Oct

10

Lunch Hour, from James Sogi

October 10, 2008 | 1 Comment

Here is a hypothesis. After a hectic morning of trading, traders are tired, have low blood sugar and tend to be pessimistic, or want to unload a position before going to eat lunch, driving the market down. After a nice lunch or an appropriate refreshment, the world looks a lot rosier and leads to buying and an up market. I remember a funny story when I was a young clerk at a law office on Wall Street back in the late 60s going out to lunch with the office. Back then the 2+ martini lunch was normal business. I'm not sure how they did any business after lunch, but everything seemed fine after lunch. By the way, I just had a nice lunch at Pepolino in Tribeca on West Broadway. Highly recommended. Today the lunch market was a bit dreary and slow as usual, but after lunch there was a nice little surge and as the market's blood sugar revived.

Here is a hypothesis. After a hectic morning of trading, traders are tired, have low blood sugar and tend to be pessimistic, or want to unload a position before going to eat lunch, driving the market down. After a nice lunch or an appropriate refreshment, the world looks a lot rosier and leads to buying and an up market. I remember a funny story when I was a young clerk at a law office on Wall Street back in the late 60s going out to lunch with the office. Back then the 2+ martini lunch was normal business. I'm not sure how they did any business after lunch, but everything seemed fine after lunch. By the way, I just had a nice lunch at Pepolino in Tribeca on West Broadway. Highly recommended. Today the lunch market was a bit dreary and slow as usual, but after lunch there was a nice little surge and as the market's blood sugar revived.

To test the hypothesis I looked at the average pre lunch, lunch time period and the post lunch time period for the last 20 years or so.

Pre lunch av. -.04

Post lunch av. .07

Might be fun to see how much more pronounced this might have been in the martini lunch era.

Oct

10

Simpler Ways of Doing Business, from Nigel Davies

October 10, 2008 | 1 Comment

In the wake of the recent debacle, I wonder if some more traditional ways of doing business are about to boom. I'm not convinced that the gloating described below forshadows the return of the Roman empire, but perhaps we will see asset based finance services doing well.

In the wake of the recent debacle, I wonder if some more traditional ways of doing business are about to boom. I'm not convinced that the gloating described below forshadows the return of the Roman empire, but perhaps we will see asset based finance services doing well.

BTW, noting some other posts comparing today to the 1930s, I believe that we are dealing with two individual samples of one, which have very little to do with each other. What we have is something new, and completely unknowable despite the comfort that might be derived from labeling it.

From the FT :

Giulio Tremonti was almost gloating when he addressed the Italian Parliament on Thursday. He described the geography of the financial crisis with relish: the Northern earthquake, with its epicentre in Iceland, its problematic “Continental dimension”, the troubles in the UK, and the fear of a spill over into the Baltics and eastern Europe. As for Italy’s banks, the Treasury Minister said they were sheltered from the crisis because they were “less advanced and sophisticated” than elsewhere.

Back-handed praise, indeed. But Italy is a demonstration of the merits of doing nothing, a conservatism that has served its stay-at-home banks well. Although Italian bank stocks have collapsed, depositors have not rushed to withdraw their cash – to the disappointment of the paparazzi waiting to photograph panic outside branches.

Oct

10

A Message from the President, from John Tierney

October 10, 2008 | 1 Comment

Following his recent death, there has been much written about John Templeton. Most stories emphasized two aspects of his life: his most recent views on the market (very bearish) , and how he made his first big score.

Following his recent death, there has been much written about John Templeton. Most stories emphasized two aspects of his life: his most recent views on the market (very bearish) , and how he made his first big score.

It's this second aspect that interests me. To recap, in 1939 Templeton borrowed $10,000 and bought 100 shares of every Big Board stock selling for less than $1.00. There were 104 of them at the time and 34 of them were in bankruptcy. Four years later, only four of the 104 proved worthless, and his initial stake had increased by approximately 400%.

I have no idea where the market is heading from here but as I have read recently, were someone to have invested a given sum every month beginning in late '29, and continued to do so through '32, he would have realized a very nice return and one which would have continued to appreciate nicely throughout the Depression years. I don't believe many would argue that the current market is healthy but might argue that there are some excellent values for those courageous enough to take the risk. Maybe it's time to "Templeton" the market.

Could the same strategy work again? With a few modifications, I believe it's worth a try. The first adjustment I made was to calculate today's equivalent to '39s one dollar stock. The calculator I used determined that a dollar back then is $14.78 through 2007. It's no big deal to find equities that currently trade at or below that figure; however, unless you possess huge amounts of capital buying 100 of every equity below $14.78 would be awfully expensive.

Now, I have many, many watch lists — several of which go back a decade. Last evening I went through them and quickly found 17 which met the price threshold. Some I have owned, some I have not. Some treated me well, others poorly. Some are relatively new, some are very old (e.g, CX was purchased in '99 and sold in '01 — until last night I had not even remembered its existence). But all are flawed in that, at one time or another, I felt they'd be a good buy or interesting speculation. Their prices today when matched against the prices I recorded when adding them to one of my watch lists indicates, in most cases, I was wrong.

Alice Allen adds:

I was glad to be reminded of Templeton's strategy after yesterday morning (10/10) when I bought 100 shares each of six stocks under $3 that I had owned earlier at higher prices. For two stocks, industry experience gives me an edge to think these companies will survive. For two stocks, excellent customer experience makes me willing to take a chance. The last stock is a small oil company with all the potential for unexpected movement. Tierney's post has encouraged me to explicitly track how this strategy works out. I'm considering each position as simply a call option with delta=1 and no decline from theta, certainly among my least risky trades in this market. Now if I can just resist increasing position size on random positive fluctuations…

I was glad to be reminded of Templeton's strategy after yesterday morning (10/10) when I bought 100 shares each of six stocks under $3 that I had owned earlier at higher prices. For two stocks, industry experience gives me an edge to think these companies will survive. For two stocks, excellent customer experience makes me willing to take a chance. The last stock is a small oil company with all the potential for unexpected movement. Tierney's post has encouraged me to explicitly track how this strategy works out. I'm considering each position as simply a call option with delta=1 and no decline from theta, certainly among my least risky trades in this market. Now if I can just resist increasing position size on random positive fluctuations…

Kim Zussman Reflects:

'39 was 10 years after the crash, and fortuitously near the end of the Depression. Presumably by that time, with the main worry survival and the start of WWII, the few who had money were more disposed to buy stocks of food than stocks of companies in bankruptcy.

