Sep

8

The Blank Swan, from Nick White

September 8, 2010 | 1 Comment

The book The Blank Swan: The End of Probability contains some fascinating abstractions. It was very thought provoking and some good non-linear ways of thinking within. I liked it, although note that it has a continental philosophical flavor which may not be everyone's particular brand of vodka.

Sep

8

The Evils of Speculation, from Jeff Watson

September 8, 2010 | Leave a Comment

Here's an article describing the evils of speculation.

Sep

8

Risk and Reward, from Duncan Coker

September 8, 2010 | Leave a Comment

A small example of risk and reward played out this morning. I live near the ocean and woke near sunrise to surf. There was a gentle rain but not a problem. As I get to the water I look out to glassy waves and a light rain, but far out on the horizon is a storm, which will probably not reach here, but a storm none the less. Then, there was a large lightening bolt that lit up the sky to the horizon and thunder. Do I surf or head home? The getting up early, driving here, getting ready, are all sunk costs, and irrelevant. I do a quick analysis of the risk/reward, but have no real data to back it up. What are the odds of being struck by lightening in the water within 10 miles of a storm? I guess, probably over 1 in a million. Does this increase with more time in the water?, My estimation is yes. Is it dark and intimidating looking? Yes, but probably irrelevant. So I decide to risk it. I catch just a few waves then head in after maybe 30 minutes. Was it just a bit more exhilarating because of the pending storm then just a normal day surfing. I will admit it probably was.

A small example of risk and reward played out this morning. I live near the ocean and woke near sunrise to surf. There was a gentle rain but not a problem. As I get to the water I look out to glassy waves and a light rain, but far out on the horizon is a storm, which will probably not reach here, but a storm none the less. Then, there was a large lightening bolt that lit up the sky to the horizon and thunder. Do I surf or head home? The getting up early, driving here, getting ready, are all sunk costs, and irrelevant. I do a quick analysis of the risk/reward, but have no real data to back it up. What are the odds of being struck by lightening in the water within 10 miles of a storm? I guess, probably over 1 in a million. Does this increase with more time in the water?, My estimation is yes. Is it dark and intimidating looking? Yes, but probably irrelevant. So I decide to risk it. I catch just a few waves then head in after maybe 30 minutes. Was it just a bit more exhilarating because of the pending storm then just a normal day surfing. I will admit it probably was.

Stefan Jovanovich comments:

According to the wife of his old colleague Croker, the Duke of Wellington had his own discipline of risk-opportunity analysis. "All the business of war ", he told Mrs. Croker, "and indeed all the business of life is to endeavor to find out what you do not know from what you do." Wellington's phrase for it was elegantly simple: "guessing what was at the other side of the hill". (Arthur Wellesley's genius was to use terrain to spare his troops from the murder of the French cannon; he had his troops lie down during bombardments on the reverse slope of hills, where the spotters could not see them. This "cowardly" tactic was ridiculed by Napoleon - himself a gunner, but it was soon copied by the more intelligent French generals. That is the further implication of the Duke's maxim: your wise opponents will steal your best ideas.)

Ralph Vince comments:

Duncan,

What you have hit upon is the peephole to an entire discipline I call "Risk-Opportunity Analysis."

It explains, say, why we will get onto an airplane even though there is a (very small) probability that it will kill us. It explains, mathematically, why we do such things, and shows the mathematical reasoning for such. It can be extended then to trading, how much to risk, etc.

The conventional notions of assessing risks do NOT address this, and, in my opinion, as proved through the tenets of Risk-Opportunity analysis, are just plain wrong.

Incidentally, and forgive my plug here, but if anyone is interested in this, I am having a 2 day course in Tampa and in Tokyo in the next two months, and you can learn more at ralphvince.com

Pitt T. Maner III writes:

Would one change actions if more information or warning was available? How does real time information play in and can one truly interprit it properly and realize the statistical significance. 1:1 million odds can change when the strikes per minute count starts to climb. These alarms can be pretty unnerving.

Normally in the health and safety field if one sees a strike then you wait about 30-40 minutes and continue work if no other strikes are seen in that time interval— its a real rough rule of thumb and hardly perfect. Some go with a 6 mile radius for the detectors. Lightning risks are considered higher if they go within that radius.

For the alert-based systems though there are a lot of factors to think about.

By the way, that Tampa area is considered the "Lightning capital of the world"

I have heard of projects being shut down over there when lightning was detected by multiple detectors within a 20 mile area because the storms can move so quickly and/or the bolts generated can cover that distance too. So it can be difficult to work outside in Florida in the summer when following a strict lightning policy.

But in South Florida we get these too— out of clear sky.

Rocky Humbert writes:

There is a huge corpus of literature that shows people's instinctive assessment of risk and reward often have little to do with the HISTORICAL probabilities. Charlie Munger gave a long-winded speech at Harvard in 1995 on the "Psychology of Human Misjudgment." And as Ralph knows, "Risk-Opportunity Analysis" is not just about trading. It encompasses everything from physical System Fault Tolerance/Reliability (my dissertation topic) to classical economic utility theory to government/regulatory policy. And don't forget Pascal's Wager either!

Most people live (and die) in the middle of the curve. And the rest live (and die) in the tails. I'd argue that the wise man should try to make decisions which maximize his eternal happiness, and ignore the statisticians and meteorologists…or as Ed Seykota supposed said "Everyone gets what they want out of the markets."

Ralph Vince responds:

Pitt,

Yes, with new information, you have a new starting point from which things can change with given probabilities. The things that might happen, and their probabilities may be the same, but you have a new frame of reference, a new starting point. Think of a horse race, where you can change your bet at the first turn.

Rocky,

Very true, and that corpus is very interesting for a host of various reasons.Usually, we find, there is an often not-so-obvious logic to people's choices even though they appear inconsistent with historical probabilities.

But what I am alluding to — the inescapable conclusions I have found myself in — there is a lot more to it than that, and it;s a big can to open up here. In retrospect, it's all very obvious, and I can look at it and say to myself, "Yes, of course, this is obvious to me now."But it isn't obvious in the main, and frankly, from the polling of people I have been doing, not obvoius to anyone at all, which is the MOST peculiar thing about all of this.

Kim Zussman adds:

As is often the case, some answers can be evaluating using limiting cases. For example, you will never die in a bicycle accident if you never ride a bicycle (approximately).

As health care provider, I note frequently patients express regrets about having done something (or not doing something). The nature of regret seems to include a miscalculation of what consequences will actually feel like were they to occur. ie, the vague consciousness that you might crash your bike feels different than thoughts about the future while traction is decompressing your spinal cord.

Part of the intellectual maturation process is the effort to improve estimation of the experience of untoward consequences.

Jim Sogi replies:

Duncan, I've surfed in gnarly thunder lightning storms and wondered the same. The surf tends to be good and uncrowded as the storm cold front pushes, and lifts the wind towards the sea making the winds offshore for a while which is good for shaping the waves. In addition, the storm front may be pushing a wind wave front. What I've since found out is that the lightning can travel over the surface of the water until it finds something grounded. Not good. I've read about mountaineers stuck on the mountain during a thunderstorm. They describe some weird effects where their tools turn blue and their hair stands on end. The lighting can travel over ungrounded surfaces looking for ground. I think in the water if there was a nearby hit, I'd hold my breath and go underwater and allow the bolt to go above me. Also, I would NOT sit the furthest out to sea. In general, if the storm is isolated, the risk reward would be good. I try to take that approach trading as well. Similar but different analysis for sharks. I'll post about that later.

There is usually a time window. Before Hurricane Iwa hit here in 82, just before the storm hit, there were 20 foot waves, with offshore winds early that morning. Only a few spot were able to hold the swell. There were only 3 guys out. At about 10 am the wind turned and things got ugly. We hunkered down but were happy to have taken the risk and rode epic waves I still talk about to this day.

