Apr

15

Game of Life (Excel Help), from Gordon Haave

April 15, 2007 | 4 Comments

The Game of Life is like the real thing. It gets complicated over time. I bought it to play with my daughter, and it is a lot different than the one I played as a kid. Now, there are various careers, which creates a bit of complexity.

The Game of Life is like the real thing. It gets complicated over time. I bought it to play with my daughter, and it is a lot different than the one I played as a kid. Now, there are various careers, which creates a bit of complexity.

The worst aspect, however, is that they have functionally removed the "buying a house" angle to the game. Although I have not done the math, it would appear that the expected return for most of the houses is negative. Perhaps for one or two of the better houses (different kinds of houses is also an addition to the game) the expected return is slightly positive if you don't buy insurance, but with the risk of a massive loss. So, I just don't buy houses ever, and my daughter seems to have figured that out as well.

Some of the careers pay off depending on what number is spun. For example, if you are the artist you get 10,000 every time the spin is "1". Also, one can buy stock. Each stock certificate has a number on it, and whenever that number is spun, you get 10K.

This necessitates everyone paying attention to what number is spun, which causes arguments because people forget to ask for their money, and then someone else says "too late, etc".

Adding to the mix is that the spinner has apparently been outsourced to China, and is a piece of garbage. It is near impossible for a kid to spin without it spinning off of the track, getting stuck, etc.

So, I have a little excel sheet (really open office) that does a few things. First, it is a 1-10 random number generator, so instead of spinning the wheel, one hits F9. Next to that is a 100-100000 random number generator. This is a control number that makes it clear if when you hit F9 you got the same number again, or you hit F8 or something by accident and in fact did not "spin".

Also, I have a little matrix where I put in the numbers that people need to keep track of, like their stock certificates, and it flashes "pay Gordon" or pay whoever's number comes up.

Here is the help I need:

One of the careers is the entertainer. He starts out on a low salary scale, but if two 8s, two 9s, or two 10s are spun in a row, he "hit's it big" and gets a higher salary.

What is the best way in Excel (anything in Excel I can translate to open office) for tracking when two 8s, two 9s, or two 10s have been drawn in a row? It should be simple, but once I sat down to do it, I could not recall ever having to have the computer remember a previous random number. Any thoughts?

Apr

12

Deception, from John De Palma

April 12, 2007 | Leave a Comment

A recent NY Times op-ed reminds me of your Junto remarks last Thursday about how insider buying can transmit a deceptive signal. Daniel Gilbert's op-ed has some examples of other potential false signals. Gilbert wrote:

A recent NY Times op-ed reminds me of your Junto remarks last Thursday about how insider buying can transmit a deceptive signal. Daniel Gilbert's op-ed has some examples of other potential false signals. Gilbert wrote:

"In an advertising campaign that began last week, Nissan left 20,000 sets of keys in bars, stadiums, concert halls and other public venues. Each key ring has a tag that says: "If found, please do not return. My next generation Nissan Altima has Intelligent Key with push-button ignition, and I no longer need these." …There is no selfish reason to bend down and pick up a key ring, but Nissan knows that we will bend without thinking because the impulse to help is bred into our marrow. Our best instinct will be awakened by a key ring and then punished by a commercial. Like rubes throughout the ages, we will be lured by a false cry of distress and quickly cured of our innocence and compassion. We are used to commercial tricks that play on our fears. The official-looking letter marked "Verification Audit" is actually a magazine subscription renewal form; the credit card company's ominous call to "discuss your account" is actually an attempt to sell new services…"

Gordon Haave adds:

The biggest investment disaster I have been a part of was Edison Brothers Stores, which went to zero. A couple of months before it went under, all the directors bought some shares on the same day. After the fact, it was clear that it was doomed when they purchased. It was a clear head-fake.

Apr

7

The Wrong Tools for the Job, from Gordon Haave

April 7, 2007 | 1 Comment

Richard_Petty_Photo.jpg) Last weekend I did the Richard Petty Driving Experience in Forth Worth After a tiny bit of training, eight laps around Texas Motor Speedway.

Last weekend I did the Richard Petty Driving Experience in Forth Worth After a tiny bit of training, eight laps around Texas Motor Speedway.

I am glad that I did it, but I would not do it again. It's very inefficient. Basically, for 20 minutes of action (including suiting up, getting latched in, learning and then forgetting all the things to do if the car catches on fire), you wait around for 3.5 hours or more. It is such a popular product that they just herd people into every class and make you wait, rather than trying to make it more efficient.

In the markets, people often use the wrong tools for the job, often due to habit and the lack of acceptance of new ideas. In the consulting industry, this is common. Consultants operate the same way that they did 20 years ago. Now, they won't say that. Every two years they invent a new ratio that they apply to past performance and claim that it is an important breakthrough. Nevertheless, in my time, I was the only consultant who actually used factor analysis and systematic statistical techniques to separate beta from alpha. I think this is because I started on the hedge fund side, so when I moved to consulting I looked at the tools and thought "these aren't the best tools for the job."

Anyway, the simple fact is that the steering wheel is the wrong tool for the job. This might sound strange, but bear with me: Normally in a car you might hold the wheel at 10:00 and 2:00. We were told to hold at 11:00 and 5:00. Why? Because the car only turns left, and by holding at 11:00 and 5:00 you never have to roll your hands over. My first thought was, "Rather than using a new tool, they changed the way they use the old tool!"

I found that driving is actually quite physical. I had always dismissed it when the NASCAR announcers said so, but I was wrong. It's quite tiring to constantly pull the wheel hard to the left, particularly as the G-forces rise (my top speed was ~140 mph). You have your arms extended about half way in front of you as you are yanking on the wheel.

Thinking about it later, the wheel is simply the wrong tool for the job. Old bombers use a wheel because they don't engage in physically exerting maneuvers, yet a fighter plan will use a stick. Think of passengers' cars as bombers, and stock cars as fighters. For the physically exerting maneuvers, it would be much less taxing to have a flight stick lower and in front of you than a wheel up high. If you had a flight stick, it would be much less tiring, and would free up a lot of attention and dashboard space for mirrors and understanding your surroundings.

From James Lackey:

The Petty Driving Experience is only a quick ride. The anticipation is half of the fun. The smell of racing gas and burnt rubber, the roar of the engines, the butterflies before taking the wheel is all the fun. Run any 50-lap racecar driving school. Two each ten lap warm-ups then a 30-lap draft run. On lap 27, the heat, the stress had me say "get me out of this thing."

The physical strength it takes to turn the wheel of a car or slam on the brakes is all in the mechanical systems. A stick on an airplane is a full computer controlled hydraulic system. In your passenger car, with traction control, computer assist and anti lock brakes coupled with hydraulic assist power steering and brakes makes for an effortless drive. Rules and restrictions in racing keep the tech low. The reason often stated is to keep the costs down. Yet the real reason is to keep the drivers input relevant. New technologies make some forms of racing basically a remote controlled car, with a human along for the ride. The reason a racecar is hard to steer is so you can feel if the tires start to lose traction, to correct before a crash.

In the glory days of racecars, the 1960s, technology had not yet made drivers irrelevant. It was easier to make more horsepower than the traction of the tires and the track could hold. A driver needed the ability to control the engines power to control the car. Nowadays everything is restricted by either rules or computers. The worst is the bureaucracy of racecar sanction rule makers. A good result may be achieved by restricting engine size alone. Let all things in the car be unlimited, besides cubic inches.

Trading has seen the same technological advances that make individual traders as relevant as racecar drivers today. We all have a friend that scales in and out of the market using size, time, average range and price. When you point out that they could just as easy program a computer to do the job, they point out that every year is different; the markets constantly change. They can do a better job on the fly then a pre-programmed box.

Market rules seem to restrict technology. Years ago we had limit down rules. The old excuse was in 1987 computer program trades crashed the system. Funny thing since we removed the tight limit down rules, smart traders can't save the market from stupid computers and limit down opens. It's remarkable how much profit I have lost as a trader since that rule change.