That the above question is being asked suggests we aren't there yet.

Oct

10

Microstructure, from Steve Ellison

October 10, 2008 | Leave a Comment

Price difference (absolute value) between consecutive ticks for the S&P 500 big contract, using E**** Descriptive Statistics:

4/7/2008 10/8/2008

Mean 0.2 0.6

Median 0.2 0.5

Mode 0.2 0.5

Standard Deviation 0.1 0.2

Minimum 0.0 0.0

Maximum 0.5 3.5

Sum 394.5 2162.7

Count 2006 3639

95th percentile 0.3 1.0

5th percentile 0.1 0.5

Oct

10

Funky Town, from Stefan Jovanovich

October 10, 2008 | Leave a Comment

An "old news" addendum: last year, the spot price for a container shipment from Asia to Europe was $2,800. This week it was $700.

"That rate is 'unsustainable,'" says Eivind Kolding, chief executive of Copenhagen-based A.P. Moller Maersk AS, the world's biggest shipping company by sales. (From WSJ Online today)

Oct

10

Oil at Noon, from Riz Din

October 10, 2008 | 2 Comments

It's all rather beautiful how the worry generating meme of permanently high oil prices and ever higher food prices has given way without anyone in the mainstream batting an eyelid. I just typed the word into Amazon.co.uk. and the first page of search results yields the following pessimistic titles:

- The End of Oil: The Decline of the Petroleum Economy and the Rise of a New Energy Order

- Beyond Oil: The View from Hubbert's Peak

- The Last Oil Shock: A Survival Guide to the Imminent Extinction of

Petroleum Man

- Party's Over: Oil, War and the Fate of Industrial Societies

- A Crude Awakening

All of these books are marked down, with A Crude Awakening trading at almost a quarter of the recommended price. I expected deeper discounts will trail further declines in the spot price. On the same Amazon page, we also have 'The Myth of the Oil Crisis: Overcoming the Challenges of Depletion, Geopolitics, and Global Warming', price unchanged.

Oct

9

Current Update of Fed Model, from Alex Castaldo

October 9, 2008 | 13 Comments

SPX = 1000

Estimated Earnings = 97.74

=> earn yield 9.77%

10-yr Treasury Yield = 3.65%

=> spread 6.12%

=> SPX fair value = 2676 = earnings/10-yr

=> undervaluation -62.64%

=> expected return = 33.74% = 0.082 + 4.172 * spread

The model is forecasting a one year return of approximately 34%.

Oct

8

A Similarity, from Riz Din

October 8, 2008 | 5 Comments

I quite like the UK deal. The banks have agreed to raise £25bn between them - they'll probably be passing the begging bowls around current shareholders, hedge funds etc, as they don't have to accept funds from the government, which would dilute ownership . The government option is there but I imagine it will only be used as a desperate last resort. Better to have diluted ownership than nothing, I guess.

'Brown's bailout' has quite a nice ring to it, but from what I've read there are many more references to deal as a 'rescue' rather than 'bailout'.

Oct

7

Volkswagen Rollercoaster, from Henrik Andersson

October 7, 2008 | 1 Comment

This must be some kind of record intraday move for a EUR 100bn market cap stock. It was up 57% intraday, apparently on a short squeeze, then ended the day down 5 Euros.

{kind=link}

Oct

7

Rolling 7 Day DJIA Returns <-15%, from Kim Zussman

October 7, 2008 | 2 Comments

9 of the 39 cases since 1928 were not during the Depression:

Date 7D

09/21/01 -0.163

09/20/01 -0.165

10/27/87 -0.178

10/26/87 -0.238

10/23/87 -0.191

10/22/87 -0.222

10/21/87 -0.179

10/20/87 -0.258

10/19/87 -0.309

05/22/40 -0.166

05/21/40 -0.212

05/20/40 -0.174

05/17/40 -0.161

03/31/38 -0.155

03/30/38 -0.161

10/19/33 -0.154

07/21/33 -0.152

10/13/32 -0.161

10/10/32 -0.183

09/19/32 -0.160

09/16/32 -0.161

06/01/32 -0.157

05/31/32 -0.158

04/11/32 -0.153

04/08/32 -0.185

12/16/31 -0.151

10/05/31 -0.198

10/02/31 -0.165

06/24/30 -0.152

11/14/29 -0.157

11/13/29 -0.274

11/12/29 -0.189

11/07/29 -0.209

11/06/29 -0.225

11/04/29 -0.157

10/31/29 -0.162

10/30/29 -0.195

10/29/29 -0.310

10/28/29 -0.238

Oct

7

Good for the Goose?, from Nigel Davies

October 7, 2008 | Leave a Comment

I took out a personal loan today for no other reason than the fact that the banks are hoarding cash. I figure that's what's good for the goose is good for the gander.

I took out a personal loan today for no other reason than the fact that the banks are hoarding cash. I figure that's what's good for the goose is good for the gander.

Meanwhile I had a look round some estate agents posing as a cash buyer of repossessions and/or remnants of what property developers want to unload. Whenever they tried the usual sales patter (e.g. people are queuing up for this one) it was interesting to see how much I could make 'em squirm with statements such as 'the banks aren't lending to anyone right now' and such like. My impression was that the agents are also exasperated with the high prices as there's no liquidity at these levels.

Oct

7

Option Volatility Spread, from Philip J. McDonnell

October 7, 2008 | 3 Comments

During one's lucubrations on the state of the markets perhaps it would be good to consider options as a way to deal with the current volatility. In particular, option spreads can help to manage the risk of a position. Given the current volatility, risk management can be a valuable thing.

One spread to consider is a volatility spread. The mechanics are simple. Buy two out of the money calls for 2. Sell one at the money call for 5. You now have a net cash credit of 1 point ($100). You will also have to maintain margin of $500 for the one call you have sold, assuming the strike prices are 5 points apart.

Assuming some realistic Greeks you might have the following:

Q Option Pr delta vega

b 2 Nov 69c 2 .32 8.5

s 1 Nov 64c 5 -.59 -10

Net 1 .05 7

In the short run you have a slightly bullish spread with an overall delta of about 5%. The spread will benefit from volatility as evidenced by the net vega of 7.

