.

While the super swarm badge is among the hardest to win, the significance of last night's event is somewhat debatable. There is very little, physically, to show for this achievement. But as social gaming takes off, game mechanics– the idea of giving out tiny rewards to encourage certain behavior– are very much in vogue, with several start-ups and marketing campaigns incorporating check-ins and badges.

Oct

8

Contrary-Contrary-Contrary Indicator, from Nigel Davies

October 8, 2010 | Leave a Comment

Please note that I have no position in gold and am therefore not posting through nervousness or to cheer my position along. So objectively speaking there are a couple of reasons why this can be an interesting moment:

1) People have been SO bullish on gold that it will take them a while to reverse their positions.

2) This kind of overwhelming consensus will draw in many weak bulls who are likely to panic.

3) Such days provide markers for many traders to enter against the prevailing trend.

But don't let a chess player worry you… N

Oct

8

Ode to a Dying Dollar, from Kim Zussman

October 8, 2010 | Leave a Comment

To the tune of Roy Orbison's Crying:

I was all right…for a while,

I could smile…for a while

But your central bank put me in the tank

Can you not debase me….so

Oh, you wished me well, but you couldn't tell

That I've been dying over you, dying over you

And you said, so long

Left me on my own

Alone and dying, dying, dying

It's hard to understand that just one sentence can

Start me dying

Thought that we were through

Helicopter view

Even faster than before

But what can I do

For you don't love me and I'll forever be

Dying 'cause of you, dying 'cause of you

Dying…dying….dying

Oct

8

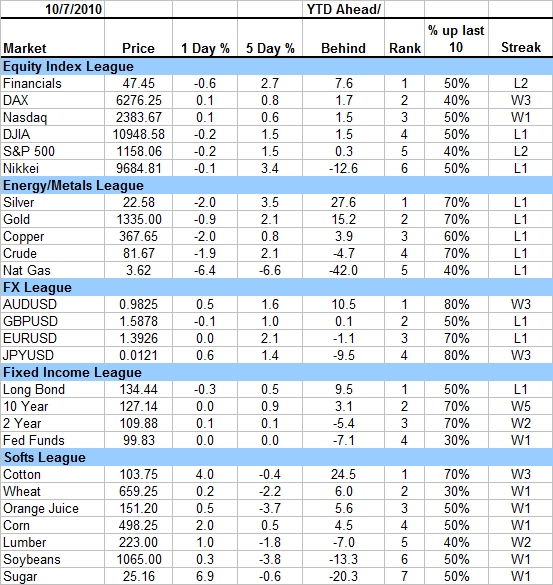

Market Standings

October 8, 2010 | Leave a Comment

©Daily Speculations 2010

The "YTD Ahead/Behind" is calculated by assigning each market a base index value of 100 as of 12/31/2009, then multiplying this base index value by the respective % change for the year (ex. +20% YTD would produce an index value of 120). Afterwards, the average of each league is calculated and subtracted from the individual current index levels to produce the amount ahead/behind."% up last 10" is the percentage of the last 10 sessions that were >0. For example, if 5/10 sessions were >0 this would register as 50%."Streak" is the consecutive number of wins/losses on a net change basis as of the most recent date. For example, W4 would mean a particular market was up the last 4 sessions. L2 would mean 2 down sessions in a row, etc.FX league is calculated expressing USD per foreign currency. This is done to normalize quotation methods across the currencies. All are expressed such that a move higher (aka % change >0) is an appreciation of the foreign currency and a depreciation of the USD. A % move <0 would be a USD gain at the expense of the foreign currency.

Oct

8

A Deserved Compliment, from Victor Niederhoffer

October 8, 2010 | Leave a Comment

One must compliment the checker player who jumps backwards and forwards for his insightful comments about the currencies and the market which in Russian fashion happened faster than a Troika from Minsk to St. Petersburg.

One must compliment the checker player who jumps backwards and forwards for his insightful comments about the currencies and the market which in Russian fashion happened faster than a Troika from Minsk to St. Petersburg.

George Parkanyi writes:

It gave me a breather at least today. Unlike all you prescient folk racking up the gold and silver bars, I'm staring down the business end of this juggernaut wondering "OK, why is nobody else over here?". Wait– a voice. Anatoly?

It's quite remarkable how little there is to hang on to on the nose cone of a rocket. So while today's jolt raises the hope of "Ah, finally, a malfunction; we're going home.", the sad Darwinian reality may be that this was only the first booster jettisoning to make way for the next.