Sep

8

Elephants, Ants and Trees, shared by Pitt T Maner III

September 8, 2010 | Leave a Comment

A fascinating article on how ants protect their trees in the savanna from elephants:

A fascinating article on how ants protect their trees in the savanna from elephants:

"It really is a David and Goliath story, where these little ants are up against these huge herbivores, protecting trees and having a major impact on the ecosystems in which they live," Palmer said. "Swarming groups of ants that weigh about 5 milligrams each can and do protect trees from animals that are about a billion times more massive."

Sep

8

Horse Whisperer Contest Submission, from Douglas Dimick

September 8, 2010 | Leave a Comment

Hi V,

Hi V,

Here is submission for Whisperer Contest.

Thank you.

dr

The Beholder, Neither Beauty nor Beast

Jackson Hole is named after Davey Jackson (1788-1873), a mountain man who trapped the area for beaver.

Having helped my father trap woodchucks at our farm as well as coming across trappers and traps during deer hunting in Maine, the chair's contest (with its market analogies so implied) is not without circumstantial if not direct correlation(s). A trap itself may be considered analogous to "boxed" (or closed loop) quantification that defines points of convergence and divergence. Moreover, animal tracks are not unlike price action footprints relative to time intervals and price patterning.

In the linked article, the hole of Jackson Hole is aptly named by those mountain men who had to descend into that valley from the North and East along steep slopes as if entering a hole. Again, relative to points of consolidation or tiers for positioning or hedging, such lows symbolize graphical referencing, wherein rivers and streams provide habitat for life generating trends and channels.

Aside: Fed Chair B.B. is listed a visitor of Jackson. After his family moved to Dillon, South Carolina, he waited on tables at "South of The Boarder" before college. During seasonal migration to and fro Maine and the Palm Beaches, this oddity was a favorite overnight of mine with dad.

The dilemma, I surmise, though, with our suggesting the best use of whispering is one of perceived symbiosis in language and environment: to wit…A horse whisperer is a horse trainer who adopts a sympathetic view of the motives, needs, and desires of the horse, based on natural horsemanship and modern equine psychology. Growing up with horses among other farm animals and having dabbed at training here and there, I came to model my understanding on the work of Monty Roberts. He and his wife Pat (my mom was also named Pat and maiden name, as my middle name, is Roberts) have adopted 47 children in addition to their own 3 kids. You may see his work here. Registered as his term for "hooking on", the phrase "Join~Up", in which a trainer negotiates with an untamed horse to form a voluntary relationship. This approach is contra-indicative to industry traditions of 'breaking" a horse, whereby physical subdual is achieved by often violent confrontation or interaction.The point here being is that a horse whisperer helps horses with people problems – sometimes, as a result, helping people with themselves. One so connects to understand with an object oriented approach, such as to help a rider and mount join-up, as portrayed in Redford's movie …

Accordingly, be it with horses or markets, one, as a whisperer with a function as so implied by Victor, must first understand that language being transmitted. This factor is elemental for issue identification and definition if not quantification. Is there such a language of the markets? For instance, when a younger horse lowers his or her head to the older mare of the herd, it may be a sign of contrition or submission. Licking of the lips may be a sign of nervousness, fear, or seeking forgiveness. Are there similar signs generally analogous so occurring within price action?

Then there are the environmental distinctions. A horse is a living thing, natural, not artificial as a human construct. Markets are artificial; the one common singularity of such may be that each operates as an electronic exchange. However, the Theory of Quantitative Relativity indicates that the energy of such systematics is neither invariant (contra a horse's need to eat) nor of a singularity (contra a horse's time of birth or death). Therefore, where do we find a comparable numeric hierarchy in horse parlance relativity to market action?If you are asking yourself whether I penned this prior query in all seriousness or was attempting instead to be funny, well… yes and yes. When keying out the question, I was serious. Upon punctuation of the sentence, the analogy seemed humorous.

Nevertheless, the contest challenge is to identify the best use of such listeners of markets. Given that markets lack both a uniform language (albeit money) and decentralized, often fractured environments, whispers here appear to be more of use to consoling or commiserating with the rider (or trader, investor, speculator, etc.) than training (or taming) the beast.

An esoteric query? Perhaps but one which those so concerned or who monitor such cocktail banter might consider to be weighty. Even if de minimis, though, it makes for worthy digression.

P.S G and V: you ain't gonna break them horses who'd done left the barn a la post repeal of Glass-Steagall unless we restring that ole fence line.

Sep

8

Why Price is King, from Rudolf Hauser

September 8, 2010 | Leave a Comment

This article about how the current behavior of the global financial system cannot be explained by "normal" models of economics or finance is an example of fallacy of composition in that it assumes what would be true for an individual is true for the economy as a whole. In this case it is not. GDP is a measure of what an economy produces in the course of a year. It is defined on a gross basis in that it does not account for depreciation of the existing asset base, but one can also look at it on a net of depreciation basis. Aggregate demand can exceed production to the extent that we import more than we export. But that is not what this author of the article was talking about. Each entity that produces either keeps what it produces as inventory or sells it. The resulting purchasing power can now be distributed to pay its employees, bondholders and shareholders or invested back in the entity in the form of investments in plant, equipment, etc. Those who were paid can then in turn can either consume, invest in their own entities, hoard currency, purchase existing or new physical assets or save using financial markets . Amounts saved as either debt or equity then provide the means for other entities to consume, purchase existing assets, make investments. It also can provide governments the financial means to engage in purchases or transfer payments. The recipients of transfer payments can then, consume, etc. Purchase of existing assets just exchanges assets some hold for purchasing power with which to purchase consumer goods, etc. or save via financial instruments (including equity). It switches ownership of goods such as housing but does not increase aggregate demand that allows for increased consumption and investment beyond what is produced (GDP) plus net imports. Looked at from a different perspective, the sale and purchase of an existing asset such as a house does not create any jobs beyond that of the middle men (realtors, etc.) whose contribution is included as part of GDP.

This is not to say that the distribution of ability to buy in excess of amounts earned is without any macro implications. In an economy with specialization we have to be able to produce something that someone else is willing to buy. Investments are made in order to be able to increase future production of consumer goods. Those investments include physical plant and equipment but also R&D, education and training (development of human capital), etc. For the most part in our modern economy the ability to put sheer labor to use it must be combined with capital that someone was willing and able to provide. When people are not able to find something to which they can apply their productive talents that someone else will buy they do not produce or consume except to the extent that someone or some entity is willing to help them out. When producers miscalculate where the future demand will be at prices that exceed costs of production (including necessary return on capital) certain physical capital and human capital will become wasted and those who invested in them will sustain losses. It also means that labor has to be redeployed. That may mean accepting lower payments as one's acquired skills are no longer valued or necessitate more human capital investment to be able to qualify for available jobs. Note that the return on human capital is dependent on the amount of time left in a working career and the premium over what their labor is worth without having that human capital. This makes it more difficult to redeploy older workers. When consumers go on a spending spree based on credit provided by savers they create more demand in industries that produce what they wish to consume. When they have to cut back capital and labor in those sectors will face lower demand and have to be reduced. When investors become more risk adverse because of bad experiences, etc. what happens is that some sectors will face higher risk premiums which may exceed the rates of return they can expect to earn or not be able to obtain capital at all. Those risk adverse investors will just drive the interest rate on low risk assets to very low levels. That can result in an economy in which government transfer payments increase resulting in higher taxes which will work to discourage even more investment and provide a place for risk adverse investors to place they savings in the form of more government debt issuance. That translates into a lower level of GDP. For an economy to maximize its prosperity one needs efficient capital markets that can move capital to where it is needed most, entrepreneurs and managers who correctly anticipate where profitable demand will be, the development of better technology and methods of production and distribution through research, trial and error, etc. and the willingness to accept innovation, flexibility in moving the means of production to where it can be used most efficiently, trust developed through ethics and culture reinforced by adequate legal systems and policing of crime, savers willing to take an appropriate degree of risk (that is prudent risk to allow innovation and new enterprise but without going into pure speculation), etc. It also requires providing the needed amount of transaction and near transaction means (i.e., money and near money) without causing a change in the overall price level (i.e., inflation or deflation).