The spread will make a profit of 1 anywhere from 64 down to zero so you are protected from banking Armageddon. Small losses will occur between 64 and 69. The max loss will be at 69 and will be limited to 4 points. Above 69 the two calls will kick in (less the short one call) and the spread will become increasingly profitable with no upside profit limit.

If one believes that the banking system is set for a domino collapse scenario then a similar spread can be done with puts. Sell 1 at the money put and buy 2 out of the money for a net credit. Then the spread will have unfettered profit potential all the way down to zero. It will lose a small amount if the underlying closes out between the strike prices. The spread also will enjoy a small fixed profit in the amount of the net credit anywhere above the upper strike price.

Dr. McDonnell is the author of Optimal Portfolio Modeling, Wiley, 2008

Oct

7

Utopia is Here, from Riz Din

October 7, 2008 | Leave a Comment

Last night, I was watching an episode of Tribe with Bruce Parry where he's helping a local tribesman to hunt for a Cayman alligator. Parry comments that the Cayman has barely evolved since the time of the dinosaurs. In one sense I thought, yes, it is the perfect creature for its environment, but then I reasoned that the only reason it hasn't evolved is that it's environment hasn't changed to necessitate such a change. In one sense, the alligator is frozen in time because it's environment is broadly frozen in time. Likewise for humans. Jones' idea that 'a grand averaging is slowing evolution's power' makes sense, but there is no reason to think the rate of evolution will not change as the world changes, and we can be sure that the world will one day experience massive change just as it has in the past.

Last night, I was watching an episode of Tribe with Bruce Parry where he's helping a local tribesman to hunt for a Cayman alligator. Parry comments that the Cayman has barely evolved since the time of the dinosaurs. In one sense I thought, yes, it is the perfect creature for its environment, but then I reasoned that the only reason it hasn't evolved is that it's environment hasn't changed to necessitate such a change. In one sense, the alligator is frozen in time because it's environment is broadly frozen in time. Likewise for humans. Jones' idea that 'a grand averaging is slowing evolution's power' makes sense, but there is no reason to think the rate of evolution will not change as the world changes, and we can be sure that the world will one day experience massive change just as it has in the past.

His final semi-positive comment is that 'Health, birth control and the healing power of lust all conspire to tell us that, at least in the developed world, and at least for the time being, evolution is over. So, if you are worried about what Utopia is going to be like, cheer up– you are living in it now.' From one perspective, I disagree wholesale with this comment, but it's more of an issue of definition. Now that we are delving deep into evolutionary mechanics with the tools of genetic research we are already able to tweak the genome in such ways that chosen traits and improvements are passed on to future generations. It may not happen in our lifetimes, but I reckon that we'll soon be juicing up evolution and better tailoring the human to it's environment better than ever before.

Relating the rate of evolutionary change to what is happening in the markets, I am led to wonder whether those living fossil creatures that have remained unchanged over the millennia are less able to change to changing circumstances. In trading, there are operators who become hard wired to old regimes. And so it is for banks and other institutions, where a successful model embeds itself ever deeper in to the biology of the company, making it more susceptible to a sudden change. Also, just as bacteria evolve at a much faster rate than larger creatures, the same seems to hold true of companies.

John White remarks:

Evolution is not a force unto itself. It is the description of the result of natural selection. Organisms that have genetically unique adaptations/mutations that provide an edge in reproducing have a higher probability of passing that adaptation/mutation along to their offspring. Humans' unique adaptation is our brain. Our highly sophisticated brain gives us the capacity for reason, and specifically, the capacity to test. The technological advances that have been produced by the scientific method have mitigated our environment’s impact on our ability to survive, reproduce, and raise viable offspring. While physical attributes will always play a part, the effects of natural selection on humans will be seen more and more in our intellectual abilities as time progresses. The corollary for business is that while balance sheets will always play their part, management and culture will become increasingly important. The question for the spec is how to measure that.

Evolution is not a force unto itself. It is the description of the result of natural selection. Organisms that have genetically unique adaptations/mutations that provide an edge in reproducing have a higher probability of passing that adaptation/mutation along to their offspring. Humans' unique adaptation is our brain. Our highly sophisticated brain gives us the capacity for reason, and specifically, the capacity to test. The technological advances that have been produced by the scientific method have mitigated our environment’s impact on our ability to survive, reproduce, and raise viable offspring. While physical attributes will always play a part, the effects of natural selection on humans will be seen more and more in our intellectual abilities as time progresses. The corollary for business is that while balance sheets will always play their part, management and culture will become increasingly important. The question for the spec is how to measure that.

Oct

7

Question for the Fixed Income Experts, from Vince Fulco

October 7, 2008 | Leave a Comment

I was wondering if 'the markets' are being held hostage by potential adverse results of the ISDA auctions for CDS settles of FNM, FRE, LEH and WAMU? See FT article.

The GSEs were completed yesterday but LEH on Friday, WAMU later in the month.

Oct

7

An Interesting Sidelight, from Victor Niederhoffer

October 7, 2008 | 4 Comments

It is interesting to learn that CEOs of firms get earnings reports some two weeks or more before their release. The B of A and Lehman released their earnings two weeks early for various reasons, and this must be the norm. Everyone knows that we give away our emotions in a hundred ways to a hundred people — the significant other, the office assistant, the very special friend, the night watchman. We do it often with a smile, a frown, or a late night at office among so many other ways. The amazing thing about it all is that stock prices of companies don't move in the direction of the earnings release much more often than they do. The quantification of this, especially big moves before the release, might well take this into account.

It is interesting to learn that CEOs of firms get earnings reports some two weeks or more before their release. The B of A and Lehman released their earnings two weeks early for various reasons, and this must be the norm. Everyone knows that we give away our emotions in a hundred ways to a hundred people — the significant other, the office assistant, the very special friend, the night watchman. We do it often with a smile, a frown, or a late night at office among so many other ways. The amazing thing about it all is that stock prices of companies don't move in the direction of the earnings release much more often than they do. The quantification of this, especially big moves before the release, might well take this into account.

Oct

7

SAT Question # 1008, from Kim Zussman

October 7, 2008 | 4 Comments

1008. During a period prone to large market declines on Fridays and Mondays, there were two consecutive weeks with crashes on Monday followed by large gains Tuesday. The first week saw a large drop from Tuesday to Friday. What happens the second week?