Oct

8

Will Oil Sink the Fed’s QE2, from Gary Rogan

October 8, 2010 | 2 Comments

I've always thought that using higher inflation as motivation for QE2 as Dudley has been doing lately is (a) deceptive (b) counterproductive (c) just plain stupid. Could this insanity work only too well quickly in one particular area?

Read more in this article $100 Oil Could Sink the Fed's QE2.

Oct

8

Coining a New Market Word, from Ken Drees

October 8, 2010 | Leave a Comment

Most all articles that proclaim "tops" from wall street news sources

are to be suspect. One must treat such advertisement as "topaganda".

"Long in the tooth" is such an old Barrons phrase– often used by "old curmudgeons".

Oct

7

Stocks and the Stock Market (1910), from Jeff Sasmor

October 7, 2010 | 3 Comments

I found this book online while searching for something else. I'ts out of copyright (from 1910).The "Read Online" mode is interesting in that it shows the underlining that someone made to this volume.

I found this book online while searching for something else. I'ts out of copyright (from 1910).The "Read Online" mode is interesting in that it shows the underlining that someone made to this volume.

Here's a section (I haven't had time to go through all of this tome) that seemed to me to have some parallels to today's situation. Actually, it's more than a bit eerie! There's also mention of the "curb market" — something I posted about recently. Later sections (~pg 57) show some stocks– none of the names I saw still exist, but most had nice healthy dividends from 5-7%.

Those were the days!

The financial and business panic of 1907 serves as the latest illustration of the significant fact. The business conditions of 1906 were the best that this country has ever enjoyed. Mills were running overtime, railroads were congested with traffic, and real estate operations were booming. The press was filled with the most roseate "write-ups" and predictions, yet despite the good news security prices showed little gain following the month o*f August. The earmarks of coming financial and business distress were at hand. The stock market was serving its purpose as the pivotal point where thousands of the brainiest men of the world were acting on judgments which-*had reference to the future and not the present.Stocks were for sale by those who reasoned correctly and knew, and were purchased by those who did not know so much. They were even sold at a sacrifice, and as knowledge of the coming state of business affairs percolated from one strata of investors to another, the selling movement became more violent, and in March of 1907 we had our first stock exchange panic. A rebound in prices occurred, but stocks were still for sale, and in July we had our second panic. In the meantime, however, business was excellent, and the press of nearly the whole country wondered what all the trouble was about, and why the Wall Street gamblers were thus losing their senses. The business depression, however, followed, and when it was a reality to even the most ignorant, the stock market had clearly discounted the event, and prices of securities refused to yield further. When business was at its worst, complaints the loudest, and the public press blue as indigo, stock market prices were again merrily ascending The exchange was again the pivotal point where thousands of the best minds of the country were ex- pressing their judgment of the future, and were willing to convert their cash into securities, because of the anticipated increase in value.

It is the failure to understand this fundamental law of price movements which has been the cause of enormous losses to the un- thinking and unknowing, whose judgments are based on what is seen and heard at the time. When the good news, whether it be big crops or large earnings, becomes common property, it has been discounted by the stock market ; and similarly, when the bad news is apparent to all, it has likewise been discounted. It is only natural, therefore, that the rank and file should regard the stock market as a most incomprehensible affair, "a bottomless pit," always going contrary to what is so perfectly evident at the time. But one should remember that the stock market is not distinct from other markets. The manufacturer, the merchant, the produce dealer and the real estate operator, all have an interest in its fluctuations, since they have an important bearing on their own transactions. Many of the stock market fluctuations, especially those of a few days or weeks, have little significance, since they may represent only some particular local cause or the whim of some speculator. But if the market steadily and rapidly declines, many business men, who know its "discounting" significance, will assume a waiting attitude as regards their planned undertakings, or curtail their production ; and this waiting attitude, since all business is closely interrelated, will react upon all other forms of business effort.

In this connection attention should be called to the operations of the so-called "bears" who speculate for the fall of stocks through the process of selling "short" that which they do not possess with the object of buying back later at a lower price, and fulfilling delivery on their contract. Many condemn and few sympathize with the "bear" in the market, because of the belief that it is wrong to sell that which one does not possess, that no economic good is performed by this practice, and that "short selling" artificially depresses security prices. In fact many have recently strongly urged the prohibition of such sales.