Tyler McClellan comments:

What a magisterial post, such deep but sensible knowledge.

I think you might have gone slightly further however and elaborated how much of our economic activity does in point of fact depend on expectations of the future, the Keynesian convention of certainty, when none such exists.

I think your lay explanation of how expectations of the future affect both the demand to save and the demand to invest is very good. Hence the complex interest rate outcome. Much better than my own attempts at driving at this fundamental problem.

Sep

7

Paul Hogan vs. The Australian T.. Office, from Nick White

September 7, 2010 | Leave a Comment

Essential viewing for everyone who loves individualism and having a good crack at the Service for taking (in this case, literally) 100% of lifetime earnings.

Essential viewing for everyone who loves individualism and having a good crack at the Service for taking (in this case, literally) 100% of lifetime earnings.

part 1 (esp from 5:01 to 6:15)

part 2

This is very different from how all of you will remember him from his acting exploits of the past. Actually, this is probably as close to true Australian spirit as you'll ever see….far more than the manufactured stuff he pumped out in those awful movies.

.

.

Sep

7

Monte Walsh, from Victor Niederhoffer

September 7, 2010 | 1 Comment

The chapter "Payment in Full" in Monte Walsh which I just read again is one of the most beautiful chapters I have ever read. It records the adventures of an accountant from the consolidated cattle company confronting Hat and Sonny about a 1200 payment that was demanded by the railroad company for the damages inflicted by the cowboys when the train men intentionally spooked the cattle they had rounded up with great difficulty the previous 5 days. If it doesn't make you cry out for joy the way Stubby Pringle and Miley Bennett story did, I'll "eat my hat lying there begging someone to put a bullet through it" as Cal said to the accountant at his desk. I can imagine a similar beginning of the meeting between the inside trading French bank and its DAX trader…"What's this. You're long 5 billion of DAX again?" "Certainly, I've been long that much half of the time this year, and that's why we're up 500 for the year."… etc.

The chapter "Payment in Full" in Monte Walsh which I just read again is one of the most beautiful chapters I have ever read. It records the adventures of an accountant from the consolidated cattle company confronting Hat and Sonny about a 1200 payment that was demanded by the railroad company for the damages inflicted by the cowboys when the train men intentionally spooked the cattle they had rounded up with great difficulty the previous 5 days. If it doesn't make you cry out for joy the way Stubby Pringle and Miley Bennett story did, I'll "eat my hat lying there begging someone to put a bullet through it" as Cal said to the accountant at his desk. I can imagine a similar beginning of the meeting between the inside trading French bank and its DAX trader…"What's this. You're long 5 billion of DAX again?" "Certainly, I've been long that much half of the time this year, and that's why we're up 500 for the year."… etc.

Sep

7

I’ll Buy Him A Ticket, from Victor Niederhoffer

September 7, 2010 | 1 Comment

Before the match between Gilles Simon and Nadal, where Simon wanted to lose because that way he could see his newborn kid a day earlier, Nadal said something funny. "I'll buy him a ticket if he leaves before the match" (a default win) he said. It reminds me of the many times I've been at the palindrome's house during the end of the summer like today, where all the attendees at his party were long or short something and I was the only one the other way. I always wanted to picket the party or some such so the trillions of birthday boys and neighbors and school comrades there couldn't go to their wires the next day to go against me one more day, especially when romance had been in the air as it always was.

Before the match between Gilles Simon and Nadal, where Simon wanted to lose because that way he could see his newborn kid a day earlier, Nadal said something funny. "I'll buy him a ticket if he leaves before the match" (a default win) he said. It reminds me of the many times I've been at the palindrome's house during the end of the summer like today, where all the attendees at his party were long or short something and I was the only one the other way. I always wanted to picket the party or some such so the trillions of birthday boys and neighbors and school comrades there couldn't go to their wires the next day to go against me one more day, especially when romance had been in the air as it always was.

Sep

7

A Libertarian Question, from Jeff Watson

September 7, 2010 | 1 Comment

With the view that there is a strong Libertarian streak across this web site, I pose these questions:

With the view that there is a strong Libertarian streak across this web site, I pose these questions:

Should investment professionals, brokers, etc be registered and regulated by the government?

Should the government be able todetermine who should or should not be in the investment business or should the free market determine this?

Is it the government's duty to attempt to preemptively protect investors from potential fraud?

Should the government have strong laws against fraud yet have few laws determining who should be in the investment business?

A discussion delving into both sides of this would be very interesting.

Stefan Jovanovich replies:

Jeff's question deserves a proper answer. Common law fraud was the strongest possible law, and it did not involve the government (as opposed to the civil court) at all. Under common law, three elements were required to prove fraud: (1) a material false statement made with an intent to deceive (scienter), (2) a victim's reliance on the statement and (3) damages. This was the legal/regulatory world that the authors of the American Constitution were familiar with. They had all - both civilians and lawyers– read Black's definition of fraud: "All multifarious means which human ingenuity can devise, and which are resorted to by one individual to get an advantage over another by false suggestions or suppression of the truth. It includes all surprises, tricks, cunning or dissembling, and any unfair way which another is cheated."

Having such a broad and general definition might seem an invitation for perpetual litigation; but it had, in fact, the opposite effect since both parties- plaintiff and defendant– had at risk the cost of their own attorneys AND those of the opposing party, if that party won the case. Nick may have a more benign view of regulation precisely because Australia follows the old American and current British tradition of requiring the loser to pay the winner's costs and attorneys fees. But, I doubt that, even in the Commonwealth countries, the sovereign has surrendered its immunity from having to pay the other party's costs and fees when the government is the loser. That immunity is really at the heart of Scott's and other's anger. The government is never required to pay its share of the burden of the regulatory system. The government can, with ease, tyrannize the citizens by bringing a criminal or regulatory action; the citizens may successfully defend themselves but they are ruined by the expense of maintaining their innocence. Under our system of sovereign immunities (the last holdover from the theocratic idea that the government is God's instrument) being the government means never having to pay any tithes for your civil servants' mistakes or, heaven forbid, requiring the civil servants themselves to have any personal stake in the outcome of their decisions.

Easan Katir writes:

There was the famous case in old England where a father on his deathbed bequeathed his interest in a brewery equally to his six daughters, thinking he was giving them a wonderful gift.

After his death, it turned out the partners in the brewery had burdened the enterprise with mountains of debt. The creditors exercised their legal right to collect from all partners. This was before the corporate shield, so all six families of the daughters were bankrupted.

Some gift.

Gibbons Burke writes:

Small businesses, farms, individual traders and some professionals still operate in a mostly free market where the rules of accountability and the mechanism of creative destruction still obtain.

Big corporations are just as much the enemy of a free market as big gummint. I am starting to think that the world would be a better place if corporations had never been allowed to exist. The idea that the owners of an enterprise should not be held responsible for it's debts or its crimes, beyond their investment in the enterprise, seems to be an immoral one with bad consequences.

Salomon Brothers was a better organization than Salomon, Inc., as Michael Lewis has observed in many of his writings. When the partners were absolved of the risk of their investment schemes, the tenor of the schemes turned malignant and metastasized. Same idea applies to ….

Sep

7

Thoughts on Prosperity, from Stefan Jovanovich

September 7, 2010 | 2 Comments

The post-World War II prosperity of the United States had only one source and cause: the private savings of individual Americans. For nearly half a decade– from the beginning of 1942 to mid-1946 Americans, both in and out of uniform, saved effectively all of their disposable incomes. They had nothing to spend the money on since everything was rationed. After rationing and price controls were lifted (much to the dismay of the Nobelistas of the time who thought it should be continued), those savings were spent– voluntarily– by individuals; and businesses responded by extending– for the first time– real credit to ordinary Americans. It was the stimulus of that private expenditure, not the government's "investment" in bombs, that produced the revival of the American economy. By contrast, Britain chose a much different path. At the same time the Republicans were passing Taft-Hartley, Britain was continuing rationing and price controls. Under Clement Attlee's Labor government, with the nationalization of previously privately-owned industries (medicine, coal), government control over the economy was expanded and extended.