Boy, was I happy after the fact on that down 500-point day a few weeks ago. No, not at all happy for the 5th day down being a 500 pointer, I was pleased to see that computers were blamed for the malfunction. We need humans in the markets. My kids need me in the market with the ability to profit. That is a much more honest answer than that the NYSE needs the specialist system to remain intact for public benefit.

When I was a little kid in the late 70s it not only took a fortune to make a drag race car run 8 flat in the quarter; it took knowledge. Money alone could not buy a fast car. The knowledge was not readily available. A few years ago I built a car for less than half of what it would cost 20 years earlier. The first day out the car ran with in 8% of perfect. On paper the car should have run 7.97 seconds at sea level. With in a couple weeks we had the car run 98% of perfect.

Yet in my class, super comp, I would guess that some 3,000 cars in the country run 99.9% perfect and any given race. A few cars have a perfect run down to the 10,000th of a second. Most of that ability to run the 99% of paper perfection is new technology. Yet that last one percent is knowledge. Let's put it this way, you can run your car with in one percent of potential and count on a loss the first round of competition.

In the markets we do not have to compete. We can in theory just buy the market and match the return. Lets call that trading not to lose. At races when conditions are good, to win you need to be with in 0.006% to win. The other day some one mentioned it was a stop run at 1424. A two-point drop on that stop run translates into only a bit over a tenth of a percent. That is tight competition.

A real stop run was last Feb when we broke down 2% on the day; the market dropped 20 more handles in an hour. After many sessions of not having a down one percent day, many were set for tight trading. In racing that would be a nice sunny summer day of practice, then rain and a 50-degree change in the temperature. The best racers have the ability to change set ups quickly.

After heavy weather, the cool air and low humidity, racecars or trading accounts, make much more power. After a big fall in the markets, the intra day moves can be wild. After the big cold front came through in Feb, if you revved your account to 5,500 rpms, dumped the clutch at the open you blew the tires right off your account.

Perhaps it is not the tools for the job, just the calibration. After the huge down it took weeks for risk mangers and funds to adjust. Two days after the fall traders adjusted and were making more than the weeks prior on half the size. If the markets can drop 50 again, they will move 20 points on any given day. It's much easier to make 8 points on a 20 point day than to make the entire 8 point range months prior, unless your investing.

Once conditions become stable at whatever temperature and pressure it becomes much harder to win. In low temperatures engines make more power. Once the car is set up to run at the increased power speeds will increase. It's the same with the markets and absolute daily returns. The problem is taking it easy until the weather and the markets become stable. You can easily crash your account. Yet once conditions are stable, everyone has adjusted, the new problem is being very aggressive with your set up.

If you are too conservative when the conditions are great a rookie will blow you away. That is to say a rookie with a good computer. It's remarkable how quickly the markets adapt vs. just five years ago.

Apr

4

Coffee, from Jim Sogi

April 4, 2007 | 2 Comments

The best coffee is Arabica. You guys drink the worst coffee. I'll bring some good Kona stuff out when I come next.

The best coffee is Arabica. You guys drink the worst coffee. I'll bring some good Kona stuff out when I come next.

I got a sampler of eight different international coffees with the new iRoast 2, in green bean from Mexico, Peru, Timor, Sumatra, Congo, Panama, Nicaragua, Guatemala, and a few others. I'm not sure if it's what they're trying to sell or just trying to get rid of, but none held a candle to fresh roasted homegrown hand-picked sun dried Kona Coffee. Most were bland. Peruvian was about the best of the bunch, but still rather bland. Some were close to undrinkable. Sumatra tasted like dirt, Panama very bland, Nicaragua very bitter, and Peru mellow, good to mix 10% with 90% Kona.

Sam Humbert asks:

Why does anyone voluntarily drink "flavored" coffee? I'm having a cup just now, because "hazelnut flavored" beans were all we had on hand in the office today. But I feel like the high-school stoner who's so desperate he'll smoke roaches. The stuff tastes like something the EPA would send HazMat-suited guys out to Jersey to detoxify.

Who buys it? Is it a ladies' drink? Would appreciate insight.

Yishen Kuik adds:

A coffee importer once told me that the flavoured coffee industry grew out of a desire to use cheaper robusta beans and yet avoid the inferior aftertaste that caused manufacturers to prefer arabica. But then flavoured coffee took off.

J T Holley writes:

Having earned and financed my college education working at various coffee shops such as Mill Mountain Coffee and Tea in the Roanoke Valley, and Food For Thought in Missoula, MT, I can tell you very few [buy flavored coffee]! Most coffeehouses have pots of coffee lined up on the counter of some sort for self pouring. The ratio to the best of my knowledge on refilling those was around 5 to 1 compared to regular coffees of many varieties.

Not that what you drank was good but there are two ways to flavor coffee. I have utilized both ways. One is with a horrible flavored oil and the other is via bottled syrup. The oiled way is to roast a rather cheap Columbian bean and then mix the oil and coat the beans (like applying chemicals to kill weeds). The other is much better and that is having an individual cup of coffee and adding a shot of flavored syrup. This seemed less toxic to me even though both are probably the same.

I witnessed very few people other than women that would order flavored coffee. Espresso drinks would be the exception to that. I would classify flavored coffee along the lines of 100 cigarettes. We used to joke that those extra long 100's were for people that like to ash not smoke. They don't smoke the cigarette they simply puff to be able to "ask" so they look sleek and sexy or something. Same with flavored coffee drinkers I've witnessed. They don't drink coffee like you and me, they sip and end up throwing half of it away in those plastic lined trash cans that weren't made to hold liquids!

My experience in the Navy taught me something about coffee as well. Cream and sugar were rarely added to a cup on my ship. Your sexual orientation back in the early 90s when I served was questioned if you had a stir stick in the cup. It was taunting or hazing thing on my ship. Words were slung at you in humiliating ways and made a man either quit drinking coffee altogether or go with the straight black cup of coffee to avoid the hassle.

It's amazing how psychological warfare works. I drank my coffee straight anyways so it wasn't a bother to me, but literally saw fights break out. Can't even imagine what would've come about if someone would have brought their own International Flavored Coffee onboard.

On a lighter note, I spent 6 to 8 years of my life roasting and serving coffee in all of its varieties. I have to confess that it is amazing how much caffeine is abused and that literal addicts consume the beverage. The mark-up on a cup of coffee from raw bean, to roasting, to brewing and serving is utterly amazing to me as well. The shops that I worked in did absolutely zero advertising as well, another fascinating fact of the coffee business.

Pitt Maner adds:

I hate to think of the abuse one might get for using the following, but based on a crude experiment it does seem that cold brewing makes for a smoother (some say lack of) taste.

With respect to Nicaragua there seems to be a fair amount of variability in the taste of the coffee. The best coffee growing region is up around Matagalpa and Jinotega in northern Nicaragua.

The Nicas seem to like to drink it black with a fair amount of sugar.

Problem with all coffee though seems to be how long it has been sitting on the shelf. You don't always get a "born on date" on the package. Of course you can pay $9 a pound for some of the brands that are sealed with nitrogen gas.

I know of someone who actually was marketing small discs that you put in your coffee maker to flavor the coffee of your choice. Better living through chemistry indeed.

Pamela Van Giessen writes:

The Irish coffee flavored stuff is the worst. My mother served it to me once when I was visiting. Being sleepy I didn't focus on the malodorous nature but the second it hit my taste buds I literally spit it out. Thankfully we were outside. I think that stuff was made for older ladies.

Scott Brooks writes:

Chicory is a plant that I use in my food plots to feed and attract deer and turkey. It is highly desirable, palatable, and nutritious to deer and turkey as well as many species of birds, and other assorted animals.