A moment's reflection, however, will show that all these conclusions have little basis in fact. These critics forget that "short" selling is a common practice in practically all kinds of business. The manufacturer is expected by the wholesaler to sell his finished wares at a definite price for some definite future delivery, and to insure the delivery of his goods at a stipulated price and time, the manufacturer expects the commission man or produce broker to sell the raw cotton or grain or metal for future delivery at a definite price, long before the crop has been harvested or the metal obtained. Contractors, likewise, in contracting for work at a definite price, are constantly selling labor and materials short. The general practice of "hedging" on our exchanges, resorted to by nearly all business men handling our important staples, must necessarily involve a short sale. In business generally, "short selling" is regarded as a necessary means of insurance against business or speculative losses. If recognized here by all persons who have an understanding of business methods, it certainly cannot be maintained that it is wrong in the stock market to sell something which one does not now possess and intends to buy later.As regards the two other contentions, that short selling does not perform an economic good, and that it actually depresses the prices of securities, these critics are in the wrong. The short seller in the stock market is often the greatest benefactor in repress- ing rampant speculative enthusiasm on the one hand, and in checking the effects on security prices of excessive pessimism on the other.

Oct

7

A Proverb, from Victor Niederhoffer

October 7, 2010 | Leave a Comment

The realization is is often faster than the anticipation. Or as they say in chess "the threat is worse than the execution".

The realization is is often faster than the anticipation. Or as they say in chess "the threat is worse than the execution".

William Weaver adds:

And many times less satisfying.

Anatoly Veltman writes:

Yes, I always remembered that one, since my coach mentioned it when I was 6; but I couldn't quite implement till I turned 12– and only then won first title.

David Hillman writes:

Like Fedex next day air. More often than not, when we ship coast to coast and the client says 'email the tracking number', I say 'you'll have the package before you have the tracking number'. Given system limitations, human intervention, variance in 'normal business hours' and time zones, Fedex makes it possible to physically move a package 3000 miles faster than we can get tracking data to the client electronically. One of the more satisfying examples of 'rapid realization'. Any market parallels?

Oct

7

Voluntary Exchange, by Gregory Rehmke

October 7, 2010 | 2 Comments

With voluntary exchange, both parties benefit, or expect to. Charity is no different, especially in a wealthy society. Local knowledge is key for effective charity, and it makes sense for a reality TV show, where an outside audience shares the vicarious pleasure from philanthropy, to research the family in need before documenting the transaction.

With voluntary exchange, both parties benefit, or expect to. Charity is no different, especially in a wealthy society. Local knowledge is key for effective charity, and it makes sense for a reality TV show, where an outside audience shares the vicarious pleasure from philanthropy, to research the family in need before documenting the transaction.

Gertrude Himmelfarb’s “The Idea of Poverty” and “Poverty and Compassion” discuss the rich history of compassion for the poor, and the challenge of helping the “deserving poor”. Elites developed charities to provide support with the least disruption of incentives.

Both parties benefit. Those who give money to improve the lives of others prefer that expenditure to alternatives. They gain great satisfaction from giving that makes a difference, and some givers also gain from the sense that their peers will be impressed by their skill in effective charity.

So three cheers for reality TV series entrepreneurs who highlight philanthropy entrepreneurs and draw additional funds from advertisers and cable subscribers to give to the deserving poor.

Oct

7

What’s With the Sixes, from Anatoly Veltman

October 7, 2010 | 1 Comment

Ever since the big S&P bear market low of 666 [on 2009/03/06] (hit precisely at the end of long voyage from 1586 top), traders seem to have found a religion. Gold bumped into 1266, and couldn't overcome it all summer long! And finally 1366 this morning. Once a staunch atheist, I'm a believer myself now– I think.

Kim Zussman comments:

This is an example of the hypo-arcsine law: X6666 is always 2/3rds of something, which is itself is an artifact of the hubristic categorization of the universe in base 10.For example in tennis, every shot has to cross the 2/3 point between players before the ball can be returned.

Oct

7

Currency Level Discovery on Columbus Day, from Anatoly Veltman

October 7, 2010 | 2 Comments

I recall February 14th of 1994, the day dubbed "Valentine Day massacre" by currency traders. Palindrome decided to cover what was rumored to be over 2 trillion Short Yen position. The position was in fact smaller; but market smelled blood, and had him pay up un-fathomable 4 full figures, for a whopping $600m daily loss…

I recall February 14th of 1994, the day dubbed "Valentine Day massacre" by currency traders. Palindrome decided to cover what was rumored to be over 2 trillion Short Yen position. The position was in fact smaller; but market smelled blood, and had him pay up un-fathomable 4 full figures, for a whopping $600m daily loss…

Approaching U.S. Columbus Day Bank Holiday, there are few obvious parallels. There is a factor, however, to keep traders up on their toes: most currency pairs are presently stretched way out of their historic norm.