The post-World War II prosperity of the United States had only one source and cause: the private savings of individual Americans. For nearly half a decade– from the beginning of 1942 to mid-1946 Americans, both in and out of uniform, saved effectively all of their disposable incomes. They had nothing to spend the money on since everything was rationed. After rationing and price controls were lifted (much to the dismay of the Nobelistas of the time who thought it should be continued), those savings were spent– voluntarily– by individuals; and businesses responded by extending– for the first time– real credit to ordinary Americans. It was the stimulus of that private expenditure, not the government's "investment" in bombs, that produced the revival of the American economy. By contrast, Britain chose a much different path. At the same time the Republicans were passing Taft-Hartley, Britain was continuing rationing and price controls. Under Clement Attlee's Labor government, with the nationalization of previously privately-owned industries (medicine, coal), government control over the economy was expanded and extended.

Sep

7

Cars of Today, from Jim Lackey

September 7, 2010 | Leave a Comment

Safety caused a change in driver behavior. My 1st vehicle was a full size Chevy van as my dad knew I would wreck or race any car. My 3rd car was a 67 Camaro and was so dangerous I had to drive it slow.

Safety caused a change in driver behavior. My 1st vehicle was a full size Chevy van as my dad knew I would wreck or race any car. My 3rd car was a 67 Camaro and was so dangerous I had to drive it slow.

The cars of today are so safe we do not realize how fast we are traveling. Turn off the tunes, books on tape, and roll down all the windows. The cars are so safe and quiet today, stick your head out the window at 45 mph, or look down at 70mph and wonder what it would feel like to hit the street at that speed falling off a motorcycle. It's fast. But today the cruise set at 74MPH ticket free interstate travel feels like we are barley crawling along. I must do 88MPH to get me to pay attention to detail vs. falling asleep on a long drive.

I hate mandates but some of it sure worked for cars. I'd say Germany was the best place to drive. They have two deals we need to adopt. Much stricter driver training. Much stricter speeding laws fines for speeding or crashes and you're certain to stick to 100K's or 62 int he zone or lose a months Army pay. That and with lights that turn yellow before green– Get ready set GO instead of me honking my horn at your Ipod playing kids but to go on the green light.

2cnd thing Germany has is when it makes sense for me to got 100MPH. Yes it's safe if you're focused and do not have cup holders. I see roads here in the US that I can land a 737 Jet on them, no traffic 5 lanes and its posted 55mph. Stupid. 55 is for junk roads. MPH range needs to be 69-74. Post it up 70 MPH and 75 and over is 500 fine…if you can afford it cool, if not you pay.

Also please do away with drunk driving. Let's just make it a rule. Medicine or not– one beer, one drink– you can't drive. No more 2 beer rules designed to raise revenue for the courts. You drink you drive no more. Period.

Sep

5

A Theory: Dropping Mark-to-Market Saved the World, from George Parkanyi

September 5, 2010 | 6 Comments

The more I think about it, I don't believe credit and debt are likely to be our biggest issues in the next couple of decades. The credit crisis was really all about the valuation of illiquid assets, and the death-spiral of marking to market assets that stopped trading outright, because no-one knew what to mark them to, and therefore couldn't assess counter-party risk. It struck me early on in the crisis that trying to mark these "assets" to market was stupid. The most obvious solution was to take troubled debt, garbage or otherwise, and refinance it over longer maturities to gain some breathing room. And that's kind of what happened, and here we are today with LIBOR nicely back to normal. If things get really bad again, central banks will just lead re-financings like the Europeans did earlier this year - and keep interest rates low, because sizeable tranches of new money will likely have to be created from time to time.

The more I think about it, I don't believe credit and debt are likely to be our biggest issues in the next couple of decades. The credit crisis was really all about the valuation of illiquid assets, and the death-spiral of marking to market assets that stopped trading outright, because no-one knew what to mark them to, and therefore couldn't assess counter-party risk. It struck me early on in the crisis that trying to mark these "assets" to market was stupid. The most obvious solution was to take troubled debt, garbage or otherwise, and refinance it over longer maturities to gain some breathing room. And that's kind of what happened, and here we are today with LIBOR nicely back to normal. If things get really bad again, central banks will just lead re-financings like the Europeans did earlier this year - and keep interest rates low, because sizeable tranches of new money will likely have to be created from time to time.

Interest rates have to stay low now because governments are running large deficits and adding to their already big piles of debt, and can't really afford to pay much higher interest. The cost of credit appears to have shifted toward a subsidy regime much like agriculture, and could very well become as politicized. Credit needs to be cheap and affordable, and kept there as everyone - governments, business, and consumers - get used to paying so little for money. Because the U.S., Europe and Japan are all in the same boat (Japan saved us seats) and represent the currencies where most reserves are parked, I think we're going to see low interest rates for a long time - even if economic growth comes back, which it should as everyone continues to refinance longer-term debts to lower rates. They'll be able to keep rates low because there really won't be any other game in town currency-wise.

This is my assessment, and who knows if it really will play out that way, but if it does, I think the current financial system and major economies can remain intact for a long, long, time, deferring the day when debt really comes home to roost. I foresee a more robust form of what Japan has gone through in the last couple of decades. Not as much growth as before, a lot of bad debt in the attic that no-one wants to write down in a big hurry, but generally better economic performance than Japan in the aggregate. The analogy I would make is the stretched family that just keeps paying off one credit card with another indefinitely. I think this will be our macro fiscal situation for a while.

Most things in the world will still function, so commodity and equity markets should return to business as usual– they pretty-much have already. With such low interest rates, not sure what's going to go on in the bond markets. When confidence increases, a lot of that money may actually shift to equities and commodities for higher returns, and with that appetite, it might soon again be a good environment for IPO's to absorb some of that capital, and the innovation that goes with that. Industries that depend on, or prosper from low interest rates should do well. Real estate and utilities might boom. Deflationary pressures may still hover near, especially if consumers remain strapped for an extended period of time in the major economies.

Inflation? Don't see it here unless low rates set off another major boom. Future crises? Probably currency, in places like Russia and Brazil. Because other economies/currencies don't have the same low-interest luxury and will be more sensitive to inflation (interest rates in Brazil look to be about 11% these days), we may get some currency devaluations. War and geo-politics are always wild cards. Dollar, Euro and Yen could stay relatively strong from the influence of carry trades (borrowing cheaply in these currencies to get higher returns elsewhere).

Any thoughts out there on this and other scenarios?

Jeff Rollert writes:

I differ… the crisis began as a liquidity crisis, and has morphed into a problem of insufficient systematic equity. Low rates are a prayer that hopefully buys enough time for debt amortization to effect a re-equitization.

Problem is it assumes stable GDP here and abroad.

Ralph Vince writes:

The villains in the story are the quants– those whose maladroit ir math mispriced the CDOs and CMOs grotesquely– then ducked back into their dusky shadows.

Not a one of them has been called to account.

Sep

5

Pinball–the Game Tech Industry of Yesterday, from Ken Drees

September 5, 2010 | Leave a Comment

Well, it's the weekend and a time to consider an old game system that at its heyday was the tech bomb –the cutting edge gamer biz. Gottlieb, bally, Williams, Stern (the only real one left).

Well, it's the weekend and a time to consider an old game system that at its heyday was the tech bomb –the cutting edge gamer biz. Gottlieb, bally, Williams, Stern (the only real one left).

I have begun investigating and accumulating machines for my game room. My son and I have already started upgrading a nice bally Solid state machine from 1980–skateball. This machine highlighted the California vibe–skateboarding, skating, surfing and the beach, sun and fun–pre nike and just teasing the 3's company TV show vibe (California fun). What a time capsule and what a way to bond with your child–advance electronics via hands on work–its all there on the internet and all parts are available! You can buy old games on eBay and craigslist and through obscure game shops. One thing here –pinball tech guys are few and far between and very busy. There is a market that is buzzing and these games are getting rehabbed and being put into homes.