A. The market is too cute to repeat except when you least expect it, so Weds-Friday continues with large gains.

B. The market is too cute to repeat except when you least expect it, so Weds-Friday repeats with large losses.

C. Volatile markets are baited heavily to maximize extinction, so you should not trade them unless you can't get another job.

D. It's October, and Treasury ran out of Treats for Tantrums. Market will be about unchanged.

E. Under the Obama administration, it is finally legal for Harriet Tubman to wed Sacajawea.

Oct

6

Why I Shop at Ace Hardware, from Steve Leslie

October 6, 2008 | Leave a Comment

I recently went to an Ace Hardware store with my neighbor Gary, who needed to take care of some things. I asked him why he chose to come to Ace rather than the Loews that was right next door or the Home Depot less than a half mile away.

First, he told me, the business is locally owned and he likes to support local businesses. Second is he feels right at home with the friendly helpful staff on hand to help him and answer any questions he might have.

With some skepticism, I walked through the door with Gary and immediately one of the employees greeted us and inquired how he might help. Gary mentioned that he needed some keys made for his auto. One of the staff said to follow her and she would take care of that right away. She proceeded to make the keys and then said before he left to go out to the car to insure that they work and she would wait. He came back and said they were just fine. He also said he needed some propane for his grill. He brought his tank in but they said that he needed a new tank and he bought one and they filled it while we waited inside conversing with the employee who made the key for us.

After the tank was filled, we got into the Cadillac Escalade he just bought and drove away. Immediately, he looked at me and said "Do you see what I mean?" "That is why I shop at Ace." I now understand.

Oct

6

Unclear, from Nigel Davies

October 6, 2008 | 4 Comments

Chessplayers have a strange vocabulary that may be of benefit to market people. For positions in which they know what is happening they'll say, 'White is better' or 'Black is better' or 'equal' or 'absolutely equal'. Either side can also be 'much better' or 'winning'.

Chessplayers have a strange vocabulary that may be of benefit to market people. For positions in which they know what is happening they'll say, 'White is better' or 'Black is better' or 'equal' or 'absolutely equal'. Either side can also be 'much better' or 'winning'.

For positions in which they don't know what's happening the word 'unclear' is often used. This means that they don't know what's happening but apply a term to it so that it represents and intelligent assessment. It's this point that I believe can be of most interest to those involved in markets, as usually people feel obliged to have an opinion.

Accordingly I'd describe a whole range of market scenarios as 'unclear', as well as the likely outcomes of seemingly obvious interventions. What has most struck me about the various bailouts, for example, is that they appear not to consider the dynamic effects of various parties' reactions. For example, I doubt that a war for capital had been considered, which now seems to be developing between both nations and banks. Presumably this kind of thing will also happen at an individual level when the credit crunch becomes more apparent to the man on the street. It only seems like these events might be controlled whilst in reality the situation is… completely unclear.

Oct

5

Mother of All Swans, from Kim Zussman

October 5, 2008 | 5 Comments

To me the biggest assumption about financial markets is that history will repeat. The second biggest assumption is that the Great Depression won't.

To me the biggest assumption about financial markets is that history will repeat. The second biggest assumption is that the Great Depression won't.

At least in terms of volatility, it looks like we are going to test both these assumptions soon.

VXO is recently over 50, which has occurred infrequently since inception in 1986. But this is a short time when studying mass-extinctions, so to study volatility over longer periods I used DJIA daily returns 1928-present, and for every non-overlapping 10 day period I calculated the STDEV. This chart shows the recent 10 day/daily STDEV is >3%, which occurred recently only in 1997, 1998, and 2001. Prior to this, all the instances were in the 1920s and 30s.

{kind=link}

Mark Isbic writes:

Today here in Israel, the mother of all swans started with the TA 25 and 100 down 7% and the Tel Tech down over 11%. If this is any indication, tomorrow will be very ugly unfortunately. I say to myself it will be a great time to jump in. Unfortunately I have been doing this for several months and have taken a beating!

Jason Shapiro remarks:

Anybody see the Bloomberg story about how current financial conditions are a black swan event? Statistically they say this is rarer than a comet's destroying the earth. And the data they used go all the way back to 1993!

Oct

4

I Just Realized How Bad it Really Is, from Daniel Flam

October 4, 2008 | 8 Comments

I was talking to my friend who is in 20 million dollars deficit on a major building project in Manhattan that is already under way. His story is that the first bank gave a promise for the money, then folded. The bank that acquired the other bank went forward and promised the money. Then it folded. This went on for a few rounds, and now he is hoping that following the bailout he won't go bankrupt together with all the contractors and workers that rely on this. Now multiply this by hundreds of thousands of projects across America and various industries… Another friend is a real estate broker, and was telling me that people are putting properties on the market at "sell at all costs" prices.

I was talking to my friend who is in 20 million dollars deficit on a major building project in Manhattan that is already under way. His story is that the first bank gave a promise for the money, then folded. The bank that acquired the other bank went forward and promised the money. Then it folded. This went on for a few rounds, and now he is hoping that following the bailout he won't go bankrupt together with all the contractors and workers that rely on this. Now multiply this by hundreds of thousands of projects across America and various industries… Another friend is a real estate broker, and was telling me that people are putting properties on the market at "sell at all costs" prices.

Here is the point of this post: I wonder, if the banks are going to do a "take the money and run" — how is the government making sure that the money is actually getting to the people who need it?

Kim Duncan replies:

The banks will sell assets to TARP and reduce their short-term borrowings (repo, Fed facilities, unsecured inter-bank borrowings) in order to reduce leverage. That will only marginally allow the recapitalisation that is required before banks begin to expand lending once again. We are in a credit contraction and TARP will not put an end to this process which could last years.

Your question is based upon a false premise. People who need the “money” (actually credit) are not necessarily the ones who deserve the credit. Is the project your friend trying to finance actually worthy of the investment? Required returns on investment are going up on everything since capital is scare, debt finance is contracting and asset prices are declining. The project will have to compete for its funding and its provision will not be based upon “need” but rather the risk-adjusted returns.