Case 1: .95 Swiss Francs never bought 1 USD in the entire FX history to-date, rallying daily over 4 straight months now!

Case 2: Australian Dollar has never before traded at parity with USD, rallying daily over 4 straight months now!

Case 3: Japanese Yen is assumed to chase its all-time record against USD, following 5-month rally!

Case 4: even the beleaguered Euro-currency, below 1.19 three months ago (with calls down to parity at that time) has just sprinted to 1.40 instead!

So the SNB [Schweizerische NationalBank] is ready to quietly offer its own currency (for Euros?), the BOJ is ready (not so quietly) to sell its currency for Dollars, the market participants worldwide are ready to finally stop bidding up unbelievably costly US fixed income paper. So what do you think of conceivable currency trend reversal: before the holiday, during the holiday or after the holiday?

Oct

6

The American Dream, from George Parkanyi

October 6, 2010 | Leave a Comment

If you think you've lost the American dream and are searching to find it again, look no further than reality TV. Yup, you heard me right– reality TV. There is a show that plays on the home and garden channels called Extreme Home Makeover, where the show picks families where the parents are wonderful, giving to people in some fashion, but are under extreme duress because of health and/or financial issues. It sends them to Disney World for a week, and in that one week tears down their barely functional, problematic and sometimes dangerous existing home, and builds them a beautiful, brand new home.

If you think you've lost the American dream and are searching to find it again, look no further than reality TV. Yup, you heard me right– reality TV. There is a show that plays on the home and garden channels called Extreme Home Makeover, where the show picks families where the parents are wonderful, giving to people in some fashion, but are under extreme duress because of health and/or financial issues. It sends them to Disney World for a week, and in that one week tears down their barely functional, problematic and sometimes dangerous existing home, and builds them a beautiful, brand new home.

They engage the local community– volunteer contractors, ordinary people, local businesses etc.– who all band together to complete these magnificent projects. Often, the sponsors help in other ways like paying off medical debts.

For example on this evening's show, they picked a couple from Toledo, a fireman and his social worker wife, who had three kids of their own, and then adopted 8 more, 5 from Haiti and 3 from inner-city Toledo. They were all living in this tiny house in pretty serious disrepair for lack of funds, and the woman was recovering from a medical condition that had already almost killed her and they were all trying to get by on his one salary and also coping with medical bills.

The wonderful thing about this show is how it changes people's lives, especially those of people that are unquestionably deserving of a leg-up. It gives a fresh start and new hope to the receiving family, and wonderfully energizes the community. Literally hundreds of people participate. That's what I think the true American dream really is abou– unbridled can-do optimism and hope. At least from the perspective of this Canadian.

Watch the show some time. I'd wager that you'll find it quite uplifting.

Kim Zussman plays the Devil's Advocate:

This may seem heartless, but this clips down to current political-hollywood rhetoric:

Lost American dream (what is it anyway?)

Searching to find it (whatever)

Families –where the parents are wonderful (and need help, but not with birth control) giving people (who wind up taking) under extreme duress (get in line) health and/or financial issues (get in line), sends them to Disney World (where else. What about going to work?) barely functional, problematic and sometimes dangerous existing home (you should see the ones in China where kids study linear algebra) and builds them a beautiful, brand new home (take a mortgage and go back to disney). They engage the local community (you knew that was coming), volunteer contractors, ordinary people, local businesses etc. – who all band together (but evidently don't need to feed their own families) to complete these magnificent projects (the ones they charge for are capitalist, evil, and taxable) paying off medical debts (because medical care is a right that hollywood will pay for to sell soap). Why not instead inspire the nascent dependency with Horatio Alger ?

Oct

6

In General, from Victor Niederhoffer

October 6, 2010 | 2 Comments

In general, when one is winning in life, sports, or markets or gold, it is not good to climb the high horse about ones greatness or profits.

Ken Drees writes:

Maybe some people are counting coup and thus only fulfilling their warrior instinct. There may be market implications here in general as one needs to be able to get one's guts into a trade and brush the enemies cheek before putting on the trade.

Oct

5

Come to Junto, from Dailyspeculations

October 5, 2010 | 1 Comment

Veronique de Rugy will be speaking at Junto on Thursday, at The Mechanics Institute at 20 West 44th St. Her talk is on "The Political Economy of Stimulus". This should be a very interesting speaker.