Kids today do not know pinball–its a social game –"way better than video, Dad–pinball is REAL". Get a pinball and your kid becomes wealthy in terms of game status! I read an interview from Stern who said that the majority of today's games go overseas or domestically into private homes. There is no more bowling alley, pizza shop, bar, or game room to put pinball games for the public–it's now underground. Kid's today are really interested in pinball if they can be introduced to it. But too bad that today's pins cost 5grand are super computerized and who can have them in a public place exposed to the public? Maybe there is a business idea here.

Stern (his son that runs the company now) said that pinball will always be a great game because its like baseball–you have a bat and you have to hit the ball or its a strike and you are out.—I thought that was great!

Ok —here are some great links

the pinball database. Thank God for these people.

Here is the skateball link.

And please read some awesome history from the late Harry Williams—the famous "williams" pinball maker.

I really never thought of pinball as a tech industry but it was and still is. I hope the list members can contribute here–my past was the early 80s gameroom the height of games when pinball went solid state from electro magnetic and video games came on the scene. My Dad was always asking me about what games were cool–atari etc. He was trying to get a handle on the tech–I was too young to realize what i was knee deep in. But I knew one thing–it was all good!

Sep

5

Wharton Energy Conference, from Will Weaver

September 5, 2010 | Leave a Comment

If anyone knows of energy companies that would like to display their products at the Wharton Energy Conference this year, please let me know. Stephanie Nieto, whom I brought to the Spec Party this year is hosting exhibiting companies.

If anyone knows of energy companies that would like to display their products at the Wharton Energy Conference this year, please let me know. Stephanie Nieto, whom I brought to the Spec Party this year is hosting exhibiting companies.

Pitt T. Maner III:

Will,

It was nice to meet you and Stephanie at the Spec Parties. I am hoping to maybe get up to Boston with my friend Martin Conroy to watch him compete in the Head of the Charles and hope to see you there too if you go.

In thinking of the Wharton conference:

As one of those long shot, nutty, literally " Don Quixote chasing windmills", sub-penny investments I have a few shares in Helix Wind, HXLW.OB. They have an interesting technology "if " they can get it patented and improve on it. http://www.fastcompany.com/1683897/let-the-great-wind-spin

CEO seems to be a skilled marketing type fellow but the stock imploded last year and you can probably tell the way it is setup if it has any viability or chance to survive. But Helix Wind is an eye catcher, "work of art" concept that brings a product with a small footprint, low noise, efficiency from wind in all directions, etc. and I have seen Target for instance in S. Florida show interest in small, vertical wind turbines (fitted into their signs) to run power to individual stores and save on their electric bills.

On another note, large, diesel-powered, portable generators for businesses and condos in S Florida became much more more prevalent after Hurricane Wilma hit several years ago. Once winds hit about 50 mph you can count on the power to go off here in West Palm Beach for days if not weeks in some cases.

With respect to Canada the stocks that used to interest me were CFK (drilling mud and supplies and tool expertise) and the driller Precision Drilling (PDS). Those are business areas that require a lot of expertise and experience and offer significant barriers to entry. But probably would tend to favor PTEN and the beaten up offshore drillers—DO, NE, RIG, etc. and good old SLB now as stocks to think about for slightly longer term given a potential rebound in energy and perhaps a return to more favorable regulatory environment. Definitely a boom /bust business cycle and one requiring much research.

Good luck with the conference.

Best regards,

Pitt

Sep

4

Wizardry, from Kim Zussman

September 4, 2010 | Leave a Comment

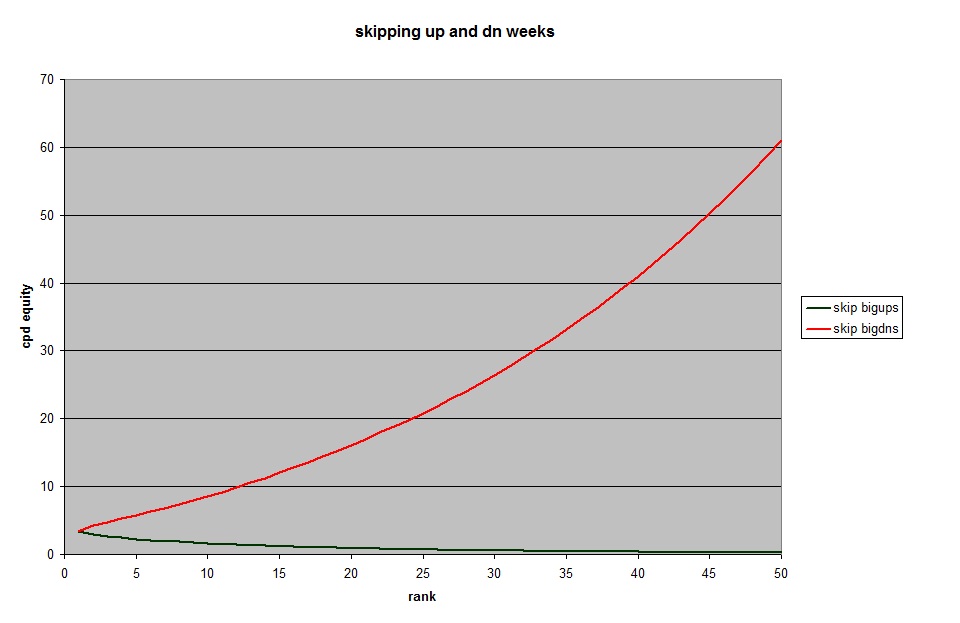

One often admires investors "without any down years" (months, weeks, nanoseconds, etc). Here is an update on compounded weekly SP500 return (SPY, with div), 1993-present - successively skipping down weeks starting with the largest drop through the 50th largest. (918 weeks total)

The attached chart shows the compounded return curve, which for the entire series is 3.415 (ie, an initial 10,000 compounded to 34,150). The red line shows compounded return altered by successively skipping big down weeks, which rapidly increases as down weeks are omitted.

Similarly skipping big up weeks reduces compounded return, but at a slower rate than it increases by skipping down weeks. This is shown in the following data, where compounded return doubles by missing the worst 6 weeks, but is cut in half by skipping the top 8 up-weeks.

skipping

bigups bigdns

3.42 3.42

3.01 4.26

2.71 4.74

2.45 5.28

2.28 5.78

2.12 6.30

1.98 6.83

1.85 7.40

1.73 8.00

1.62 8.58

1.53 9.20

1.43 9.86

1.36 10.54

Now where is that pointed hat?

Sep

4

Movie Rental Rules of Thumb, from Dan Grossman

September 4, 2010 | 7 Comments

Movie rental rules of thumb especially for one whose girlfriend has a more humanitarian, international sensibility:

Movie rental rules of thumb especially for one whose girlfriend has a more humanitarian, international sensibility:

1. Avoid movies about poor people in f**cked up countries.

2. Avoid movies relating to "the troubles" in Northern Ireland. (This is by and large a subcategory of 1 above, since Ireland much of that time was a f**ked up country.)

3. Most movies would be improved by the addition of scenes involving the machine-gunning of Nazis. (This includes movies like Julie and Julia, Sideways, and A River Runs Through It.)

Can specs offer other rules of thumb?