However, the other part of your question - “Take the money and run” is misleading. Banks will sell assets to the Treasury and reduce their borrowings. The Treasury will increase their borrowings by precisely the same amount which the banks reduce their borrowings. Leverage will be reduced in the banking system but the government borrowings will exactly offset. As a result, the same amount of cash freed up from lending to banks will be absorbed by lending to the government. As far as the banks are concerned, the lower leverage will not likely lead to lending capacity and hence the TARP will not, on its own, lead to new credit being offered to the private sector. The best that can be hoped for is that some price momentum of distressed assets will lead to an improvement in sentiment towards and between the banks thereby allowing the interbank lending and deposit markets to function. A first step, perhaps, but clearly no panacea.

Oct

3

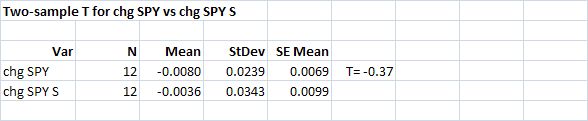

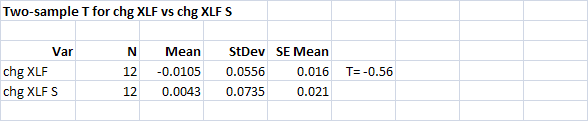

Dood, What Happened to My Shorts? from Kim Zussman

October 3, 2008 | 1 Comment

1. Has the behaviour of XLF changed since the SEC restricted shorting of certain financial stocks?

First compare daily return SPY for the period before and after the shorting ban (after=S):

SPY down for both periods, difference N.S. Now the same for XLF:

Again the difference was N.S. Like SPY, XLF was down in the pre-short ban period, but unlike SPY it went up post.

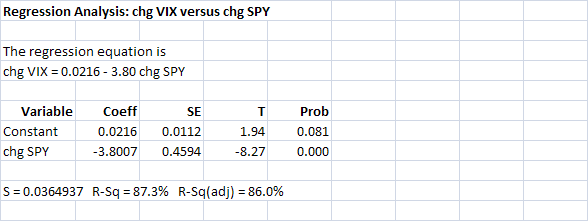

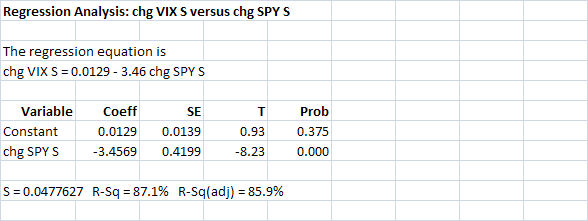

2. What about correlation with VIX? (First the control group)

Here is regression of daily change VIX vs SPY for the 11 days before the ban on shorting:

And the same since the change:

R^2 the same at 87%.

Oct

3

Car Dealerships, from Alan Millhone

October 3, 2008 | Leave a Comment

I wonder, in the next few months how many car dealerships around the US will fold up their tents? On a trip today, I noticed a fellow dressed as a clown in Hilliard, Ohio holding a sign offering "FREE RENT." An obvious sign of a struggling economy. I was moving in traffic and could not stop to get one of the flyers he was holding in my other hand.

Oct

3

A Reflection, from Victor Niederhoffer

October 3, 2008 | 1 Comment

Without in any way indicating prognosticativability, I note that the proverbs "the threat is worse than the execution" and "buy the rumor, sell the news" were illustrated a hundred times to the horror this week.

Mike Libert adds:

"Buy on mystery, sell on history"… The sentiment is the same, but it rhymes!

Oct

3

On the Road to Marion, Illinois, from Alan Millhone

October 3, 2008 | Leave a Comment

My Blackberry was busy today vibrating as the many market-related emails came through, but dangerous to read while driving! After I left Belpre this morning for my 523 mile trek, I was noticing gas prices, and the cheapest I saw was outside of Lancaster, Ohio (birthplace of General Wm. T. Sherman) at a Valero station, 3.39 per gallon. Traffic was heavy today with 18 wheelers as I traveled across Ohio and approached Indiana. Looks like the new football stadium is completed at Indy. They call it "Lucas Oil Stadium." Any of you know the story on the name? It would take oil profits to build that massive stadium that can be seen way out of Indy! Leaving Indy a billboard caught my eye. I have seen this fellow and his business on billboards around Indy, but today his ad was different. It advertised Sycamore Chevrolet, and showed the usual photo of Dennis Meng (the dealership's owner), but today with his photo had a statement attached that read, "I stake my reputation on each and every 'reconditioned' [that word concerning cars has always bothers me] car that we sell from our lot." Car dealers and politicians always make promises along those lines. Illinois State Police were in unmarked cars today hidden, behind overpass bridge pillars to run their radar. I always run with the traffic, which was moving along at 70 plus today.

My Blackberry was busy today vibrating as the many market-related emails came through, but dangerous to read while driving! After I left Belpre this morning for my 523 mile trek, I was noticing gas prices, and the cheapest I saw was outside of Lancaster, Ohio (birthplace of General Wm. T. Sherman) at a Valero station, 3.39 per gallon. Traffic was heavy today with 18 wheelers as I traveled across Ohio and approached Indiana. Looks like the new football stadium is completed at Indy. They call it "Lucas Oil Stadium." Any of you know the story on the name? It would take oil profits to build that massive stadium that can be seen way out of Indy! Leaving Indy a billboard caught my eye. I have seen this fellow and his business on billboards around Indy, but today his ad was different. It advertised Sycamore Chevrolet, and showed the usual photo of Dennis Meng (the dealership's owner), but today with his photo had a statement attached that read, "I stake my reputation on each and every 'reconditioned' [that word concerning cars has always bothers me] car that we sell from our lot." Car dealers and politicians always make promises along those lines. Illinois State Police were in unmarked cars today hidden, behind overpass bridge pillars to run their radar. I always run with the traffic, which was moving along at 70 plus today.

Traveled down 57 for about 90 miles, and now in my room in Marion. Had a nice Mexican platter up the street before settling into my room. Likey I won't have TV on this weekend, and will concentrate on my Checker game tomorrow and Sunday. Read a posting just now that Riz is going to quit the trading game. I might suggest taking up Chess or Checkers — that will challenge you as much or more than the Market Mistress ever dreamed.

N. Petit reminisces:

…We crossed Ohio, the three states beginning with 'I'…

Oct

3

Caravaggio Is No More, from Riz Din

October 3, 2008 | 7 Comments

I've decided to call it quits on the trading front (I was trading only my personal account) due to reasons of insufficient capital. Just thought I'd share my last trading blog post.

The final blog post concerns Ivan Drago, and an accounting of the similarities between myself and the real Caravaggio.

1/ In Rocky IV, Rocky Balboa is in Apollo Creed's corner watching Creed get absolutely pummelled by Ivan Drago, a stone cold Russian killing machine. Creed is under-trained and over-the-hill and Rocky knows it, but he can't bring himself to dropping the towel and calling an end to the fight until it is too late - Drago delivers a literal killing blow with no remorse, famously commenting 'If he dies, he dies.'

Rocky, sorely racked with guilt and anger, desperately needs revenge. He heads out to Russia to train in the mountains and fight Drago on his own turf. Up against the odds, Balboa achieves the impossible. He succeeds in defeating Ivan Drago, winning over the hostile crowd in the process. Let's get one thing straight: this is Hollywood. Rocky Balboa was in the wrong. He should have dropped the towel and let Creed's pride take a hit. Balboa let his friend die and there is no coming back from that. Beating Drago in a revenge match may bring some sense of justice but the responsibility still lies with Balboa. We can also make the case that just as Creed shouldn't have fought with Ivan Drago, nor should Balboa, despite all his training and despite the victorious outcome. Of course, that may not have made for a very exciting movie. Hollywood is filled with such underdog stories and they make for enjoyable viewing but we must remember that if you fight the odds all the time in the real world, they'll eventually catch up with you. (1)

Here we have one of the most important lessons from the game of trading: process trumps outcome over the long-term. It is because of this idea that I am making the decision to throw in the metaphorical towel. For all intents and purposes, my trading life is over. It was inevitable.

Just as we should consider the alternative outcomes that never materialised in Rocky IV, so we must do the same with our trading. I know that I have died many a death in the alternative histories that never happened but that could have happened had the gods of chance not been so generous with the roll of the die. My capital is pathetically low (an affliction suffered by most traders) and I wanted to build up my equity to the stage where I could enact the right trading processes. I knew it was only then that I could start trading properly. But the paradox is that in order to get there I needed to take outsized risks to build up the capital in the first place. It was a classic Catch-22 situation, one where I had to follow the wrong path to get to the right path. I crashed and burned, worked my back up, burned again, and partially recovered. But it is not sustainable. I cannot keep on fighting the Drago. It is not healthy and conducive to practising the virtuous life.

My passion for the financial markets remains undimmed but this is my last blog post for the foreseeable future. I hope it serves as a useful record of a solitary trader's efforts. The journey has been worth taking in every respect and I thank you all.

—

In this section, I compare my trading life with that of the real Caravaggio.

2/ Caravaggio the artist lived from 1571 to 1610 and what a life. He was a supremely gifted painter but Caravaggio was not a nice person to be around. Rebellious to the extreme and prone to outbursts of excessive aggressiveness, Caravaggio was always getting in trouble every where he went, trouble that would often included a burst of violence along the way.

I don't model myself on this guy but there are similarities. My antics in the market place were often akin to Caravaggio's pointless brawls and arguments, usually ending with me the worse for wear and filled with gloomy self-loathing. By the time I started this blog I felt I had a much better control of my emotional trading faculties, but just as Caravaggio was left badly wounded after he fought and killed Ranuccio Tommasoni in a knife-fight in Rome, I too was left with permanent scars from these pointless battles. These tumultuous events were pivotal in both lives. The artist had to flee to Naples as the authorities in Rome had put a price on his head (a pena capitale). In my objective mind I knew my days in the trading arena were numbered, but I tried to run from this reality. Caravaggio the artist continued to paint. I continued to trade. The lives we made for ourselves caught up with us both.

The desperate search for redemption is another tie that binds. Caravaggio, somehow hearing that Rome was likely considering granting a pardon, made his way back to Chiaia in Spanish Naples, where it his thought his first patroness may have been able to help in influencing the papal authorities in Rome to issue to the pardon on his behalf. Alas, it is here that the artist was so brutally attacked and mutilated by unknown assailants that word spread of his death. In Simon Schama's 'The Power of Art', Schama notes that Caravaggio stayed in Chiaia and kept painting. He says of these paintings they 'were images of redemptive suffering and, yet again, decapitation, as if he couldn't get the image of his own pena capitale, his capital sentence, out of his mind.' My brush with death came this February, and it was a dangerous one. My self-loathing hit a new high, made worse that the fact that my capital sentence (a shortage of capital) was of my own making. I equated redemption with getting back to break-even - this would be my pardon from Rome - but I now realise that it is not here that redemption lies. It lies in being true to oneself and stopping now.

[PIC : David with the Head of Goliath, 1610]

{kind=link}

It is during Caravaggio's time at Spanish Naples that he painted David with the Head of Goliath, pictured above (2). The painting is widely thought to be a form of double-self portrait; at the very least the decapitated head is surely Caravaggio's. As with almost all art, the exact meaning of the piece is open to interpretation but right now the message that resonates with me is one of a deep understanding of the self, of the idea of redemption by making a clean break of the troublesome Caravaggio of old, and lastly, there is a heap load of self-loathing (see David's disgust with what he is holding). Schama says of this painting, 'You see something that had never been painted before and would never be painted again: a portrait of the artist as ogre, his face a grotesque mask of sin', describing the young slayer of the giant Goliath as the 'most conflict ridden David ever to be imagined in either marble or paint.' I can relate. There have been times when I felt like David and the market was Goliath, and other times when the market seemed the true David and I the ogrish Goliath, but the long standing truth is closer to idea of the double self-portrait, that I am both characters, and that today I officially severed the wicked head of my alter-ego (3). There will be no more half measures.

Rebirth denied - Caravaggio met with a tragic end. Still seeking redemption but now with a pardon apparently on the way, the artist boarded a boat for Rome, taking with him a collection of paintings he intended to give to people of influence and win favour. However, when the ship pulled in at the port of Paulo he was arrested for unknown reasons. By the time Caravaggio got out of jail the ship had sailed off with his paintings still on board. Some think that Caravaggio actually saw the ship sailing away and that, in a frenzy, he gave chase. What we do know is that Caravaggio made it as far as Port Ercole but there he collapsed on a beach with severe fever. In this pitiful state, he was taken to a local hospital where the troubled artist died. So near and yet so far.

As with Caravaggio's near redemption, my ship has also sailed (4). In the place of the important payload of valuable paintings are valuable trading secrets that could lead to success in the market. These are the product of several years of relatively intense trading and they will stand me in good stead when and if I ever return to trading with a reasonable level of capital. Of course, they are not secrets of the 'key to riches' variety, simply crucial lessons that I noted from my experiences trading the markets. My full-time trading career is over. I still plan to trade in extremely small size, seeding my two trading accounts with £500 each, but this is only to maintain an active in the markets until the day I am ready to return, if ever.

[PIC : Saint Jerome in Meditation, 1605]

{kind=link}

These introspective paintings of Saint Jerome and Saint Francis touch on ideas of contemplation of the self, mortality, and man's role in relation to the world. It is apt to end with a famous quote by Socrates:

'The unexamined life is not worth living.'

The End

(1) Later Rocky films address this issue, with the writers giving Rocky Balboa permanent brain damage as a direct result of the thunderous blows delivered by Ivan Drago. Rocky also experiences a humbling of his financial status that forces the boxer to give up his extravagant high-life and return to his old neighbourhood.

(2) Wikipedia observes the letters H-AS OS inscripted on David's sword, an abbreviation for the latin phrase 'Humilitas occidit superbiam', or 'humility kills pride'.

(3) The non-Caravaggio me lives on here.

(4) Given my chosen trading name of Caravaggio, the question of whether I subconsciously expected this fate hangs over me. Fortunately I don't delve that deep.

Steve Leslie writes:

Your insights are exquisite and insightful and express feelings that all of us who have been at this for any extended time have gone through. Although your trading may take a hiatus (I suspect you will be back) I hope you continue to write on your lessons learned and share on this website. It takes a very special person to admit defeat but all of us have done so in our trading lives. One of the central themes of Stallone characters is the underdog who withstands great odds against him and finds the character to endure rebuild and ultimately vanquish the foe. It closely parallels his personal life in many ways. I look forward to more postings of your marvelous vision going forward. We here have much to learn from you.

Oct

3

Cost of Living Over the Centuries, from Stefan Jovanovich

October 3, 2008 | Leave a Comment

Being too lazy to find out on my own and, therefore, that much more curious about the answers, I repost this past exchange by Yishen and Kim in the hope that they may have further thoughts on the subject. How much, I wonder, has the cost of lodging changed over the centuries and in the recent slump for an unskilled laborer? I can provide one factoid: for the unskilled laborer without papers here in the SF Bay Area the price of housing - i.e. sharing a bedroom with 3 other laborers in a ranch house in the non-posh suburbs - has gone down by 30-40%. House rents have slumped badly as the supply of tenants has fallen even faster than housing prices (the decline in remittances from the U.S. to Mexico is a lagging indicator of this trend.)

Yishen wrote:

I recently took a look at cost of living in 1700s London versus 2000s New York City.

I took the approach of figuring out how much of each item could an unskilled worker consume a year based on his salary and the price of goods then.

For instance, an unskilled laborer could purchase 511 lb of bacon in 1700s London with his annual paycheck versus 4122 lb of bacon in NYC today.

There's a lot of detail one can get rigourous about (like correcting for various taxes) and a lot of assumptions about prices, so I don't think the numbers I cite contain much (or any) precision, however the magnitudes of improvement should tell the right story:

Item 1700s 2000s Postage 80 miles 1872 83324 Coarse Soap, 1lb 3744 5833 Beer, 1qt 1404 3888 Barber visit 936 1167 Butter, 1lb 624 5833 Bacon, 1lb 511 4122 Mail, London-NY 468 41662 Steakhouse dinner 468 583 Candles, 1lb 165 1458 Coffee, 1lb 94 1326 Tea, 1lb 62 1750 Simple dinner 899 1167 Ticket 45 93 (Handel's messiah vs Madonna's latest tour)

Our average Joe benefited the most in communication anywhere from 40 fold to 90 fold greater consumption.

Agricultural goods came next, some 10 to 30 fold for tea and coffee, 8 to 9 fold for processed goods like candles, butter and bacon.

Finally, a trip to the barber didn't change all that much in terms of affordability for the average Joe.

Kim Zussman replied:

By any measures standard of living (i.e., real wages/real cost of living) has improved dramatically since the 1930s. Just check any data source (government conspirators), and you will see that with improved productivity and agriculture, this is true over time in most periods.

However it is still possible, with 2006 dollars, to eat for less than $20/week:

Source .

Oct

3

WSJ Medical Article Parallels Current Economy, from Riz Din

October 3, 2008 | 1 Comment

The WSJ has an interesting article titled 'The Body as Bacterial Landlord' discussing the Nobel winning finding that it is not stress that causes stomach ulcers but the bacteria Helicobacter Pylori. Widespread use of antibiotics did lead to a significant decline in the ulcer rate but there seems to be a whole bunch of unintended negative consequences. These include increased rates of allergies, eczma, hay fever, gastric reflux and esophageal cancer. Microbiologist Dr Blaser suggests that in our eager efforts to stay clear of bacteria we may be forgoing the various protections they have provided us over hundred of thousands of years of evolution. The article emphases the idea of a co-evolution with these little critters and that we may need to adjust our mindset of viewing bacteria as harmful. On a positive note, research in this area seems to be flourishing and it will be interesting to see what we learn in the years ahead. The article concludes with: "They live with us, and they are part of us," says Dr. Chervonsky. "That does not mean there is no tug of war.".

When I read this I couldn't help thinking about the financial markets and wider economy as a similarly complex system and how recent measures by governments, particularly the ban on short selling, is the sledgehammer equivalent of the application of antibiotics in that it severely hinders a tug-of-war co-existence that has a long run benefit to the system itself. As for the the unintended consequences, off the top of my head: in the UK, the nationalised bank Northern Rock has experienced the opposite of a bank run as depositors rush to a bank fully backed by the government; Ireland has a 100% guarantee on deposits, and this risks an escalation of protective measures through the world as money heads to where it is most safe; why should banks lend to each other when they can get risk-free funding from the seemingly endless billions that are being pumped into the overnight markets by the central banks (I'm not surprised the TED spread is where it is with this kind of distortion); when the Fed announces massive bailout programme, the banks must surely be incentivised to stop trying to fix the problem themselves (raise capital, face the pain, etc) as they know a massive buyer is about to come to the market. It's a complex system and we are fudging our way through by swinging sledgehammers in every direction. I know something has to be done, but I don't like what I see.

Oct

2

Abandon All Hope Ye, from Nigel Davies

October 2, 2008 | 1 Comment

It's good to see that at least someone's enjoying himself. Which reminds me of the vultures in the kid's movie 'Ice Age: The Meltdown'. Some quotes:

Lone Gunslinger Vulture: [singing] Food, glorious food / We're… anxious to try it!

Traffic Vulture: [giving "traffic report"] We've got an overturned glytpodont in the far right lane, traffic backed up as far as the eye can see. Lone Gunslinger Vulture: Ooh, and it looks as though there may be a fatality! Lone Gunslinger Vulture: [pause] I call the dark meat!

Lone Gunslinger Vulture: Look around. You're sittin' a bowl. Bowl's gonna fill.

Lone Gunslinger Vulture: It's real alright, and it's comin' fast. I mean look around, you're in a bowl, the bowl's gonna fill up, and no way out. Unlesss you can make it to the end of the valley. There's a boat, it can save you.

Lone Gunslinger Vulture: Y'all better hurry, grounds melting, walls tumbling and rocks crumbling, survive that, you'll be racin' the water. In three days time it's gonna hit the geyser field. Boom!

Lone Gunslinger Vulture: There is some good news, though. The more of you die, the better I eat. I didn't say it was good news for you.

Oct

1

Concussions are Suspected of, from Russell Sears

October 1, 2008 | Leave a Comment

This reminds me of a "survey" that I heard of so many times with a different twist I believe it is an urban ledgend in the Olympic sporting community.

This reminds me of a "survey" that I heard of so many times with a different twist I believe it is an urban ledgend in the Olympic sporting community.

Many promoting stricter drug regulations in sports would say something like a survey of ____ athletes were asked if they would take a pill that would guarantee them a ___ but would cause them to die a painful death 5 years latter, and 95% said "yes". The blanks would be filled in by High School/College/elite athlete an championship ring/gold medal.

The gist was that young people are too competitive and foolish to make those decisions for themselves. And while I agree with Scott that as a parent these decisions of momentary glory versus lifelong debilitating risks should be left to a mature adult.

The parent should also prepare kids to make these decisions for themselves.

Perhaps my soul-searching answer to that legendary survey would help parents accomplish both objectives.

Rather than question my dedication, sacrifice and risks taking even to the point of debilitation or death for distance running, it made me question my definition of "success" and what my goals ultimately were that I was willing to go to such extremes. In other words if your goals are not broad and high enough that you are willing to die for them then your definition of success is too narrow and shallow.

And while I enjoy the company of those few willing to make such great sacrifices and take such risks in pursuit of excellence and high glorious goals, those fewer amoungst these that I enjoy most are those that have a similar broad definition of success.

Oct

1

How To Buy Toxic Mortgage Paper? from Charles Pennington

October 1, 2008 | 6 Comments

Mark Cuban was on one of the business channels last night promoting the idea that all the toxic mortgage backed securities be rolled up into a giant publicly traded ETF. I'd have to guess that with so much forced selling, the most distressed mortgage backed securities must be good buys, yet there doesn't seem to be any vehicle for regular folks to participate. Is there something out there that I'm missing?

Mark Cuban was on one of the business channels last night promoting the idea that all the toxic mortgage backed securities be rolled up into a giant publicly traded ETF. I'd have to guess that with so much forced selling, the most distressed mortgage backed securities must be good buys, yet there doesn't seem to be any vehicle for regular folks to participate. Is there something out there that I'm missing?

Rocky Humbert offers:

I like these two closed-end funds: HSM (Hyperion Strategic Mortgage) and HTR (Hyperion Total Return). They are both at steep discounts to their NAV, they are managed by Lew Ranieri (the father of mortgage backed securities… Liar's Poker, etc.), and they have quality assets which have been dragged down by the sector collapse. If you are looking for true toxic waste, then consider RMA, RHY, RSF and RMH. These closed-end funds were previously managed by Morgan Keegan, and Lew Ranieri agreed to manage them after the meltdown (and lawsuits).

George Parkanyi adds:

UYG on the Amex — the ProShares 2x Financials ETF. It is loaded with US financial companies, which in turn are arrayed with every imaginable kind of toxic debt to suit your fancy. It’s not a toxic debt pure-play but if you can move past the token deposit-taking and convential-lending distractions, these guys have simply astonishing toxic debt franchises.

Oct

1

Why? — I Just Don’t Know, from Anatoly Veltman

October 1, 2008 | 10 Comments

1. At 11:09 this morning, E-mini stopped her collapse — just as she bottomed at 1143.75 = 50% retracement of 1112->1175.75; why — I don't know…

1. At 11:09 this morning, E-mini stopped her collapse — just as she bottomed at 1143.75 = 50% retracement of 1112->1175.75; why — I don't know…

2. Today's US collapse initiated from 1161.75 pinnacle, where she retraced 38% of 1175.75->1152.75 earlier decline; why — I don't know…

3. Yesterday's closing bell terminated the unprecedented single-session rally 1112->1175.75 just short of 38% retracement of 1291.25->1112 seven-session drop; why — I don't know…

4. Yesterday's European slide 1154.5->1132 reversed up from 50% retracement of Asian 1112->1154.5 rally; why — I don't know…

5. That Asian rally reversed at 1154.5 = 38% of the preceding crash day 1221.25->1112 drop; why — I don't know…

6. The crash initiated after down-side reversal from 38% retracement rally of preceding Sep19->Sep24 decline 1291.25->1180.25; why — I don't know…

7. The 1291.25 limit-up pinnacle terminated record two-session rally 1136.25->1291.25 at 50% of EPZ entire summer's bear move 1443.5->1136.25; why — I don't know…

What's all this nonsense with E-mini futures?

And why did the two panic single-session Dec Bond rallies on Sep29 and Oct1 terminated at 62% of the way to preceding high? - I just don't know…

« go back —Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- Older Archives

Resources & Links

- The Letters Prize

- Pre-2007 Victor Niederhoffer Posts

- Vic’s NYC Junto

- Reading List

- Programming in 60 Seconds

- The Objectivist Center

- Foundation for Economic Education

- Tigerchess

- Dick Sears' G.T. Index

- Pre-2007 Daily Speculations

- Laurel & Vics' Worldly Investor Articles

{kind=link}