Veronique de Rugy will be speaking at Junto on Thursday, at The Mechanics Institute at 20 West 44th St. Her talk is on "The Political Economy of Stimulus". This should be a very interesting speaker.

She is taping with Stossel today.

Everyone is welcome.

[Ed.: Note well: 20 West 44, corrects earlier error].

Oct

5

How to Jump Off a Runaway Train, from Rocky Humbert

October 5, 2010 | 2 Comments

Certain (unmentionable) positions in my portfolio are starting to act like a runaway freight train. It therefore seems an opportune moment to consult my copy of The Worst Case Scenario for the correct methodology for "how to jump off a runaway train." (One notes the instructions do not mention the purchase of puts and put spreads.)

Certain (unmentionable) positions in my portfolio are starting to act like a runaway freight train. It therefore seems an opportune moment to consult my copy of The Worst Case Scenario for the correct methodology for "how to jump off a runaway train." (One notes the instructions do not mention the purchase of puts and put spreads.)

1. Move to the end of the last car.

2. If you have time, wait for the train to slow as it rounds a bend in the tracks.

3. Stuff blankets, clothing or seat cusions underneath your clothes.

4. Pick your landing spot before you jump. Avoid trees, bushes and of course rocks.

5. Get as low to the floor as possible, bending the knees, so you can leap away from the train.

6. Jump perpendicular, leaping as far away as you can.

7. Cover and protect your head with your hands and arms, and roll like a log when you land. Don't try to land on your feet, or you'll likely break your ankles and legs. Do NOT roll head over heels.

Vince Fulco jokes:

Come on Rocky. The ice floating in the punch bowl has just settled after getting a "perceived" refill which may, just may, overflow the bowl. This is when the Bernanke dance party really starts to pick up with the fast music. Earning ZIRP and saving is for the wallflowers.

Scott Brooks comments:

Rocky's mention of some stocks acting like a runaway train makes me think that it's time to review my very simple fool proof methodology for stock investing.

Take two pieces of paper, one green one red.

On the green sheet, put all stocks that are going to go up. On the red list put all the stocks that are going to go down.

Then, go long all the stocks on the green list, and short all the stocks on the red list.

Sell any green list stocks once they go on the red list and cover your red list shorts once any stock goes onto the green list.

Repeat this process early and often.

Enjoy your profits!

John Lamberg writes:

And I thought the secret to the stock market was to buy low and sell high. Similarly, in the casino the secret is to bet big when you are going to win. Unfortunately, I seem to buy high and sell low, and every time I bet big it seems the dealer gets blackjack, although occasionally I get blackjack too, but being a fool I take even money when that happens.

Oct

5

The Heavy Hand of War, from Jim Sogi

October 5, 2010 | Leave a Comment

It's interesting trading in bonds and yen where you have large governments saying what they want the outcome to be. Even though it does not follow the script, there is a heavy hand over the market. When the policies start to collide, it appears to be a form of warfare.

Oct

5

TED Spread, from Ken Drees

October 5, 2010 | Leave a Comment

Lobag beginning anew?

Oct

4

One of the Greatest Errors, from Victor Niederhoffer

October 4, 2010 | 4 Comments

One of the greatest errors people make is to think that the level of good or bad economic or earnings news is related to future stock market performance. Always the market is anticipating the future, and the market now has in its sights the election, the coming increases in service rates, and all else.

One of the greatest errors people make is to think that the level of good or bad economic or earnings news is related to future stock market performance. Always the market is anticipating the future, and the market now has in its sights the election, the coming increases in service rates, and all else.

It is interesting to contemplate a graph of the DJI and its 10% continuous rise in September and relate it to Iowa bets on the outcome of the November election with its steadily decreasing blue line and increasing red line graphed below.

Ken Drees writes:

The idea that the market is a seeing creature, very blind short term but correct and on target 6 months out really has been taken for granted as an old sharp cutting saw. So what is the market seeing now 6 months out? In April when the market was topping–what did that market see for this October. Thereby in March of this year when the market was moving up–it forecasted the best September in 70 years?!

I really don't get this, but actually am programmed to believe that somehow the market sees things that the crowd doesn't. Now we are told that the market sees a republican victory and stoppage of anti-business actions–maybe the start of repeals against major programs, or at least old fashioned gridlock. What is the best way to use the market as a "seeing" tool?

Gary Rogan writes:

Everywhere I turn I read about how the liquidity injections by the Fed are what's really pushing the stock market higher. How would one go about separating the effects of the extra liquidity from the anticipatory ability of the market?