Disclosure as to where I'm coming from: The movies I'd rate highest over the last couple of years (at least the ones I can remember):

The Queen

History of Violence

No Country For Old Men

Lives of Others

Taking Chance

Victor Niederhoffer comments:

Explain to girlfriend that if they take from the rich and give to the poor, it's a taking based on singling out one group based on attributes that the majority does not like, and it is very dangerous when extended. Explain that it has to come at some one else's expense. Explain that when a game is played, it's unfair to take the chips from the winners after the game. Explain that if two people vote to take the third 's chips away, it's like a robber coming and taking it away. Explain that once you take it away from one group, after another, there won't be any one else to take it from, ( the Jews thing from the bishop again). Explain that people stop trying after they keep having to have it taken away. Explain that it's not theirs to give. That it's wrong to steal from others, even if there's a vote. Explain that when people approach each other from each according to their ability to each according to needs, they begin to hate each other always being afraid of what the other guy is wanting from you or you can get from him. Explain that there's no difference between taking from the rich and giving to the poor to buy votes and all this, and that this is the idee fixe of the party in power. Explain that buying votes by taking a small amount per capita from one group and giving to another, earmarks and logrolling is the same thing.

Explain to girlfriend that if they take from the rich and give to the poor, it's a taking based on singling out one group based on attributes that the majority does not like, and it is very dangerous when extended. Explain that it has to come at some one else's expense. Explain that when a game is played, it's unfair to take the chips from the winners after the game. Explain that if two people vote to take the third 's chips away, it's like a robber coming and taking it away. Explain that once you take it away from one group, after another, there won't be any one else to take it from, ( the Jews thing from the bishop again). Explain that people stop trying after they keep having to have it taken away. Explain that it's not theirs to give. That it's wrong to steal from others, even if there's a vote. Explain that when people approach each other from each according to their ability to each according to needs, they begin to hate each other always being afraid of what the other guy is wanting from you or you can get from him. Explain that there's no difference between taking from the rich and giving to the poor to buy votes and all this, and that this is the idee fixe of the party in power. Explain that buying votes by taking a small amount per capita from one group and giving to another, earmarks and logrolling is the same thing.

George Parkanyi writes:

Generally I agree with the points you make, but you need to define "rich", and how they got that way. If you are rich because of looting, subjugating/brutalizing, running people off their land, government subsidies, inside information/cheating, exploiting misery (in a way that perpetuates/worsens, not improves it), generally racketeering and so on (in business or politics) - no sympathy whatsoever. And if you are rich by benefiting from the commons - the environment, shared infrastructures such as roads/highways etc. then a fair contribution should be put toward the custodianship of that (fair being the same formula for rich or poor). But where someone acquires wealth by imagination, creativity, and effort within on a fairly accessible, level, playing field, then I agree wholeheartedly that forced re-distribution of wealth is wrong. As for inherited wealth, although that may appear to be a free ride, if someone bestows upon you the fruits of their work, ultimately it is their right to spend their wealth that way, so that also should fall under protection from external plunder.

T.K Marks writes:

At the early onset of a relationship, there's always a little dance that takes place. I call it the pas de deux period, the part of the performance wherein the two principals gingerly feel their respective ways around one another.

In one's youthful exuberance this situation invariably takes place against a backdrop of lots of saloons and even more beer.

However as one gets older and lest their elevated liver enzymes leaving them forever dancing with two left feet, they must summon up their inner-Balanchine and modify the mating choreography a bit.

As such, and with respect to film rentals, there is a cinematic litmus test of sorts that affords one a little window into exactly what they're about to get into.

Think of it as a diagnostic dating tool. Kind of like an MRI of the soul.

Simply explain to the lady that you're in the mood for a classic film and since the ultimate choice of the rental should should only fairly be a bilateral decision, how about if you choose the director, and she, the exact film.

She may very well be taken aback by your quick sense of interest in her input and tastes in art.

Then you tell her that the two directors you had in mind were Frank Capra and Ingmar Bergman, a blithe/bleak dichotomy if there ever were one.

If she bites on Bergman, you might as well just have snuck a peak into her medicine cabinet. That thing is probably going to choking with Paxil, Zoloft, or whatever the latest SSRI big pharma is pushing at the moment.

However, if she's reflexively goes for Capra, there's a better than even chance that the serotonin issue is off the table and you may have just walked into a Norman Rockwell painting.

Sep

4

The Employment Report, from Victor Niederhoffer

September 4, 2010 | 3 Comments

As one who believes only numbers important in the employment report is the rate, which was up from 9.5 to 9.6, because the numerator and denominator have the same faulty seasonal adjustments, I was not overly impressed with the report from a economic activity standpoint especially since I believe that the numbers are vetted heavily by the flexions, as witness the prior afternoonionic moves, and rabbi-ed by …

Kim Zussman adds:

Here is graphic of monthly unemployment rate, 1948-8/10 (seasonally adjusted, BLS data).

The '81 recession was worse in absolute terms, but the recent recessions rapid climb from 4.5% to 10% in 2 years is unprecedented in the series. It also appears that the rise to peak unemployment in recessions is generally much more rapid than the fall afterwards.

Sep

4

Fishing for Input from Jovanovich, from Charles Pennigton

September 4, 2010 | 2 Comments

I saw this written about Churchill:

I saw this written about Churchill:

When Churchill entered the inner Cabinet as First Lord in 1911, Britain was first nation on earth and ruler of the greatest empire since Rome. When he left in 1945, Britain was an island dependency of the United States:

"..he schemed constantly behind closed doors agitating for war at every opportunity.

"He was also a first rank opportunist. Supported nationalizing industries when he thought he might be able to run them. switched to Hayek when out-socialized on the left.

"Switched political parties numerous times.

"Lots of bravado about being tough when losing his empire and sending boys to their deaths, if that is an admirable trait.

"There wouldn't have been Nazi's in the first place if not for his (and others) role in Versailles. He lived for war. wanted war at every turn, and it cost Britain her empire."

Can Mr. Jovanovich give his opinion?

Stefan Jovanovich obliges:

Churchill's disastrous military mistakes as CIC– Gallipoli, Narvik, even Singapore– all had the same source: he was determined to avoid any repetitions of the "meat-grinder" of the Somme. Churchill's fascination with "wonder weapons" and "special executive" missions came from his hope that these alternatives to conventional warfare could offer an escape from the unavoidable truth about wars fought between opponents who will not cut and run.

The European continent has had a history of warfare that is unmatched by any place else on the globe. That is– in the end– probably the best explanation for how some soggy islands, river deltas, and dry mesas produced world empires; the inhabitants were constantly tinkering to build better weaponry.

To take that tradition of strife and then say, "Oh, an unfair (sic) peace treaty and a bad choice for gold-sterling exchange rates is the explanation for Hitler, Stalin and Mussolini" seems to me more than a bit of a stretch. If you are going to blame peace treaties for the continuation of the Western Way of War, you have to look to the treaties of the 1870s.

Sep

4

Good in the Minors, Bad in the Majors, from Victor Niederhoffer

September 4, 2010 | 1 Comment

An article in the WSJ reports that there are certain players, Ferrer, for example, who do very well in minor tournament events but never get to the quarter finals in a major. The opposite is Serena Williams who never wins a minor but always wins the majors. One wonders how the bulls and bears of the markets are at winning on the big ones. What are the big ones and little ones? The big change days and small change days? The beginnings and ends of weeks? The days of the big announcements like yesterday. Are there hot hands that get used up after winning the majors. Once again the field of sports gives one a thousand useful hypotheses to test.

An article in the WSJ reports that there are certain players, Ferrer, for example, who do very well in minor tournament events but never get to the quarter finals in a major. The opposite is Serena Williams who never wins a minor but always wins the majors. One wonders how the bulls and bears of the markets are at winning on the big ones. What are the big ones and little ones? The big change days and small change days? The beginnings and ends of weeks? The days of the big announcements like yesterday. Are there hot hands that get used up after winning the majors. Once again the field of sports gives one a thousand useful hypotheses to test.

George Parkanyi writes:

This particular example may have to do with the ability to handle pressure. Some traders might perform quite well and consistently trading a relatively smaller amount of capital, whereas a few may be able to trade successfully in much greater size because they can stay calm and still function at a high level under the pressure of drawdowns and reversals. So position size would definitely be a big/little differentiator.

This particular example may have to do with the ability to handle pressure. Some traders might perform quite well and consistently trading a relatively smaller amount of capital, whereas a few may be able to trade successfully in much greater size because they can stay calm and still function at a high level under the pressure of drawdowns and reversals. So position size would definitely be a big/little differentiator.

In sports, increased media scrutiny probably influences player performance. Another big/little differentiator could be the amount of external influences/distraction that might affect your decision-making. For example in a position trade, while, you're holding, you could be subjected to all sorts of external influences - economic news, personal life, someone's opinion. Let's call it noise. Will a big noise shake you out of your position? Will a series of little noises aggravate you out? Or can you hold/trade through it? Can you effectively differentiate between noise and something materially important?

Steve Ellison writes:

I once read a suggestion that golfers practice coming through under pressure by not allowing themselves to finish practice until they make 25 consecutive three-foot putts. The 24th and 25th putts simulate high-pressure situations as the golfer has to start all over if he misses.

In football, Joe Montana had an incredible knack for winning the big one. This trait was in evidence as early as his sophomore year at Notre Dame, when he came off the bench a few times and led comebacks from multi-touchdown deficits. Montana was probably an average athlete by NFL quarterback standards, certainly not as gifted as Dan Marino or John Elway. Yet, when he met these men in Super Bowls, Montana came away the winner.

As a counterexample, the San Francisco Giants had a pitcher who was notorious for coming apart under pressure. He was good enough to appear in the All-Star game, but gave up a grand slam in the game. I groaned when this pitcher was named as the starter for game 7 of the league championship series, knowing what would happen; sure enough, it did.

Sep

4

The Standardized Tests for 4 Year Olds, from Victor Niederhoffer

September 4, 2010 | 1 Comment

The process of socialization of school is crystallized in these tests. All the questions on the comprehension thing for 4 year olds are variants of "why is it good to share" "what can we do to keep the environment safe?" "why should we follow rules" "why do we need policemen" "why do we take turns" "why can't children stay at home alone" "why do we need to wear seat belts" "why should we recycle" "why do we say sorry" "Why do we need to wear helmets when riding bicycles" "why do children have to go to school" "why do we raise our hands" "why do we have to wait in lines" "why do we have addresses" "why should we read the news" "why do we have a president."

The process of socialization of school is crystallized in these tests. All the questions on the comprehension thing for 4 year olds are variants of "why is it good to share" "what can we do to keep the environment safe?" "why should we follow rules" "why do we need policemen" "why do we take turns" "why can't children stay at home alone" "why do we need to wear seat belts" "why should we recycle" "why do we say sorry" "Why do we need to wear helmets when riding bicycles" "why do children have to go to school" "why do we raise our hands" "why do we have to wait in lines" "why do we have addresses" "why should we read the news" "why do we have a president."

You might think I'm kidding or superfluous but all these questions are asked on the test. The only thing missing is "why do we all have to pay 100% of our earnings over our life to the …?"

Sep

4

Four Lessons from Druckenmiller, from Rocky Humbert

September 4, 2010 | 1 Comment

Here is an article about the lessons from Stan Druckenmiller's career. The author identifies four lessons: "Size matters," "Outperformance is possible," "Excellence takes hard work," "The money doesn't matter."

Here is an article about the lessons from Stan Druckenmiller's career. The author identifies four lessons: "Size matters," "Outperformance is possible," "Excellence takes hard work," "The money doesn't matter."

I note that these platitudes are not unique to money management– and could be straight out of a Tom Peter's Motivational Speech. The sad truth is that no matter how much I love, study and practice basketball and purchase AirJordan shoes, I still won't play like Michael Jordan. But it's a nice dream to think otherwise.

Pitt T. Maner III writes:

With practice there are many (even Rocky) who could give MJ a challenge at the free throw line or from the 3-pt line or playing "HORSE". Specialists in narrow aspects of the game. Trick shot artists. The niche players. So by practicing the unpracticed skills one might eke out a small advantage against the pros in the arcane areas where there is not actual physical contact.

It seems though there is a certain lack of diversity these days in basketball compared to era of Earl the Pearl, "Lucas layups", Pete Maravich, underhand freethrows by Rick Barry, Dr. J, Bird, Magic, et al.—more athleticism and muscle now (aka Shaq-types) with more plain vanilla in most cases and less skill/finesse. More of a business and more money on the line and more risk adverse to unusual styles. Defense and team play emphasized where every knows his "role". Even Lebron will have to adjust to team play at Miami and pass more and do other things.

On another note, interesting also that Mr. G is rolling out new mutual funds and a sequel to his "magic formula" book that apparently has many followers and "still beats the market" for now.

Victor Niederhoffer adds:

Knowing of the humility and inabilities of some of the people mentioned here, including myself, and there is certainly no absence of down years and sub par performance in the ones that I know about very well, including the 50% down year, in the year before I met him of one of them, and 7 years of 0 performance after that, I am still amazed that the records can be so good. I attribute most of it to the remaining winner of the coin toss problem. But something else is going on. The one thing that seemed right in the four lessons. They all go to the same schools. They lived next door to each other in the summer and often had dinners together or talked to each other every day. They all were agrarian reformers. And they all hated free markets. Thus with the idea that had the world in its grips. But mainly, they were always on same page with their positions, especially until the end of the year. Not an artifice I believe.

Vince Fulco adds:

And I think it was mentioned (maybe here, too much reading material this week) that Biggs is his father-in-law? Guessing the Pequot-MS cabal loomed large in the mix.

Russ Sears writes:

After 08-09 it should be clear that much of the MBS and other structured securities markets were a Lemon Market. With the manufactures putting all the faulty parts into the same car, One side knew exactly which cars were clunkers.

Further, while perhaps they were totally naive to get so close to the edge, once near, there was plenty of muscle willing to give company after company the final shove over the edge by marked to market in a lemon market. So much so that even those securities with seasoned cash flows and stockpiled protective subordinates tranches became suspect.

Of course if size is a disadvantage and does not matter, why would you buy so much insurance on these securities that you knew the counterparty would never have enough collateral to pay you. Unless of course that was the whole idea.

Sep

4

The Checker Maven, from Alan Millhone

September 4, 2010 | 3 Comments

Dear Mr. Niederhoffer,

Dear Mr. Niederhoffer,

Bob Newell, as long as I have know him, has remained neutral on politics, etc. on his webzine, the Maven till his article today.

Sincerely,

Alan

Sep

4

Quibids, from Allen Gillespie

September 4, 2010 | Leave a Comment

I have become fascinated with this site Quibids as a lab in which to study pricing particularly as it relates to psychological and odd pricing and substitute good pricing. Any thoughts and commentary would be appreciated. What are the fractional relationship of goods at various price points and what impact does the prior action have on the subsequent auction. Does a $100 gift certificate for different stores tend toward different average prices. Are these different prices also reflect of perceived value of the store and offer insight in the company's related stock price. Does the average price of a company's gift certificate auction lead moves in its stock price? So many questions this site creates.

I have become fascinated with this site Quibids as a lab in which to study pricing particularly as it relates to psychological and odd pricing and substitute good pricing. Any thoughts and commentary would be appreciated. What are the fractional relationship of goods at various price points and what impact does the prior action have on the subsequent auction. Does a $100 gift certificate for different stores tend toward different average prices. Are these different prices also reflect of perceived value of the store and offer insight in the company's related stock price. Does the average price of a company's gift certificate auction lead moves in its stock price? So many questions this site creates.

Sep

4

Speed Trading, from George Parkanyi

September 4, 2010 | 1 Comment

Chess players play speed chess to exercise their minds under pressure and hone their instincts and reflexes. A question– do or have any of you put yourself in a position of making rapid-fire decisions about a market direction as a way of warming up or practicing reaction time and decision making under pressure? I understand that some of you probably do this in your actual trading, but does anyone do it for practice, either on paper or with small amounts of money with actual trades?

Chess players play speed chess to exercise their minds under pressure and hone their instincts and reflexes. A question– do or have any of you put yourself in a position of making rapid-fire decisions about a market direction as a way of warming up or practicing reaction time and decision making under pressure? I understand that some of you probably do this in your actual trading, but does anyone do it for practice, either on paper or with small amounts of money with actual trades?

Example of a possible scenario. After the market has opened, someone calls out to you rapid-fire a number of futures markets or stocks, and you have to instantly answer– without hesitation– buy or sell. And you measure the results over a given holding period. I wonder if the results would be random? Would the results be different on paper vs. actually trading the answers?

Sep

4

Article on Information Theory, shared by Steve Ellison

September 4, 2010 | 1 Comment

Here is a very interesting article I found on Information Theory:

Excerpts:

The noisier the channel, the more extra information must be added to make error correction possible. And the more extra information is included, the slower the transmission will be. [Claude] Shannon showed how to calculate the smallest number of extra bits that could guarantee minimal error–and, thus, the highest rate at which error-free data transmission is possible. But he couldn't say what a practical coding scheme might look like.

Researchers spent 45 years searching for one. Finally, in 1993, a pair of French engineers announced a set of codes–"turbo codes"–that achieved data rates close to Shannon's theoretical limit. The initial reaction was incredulity, but subsequent investigation validated the researchers' claims. It also turned up an even more startling fact: codes every bit as good as turbo codes, which even relied on the same type of mathematical trick, had been introduced more than 30 years earlier, in the MIT doctoral dissertation of Robert Gallager, SM '57, ScD '60. After decades of neglect, Gallager's codes have finally found practical application. They are used in the transmission of satellite TV and wireless data, and chips dedicated to decoding them can be found in commercial cell phones.

—-

The codes that Gallager presented in his 1960 doctoral thesis (http://www.rle.mit.edu/rgallager/documents/ldpc.pdf) were an attempt to preserve some of the randomness of Shannon's hypothetical system without sacrificing decoding efficiency. Like many earlier codes, Gallager's used so-called parity bits, which indicate whether some other group of bits have even or odd sums. But earlier codes generated the parity bits in a systematic fashion: the first parity bit might indicate whether the sum of message bits one through three was even; the next parity bit might do the same for message bits two through four, the third for bits three through five, and so on. In Gallager's codes, by contrast, the correlation between parity bits and message bits was random: the first parity bit might describe, say, the sum of message bits 4, 27, and 83; the next might do the same for message bits 19, 42, and 65.

Gallager was able to demonstrate mathematically that for long messages, his "pseudo-random" codes were capacity-approaching. "Except that we knew other things that were capacity-approaching also," he says. "It was never a question of which codes were good. It was always a question of what kinds of decoding algorithms you could devise."

That was where Gallager made his breakthrough. His codes used iterative decoding, meaning that the decoder would pass through the data several times, making increasingly refined guesses about the identity of each bit. If, for example, the parity bits described triplets of bits, then reliable information about any two bits might convey information about a third. Gallager's iterative-decoding algorithm is the one most commonly used today, not only to decode his own codes but, frequently, to decode turbo codes as well. It has also found application in the type of statistical reasoning used in many artificial-intelligence systems.

"Iterative techniques involve making a first guess of what a received bit might be and giving it a weight according to how reliable it is," says [David] Forney. "Then maybe you get more information about it because it's involved in parity checks with other bits, and so that gives you an improved estimate of its reliability." Ultimately, Forney says, the guesses should converge toward a consistent interpretation of all the bits in the message.

Jim Sogi writes:

I think that is why many market price moves come in threes as an error correction devise. Like the recent triple bottom.

Jon Longtin writes:

Very interesting articles on the history of encoding schemes.

One interesting thing to note is that if you take even a simple information stream and encode it with any of the numerous algorithms available, the encoded version of the information is typically unintelligible to use as humans in any way, shape, or form.

‘hotdog’ for example, might encode to ‘b$7FQ1!0PrUfR%gPeTr:$d’

These encoding algorithms work by rearranging the bits of the original word, looking for patterns, and applying mathematical operators on the bit stream.

Many of the financial indicators and short-term predicative tools that abound today are based on some combination of the prior price history, but often in a relatively simplistic way. For example, although the weightings may change for various averages, their time sequence, i.e. the order in which they are recorded and analyzed is the same: a sequence of several prices over some period is analyzed in the same order in which it was created.

Perhaps, however, there is some form of intrinsic encoding that is going in the final price history of an instrument. For example, it could be reasoned that news and information does not propagate at a uniform rate, or that different decision makers will wait a different amount of time before reacting to a price change or news. The result might be that the final price history that actually results, and that everyone sees and acts upon, is encoded somehow based on simpler, more predictable events, but the encoding obfuscates those trends in the final price history.

Maybe it is no coincidence that Jim Simons of Renaissance Technologies did code breaking for the NSA early on in his career.

Unfortunately reverse-engineering good hashing codes, particularly those designed to obfuscate, such as security and encryption algorithms are notoriously difficult to crack. (The encrypted password file on Unix machines was, for many years, freely visible to all users on the machine because it would simply have taken too long to crack for machines of the time.) On the other hand, the cracking algorithms often require little knowledge of the original encoding scheme, instead simply taking a brute force approach. Thus if there were such an underlying encoding happening with financial instruments—and the encoding might be unique for each instrument—then perhaps there is some sliver of hope that it might be unearthed, given time, a powerful machine, and some clever sleuths.

For all I know this has been explored ad nauseum both academically and practically, but it does get one wondering …

Sep

4

King Me, from Alan Millhone

September 4, 2010 | Leave a Comment

All who are interested look at the blog King Me. A segment of this upcoming documentary on the game of Checkers will be submitted to the Sundance Film Festival.

All who are interested look at the blog King Me. A segment of this upcoming documentary on the game of Checkers will be submitted to the Sundance Film Festival.

Part of the movie centers around a very poor but top South African player of color named Lubabalo Kondlo from Port Elizabeth who struggles everyday.

The blog is well worth a look

Regards,

Alan

Sep

4

Scoring From the Bench, from George Parkanyi

September 4, 2010 | Leave a Comment

Back in 2006-2007, for amusement I participated in the Motley Fool's CAPS stock-picking game. After playing for a while I pointed out some mathematical flaws in their scoring system, and exactly how it could be gamed (which I did for a while because it was easy). They chose not to fix the flaw. Well, I racked up a pretty high percentile score and was one of their top stock-pickers for a time. Then as I started my own blog, I got tired of it and finally just forgot about it. Now again, after 3 years of doing nothing to the position I had abandoned– not even logging into the site, I was informed by email today that I once again have near-genius status as some kind of ace stock-picker at the 97.44th percentile.

Back in 2006-2007, for amusement I participated in the Motley Fool's CAPS stock-picking game. After playing for a while I pointed out some mathematical flaws in their scoring system, and exactly how it could be gamed (which I did for a while because it was easy). They chose not to fix the flaw. Well, I racked up a pretty high percentile score and was one of their top stock-pickers for a time. Then as I started my own blog, I got tired of it and finally just forgot about it. Now again, after 3 years of doing nothing to the position I had abandoned– not even logging into the site, I was informed by email today that I once again have near-genius status as some kind of ace stock-picker at the 97.44th percentile.

Maybe my friend and once stock market mentor in the early days Omar Sheriffe Vernon el-Halawani was onto something when in his last years he would keep telling me– "George, why bother to sell?" (He was a high-school teacher and one who consistently made money in the stock market over the decades. He had a great nose for value, not in the Graham and Dodd sense, but rather in understanding which were the economically important up-and-coming industries, and once he bought something he liked, he would hang on to it like a dog to a bone. He traded a little around the edges, but only for amusement. He also loved selling puts for income.)

Or maybe as a broken clock is right twice a day, so is a fool right once every three years …

Sep

4

Ryan Harrison, from Jay Pasch

September 4, 2010 | Leave a Comment

The Harrison kid looks to have quite the bright future, compact and gritty on the inside…

The Harrison kid looks to have quite the bright future, compact and gritty on the inside…