Gordon Haave adds:

I am a big chicory fan. The only kind to get is Cafe Du Monde. Every other kind I have tried is terrible. That being said, I don't know that it mellows the flavor, unless the underlying coffee is much more harsh than regular. I drink it with sugar and cream.

Mar

31

On the Coming Commoditization of Hedge Fund Strategies, from Henrik Andersson

March 31, 2007 | Leave a Comment

I believe hedge fund strategies will be new frontiers in the ETF market. As we are seeing ETFs move into more active strategies, we have already seen the beginning of this trend. The quantitative backdrop for evolution can be found in these articles by hedge fund Bridgewater, on selling beta as alfa and levering betas.

I believe hedge fund strategies will be new frontiers in the ETF market. As we are seeing ETFs move into more active strategies, we have already seen the beginning of this trend. The quantitative backdrop for evolution can be found in these articles by hedge fund Bridgewater, on selling beta as alfa and levering betas.

My prediction is that the increased accessibility will make it harder to prosper for hedge funds that are currently selling beta as alpha. In effect I see no reason why it couldn't soon be as easy to access some of these strategies as it is to trade the QQQQ today.

Gordon Haave writes:

Yes, but the whole point of the ability to replicate these funds is that you don't need the lockup, or at least not as much of one. One can short volatility without a 1-year lockup.

From Bill Rafter:

The largest portion of hedge fund money is employed in long-short. Long-short is highly liquid and highly scalable, and could easily endure a zero-day lockup. For example, we have a long-only (in theory, less liquid that long-short) large-cap program that has a zero-day lockup. One might ask why. Our answer is "marketing." Investors (particularly pros) are a lot less reluctant to give you money if they can get out on an instant's notice.

Lockups are really only necessary for strategies such as event-driven or distressed assets. The hedge fund industry mostly uses lockups to keep control of its assets. Recall how the recent ('06) Greenwich-based fund went guts-up and tried to manipulate its reports to shareholders to have the latter miss a redemption deadline.

Brian Haag adds:

If the funds are algorithmically managed, they are a short. Fixed systems die. If the funds are actively managed, they are a short. They will not attract the talent that 2/20 type arrangements will, and will thus be the mark at the table.

This whole "you can replicate any hedge fund strategy by adding beta and a few formulas" meme is no different from the "You can beat Wall Street at its own game!" type hucksterism so prevalent in the late 90s. It's just marketing crapola. While the base idea may be sound, that you don't have to get involved in hedge funds to receive average returns, so what? The only possible outperformance in products like these is relative to managers with subpar returns. It's all just another way for the industry to sell average performance.

Managers who do add alpha are very happy about this whole development. It's another source of edge. One needs to look no further than the "Goldman roll" in commodities to see an example.

Charles Sorkin adds:

I have been offered structured notes (intended to be re-offered to our customers) that pay interest based on the Tremont hedge fund indices. Depending on the degree of index participation desired, investors have the option to have total return floored at zero percent (principal guaranteed, like a bank note). Naturally, the secondary market for such a thing is limited, but it's still better than a hedge fund lock-up. Moreover, the issuer is generally an AA-rated large European bank.

Need to get more aggressive? Just buy 'em on margin…

Henrik Andersson adds:

Some of these structured products, which are particularly popular in Europe, are selling with a participation rate of 100% and no Asian etc. This is strange since it seems you get the put for free; but in these cases the cost of the option is most likely taken from the fees of the underlying funds.

Mar

31

Activist Funds, from Gordon Haave

March 31, 2007 | Leave a Comment

I used to work for my Dad's hedge fund. At peak we had ~300 million. We never considered ourselves an "activist fund" in the new sense. We were just money managers. Now "activist fund" is the new fad. When I was in college my dad sent me to wage a proxy fight at Ceradyne (CRDN). We frequently owned ~15% of companies, and were involved in this sort of thing.

I used to work for my Dad's hedge fund. At peak we had ~300 million. We never considered ourselves an "activist fund" in the new sense. We were just money managers. Now "activist fund" is the new fad. When I was in college my dad sent me to wage a proxy fight at Ceradyne (CRDN). We frequently owned ~15% of companies, and were involved in this sort of thing.

In the instance of Ceradyne it was somewhat of a surprise attack, but we had ~17% and another guy with ~5% was on board with us. The CEO knew we and the other guy were cheesed off. There was cumulative voting for directors at CRDN. So I show up at the meeting, I nominate the candidate. The vote is called, I show my proxies. The CEO didn't challenge them at all. Why? He knew. He knew how we felt, and he knew how the guy with ~5% felt, and he saw in my hand the proxy from the guy with ~5%. It wasn't that hard for him to know.

So when a hedge fund calls up and says others are with him, what do you do? Say, "I don't believe you unless you tell me who they are." Then you call them and ask them. It's not that tough. When I worked at Devon I knew the IR guys. They knew darned well who owned the stock and what they thought of management. That was their job.

Once, the unions were leading a big proxy fight against Avondale Shipyards (AVDL). The unions claimed big shareholders were on their side. So what did management do? They looked at the 13Fs, talked to the custodians to try to get ownership info, and they called the shareholders. It's not that hard, happens all the time.

Mar

30

I Would be a Great Fed Chair, from Gordon Haave

March 30, 2007 | Leave a Comment

I would be a great Fed Chair. I would just leave the money supply alone and never touch it. Now, some say that deflation is a bad thing. Why should it be? Wouldn't you like the prices of the goods and services you buy to go down?

The argument is made, though, that wages are sticky, and wages won't move down, so the net result is economic slowdown because wages are too high. Fine. If the economy is forecast to grow 4% this year, increase the money supply 4%.

Mar

30

Interesting Bifurcation, from Steve Ellison

March 30, 2007 | Leave a Comment

While oil goes above 65, agricultural commodities widely viewed as alternative energy sources fall, with corn near a 2-month low and sugar below the round at an 18-month low. What does this apparent schizophrenia portend?

From Gordon Haave:

As energy goes up, the price of that drill bit, and the price of moving that rig, etc. goes up. Drilling costs are up 100% in the last few years. This causes people to drill less, just as they would if they actually counted all of those inputs.

From Stefan Jovanovich:

The actual numbers for the rig counts over the past few years are rather different.

It is the spread that matters, not the absolute cost. The increased cost of drilling only cuts back on the rig count if drilling becomes unprofitable at the anticipated revenue from production. The difficulty with alternative fuels - like bike paths and free subways - is that their marginal costs are inflexibly high. None of them has the declining marginal cost curve that coal, oil & gas production still has. The costs (both in dollars and in gross energy consumption) of the fertilizer, water and mechanical energy to produce #X barrel-equivalent of corn or sugar-based energy are not significantly different from those for #X-1. (Neither are they for subway train or bicycle #x vs. #x-1).

For oil & gas and (to a lesser extent coal), the numbers are very, very different. I hate to quarrel yet again with James about transportation history; but he has it backwards. The evil oil companies and their customers built the roads in the United States. Three quarters of the paved roads in the United States were built after 1950, and they were funded almost completely by the taxes paid on gasoline and diesel fuel consumption. It was those same funds that have paid for and continue to pay the subsidies for mass transit as well as all Federal Highway improvements. It may be different in Hawaii, but the state contribution to road building here in California has been funded by state fuel taxes. As usual, the devil is in the counting details.

Mar

30

My Viking Beard of Sun and Fire, from Gordon Haave

March 30, 2007 | 1 Comment

I haven't shaved for weeks. The result is my manly Viking beard. You see, most men have difficulty growing nice beards — they are spotty on the chin. Not mine. Mine is a mixture of red, blond, and light brown. And it was even better back in 1997-2000, when my beard was soaked with sun, salt from the wind, seawater, and rum.

I haven't shaved for weeks. The result is my manly Viking beard. You see, most men have difficulty growing nice beards — they are spotty on the chin. Not mine. Mine is a mixture of red, blond, and light brown. And it was even better back in 1997-2000, when my beard was soaked with sun, salt from the wind, seawater, and rum.

Most people don't like beards in the business world, maybe because most people can't grow good ones, and their inferiority complex leads them to marginalize beard growers.

Roger Arnold advises:

W-2? A shave is due.

1099? You look just fine.

Mar

15

Managing Directors? from Justin Klosek

March 15, 2007 | 1 Comment

Brothel Discounts 'Matinee s-x' for Pensioners

Brothel Discounts 'Matinee s-x' for Pensioners

Mar 14, 2007 11:57 AM Reuters News Agency

BERLIN — A brothel in Germany hopes to capitalise on the growing number of pensioners interested in "matinee" s-x by offering them a 50 percent discount during the afternoon hours.

The "Pascha" in the western city of Cologne has introduced reduced rates for s-x sessions for clients aged 66 and above — provided they can prove they are old enough.

"All clients need to do is show us some proof of age," said a spokesman for the brothel's managing director Armin Lobscheid. "A 'normal session' costs 50 euros with us — and we're now paying 50 percent of that for these older guests."

"Life begins at 66!" it says in an advert for its "senior citizens afternoon" next to a picture of a motorcycle rider.

Brothels have Managing Directors? Wow, I bet those MDs at Morgan Stanley feel super-special now.

Gordon Haave replies:

And I'd bet the "talent" are all vice-presidents.

Roger Arnold queries:

How does this get accounted for in GDP? Is it a deflationary indicator or indicative of an increase in productivity? Are there any hedonic adjusters that need to be accounted for? Looks like free market animal spirits are beginning to reawaken in Europe!

George Zachar responds:

Simplistically, I'd say it would show up as a decline in productivity, as seniors will simply shift their s-x purchases to the earlier time slot, with the establishments earning only half their prior revenue per session. GDP would similarly take a hit, and assuming quality remains constant, this would show up as a price decline.

So look for Trichet, at his next press conference, to be asked about stag-de-flation.

Marion Dreyfus explains:

George's explanation is a wrong take entirely. The early bird special is income that would be extra, since these are men who would not be coming in at all, short of lowered price per assignation. These are men who are thus providing income in the slow early afternoon hours when nothing much else is happening. Since the wear and tear on the females is supposedly less (I don't know from experience what the difference is in men from 20s, 30s, to 70s, etc.) than from the younger males that give them a harsher workout, maybe the lower price is fair, since they are not working as hard for the money.

Thus it seems like a win-win, actually. Management is selling product in normally slow hours, and the clientele will be doubly pleased at low-priced but professional action and can get a workout without having to be especially nice to their wives. Or if single, they can feel manly again, despite not being able to date perhaps, at their age or with a paucity of date-objects around. And likely as not, some of the men will use the opportunity to simply talk, as a surrogate for therapy, and bloviate on topics they can't share comfortably with their wives or friends without censorious responses.

I think the whole thing a fit subject for a PhD, actually, when one considers all the ramifications.

Adi Schnytzer adds:

I agree entirely. This is very definitely a topic for a PhD in sexual economics, a field I will be delighted to pioneer if anyone wants me as a supervisor and who isn't scared of fieldwork. Marion's gritty microanalysis makes a lot of sense and an econometric analysis of the wear and tear caused by different age males on working females is long overdue.

Mar

14

“Speed Was a Contributing Factor,” from Gordon Haave

March 14, 2007 | Leave a Comment

I have written before about meaningless statements in finance, like "overdue correction." This sort of thing is not unique to finance, however.

I have written before about meaningless statements in finance, like "overdue correction." This sort of thing is not unique to finance, however.

Someone flipped his Mustang over the median and ran into a truck in Oklahoma City today. I am watching the news right now. The police say "speed was a contributing factor." Well, isn't speed a contributing factor in every automobile accident? How does one car hit another if speed is not a contributing factor? I suppose that if a car were parked precariously on the wall of a parking garage and the wind blew it off and it fell on to a car below that speed would not be a contributing factor, but that's about the only example I can think of.

What they mean, of course, is that excessive speed was likely what caused the accident, i.e., the idiot was doing 100mph around a turn and lost control. But if so, why not just say that?

It reminds me of the two years I spent on a federal grand jury (one or two days per month). A DEA agent was before the grand jury telling us about a drug bust, and he emphasized that the suspect had a "saleable amount" of cocaine.

I asked him what a saleable amount was. He said "He had X grams, and that is enough to sell." I said "But isn't any amount of cocaine a saleable amount?" He said "Well, he had X grams."

I said, "I understand, it's just that you didn't say that he had 'an amount' of cocaine. You said he had a saleable amount. I am trying to determine what the cutoff is for a saleable amount. If he had the tiniest amount on the eraser on a pencil, would that be a saleable amount"

He said, "Well, yes, you can sell any amount of cocaine."

And I said, "Well, that is my point, the phrase 'saleable amount' has no meaning, and you just use it for effect."

He started to say something, and then the Assistant US Attorney stepped in and stopped my line of questioning. Something also happened when I questioned the definition of "packaged for sale" when it comes to drugs. In short, unless it is scattered on the floor, it is packaged for sale.

Craig Mee replies:

I recently drove with my father. He has much driving experience, though he hadn't been on a highway for quite some time. With me in the passenger seat, he was tailgating cars at 100kph, not something he has normally done. The perception of distance and safety for him has obviously been impaired, as has sensing trouble with cars braking in front of him.

The relationship to the market is this: Having a good understanding of trading and knowing what needs to be achieved may be fine. But diminishing perceptions and feel for the market may interfere with results over time and might lead to a major disaster if not detected early.

My father also recently mentioned to me that life and death situations which he narrowly avoided in his youth, and did not think too much about at the time, had recently come back to haunt him in the shape of dreams and waking up in cold sweats.

Being on guard and aware of changes taking place is paramount.

Nigel Davies adds:

Consider how someone knows he's driving too fast. Speed tolerance varies greatly from one person to another. For me it's when I feel tired after the journey because of the stress. My body's telling me I wasn't fully in control. Of course, here in the UK there are so many speed cameras now that it is difficult to get so stressed without losing one's license.

Can this be applied to markets? Are constant feelings of market-related stress due to "lack of control" an important message from our bodies?

Sam Humbert notes:

From After the Race, in James Joyce's 1914 collection Dubliners:

The car ran on merrily with its cargo of hilarious youth. The two cousins sat on the front seat, Jimmy and his Hungarian friend sat behind. Decidedly Villona was in excellent spirits, he kept up a deep bass hum of melody for miles of the road. The Frenchmen flung their laughter and light words over their shoulders and often Jimmy had to strain forward to catch the quick phrase. This was not altogether pleasant for him as he had nearly always to make a deft guess at the meaning and shout back a suitable answer in the teeth of a high wind. Besides, Villona's humming would confuse anybody: the noise of the car, too.

Rapid motion through space elates one; so does notoriety; so does the possession of money.

Mar

14

Subprime Information and Real Estate, from Gordon Haave

March 14, 2007 | 3 Comments

Why is it whenever the government decides to protect us from market forces, we tax payers get the shaft? Would it not be better just not to interfere in the first place?

Financially it would be better to let the foreclosures happen. Not foreclosing on bad debts means the economy doesn't get to reallocate capital to its best uses. That, in short, was the cause of the 10-year recession in Japan.

If it is in the interest of the lenders to give people breathing room, they will do so without the government forcing them to.

Rich Ghazarian adds:

Not long ago, I was involved in building predictive models for sub-prime products for one of the major shorts in the market today. There was no way of predicting today's scenario, because a large part of the poor credit performance is due to fraudulent mortgages (loans originated on falsified information). Thus, most of the models are based on false historical data. For instance, a borrower with a Debt to Income Ratio (DTI) of 0.4 is now all of a sudden a borrower with a DTI of 1.4 … oops! It is interesting that this fraud was mostly conducted by "Loan Officers" and not the borrowers. Here is an example of quant models being useless!

Mar

9

This is very, very important. In previous career as a consultant, I reviewed hundreds if not thousands of pitches for "growth stock" managers. At least half of them had the same theme, some form of informal study about how accelerating earnings estimates, increases in number of analysts raising estimates, etc., had a positive impact on stock prices.

Because such numbers are easy to calculate, and because there are so many players playing that same game, I generally found it amusing that one would think one could make money in a strategy that is widely followed. If I prodded a manager on that, the response was always something along the lines of "well, but the numbers continue to work".

Well, now we know why "the numbers continue to work". The numbers are no good. Click for relevant article.

Mar

9

Once again, we see the common meme whenever there is a big down day. From various email lists, to chat boards, to news sites, and to TV, the commentary is all the same: What went wrong? This is usually followed by posts about how this or that system that is supposed to prevent the market from going down didn't work.

Never is there consideration that the movement might have been random, or that in fact the move was in fact an act of the capital markets efficiently pricing in new information.

Noticeably absent, of course, is the lack of "what went wrong" statements whenever the market goes up big.

Why? I offer two explanations, and the answer is likely a combination of both.

First, human psychology. It is well known that people tend to assign their winnings to skill and their losses to luck, malfeasance, someone's part, or a system breaking. Most likely there is a large issue at play regarding people refusing to view events logically when the event itself is negative. Perhaps Dr. Dorn could comment.

The other explanation is a mistaken view of the role of capital markets, specifically the stock market, in an economy.

The role of capital markets in an economy is, at its most basic, to serve as a meeting place for those with surplus capital and those with a shortage of capital. The primary market in equities consists of those with excess capital wanting to buy shares in companies who are in need of capital.

The secondary markets then serve to offer liquidity to those who purchased equity in the primary markets. The secondary market is critical to the success of the primary market. Without the liquidity of the secondary market, investors would take a liquidity discount on what they are willing to pay in the primary market.

In order to entice investors to invest in common equities, they must offer a risk adjusted return that is above other more secure investments. If there was no risk adjusted return, people wouldn't invest in the secondary markets, and thus people wouldn't invest in the primary markets.

For most of the century, the figure needed to keep the equity markets chugging along has been around a 10% annual return.

The pricing in the equity markets also sends resource allocation signals to the economy as a whole.

Now, most people don't see that as the purpose of the stock market. Most see the purpose of the stock market being "to go up." Therefore, when it goes down they think that something has gone wrong.

But, the purpose of the stock market is neither to go up nor go down. For it to serve its purposes, it must go up over time, but going up is not its purpose in and of itself.

In short, the market went down today. If you lost money, it is nobody else's fault but your own. If you made money, there's a good chance it was luck.

Janice Dorn writes:

In partial response to Professor Haave's insightful commentary, I have a several minute-long video which I made on January 24. 2007, discussing what is known as the self-attribution cognitive bias. If I am able to send it to the list, I will. Until then, perhaps this will be of some assistance, perhaps not.

Human beings are fragile as regards the whole situation of self-esteem. This is much more detailed than the small paragraph or two, but perhaps it captures some of the essence.

The human brain has many ways of protecting against assaults on the fragility of self-esteem. In psychoanalytic literature and much of the psychiatry literature, these protective tactics (which are, in large part, little or big lies we tell ourselves) are called defense mechanisms. In the language of behavioral neurofinance, they are called cognitive biases.

The self-attribution bias manifests as a tendency for good outcomes to be attributed to skill, and bad outcomes to be attributed to just plain hideous bad luck.

A decision matrix for self-attributional bias looks something like this:

GOOD OUTCOME BAD OUTCOME

Right Reason Skill ( or luck) Bad luck

Wrong Reason Good Luck Mistake

Among the questions that follow from this very brief discussion of self-attribution are:

- When are we lucky and when are we skillful?

- Are we right for the "right" reason, or are we right for some other reason.

- Does it matter, as long as we are right?

- How do we measure and "fess up" to mistakes, i.e. recognize mistakes as mistakes by taking personal responsibility and accumulating regret?

- Is it important to do this, and why?

- How do we learn from this and what do we learn from this?

- How important is it to learn from this?

- What about all the other cognitive biases and how they impact self-attribution?

The essence of the self-attribution bias is: Heads was skill, tails was bad luck, with all and every due apology to any long tails who may or may not be listening in!

Art Vandalay writes:

This article is two months old but very important in my opinion. It will be the main driver this year.

Mar

5

I Just Did a Linux Install, from Gordon Haave

March 5, 2007 | 5 Comments

I am not at all computer literate, so this might be useful to others who are not.

I am not at all computer literate, so this might be useful to others who are not.

I have generally not had problems with Microsoft. I have had no problems with WindowsXP and OfficeXP, although prior to the release of IE7, I thought IE6 was very poor. But I got around that by using Firefox and/or Opera.

Anyway, I find WindowsVista to be so outrageous that I have determined never to use it. My current laptop and wife's computer are WindowsXP machines, and I figure both have a two-year lifespan left. So I took an older Dell and installed Ubuntu on it. I totally wiped out WindowsXP, so I don't have two partitions.

The problem with leaving the Microsoft world is some of the applications. Now, OpenOffice actually seems to be pretty good. But I regularly use Crystal Ball, which is an Excel add-in. I suppose I could hope for it to be available on Linux in two years. But my question is, what do Linux guys do? How do they deal with the fact that most business software is Windows only?

Anyway, the install went quickly and there were no problems. It has sped up the computer compared to how it ran with WindowsXP. The multimedia packages don't have the codecs for mp3s, but a quick question about that to a message board got me the answers I needed.

I intend to use this computer frequently for the next two years as training for a planned ditching of Microsoft altogether.

Mar

2

Treachery, from Gordon Haave

March 2, 2007 | 1 Comment

McCain's Campaign Collapses

Dick Morris & Eileen McGann, Tuesday, Feb. 27, 2007

The John McCain candidacy, launched amid much hope, fanfare, and high expectations, may be dying before our eyes. Even worse, it may go out with a whimper instead of a bang. It may not end in an Armageddon style primary defeat, but just dry up from lack of support, money, or interest.

When Benedict Arnold moved to England, he discovered the English didn't like him, either. Nobody likes a traitor. The McCain hype was built on his disagreements with the GOP mainstream. Now that he has either turned back on some of those issues, or they are no longer issues, the GOP faithful still don't like him, and surprise, surprise — now that the Dems and the media have no use for him anymore, they don't like him either.

Feb

20

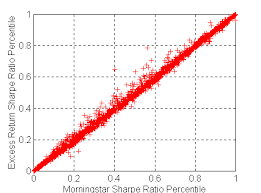

Analyzing Hedge Funds, Like Sharpe Ratios, from Allen Gillespie

February 20, 2007 | Leave a Comment

Is ROIC (return on invested capital) a viable alternative to measures such as information ratio, Sharpe ratio, etc.? It appears to me that even some of the marquee hedge funds employ a lot of capital in order to realize ordinary returns.

Is ROIC (return on invested capital) a viable alternative to measures such as information ratio, Sharpe ratio, etc.? It appears to me that even some of the marquee hedge funds employ a lot of capital in order to realize ordinary returns.

Should one be using net exposures or truly looking at gross exposures, or are there alternative measures that would be useful?

Gordon Haave notes:

The problem with ROIC is that it doesn't account for the level of risk the capital was exposed to in order to generate the returns.

Feb

17

Love It or Hate It, from Gordon Haave

February 17, 2007 | Leave a Comment

"One of the things I look for in DVD reviews on Amazon is extreme and opposite reviews. That is, where the DVD is completely loved by some and hated by others. With such a movie, the chances are that you too will either love it or hate it. However, if you are afraid of losing $15 on a bad movie, you will also miss the great movies. Examples of this are the reviews for the movie "The Thin Red Line."

For what it's worth, I think the movie is amazing. It just popped into my head that perhaps there is an application to the markets. Here it goes:

In my first job out of college, I invested in deep-value and distressed situations. Typically, nobody ever had mixed opinions on these investments. Anyone with any opinion on them typically loved or hated them.

From this came big losers, but big winners also. One could not, in my opinion, have had the big winners while also having some big losers. I considered the big losers to be the price of the big winners, and since so many investors won't pay that price, there is a fair amount of alpha to be had in those strategies.

Back to the Amazon reviews: Now that Wall Street analysts occasionally tell the truth and put out negative opinions on stocks, might a good way to screen for ideas to be to search on stocks that only have very positive and very negative opinions on them?

Perhaps this could be done using a measure of earnings estimates divergence (one would have to adjust for financial and operational leverage to compare estimate divergence across companies, i.e., a 30 cent divergence on a utility might say more than a 40 cent divergence on a tech company).

Feb

15

Empty Voting, from Gordon Haave

February 15, 2007 | 1 Comment

'Empty voting' ploy used by hedge funds is on SEC's radar By David Hoffman February 12, 2007

PHILADELPHIA — The practice of borrowing company stock to manipulate the outcome of company votes has piqued the interest of the Securities and Exchange Commission and has rekindled a debate over stock lending. In at least two speeches this year, SEC member Paul S. Atkins talked about the practice, which has been dubbed 'empty voting.'

If investor A doesn't care about the outcome of a vote, and investor B does, why shouldn't investor B be able to pay investor A for the right to vote investor A's shares?

This is in fact economics at its best. If investor B's voting harmed the long term interests of Investor A, then investor A wouldn't lend investor B the shares.

Feb

15

Last of the Mohicans, by Gordon Haave

February 15, 2007 | 1 Comment

I bought the director's cut of Last of the Mohicans. I have always found that film to be remarkably beautiful, both the scenery (filmed in the mountains of North Carolina) and the last 20 minutes of the film, particularly when Alice leaps to her death. Anyway, if like me you always wondered which of the Mohicans was last (the dad, or Hawkeye, the adopted Mohicans), it is settled in the directors cut. At the end of the film the dad proclaims himself the last of the Mohicans.

I bought the director's cut of Last of the Mohicans. I have always found that film to be remarkably beautiful, both the scenery (filmed in the mountains of North Carolina) and the last 20 minutes of the film, particularly when Alice leaps to her death. Anyway, if like me you always wondered which of the Mohicans was last (the dad, or Hawkeye, the adopted Mohicans), it is settled in the directors cut. At the end of the film the dad proclaims himself the last of the Mohicans.

I don't necessarily recommend the director's cut. It's really only an extra 10-15 minutes or so, and most of that is filler (the Mohicans spending more time running through the woods). The two notable scenes are the bit at the end when we find out which Mohicans is last, and there are 3 extra minutes or so at the siege of Fort William Henry, where major Heyward leads a column of British troops outside of the fort to fight the French and the Indians.

Feb

13

Excalibur, by Gordon Haave

February 13, 2007 | Leave a Comment

"I dreamt of the dragon."

"I dreamt of the dragon."

"I have awoken him."

"Can't you see all around you the dragon's breath?"

From one of the greatest movies of all time.

I watched the director's cut of Blade Runner, which is fantastic, and finally in this cut it becomes apparent that Deckard himself is a replicant.

Now, I am watching the movie with the above lines, where, interestingly, Patrick Stewart plays a role.

Feb

9

Accuracy and Precision, from Gordon Haave

February 9, 2007 | Leave a Comment

Accuracy and precision are conflicting traits in any forecast. Most market forecasters are completely inaccurate, is it because they are trying to be too precise? After all, what kind of forecaster would get paid if he didn't at least try to nail down next year's market return within 5%?

Accuracy and precision are conflicting traits in any forecast. Most market forecasters are completely inaccurate, is it because they are trying to be too precise? After all, what kind of forecaster would get paid if he didn't at least try to nail down next year's market return within 5%?

Perhaps more value can be added by drastically reducing the attempted precision, and so I offer the following:

The market gives 10% per year to those who are willing to freely accept it. This 10% includes big drawdowns such as 2000-2002, and fall 1987.

Therefore, if one could target precision of simply "is there a high chance of a 30% drop in the market", one could add a worthwhile amount of return to the 10% offered by the market.

The P/E ratio is probably the ratio that is most commonly used in inaccurate forecasts, but I give you the following:

I don't know which direction the market is going to go, and I don't know what will happen to corporate earnings.

I do know the following per the graph: Despite the strong bull market since 2003, the PE ratio is exactly where it was at the start of the late 1990's bull market. Combine that with the fact that the Earnings yield on the SPX - the 10 year yield is positive (and it was negative in 2000 and late 1987), we can perhaps safely assume that a negative 30% year is not in the cards, and therefore the expected return on the stock market this year is greater than 10%.

Feb

6

Underperformance, by Gordon Haave

February 6, 2007 | 1 Comment

I currently monitor how many managers beat the relevant indexes every quarter. It appears to be surprisingly cyclical. For 2006, most managers (defined by separate accounts in the PSN database ) underperformed the indices. In fact, in many categories only 20% of managers beat their indices. The issue, though, is finding an explanation for this. What is it about the average separate account manager that he underperformed this year?

I postulate trend following. Most managers outperformed in some prior years, and I wonder if perhaps a trend following instinct leads them all to be overweight in, say, oil compared to the indices, and then oil breaks and they all get hit hard.

I suspect the fund flow out of active managers differs from the fund flow into ETFs. If someone withdraws money from a manager who closely tracks the S&P 500 and puts it into an SPY, there will not be any change in the outperformance of managers vs. the index.

Perhaps, though, the ETFs are representing a total allocation that is different from all the active managers combined. Active managers must hold a significant, say, a few percent at least, of stocks that aren't covered by the better-known indices, and these holdings are hurting them.

This should be testable in various ways. For example, stocks that are more heavily overlapped in indices should be outperforming now.

Alston Mabry replies:

Portfolio-weighting may play a role, too, as it interacts with changes in the small cap/large cap cycle. Indices are cap-weighted, so in order to produce a return different from the index, a fund portfolio must move some distance away from the cap-weighted index, towards equal - or random - weighted portfolios. When small cap/midcap stocks are doing well relative to large caps, there's a greater chance that an equal/random - weighted portfolio will beat the S&P. The reverse is true when large caps are the best performers.

I'm conflating funds that would say they have different benchmarks (large, mid, small, value, growth); but I would think that the analysis holds up even when restricted to subsets of stocks.

Feb

3

Shilling Website, by Gordon Haave

February 3, 2007 | Leave a Comment

OK, it's been settled. We have found the winner for the influential financier with the most vague, yet still wrong predictions award.

OK, it's been settled. We have found the winner for the influential financier with the most vague, yet still wrong predictions award.

I was thinking of commenting on it line by line, but there are no good markers for how to separate the different ideas. It is one continual BS stream of consciousness. Notice of course that three of his predictions use the term "might," and how he congratulates himself for his predication that a renewed bear market in U.S. stocks might occur.

A year ago, Gary Shilling, in his monthly INSIGHT newsletter,

outlined his 6 investment themes for 2005.He said three of them were likely to develop in 2005

while three would maybe unfold last year.What made those six ideas stand out

was that they were not simply a rehash

of what most Wall Street analysts, economic forecasters

and other cheerleaders were saying at the time.In fact, all six were non-consensus and, therefore, could produce

significant investment rewards.

One year ago, Gary Shilling

1. predicted a rally in the dollar.

2. forecast spreading deflationary expectations.

3. said the yield curve would continue to flatten.

4. said the housing bubble might burst.

5. said a renewed bear market in U.S. stocks might occur.

6. stated that a hard landing in China might happen.How did things turn out? The dollar rallied. Deflationary

expectations spreading beyond autos and into appliance stores,

department stores, computers and recreational vehicles. The yield

curve flattened and, late in Dec. 2005, inverted. While the housing

bubble hasn't burst, that red-hot market has evidently cooled. While

U.S. equities didn't plummet like they did in the 2000-2002 bear

market, the Dow Jones Average last year was down while the S&P 500 and

Nasdaq registered only slight gains. And despite efforts to cool an

overheated economy without dumping it into a recession, China's

economy appears to be facing serious difficulties.Gary Shilling has often been way ahead of the crowd. [Read more here]

Jan

31

The Flawed Sharpe Ratio, by Gordon Haave

January 31, 2007 | Leave a Comment

Let's be clear that the Sharpe ratio is an extremely flawed measure. It makes perfect sense only in a purely efficient market. Otherwise, there can be plenty of ways to generate a good Sharpe ratio without really adding any value.

Take, for example, investing in timber or other forms of private equity (or like all the side pockets that hedge fund managers are doing these days) and then only marking the investments to market once per quarter. Voila! You can assign near zero volatility to your investments and get a great Sharpe ratio that you put in your powerpoint presentation.

Jan

20

Presentation of Predictions, by Victor Niederhoffer

January 20, 2007 | Leave a Comment

Sparked by an article on euphemism in politics, I have been studying the tendency of market participants and commentators to present themselves in a favorable light. The topics I have reviewed include the theories of boasting, euphemisms, biases in self reporting, self evaluation bias (325,000 entries), the superiority complex, the halo effect, and presentation of self in everyday life and deception. Nothing quite fits. However, considering that there are 132,000 entries for "as predicted" stock market on Google, I feel the topic deserves some serious consideration. Lacking theories or quantifications exactly on point, I'll have to take a crack at the subject myself.

My previous forays into this subject in Education of a Speculator started with the consideration of how the oracle of Delphi was able to maintain its prominent place in Greek life for over 2000 years. I concluded that the key was never to administer a forecast that could be falsified, maintain an impressive site and a mystical ambience, evaluate your forecasts yourself, deceive with the startling forecast when you already know the answer, and mix in Bacchanalia. I gave examples of market people who had adopted these principles and classified them as mystic (the secrets of pi), unappreciated (I stood alone in making the forecast), other worldly persons ("the parking lots are as empty as the ships in the harbor"), mathematicians (the lognormal distribution explains it), the traditionalist (the opera chairman, the palindrome and the abstract mathematician use my methods), the Washingtonian (I met with the Fed chair often), the correlation expert (soybeans traditionally fall before a rally in bonds), the loner (I am on an around the world cruise), and the Insider ("a bullet bid has been made").

My previous forays into this subject in Education of a Speculator started with the consideration of how the oracle of Delphi was able to maintain its prominent place in Greek life for over 2000 years. I concluded that the key was never to administer a forecast that could be falsified, maintain an impressive site and a mystical ambience, evaluate your forecasts yourself, deceive with the startling forecast when you already know the answer, and mix in Bacchanalia. I gave examples of market people who had adopted these principles and classified them as mystic (the secrets of pi), unappreciated (I stood alone in making the forecast), other worldly persons ("the parking lots are as empty as the ships in the harbor"), mathematicians (the lognormal distribution explains it), the traditionalist (the opera chairman, the palindrome and the abstract mathematician use my methods), the Washingtonian (I met with the Fed chair often), the correlation expert (soybeans traditionally fall before a rally in bonds), the loner (I am on an around the world cruise), and the Insider ("a bullet bid has been made").

I also reported favorably on the late Harry Browne's magnificent analysis of self administered reports. He gives repeated hilarious examples of "as predicted" that actually weren't the way they predicted. He also gives examples of pretended modesty in admitting a gap in accuracy that is designed to make you feel that the forecaster is so much more honest than you or I that he's a model of integrity as well as a genius. (Such a deceptive technique is particularly relevant today as the world's worst forecaster in my opinion, the weekly financial columnist, who has been consistently bearish on stocks 100% of the time while the Dow went up from 800 to 12,500 over 40 years, admitted in his January 22 column that he gave a terrible forecast in saying that oil would go to 70 before 50). "The only thing positive about that prediction was that it didn't take more than a wink for us to be proved wrong." This technique is also detailed in The Perfect Lie of distracting attention from the real deception (i.e. his grotesque record on stocks, while admitting the oil statistics to be wrong).

Such a typology holds up pretty well after 12 years, but I feel it misses the essence of all the "as predicted" ones. For example, it doesn't focus on the multiple prediction, the person who predicts so many things that he has to be correct on one of them. A beautiful example of the same, as it's so compact, would be the person that says "X is the key level" and then boasts about being right if it goes up or down from that level. Also missing is the retrospective forecast, the forecaster that lets you know that he was bullish well after the bull move has started. Another omission is the survival biased forecaster, the person that reports just the fund or stock results that are extant right now, leaving out the results of the funds that have folded, or less insidiously, just the years or the results that were completely unfavorable. Another omission is the academic forecaster (the academic who writes a paper uncovering an anomaly with almost a clarion call for funding contained in the retrospective low priced impacted data presented). Another more subtle fudger is the person who reports their results while the going is good and then hides ostrich-like in the sand when the going is bad. (I have used a variant of this in my own business where I was happy to report while I was making returns sufficient to win awards but stopped when the going got tough. All I can say in my defense is that I figured that if my future results were good, it would create less supply against me and more demand with me. If they were bad, why should I give my adversaries the platform on which to drive in the final nails?)

Here are preliminary suggestions for those who wish to present performance figures without undue boasting and hype:

1. All results should be presented with a view of providing the truth, the whole truth, and nothing but the truth, and should be accompanied by a statement to that effect.

2. Particular care should be made to present the results of programs and funds that are no longer in existence or no longer reported for any reason with which you are associated. For example, one should never report 40% a year returns on the one program or two programs that you still have outstanding if others, invariably involving much higher amounts of money under management, have been eliminated.

3. A complete enumeration of money contributed, money taken out, profits made, commissions taken out, fees taken out, and net to customers should be made by month.

4. A similar enumeration should be made for any funds the manager was associated with that are not included in 3. (for example, the biotech fund or the growth stock fund or the trend following fund in stocks that is no longer in existence)

5. All changes in style of investment, markets invested in, fee schedules and leverage used should be noted with a fair discussion of how this would change results.

6. Third party arrangements of any kind with selling groups or brokers or service providers should be enumerated by year.

7. The independent third party that reported and calculated these results should be noted and addresses should be given and auditors enumerated.

In addition to following the above guidelines where applicable, those who make forecasts should add the following:

8. The exact time and levels of the items being forecasted and what it is you are forecasting and how to measure what is being forecasted.

9. A complete enumeration of all forecasts made over the last five years with the information required in #8.

10. An assessment of the accuracy of the forecasts made in the past, with the bad forecasts as well as the good ones equally featured.

11. A measure of the a priori likelihood of the forecast being true due to chance factors alone, for example, the forecast that oil will be higher in the future would have a 100% a priori chance of being true.

12. The independent party, like Hulbert who has vetted your forecasts or advisories in the past.

13. The amount of self interest the forecaster has in what he's forecasting. For example, whether he has a position in the recommendation, did he front run, and what his policy is in extricating from the forecast with respect to his own positions.

No matter how carefully one develops a set of guidelines, it will always be possible to violate it in some way even when someone is not overly lax in presenting the truth, the whole truth, and nothing but the truth. As such, a letter from the forecaster describing any problems or gaps that the user might have in using the forecast should accompany the forecasts. For example, was the manager once managing a considerably larger set of assets? Has his organization changed now that he is a mere shadow (what used to be called a ghost in the stock markets of the 19th century) with a much smaller organization? Or have the financial circumstances of the manager changed so that he has an interest in a Hail Mary kind of prediction because he has been so devastated recently or as in the case of the weekly financial columnist, he's been short for so long that if he ever closes his trade, he'll realize a 1500% percent loss or so?

No matter how carefully one develops a set of guidelines, it will always be possible to violate it in some way even when someone is not overly lax in presenting the truth, the whole truth, and nothing but the truth. As such, a letter from the forecaster describing any problems or gaps that the user might have in using the forecast should accompany the forecasts. For example, was the manager once managing a considerably larger set of assets? Has his organization changed now that he is a mere shadow (what used to be called a ghost in the stock markets of the 19th century) with a much smaller organization? Or have the financial circumstances of the manager changed so that he has an interest in a Hail Mary kind of prediction because he has been so devastated recently or as in the case of the weekly financial columnist, he's been short for so long that if he ever closes his trade, he'll realize a 1500% percent loss or so?

These are just preliminary suggestions. Remember that even with perfect reporting, past results have little or no reason to be predictive of future results because of the problem of ever changing cycles, and ageing as described by Bacon. However, exceptionally bad past results would seem to be somewhat predictive to the extent that they usually result from excessive fees and grind paid to the house.

I would be interested in any augmentations or suggestions that the readers might make here that would improve reporting and predictive methodology so that the users will have a better backdrop for decision making.

Vic further adds:

What he wrote for Mr. Wiz and myself, which he considered his best book, was that "when a master seems to fall into a trap, be doubly careful." This is an extension of what the able Mr. Mee had in mind and I am sure that Mr. Grandmaster Nigel Davies will have a few apt comments on this point.

Vincent Andres comments:

Another omission is the survival biased forecaster, the person that reports just the fund or stock results that are extant right now, leaving out the results of the funds that have folded …

This reminds me of a scene in Groucho Marx's biography (hope not to confound). Groucho was negotiating a contract about an advertisement using his image. The man proposes Groucho $500. Groucho laughs and says no. The man proposes Groucho $5000. Groucho also says no. The man proposes Groucho $15000, and Groucho agrees. Then the man brings out of his pocket a $15000 check, already written.

"By the hell, how did you know I will agree at $15000?" asked Groucho.

Well, I have four pockets said the man. In pocket one a $500 check, pocket two a $5000 check, pocket three a $15000 check, and pocket four a $30000 check.

Aaaaaaaaaaaaaarg! said Groucho.

Sorry for the approximate English and certainly an approximate remembrance.

Hany Saad adds:

While this is a very valuable framework for thought and it definitely will give one a significant edge in markets as well as the proverbial "don't take things at face value," I suggest looking at the other side of the coin, which admittedly is less common but every bit as valuable in solving market puzzles. I am talking here about the money manager who only talks about his losses and how tough it is to manage funds yet one realizes at year end that he outperformed all his peers by a large margin. The money manager who always starts his speeches with "I am a smaller fish than I like to admit" or "what do I know" or "after a very tough year" or my all time favorite, "yes, finally a good one" in response to a congratulation over a trade so outstanding that it can no longer be hidden under the carpet. The money manager whose performance is so mediocre that he was debating retiring in his thirties and only stopped when he realized that this year could be a good year as well … so why not? The lessons are very valuable since this practice keeps the enemy away and prevents envy, or so goes the tale. The only problem with such a practice is that year after year, the adversary starts noticing your bluff, and as he's leaving your office after you utter your usual "yes, finally a good year," you hear him murmur invariably "yeah, right."

It is mind boggling how people learn so quickly that you are laying low, but they hardly ever call your bluff when you practice your shameless grandiose on them a la Ableson.

Gordon Haave offers:

The most common euphemism that I noticed was the naming of every downturn in almost any asset price as a "correction." One of the reasons that I find it notable is that those who call it a correction invariably are implying that the long term trend is still up. Well, if the future price will be higher, then why is having it go down today "correct" in any manner?

A good example of this would be today's bloomberg story about Rogers saying that the downward movement is just a "correction" and that the price will later go up to $100. If the price is going to $100, then any significant downward movement is not a "correction." Rather, it is a "mistake."

I for one think that oil is going to stay down, but that's not the point. The point is that this idea that anyone who is long can at the same time justify or excuse a downward price movement as being an ok event will still proclaim a long term rise in price.

Jan

16

Venezuelan Bonds, by Gordon Haave

January 16, 2007 | Leave a Comment

Venezuelan 2027 bonds are now yielding 1.7% over comparable treasuries. Thus, rational investors would not expect a credit loss of greater than 1.7% per year.

(This is a simplified model in many ways, but close enough for this analysis.)

The credit loss would be the probability of a credit event times the expected loss in a credit event.

(So, for example, a 10% chance of a credit event times a 50% loss if such an event happened would be an expected annual default loss of (.1*.5)=5%)

Any investor in these bonds must expect an annual credit loss of less than 1.7%.

Recently, Argentina "got away with" giving foreign creditors a 66% loss of principal. If Chavez decided to stick it to the dollar bond holders (like he shows every indication of doing to many foreign equity owners), there is no reason to expect that the bondholders would recover more than 33%.

So, we then solve for 1.7% = X * .66 = 2.57% This shows that an investor in these bonds must expect a less than 2.57% chance of Chavez defaulting, or a greater than 33% loss given default.

Given his political sensibilities, thoughts on economics and investors in general, and massive spending plans, would you bet that there is only a 2.57% chance of Chavez defaulting? I wouldn't. I also wouldn't bet on an only 66% loss given default. I wouldn't be surprised if there was an event where the loss given default on these bonds was 100%.

Read Venezuelan Dollar Bonds Rise, Rebounding From Last Week's Drop

Dec

21

Don’t Forget the Drift, by Victor Niederhoffer

December 21, 2006 | Leave a Comment

One must repeat that the unconditional drift of the market is 10% a year. Whenever you are short, you have a drift going against you. When you wish to go short, chances are that the drift of the market will be above 10% a year. That’s because you and others think there’s a bear market retrospectively, and require a higher rate of return to be invested. In addition there are frictional costs to being short. Put them all together, and I’ve never seen a short seller who’s made money, nor has the Palindrome. It does give psychic value however in that it lets you vent your hatred of the system and yourself. It also gives stature because you are always on the negative which seems so much more poignant than the positive.

Since you always are giving away money on the short side, on an expectational basis, it is best not to consider it as the wind is against you unless you are truly insecure. The question of when you should go short is the wrong question. A better question is when you should increase the leverage of your long investments. I would propose a hypothesis that it is good to do that when the market has suffered a decline with a given period of a certain magnitude or more.

I believe the above reasoning, as well as the questions I ask bears about whether things are truly so much worse than before, and whether if they are, is this bullish or bearish, which I have made repeatedly since 1960 but also for the last four years, during which the market has doubled, has prevented many people from self destruction.

Dr. Janice Dorn provides a different perspective:

Part of the profundity of Victor’s remark is that the bears make poignant arguments which are almost tailor-made to touch something very deep inside of those who are always watching and waiting for some disaster or catastrophe. The bearish arguments tend to be more scholarly, detailed, laced with Latin words and appeal to the limbic core of the brain (which holds memories of fear and terror and sees them even in their absence), as well as the higher neocortical areas which are, in some way, hard-wired to process, consolidate and retain bad news more firmly and longer lasting than good news. Bad news is stored as pain and that pain can be evoked in almost any situation. Good news tends to be more fleeting and there is more difficulty reaching into the brain stores to retrieve the memories of euphoria. Perhaps the neurochemistry of euphoria (be it dopamine, serotonin, norepi, or any of the thousands of neurochemicals) is configured in a way as to be more transient, spontaneous and non-entrained. Depression, disaster, danger lurking around every corner is much more “reachable” in terms of our psyche. Once again, this is likely a function of the way that the cortical neuro-pathways are laid down and communicate electrochemically with each other in the vast cortical landscape.