Also, since correlation does not imply causation, could it be that some of the same underlying causes that result in high liquidity also result in the increased republican takeover. For instance:

High Unemployment -> More Liquidity to Spur Employment -> Higher Stock Market

High Unemployment -> Higher Republican Chances

High Unemployment -> Lower State and Federal Revenues -> More Need To Borrow -> More Need for Low Interest Rates -> Higher Liquidity -> Higher Stock Market

…-> More Need To Borrow -> More Dissatisfaction with High Debt -> Higher Republican Chances

… -> More Need To Borrow -> Lower Dollar -> Higher Stock Market in Today's Dollars

High Unemployment -> Higher Mortgage Defaults -> More Government and Fed Intervention to Prevent Defaults -> Higher Dissatisfaction with These Efforts -> Higher Republican Chances

… -> More Need To Borrow -> Higher Concern with the Stability of the System -> Higher Gold Prices -> Higher Stock Market to Maintain Some Parity with Gold

This can go on for a while, but I think the point is clear.

Charles Pennington comments:

It would be alarming that the public apparently trades so poorly, but I've never actually met anyone who was a member of the public, so likely the losses are not significant, and whatever they are, surely they are compensated by all the winnings at poker, for I have not heard of a single soul who loses at that game.

Mr. KrisRock writes:

Has anyone seen "my old friend" Gold…he was supposed to top out like the way "gut feel" counting Russian said it would…unfortunately, Ben Bernanke's actions have made the Russian feel like he's not welcome at the FED…happiness in when you don't fight the FED but unlike the public who are buying GOLD hand over fist, the PROS always know right.

Jeff Watson adds:

Conversely, perhaps it's us "professionals" who are the ones who trade poorly, like I did a week ago last Friday going long the entire grain complex, only to get blasted on Monday and Tuesday. Or, like some of us who play poker, people like me who play six games at a whack on six screens on Pokerstars, losing at 5 of the games. Those losses, plus the vig, the mistakes, and the admitted waste of time and talent are the real crime.

Oct

4

Evolution in Warfare, from Gary Rogan

October 4, 2010 | Leave a Comment

Most warfare advances involve ever-increasing sophistication on both sides. But just like in nature where extremely primitive prions are unfailingly fatal to advanced mammals, warfare strategies obviously have to deal with primitive but effective threats. This is an interesting article about one example. A brief excerpt:

Most warfare advances involve ever-increasing sophistication on both sides. But just like in nature where extremely primitive prions are unfailingly fatal to advanced mammals, warfare strategies obviously have to deal with primitive but effective threats. This is an interesting article about one example. A brief excerpt:

US navy to battle Iranian mini-ekranoplan swarms with rayguns

The US military-industrial complex has unveiled its answer to the much-vaunted "swarm" tactics of the Iranian Revolutionary Guard naval forces, which might see squadrons of "stealth" flying boats and attack craft overwhelming the defences of US warships in the Persian Gulf. The US Navy will deal with this, apparently, using rapid-firing laser raygun cannons to sweep their swarming enemies from the seas and skies around them. American weaponry megacorp Northrop Grumman says that shorebased testing of its Maritime Laser Demonstration (MLD) blaster cannon have been successful, and the firm is confident that seagoing trials later this year will be a triumph.

Oct

4

Open Question About the Federal Reserve, from Vince Fulco

October 4, 2010 | Leave a Comment

What is the use of this statement which shows up in every fed speech:

"As always, the views I express are my own and do not represent those of the FOMC or the Federal Reserve System."

Especially when delivered by the most senior people in the org. Is it a

1) legal requirement

2) a 'wink, wink, nod, nod' or a

3) explicit back door out should policy not create its intended reaction in capital markets? it would be a wonderful thing if specs were given a few 'mulligans' every month…

Oct

4

Market Order, from Duncan Coker

October 4, 2010 | 3 Comments

It would be interesting to know which broker and clearing house accepted an order to sell 75,000 emini sp in apparently some sort of staged (GMTFO) market order that lead to the 5/6 event. 10% slippage I guess was acceptable, and had it been in just one stock no one would have noticed, but to move a whole market is different. The order only represented 3% of the daily volume. I wonder had it been placed closer to the more liquid open would it have had the same affect. Or did someone come back from lunch, see the market down 1% or so on a $10b fund, and have a change or heart. I don't think the HFT boys made on this, many smaller players margined out at the lows, brokers made their commission, customer filled his order, but hard to find much of a conspiracy other than a sloppy trade and a sloppy execution.

Vince Fulco writes:

The official line was it was a staged order supposed to make prints along with ~9% of the volume. Either we have extremely sophisticated HFT sniffers in our midst in ES or someone has a fat mouth. Once WR's actions were known, it was just a matter of other parties getting ahead thereby turning it into a 1987 portfolio insurance like scenario, the lower it goes the faster WR needed to sell.

Oct

3

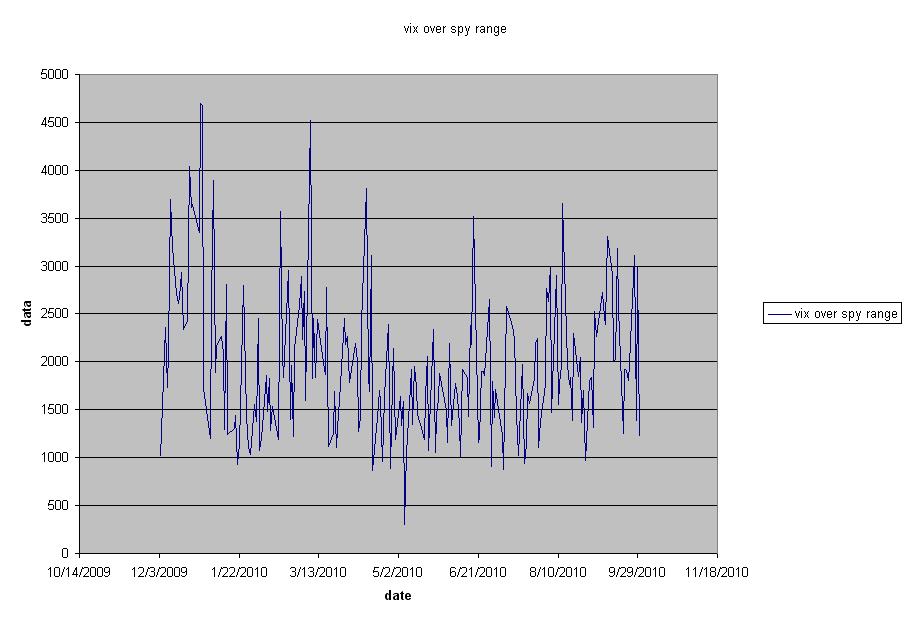

Flashing, from Kim Zussman

October 3, 2010 | 1 Comment

The attached plots the ratio of VIX (daily close) to SPY daily range, defined as (H-L)/{(H+L)/2}.

There is an obvious down-spike which occurred on 5/6/10 - now known as flash crash day.

Deleting that day and comparing VIX/SPYRANGE for the 102 days prior and before flashcrash:

Two-sample T for vix/range vs vix/range pre

SE

N Mean StDev Mean

vix/range 102 1867 615 61 T=-2.03

vix/range pre 102 2081 870 86

>> VIX/SPYRANGE is significantly lower since flashcrash. Interestingly both VIX and SPYRANGE are lower since flashcrash:

Two-sample T for vix vs vix pre

N Mean StDev SE Mean

vix 102 26.95 4.93 0.49 T=12.57

vix pre 102 19.83 2.91 0.29

Two-sample T for SPY rge vs SPY rge pre

N Mean StDev SE Mean

SPY rge 102 0.01639 0.00715 0.00071 T=5.9

SPY rge pre 102 0.01126 0.00512 0.00051

Oct

3

Models of Host-Parasite Coevolution, from Victor Niederhoffer

October 3, 2010 | 1 Comment

The mutual aggression model.

The mutual aggression model.

Host(h) and parasite(p) are taking part in an evolution arms race. The prudent parasite model. Selection in the p is always for characteristics that limit the damage done to the host. A de-escalating arms race (rabbits and myxomitosis in austral) incipient mutualism co-evolution is actively cooperative with both evoluting attributes so as to promote the continued presence of the other. A p that kills its host before it can transmit itself to other hosts doesn't get any genes into the next generation. The costs and benefits of a particular strategy determine the type of interaction that will occur. (From lecture 17 co-evolution and host parasite interactions): "it is important to contemplate an entangled bank clothed with many plants of many kinds, with birds singing on the bushes, with various insects flitting about, and with worms crawling through the damp earth, and to reflect that these elaborately constructed forms, so different from each other, and dependent on each other in so complex a manner, have all been produced by the laws acting upon us." Darwin, 1859. Okay, my query is how do the sponsor, the palindrome, the sage, the flexions–indeed the whole ball of Was– fit into this structure, and what predictivity can be drawn from it?

Gary Rogan writes:

The prediction would be that they will stop the nonsense before they let the economy disintegrate into complete chaos. However, there is a difference between genetic evolution and a single case. The evolution rolls the dice millions of times and the parasites that procreate are tautologically the ones that make it into the nth generation. Each particular parasite doesn't "know" whether it's killing the host. And with the flexionic complex we have just one roll of the dice so the results seem hard predict. They are supposedly sentient beings so that can be substituted for evolution, but what if they all individually have totally incorrect beliefs? What if they really don't care about killing the host? What if some of them are so close to the end of their lives that that's not even a consideration? What if some of them only care about the pinnacle of political power for however long they have as the most important concern? What if they have enough assets outside the system so that they don't have to worry? What if they don't have complete freedom to act anyway?

Overall, I don't believe they are actions can be analyzed as if they will preserve the system when push comes to shove. I can't even answer the question whether Ben Bernanke has any idea about what he is doing, and if so to what degree. I don't know what his ultimate goal is nor whether he can be self-critical to any degree. I hope others are able to make predictions.

Kim Zussman writes:

Another hypothesis is that government actions in the wake of the crisis reflects human nature with respect to pain. It is normal to avoid pain, and if given a choice between extreme pain of short duration and moderate pain which lasts a long time, many would choose the latter - even if "total pain" (something like level of discomfort * time) is greater.

The analogy may extend to the use of multiple drugs to lower immediate pain; it is hard to know how they will interact, and what unintended long term effects may develop, including addiction or death. Inexperienced doctors are sometimes overconfident in their ability to manage disease, but with time learn to carefully observe signs of normal healing, reassure the patient, and let the powerful mechanisms of natural repair work on their own.

Marion Dreyfus writes:

Speaking for someone who has this past fortnight endured pretty sever immediate pain, which has subsided into a moderate constant ache–I would much rather endure the latter, over a longer period, than the former. I trust nature will expunge the dull ache and pain I have now, eventually.

Oct

3

Protecting Yourself and Your Children, from Victor Niederhoffer

October 3, 2010 | 9 Comments

One of my daughters just got asked by a man to help her carry and buy groceries at a supermarket, and he had a young girl with him in tow or some such. The attempted crime didn't get carried out according to the daughter because "she didn't have enough money or she wanted to go into the grocery store" or some such. I recounted the story of Ted Bundy to her whose Volkswagen that he had lured a hundred college girls he killed into was on display. She asked me what the moral of the story was, and I said, "never trust a man who wants you to go with him to a private place no matter how needy or how much in authority he is." She said "you mean, never trust a policeman or fireman?" (one of the lures that Bundy and many others use and I said something like "yes". I don't think I gave her a good moral for the story. Could you help me say it better?

One of my daughters just got asked by a man to help her carry and buy groceries at a supermarket, and he had a young girl with him in tow or some such. The attempted crime didn't get carried out according to the daughter because "she didn't have enough money or she wanted to go into the grocery store" or some such. I recounted the story of Ted Bundy to her whose Volkswagen that he had lured a hundred college girls he killed into was on display. She asked me what the moral of the story was, and I said, "never trust a man who wants you to go with him to a private place no matter how needy or how much in authority he is." She said "you mean, never trust a policeman or fireman?" (one of the lures that Bundy and many others use and I said something like "yes". I don't think I gave her a good moral for the story. Could you help me say it better?

George Parkanyi writes:

Things aren't always what they seem, and it only takes once to make a fatal mistake. The most successful lurers/killers are the ones that are charming, or blend in with regular jobs/lives, so you can't make assumptions about how a person looks and talks.

Any valid person in authority knows they will run afoul of the law if they insist on being alone with a woman or child (or man)– especially on the strength of that authority. There are usually strict protocols in place (we have them in Scouts– never an adult alone with a child other then their own at any) to prevent potential abuse and also because of the potential liability issues. Call them on it. If someone asks your daughter to go alone with them for any reason– she should by default (politely but firmly) refuse unless someone else can go along as well, preferably another person in authority (a second officer, etc.), or someone she already knows and trusts (say a friend). Though even two or more going off somewhere with a strange person can still be very risky (they could have a weapon or accomplices)– best to avoid any such situation.

Also important to avoid situations/places where there is the risk that if accosted, no one else is around to help.

She should also never volunteer information as to where she lives (especially not take anyone there like the grocery guy), or give out any phone or email numbers. A second wallet with some cash and expired credit cards (with different numbers than the current ones) could also be a useful decoy for getting rid of someone accosting for money (say a drug addict).

Russ Sears writes: