Jul

22

Merry Wives, from Duncan Coker

July 22, 2014 | Leave a Comment

I had the pleasure of seeing a very entertaining production of The Merry Wives of Windsor the weekend. It was fictionally set during the 1960s at a summer resort in the Poconos. Think Dirty Dancing meets Downton Abbey. The play shows Falstaff in all his completeness. The sometimes modern theme of women outsmarting their dullard husbands began long ago in this play. But in this story somehow the mockery is not spiteful or malicious, but to use a pun is "playful" with a touch of ribaldry to keep it interesting. I highly recommend everyone get out to see open-air Shakespeare somewhere this summer.

Oh yeah, and the play contains a fantastic use of the word alacrity: "I have a kind of alacrity in sinking"

- Falstaff recounting being tossed into the bog, outsmarted by the Wives.

Jul

16

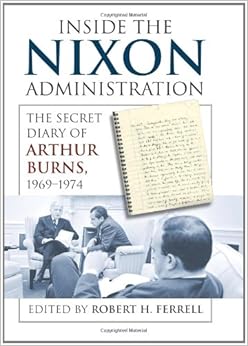

The Secret Diary of Arthur Burns provides a first hand account of the Federal Reserve Board Chairman for the period of 1968 to 1974. It was an interesting time frame for Fed policy. Among the issue they faced were; leaving the gold standard, floating the currency, renewing deficit spending, managing tariff/price controls, and dealing with an energy crisis to name just a few.

The Secret Diary of Arthur Burns provides a first hand account of the Federal Reserve Board Chairman for the period of 1968 to 1974. It was an interesting time frame for Fed policy. Among the issue they faced were; leaving the gold standard, floating the currency, renewing deficit spending, managing tariff/price controls, and dealing with an energy crisis to name just a few.

The context of the book takes the reader back to the highly regulated world of pre-Reagan America. Industry, trade and currencies were overseen by technocrats and this Republican administration had their hands seemingly everywhere. Bureaucracies like a wage and price boards set industrial pricing. Tariff boards controlled international trade, and currency pegs served to formalize handshake agreements between countries. The Nixon administration, however, marked the beginning of the end for at least some of these controls. Gold, famously, was the first to go. The metal increased from the longstanding $35/ounce peg. Eventually it floated freely.

The book portrays a cabinet completely preoccupied with politics, internal power struggles, and meddling in economic areas beyond their competence. On the monetary side, Milton Friedman's ideas were used but they were misapplied. The Fed boosted M1 as stimulative, but then developed a spider web of price controls to reduce the inflationary results. Hubris and indifference to basic economics were displayed by all the central players, Nixon, Burns at the Fed, Shutlz on Budget and Connally at Treasury.

For example, in dropping the gold standard Burns was the first to admit they had no idea what the consequences would be. It was purely a politically expedient decision. They needed more paper dollars to fund the ending of the Vietnam War. Also, they wanted to begin what would become many decades of federal deficit spending. In one such discussion he outlines the dynamics of a typical meeting:

page 66. "Here we were Kissinger, a brilliant political analyst but admittedly ignorant of economics; Connally, a thoroughly confused politician… Shultz, a no less confused amateur economist; I (Arthur Burns) the only one there with any knowledge of the subject, but even I not a real expert on some aspects of the intricate international problem"

Burns did argue for some growth policies including tax reductions and industry incentives. However, he was not persuasive enough. Time and time again the economically correct course was discarded for the politically easy one. Tariffs were arbitrarily thrown up to protect certain jobs prior to an election. The currency was expended to allow for politically targeting spending. Double digit Inflation was an acceptable consequence for fiscal expansion.

As an unintended benefit the book gives an interesting preview of recognizable characters in their youth like, Volcker, Shultz, and Kissinger. Burns though is often brutal in his character assessments. Burns made clear the book was not to be released until 30 years after his death. I can see the reason why.

Jul

9

It’s Happening Again, from Duncan Coker

July 9, 2014 | Leave a Comment

It is happening again. Starting in mid June the realized volatility of stocks futures, calculated with a 20 day look back, is lower than the realized volatility of 30 year bonds futures. Over the last 10 years it happens about 15% of the time. The returns for stocks are slightly negative during these time compared to the normal positive drift for stocks. Bonds are flat. This makes intuitive sense as the now less risky stocks would underperform the more risky (yet still risk free) bonds.

Jul

1

Grains, from Duncan Coker

July 1, 2014 | Leave a Comment

Even I am starting to take note of the moves in the grains, logabola and then some.

Even I am starting to take note of the moves in the grains, logabola and then some.

Like the taxi driver commenting on stocks he is buying unsolicited by passengers, this must be some sort of indicator and I offer it as a free fade to the pros on the site.

Jeff Watson writes:

When you think about it, Ceres is the most important market mistress, because everyone has to eat. Even the insiders tread lightly around her, the medieval devices of torture she still employs are very painful.

Jul

1

First Day, from Duncan Coker

July 1, 2014 | Leave a Comment

First day of the quarter goes up about 65% of the time since 2000 versus 52% of the time on other days. As if the market likes to establish an early lead. So any fund managers, investment advisers or traders who were prudently on the sidelines are forced to play from behind for the rest of the quarter. When you're playing catch-up in any sport or game, like tennis, eventually you have to take riskier shots. While your opponent, in this case the market, can just keep hitting them high and deep to the backhand, waiting for you to make an error.

First day of the quarter goes up about 65% of the time since 2000 versus 52% of the time on other days. As if the market likes to establish an early lead. So any fund managers, investment advisers or traders who were prudently on the sidelines are forced to play from behind for the rest of the quarter. When you're playing catch-up in any sport or game, like tennis, eventually you have to take riskier shots. While your opponent, in this case the market, can just keep hitting them high and deep to the backhand, waiting for you to make an error.

Jun

30

Golf Aphorisms, from Duncan Coker

June 30, 2014 | Leave a Comment

Here is a list of golf aphorisms written by a friend of mine. He is a competing low handicap golfer of just 20.

Here is a list of golf aphorisms written by a friend of mine. He is a competing low handicap golfer of just 20.

You can't win a tournament on Thursday, but you can definitely lose it.

There is no picture on the scorecard.

It is good to compete. It brings out the best of your abilities.

There will always be new swing ideas and people in your ear about mechanics. Stick to the swing that is natural and successful for you.

Approach the toughest hole with the same strategy as the easiest hole.

Golf is a test of your will versus the course, the natural elements and the tournament.

You can't walk off the course and go back to the range.

Play with what you're hitting that day be it hook, slice, or draw.

Have just one or two "swing thoughts" for the day.

If a putt lips out but you hit it the way you wanted, that's all that can be asked.

Learn how to play in different conditions and environments. It won't always be 75 degrees and sunny.

Sometimes hitting the driver 300 yards isn't the best play. Figure out when to be aggressive and when to be tactical.

Always forget your bad shots or good shots for that matter. Focus only on the shot at hand.

Sunday on the back nine you may have to change tactics completely.

Often times a bogey is a great score.

Never get angry with the course set up, the greens, or pin placements. Everyone plays the same course.

Approach practice like a tournament. Make each practice shot live and relevant.

-Austin Williams USC 2014

Jun

27

Roll ‘Em, from Duncan Coker

June 27, 2014 | 1 Comment

This is a technical observation but in doing some housekeeping and looking at S&P 500 futures data going back to 2000, we are almost at the point where a roll adjusted continuous time series is the same as the non-roll adjusted time series. In other word since 2000 there have now been almost as many positive carry months as negative carry months for SP futures. The changing of the guard if memory serves was some time in 2008 when short term rates (cost to borrow) became lower than the dividend yield of the cash SP 500. At that time the term structure of futures went into backwardation and there it has remained.

Charles Pennington writes:

We should thank 'anonymous' who told us back then that backwardation would be good for stock investing.

anonymous clarifies:

My supposition [was] based on comments by Philip Carret in his 1931 book The Art of Speculation.

Mr. Carret talked about periods when stocks "carried themselves"

because their dividends were sufficient to cover the cost of borrowing.

As of today, stocks are still carrying themselves, as Mr. Coker notes.

Jun

8

My Catch 22 Trade, from Jeff Watson

June 8, 2014 | Leave a Comment

Heller wrote in Catch 22:

Heller wrote in Catch 22:

Seven-cent Maltese eggs cost the sellers in Malta four and one-quarter cents each to procure. Milo is actually buying the eggs from himself in Malta, which means that as a seller there he is making two and three-quarter cents each egg. After he resells the seven-cent eggs to the mess halls for five cents each, he is still making a three-quarter cent profit per egg.

However, it turns out that Milo's Maltese eggs are actually one-cent Sicilian eggs which he has secretly shipped to Malta to drive up their value, yielding him another three and one-quarter cents profit per egg.

In short: in all these dealings, where Milo is the producer, consumer, and middleman (twice), he can afford a two cent per-egg loss, because overall the syndicate is making six cents revenue per egg. And everyone has a share.

I'm involved in a cash grain deal that is turning into something like this.

Duncan Coker writes:

I can only fictionalize (a la Heller Catch 22) what arbitrage Jeff has in place and the exotic transport involved. Buying Ukraine wheat shipped via ex-Russian military transport vehicle to the Black Sea, to load into barges to go down the Bosphorus to Istanbul. Then by freight via the Suez to Singapore for delivery against the Hong Kong futures sold for August. Just one possibility.

May

10

The Bond Market, from Duncan Coker

May 10, 2014 | Leave a Comment

One of the bigger surprises this year for me has been the rally in the bond market up some 7% on the long end. It appears as if the vigilantes will never ride again. Rather than the Fed as the cause, I would look to the Treasury. Related surprises are the federal deficit which has decreased sizeably from the peak several years, and spending, as bad as it is, has remained relatively flat. Massive new discoveries of energy reserves have helped to push down prices in commodities and boosted tax receipts. As the Fed unwinds its buying program apparently there are many others willing to step up.

Apr

29

Averages, from Duncan Coker

April 29, 2014 | 1 Comment

Averages are interesting and ubiquitous. I use averages every day and they are a part of my trading research. However, they are often misapplied in a social context. Find the average man, for example, and he does not exist, except in films like Idiocracy (highly recommended for a laugh). Thomas Sowell has written about this when statistics refer to average wealth, income, etc. In the sense that these are real flesh and blood people, the statistics deceive. For example, if there were just two earners, one making $50,000 and one making $1,000,000, the average is $525,000, surely not reflective of the underlying population.

Averages are interesting and ubiquitous. I use averages every day and they are a part of my trading research. However, they are often misapplied in a social context. Find the average man, for example, and he does not exist, except in films like Idiocracy (highly recommended for a laugh). Thomas Sowell has written about this when statistics refer to average wealth, income, etc. In the sense that these are real flesh and blood people, the statistics deceive. For example, if there were just two earners, one making $50,000 and one making $1,000,000, the average is $525,000, surely not reflective of the underlying population.

The market on average has an equity of premium of 6% per year and a nominal increase of around 9%, but very few years actually are near this. Just look at the last 10 years starting in 2004 for the SPY etf. (10.7, 4.83, 15.85, 5.14, -36.81, 26.37, 15.06, 1.89, 15.99, 32. 31) avg=9.1. Certainly there's nothing "average" about this decade.

This is not news to anyone reading this site, but it is interesting to think about. In practice, in life, and as traders we live in the variation. If I can be philosophical, we live in the journey not the destination. The journey being the many deviations from what we expect might occur. The variation around the expectation, in more interesting, positive and negative extremes, and how we will deal with them when they occur. This is what defines us as individuals.

Apr

2

Trading and Fishing, from Hernan Avella

April 2, 2014 | Leave a Comment

In preparation for my first fishing trip of the year next weekend, I watched the film Low and Clear. It starts with the usual boring fishing-zen dialogues, but then it presents an interesting parallel between mentor and student reunited for a steel-head fishing trip in BC. The mentor is a fishing master that has done little else with his life and has a relentless approach to catching fish. The student now has a life outside fishing, but he is not as good fisherman anymore and he focuses more on the experience of fishing and other superfluous things like a "spade cast".

In preparation for my first fishing trip of the year next weekend, I watched the film Low and Clear. It starts with the usual boring fishing-zen dialogues, but then it presents an interesting parallel between mentor and student reunited for a steel-head fishing trip in BC. The mentor is a fishing master that has done little else with his life and has a relentless approach to catching fish. The student now has a life outside fishing, but he is not as good fisherman anymore and he focuses more on the experience of fishing and other superfluous things like a "spade cast".

This contrast reminded me of the time when I discovered that trading didn't need to be a beautiful process, it only needs to get the job done. And somehow I don't see around the guys who were obsessed about catching the big swing with fancy methods. I do see the disciplined hybrids (specs/grinders) consistently making money every year.

A quote from the Palindrome seems appropriate:

"A lot of people of average intelligence make a good living. Really smart people can accumulate a fortune if they are truly committed. The problem with you is that you like to do interesting work. Someone who wants to be rich doesn't care what he does. He only focuses on the bottom line. All day long he thinks how can he make more money. If that means setting up more shoe shine stands, that's what he does."

Happy Fishing, and trading!

Duncan Coker writes:

It is good to hear from another angler on the list. Hernan brings up the "winning ugly" concept as it relates to fishing and trading. It is definitely better to win ugly, then lose gracefully in trading, in sports and many other things. In fact all my trades are ugly. It is a scrappy dog fight.

Fishing, though, is a respite and pastime in nature, not a vocation. If I was a guide maybe I would feel differently. But as an amateur and outdoorsman, I like all the aspects, walking to the river, scouting for fish, setting up, casting. On style, I much prefer spending the day taking long casts with a dry fly versus "hucking-lead", the equivalent of bait fishing on a river. My fishing buddy and I fit the two different profiles well. It ain't pretty, but he catches more fish. I am slow and deliberate. He races from one spot to the next and probably works a bit harder on the river. I suppose it is how you define success. In trading it is clear, P&L is all that matters. In fishing a day on the river is always a winning trade and I don't define fishing success relative to anything. Like an aspiring Zen master on the river, fishing simply is.

Mar

10

Lunch Econ, from Duncan Coker

March 10, 2014 | Leave a Comment

Here is an economics anecdote on trade that I can explain to my six year old. Yesterday at an outdoor plaza there is a soup vendor I normally go to and a taco guy next door. I notice my soup guy is eating tacos, and I look over to taco stand and he is having soup. I ask the soup vendor about it and he quips that he is checking out the competition and hopes he is not poisoned. But I see a nice illustration of comparative advantage, value creation and utility curve optimization.

Feb

21

Dollar Policy, from anonymous

February 21, 2014 | 1 Comment

It is time honored policy for governments to run up huge debt, then via inflation to pay back that debt in pennies to the dollar or not at all. The most extreme example would be Wiemar republic in the 20s, but there are devaluations all the time, witness Argentina. It is an easy and quiet destruction of wealth of the citizenry by their government. Keynes wrote about it. Though eventually it will work in the US, there must be frustration it is taking so long here. There must be other forces at work holding up the dollar I would call these the positive affects, like the production, innovation, demand for US currency for trade, a slowing of credit growth (second order affect). Amazingly for the time being these forces counter-act a destructive currency policy and there is a stand-off.

It is time honored policy for governments to run up huge debt, then via inflation to pay back that debt in pennies to the dollar or not at all. The most extreme example would be Wiemar republic in the 20s, but there are devaluations all the time, witness Argentina. It is an easy and quiet destruction of wealth of the citizenry by their government. Keynes wrote about it. Though eventually it will work in the US, there must be frustration it is taking so long here. There must be other forces at work holding up the dollar I would call these the positive affects, like the production, innovation, demand for US currency for trade, a slowing of credit growth (second order affect). Amazingly for the time being these forces counter-act a destructive currency policy and there is a stand-off.

Stefan Jovanovich writes:

I think anonymous' point needs further support. Governments have not, in fact, "paid back" debt using inflated currencies. That is one of Keynes' historical fantasies. The debt was simply defaulted. After the new currency was refloated, some of the former debtholders (but never all or even a majority) are lucky/influential enough to be "repaid" by having their old debt instruments swapped for new IOUs using the new "sound" currency; but actual payments that extinguish the debt are never made for the simple reason that the government had no reserves in the old currency and no political ability to make one grand final payment in full. This may seem like a distinction without a difference, but it is not. Default allows the governments to wipe out all the other promises made that were not secured by indentures (pensions, social service payments, subsidies) in the name of "reform". If those obligations had, in fact, been "paid back" in the inflated legal tender, the claimants would at least have gotten old "dollars" that were worth new pennies; what, in fact, happens is that they get nothing.

The rise of the National Socialists can be directly tied to the fact that the currency reform after the hyperinflation left all the old Bismarck safety net promises in default. Hitler's most successful campaign promise was that he would restore those vanished pensions at full value (one can find parallels with the American Progressives' promise throughout the last third of the 19th century and all the times thereafter to assure farmers that they would receive "par" for their crop payments. The just-passed farm bill is a legacy of that toxic doctrine of equalism.)

Feb

6

Specialize or Diversify, from Duncan Coker

February 6, 2014 | Leave a Comment

In the short term trading world is it better to diversify and trade many things or specialize and trade just a few. I am in the later camp, as it takes all my usable mind capacity to manage just one or two positions concurrently.

In the short term trading world is it better to diversify and trade many things or specialize and trade just a few. I am in the later camp, as it takes all my usable mind capacity to manage just one or two positions concurrently.

Others prefer to trade many instruments saying it increases opportunity and reduces risk by diversifying. However in futures trading, and short-term in particular, there is no Markowitz "free lunch" that comes from diversification which applies only to stocks. By trading more instruments it does perhaps give you something to do when other markets are slow. This however could also be viewed as a negative, and maybe it is better to not be in the markets at times. It makes sense to me to trade based on opportunity. Yet, in practical trading-life these opportunities are so difficult to find, it takes being a specialist to uncover them.

In angling, I am a bit of a hybrid. I specialize in flyfishing, but I will go after anything with gills and scales and recently added the beloved carp to my list. In economics, comparative value tell us to specialize and has been the source behind much advancement. Ben Green traded just horses and the occasional mule. Bacon just bet on the ponies. Specializing served them both well.

Anatoly Veltman writes:

The main advantage of algo trading is the ability of your portfolio to simultaneously participate in all futures you've pre-programmed. Certainly that's an impossible task for a manual trader

Kim Zussman comments:

Duncan isn't trading index futures lunching with Markowitz? (Albeit less so than before the period of widespread indexification).

Jan

17

Short and Long-Term Thinking, from Duncan Coker

January 17, 2014 | Leave a Comment

Keynes is famous for writing "in the long-term we are all dead". Focusing on the long term may be important but ultimately is meaningless to the individual. He also wrote that for businesses planning the short-term is predictable, while the longer-term from year to year becomes random. For governments multiply this by many factors. Anything in a government budget beyond year t+3 is complete fiction. Wall street convictions say the opposite, that stocks are unpredictable in the short-term. In the long-term, however, stocks will enjoy an upward drift. Fischer Black wrote about this issue in his business cycle theory saying that firms attempt in the short-term to produce for future long-term demand. When they plan and execute well there is economic growth. When they plan and execute poorly there are recessions. The 2008 mismatch being a tremendous oversupply of housing and credit, for example.

Keynes is famous for writing "in the long-term we are all dead". Focusing on the long term may be important but ultimately is meaningless to the individual. He also wrote that for businesses planning the short-term is predictable, while the longer-term from year to year becomes random. For governments multiply this by many factors. Anything in a government budget beyond year t+3 is complete fiction. Wall street convictions say the opposite, that stocks are unpredictable in the short-term. In the long-term, however, stocks will enjoy an upward drift. Fischer Black wrote about this issue in his business cycle theory saying that firms attempt in the short-term to produce for future long-term demand. When they plan and execute well there is economic growth. When they plan and execute poorly there are recessions. The 2008 mismatch being a tremendous oversupply of housing and credit, for example.

In life and business, it is sounds more wise and mature to have long-term thinking, childish to think only of tomorrow. The Sage holds investments forever, yet the insurance premiums collected I am sure are tallied ever day. A Zen philosophers would say we should live in the moment, the extremely short-term. I agree with Fischer Black's thinking. It is good to embrace that the future is highly unpredictable and every decision we make involves time and uncertainty. I still work hard in the short-term towards long-term goals, but expect some variation along the way. The Yangtze has many twists and turns before reaching the sea; Fortes fortuna adiuuat.

Jan

6

Stats Songs, from Duncan Coker

January 6, 2014 | Leave a Comment

This may be already be obvious, but there is an amazing similarity between statistical analysis and writing country music songs. In song writing, you have two or three verses and a chorus to try to convey one idea and maybe a supporting storyline. The chorus has to be convincing, and if you accompany this with a nice melody the song will have an emotional impact on the audience.

This may be already be obvious, but there is an amazing similarity between statistical analysis and writing country music songs. In song writing, you have two or three verses and a chorus to try to convey one idea and maybe a supporting storyline. The chorus has to be convincing, and if you accompany this with a nice melody the song will have an emotional impact on the audience.

The same is true in statistics. The best graphs, tables and charts are the simple ones that can easily convey one big idea. Statistics when presented well have an emotional impact, just like a song, that wow affect. True it is hard to hum confidence intervals or t-scores, but otherwise they are not to far removed.

Dec

13

Market Avalanches, from Jim Sogi

December 13, 2013 | Leave a Comment

Avalanche prediction requires the study of the snowpack both historically and how the snow structure has metamorphosed over time. One of the prime causes of avalanches are weak layers and slab formation. Weak layers in the snow pack are layers in the snow that cause the snow on top of it to slide off it and down the hill causing an avalanche. Weak layers can be low density snow or an ice layer or hoar frost flakes. Slab avalanches are created when higher density snow bonds together then slides on a weak on steep hill. Avalanches can kill.

Avalanche prediction requires the study of the snowpack both historically and how the snow structure has metamorphosed over time. One of the prime causes of avalanches are weak layers and slab formation. Weak layers in the snow pack are layers in the snow that cause the snow on top of it to slide off it and down the hill causing an avalanche. Weak layers can be low density snow or an ice layer or hoar frost flakes. Slab avalanches are created when higher density snow bonds together then slides on a weak on steep hill. Avalanches can kill.

Avalanches remind me of markets. You can study market structure historically by looking at the number of trades at a price. Over time the density may change. Market order depth structure is not available in full but could be inferred to some degree. Some parties have access to full book.

The theory is there are weak layers in the market structure that might cause a market avalanche or rapid rise. There may also be dense layers in the market structure. An example is a long bar with big price change but low number if trades. Time may change the number of trades at the prices or depth of orders might affect the reactivity of the bar. And a gap is also an example of a weak layer.

Duncan Coker adds:

Jim's post on avalanches' relationship to the market can be summed up in one word. Respect. Respect that at any point in time the market is in equilibrium. It is priced correctly given forward required return, the price of risk. If one disagrees and expresses this in a position, the null hypothesis is the market is right and I will be wrong. The mountains always prevail in the same way, and if I am venturing out in the back country, I will show due respect.

Oct

30

Collateral, from Duncan Coker

October 30, 2013 | Leave a Comment

Collateral plays a big role in the system at large. If the banks can survive only through overnight funding at either the repo, MRO/LTRO, or Fed discount window, acceptable collateral is as important as rates. To ease the Fed can ignore rates and just say one day they will except IBM or Apple debt or commercial paper as collateral in exchange for loans. Conversely they could slip in some language about raising "haircuts" on notes or bills to have a tightening effect. While all are focused on the level of bond buying, there are many other tricks they can pull from the sleeves.

Richard Owen writes:

They say the securitisation markets died.

Not so. It is just the banks began wrapping to repo rather than sell.

The ECB gave it a pill by agreeing to accept any AAA collateral. Standard practice is to wrap your doo doo, top slice it, and fund the AAA at ECB.

Oct

28

Beginner’s Luck, from Duncan Coker

October 28, 2013 | 1 Comment

We have all experience or witnessed the thing called beginner's luck in sports, games or other competitions. I will make a hypothesis that this is not luck at all, but a non-random effect. It may be like the home field advantage, which was never fully explained until recently. In beginner's luck what the player lacks in experience he more than makes up for in other attributes allowing him to compete better. It could be a higher performance mental state. Lacking experience the player also lacks other things like fear, disappointment and loss. Free of these, he is willing to take on more risk. He is not anchored to one belief system or set of rule. Rather he is quite flexible and adaptable to new conditions as they present themselves. Beginners see the world as children again, albeit all too briefly, and may find simple opportunities that a more experienced player would overlook. In a competition, an opponent could underestimate a beginner giving him an advantage and allowing him to play with less pressure to win. It would do well for a more experience players to understand what is behind beginner's luck and to find ways to either adopt or counter it.

We have all experience or witnessed the thing called beginner's luck in sports, games or other competitions. I will make a hypothesis that this is not luck at all, but a non-random effect. It may be like the home field advantage, which was never fully explained until recently. In beginner's luck what the player lacks in experience he more than makes up for in other attributes allowing him to compete better. It could be a higher performance mental state. Lacking experience the player also lacks other things like fear, disappointment and loss. Free of these, he is willing to take on more risk. He is not anchored to one belief system or set of rule. Rather he is quite flexible and adaptable to new conditions as they present themselves. Beginners see the world as children again, albeit all too briefly, and may find simple opportunities that a more experienced player would overlook. In a competition, an opponent could underestimate a beginner giving him an advantage and allowing him to play with less pressure to win. It would do well for a more experience players to understand what is behind beginner's luck and to find ways to either adopt or counter it.

Anatoly Veltman writes:

I experienced it first hand in spring of 1987. I've decided to make my first major trade by that time, because I spent several months eyeballing all available charts and was struck by an unmistakable basing pattern in Silver. I surveyed dozens of veteran Silver traders around COMEX - and none of them would get excited at that particular junction. They all got burned, some less and some totally, in the course of the preceding 6 years worth of price action in Silver - and that seemed to convince them that Silver can never again master a sustainable rally.

Well, as my beginner's luck would have it: I started accumulating as much as I could over 30 consecutive trading days from 50k of initial margin money, and by April 27 I already owned hundreds of lots, worth over a million! But on that one day - easy come easy go - Silver rolled back from $11.25 to $7.50, leaving me with barely positive equity and a single lot for memory keep-sake! So, admittedly, the old wolves did end up skinning me: during that one unprecedented futures session, which flipped all futures months from limit-up to limit-down lock - only they knew how to execute in the Spot month of un-traditional April futures and front run (via switches) all outside would-be sellers, none of whom got to sell anything that day! And by next day the April contract was not just spot delivery - it didn't even exist!! That one trading session proved too arcane for any amateur futures trader, and the Exchange insiders fully capitalized. Just like in their good ole times of the famed January 1980!

Oct

3

Employment, from Duncan Coker

October 3, 2013 | Leave a Comment

There is a second derivative of deception on tomorrow's employment data. Not only don't we know the number, we don't know when they plan to release the unknown number. And since all is closed, we don't know when they will even announce when they will announce the unknown numbers. The markets, the great discounters of all information, will have to work extra hard.

Sep

23

Reserve Currencies, from Duncan Coker

September 23, 2013 | 2 Comments

I heard an interesting economist speak recently regarding currency and in particular what is required to be a Reserve Currency. There are three important requirements. First, the currency must float freely. The world won't hold a currency that is incorrectly priced. Second, there must be an active and legitimate bond market to set rates of interest. Third, and most interesting to me, a strong navy. In global trade there is an implied guarantee that goods held in a Reserve Currency will reach their destination unharmed. That is not to say a global Reserve cannot change, it just requires some doing. British Sterling met those standards in the 19th century, when she ruled the seas. Not so now. At present the Chinese Yuan is deficient in all three, the Euro is lacking in one.

I heard an interesting economist speak recently regarding currency and in particular what is required to be a Reserve Currency. There are three important requirements. First, the currency must float freely. The world won't hold a currency that is incorrectly priced. Second, there must be an active and legitimate bond market to set rates of interest. Third, and most interesting to me, a strong navy. In global trade there is an implied guarantee that goods held in a Reserve Currency will reach their destination unharmed. That is not to say a global Reserve cannot change, it just requires some doing. British Sterling met those standards in the 19th century, when she ruled the seas. Not so now. At present the Chinese Yuan is deficient in all three, the Euro is lacking in one.

Aug

30

Bonds and Stocks, from Duncan Coker

August 30, 2013 | 1 Comment

I am reading a book on equity risk premiums and it provided a nice frame work to view bonds and stocks. The equity risk premium P is fairly stable over time, meaning the excess required return to hold the riskier* asset of stocks over bonds. So when bonds go down, for example, as they are now, riskless rates are going up. This means the required return for stocks = riskless rates plus P, in now also higher. So either the future prospects for stock earnings must be better, or stocks must go down now to make up the difference. That seems to be the battle we will be in for the post Bernanke world. One eye on earnings, the other on bonds.

*Note the last few years has proved there really is no such thing as a riskless rate, real rates can stay negative for a long time, and sometimes in bond risk is higher than equity risk. But all that hurts my brain too much to contemplate.

Aug

19

The Cup, from Duncan Coker

August 19, 2013 | 1 Comment

I was speaking with a sailor friend recently about the new boat designs for the Americas Cup race. They are now completely foil keel, which means very little of the boat is actually in the water, and more like hovercraft. The sail coverage and mast size to boat size ratios are at an extreme, with the mast now double the length of the boat. They are incredibly fast and incredibly unstable. To move the boom requires a mechanical device rather than sailor sweat and strength. Sadly, there was a fatality in this year race and more than one lost boat. All this means a captain must react well ahead of the wind and conditions to stave off disaster. This reminds me of another activity many are involved with on the site.

I was speaking with a sailor friend recently about the new boat designs for the Americas Cup race. They are now completely foil keel, which means very little of the boat is actually in the water, and more like hovercraft. The sail coverage and mast size to boat size ratios are at an extreme, with the mast now double the length of the boat. They are incredibly fast and incredibly unstable. To move the boom requires a mechanical device rather than sailor sweat and strength. Sadly, there was a fatality in this year race and more than one lost boat. All this means a captain must react well ahead of the wind and conditions to stave off disaster. This reminds me of another activity many are involved with on the site.

Aug

6

Summertime, from Duncan Coker

August 6, 2013 | 1 Comment

Gershwin's Summertime is written in a minor key which gives it a dark, listless feeling like floating down a river on a hot, humid day. The generally optimistic lyrics are incongruent with the minor key of the melody. If it was written in a major key it would be completely different, but he chose minor. The song gives the listener a sense that things are not really so wonderful and the "living is– not really that– easy".

Gershwin's Summertime is written in a minor key which gives it a dark, listless feeling like floating down a river on a hot, humid day. The generally optimistic lyrics are incongruent with the minor key of the melody. If it was written in a major key it would be completely different, but he chose minor. The song gives the listener a sense that things are not really so wonderful and the "living is– not really that– easy".

As the optimistic stocks market drifts ever higher and higher in the summer heat, the bond market is playing a minor key melody. Bond volatility is higher than stocks, and their role as substitutes for one another has changed, giving the listener a sense that the living is not that easy. Then again, maybe it is just summertime trading.

Jul

14

Fishing, the Art of Waiting, from Duncan Coker

July 14, 2013 | 2 Comments

I found myself on a mountain lake one morning recently, watching the sun rise over a distant peak. For the first half hour I try some standard streamer patterns, casting more or less blindly into the crystal smooth waters and looking to attract some attention. Though it is relaxing to cast and practice the timing, it is really a prelude to catching fish. In fact it is probably counter-productive. The lake being so calm at this time of day the splash and vibration from the line will scare any fish in the vicinity.

As the sun starts to rise and warm up the lake small duns hatch and hop along the surface. I decide on another approach, and do nothing for a while, wait and observe. There are splashes far out in the middle of the lake as fish being to feed on the duns. The light is getting better, particularly looking south along the bank. I’m able to scan far ahead and deep into the water looking in this direction, while to the north I see only the black surface of the lake. I wait some more and notice a small fingerling trout feeding in a corner bank where the sun is just started to reach. The duns are getting heavier now. Finally I see a nice sized brown trout near the smaller fish, circling , stopping, and feeding in the shallow water. Here, is a fish a might have a chance to catch.

I change flies to one slight larger than the duns, but same color and a close match. The trout has not seen me I think, but perhaps out of instinct he moves away into the shadows, before I can cast. So I wait some more. Out of the shadow he emerges and I can see him circle back in my direction. It is so calm, a direct cast will scare him. So I make guess where he might go and cast there. The fly lands and he is unaware, meandering in that direction. Now I am acutely interested, focusing on the fly and the trout just below surfaces, as he heads to the dun fly. He sees it, moves, and takes it! I have him on the line and keep it tight as I steer him to the shallow water by the shore. The hook is well set in his upper jaw but easy to remove. For a brief moment I can appreciate his beautiful coloring and wildness before sending him back to his breakfast routine.

Then sun is rising more overhead and I see more splashing to my right. But after this encounter I decide wait some more, to let the water get back to its natural state. Then I head south along the bank I scouted earlier. I see a nice cruising fish headed my way far ahead. I raise the rod to cast, but my shadow alone sends him off to the middle of the lake. I wait some more. Now I am walking along the bank holding the fly and line in the opposite hand from the rod. This is the way the bonefish guides teach you in Andros to prepare, and no false casting allowed. “Wait, wait, wait”, then say. “Until you Seeeee the fish”. Then and only then you do cast with conviction, accuracy and intention. You make the first one count because by the second or third cast he is gone. I am able to land a few more this way before the tranquility of the lake starts to wane as the other anglers join in. The heart of the morning begins and I head back to join my family for breakfast and start the rest of the day.

Jul

10

Risk Parity Crossover, from Duncan Coker

July 10, 2013 | Leave a Comment

Bonds are traditionally considered safe, but they have become a bit dicey last month. I calculated the 20 day historical volatility using adjusted 30 year bond futures and sp500 futures from July-2003 to June 2013. Roughly 75% of the time stocks are more volatile, and 25% of the time bond volatility is higher. The most recent occurrence when bond vol was greater was in late May to mid June. Looking just at the period from June 2010 to present, S&P returns were normal, while bond returns were negative during these episodes.

Alex Castaldo adds:

Probably not a coincidence that at this time 'A Big Risk Parity fund is under the weather ' according to a Reuters story from late June.

Jun

27

Lacker, from Duncan Coker

June 27, 2013 | Leave a Comment

Today as the market looks to get even for the month, Lacker is part of the rescue. He is one of the most hawkish on the Fed, but is also a realist commenting on how there is no meaningful reduction in bond purchases anywhere on the horizon. Tapering, he points out, is a derivative, changes in the rate of purchases, but still purchases.

Today as the market looks to get even for the month, Lacker is part of the rescue. He is one of the most hawkish on the Fed, but is also a realist commenting on how there is no meaningful reduction in bond purchases anywhere on the horizon. Tapering, he points out, is a derivative, changes in the rate of purchases, but still purchases.

As an aside, in swimming, tapering is the last phase of a rigorous training schedule in preparation for a race. Tapering implies some sort of disciplined or difficult action preceding it. It will be nice when the word retires from the financial lexion as "the cliff" did.

At present, Lacker is a non-voting member so has nothing to lose by telling the truth. With B retirement talk, Lacker would be the best candidate, but the odds can't get long enough and better to wager a summer claiming race at Saratoga.

Jun

7

Market Story Time, from Duncan Coker

June 7, 2013 | Leave a Comment

Everyone loves a good story and I try to read to my children every night. The current market narrative is that the last 6 month rally is entirely Fed driven and without Fed support equity markets are doomed. I'd argue stocks have gained on an improving economy and corporate profits. Real rates have gone up for the same reason as seen in TIPS ( though still negative). But as long as this narrative is floating around there will disparate opinions which is what makes a market.

Everyone loves a good story and I try to read to my children every night. The current market narrative is that the last 6 month rally is entirely Fed driven and without Fed support equity markets are doomed. I'd argue stocks have gained on an improving economy and corporate profits. Real rates have gone up for the same reason as seen in TIPS ( though still negative). But as long as this narrative is floating around there will disparate opinions which is what makes a market.

I think this will be the summer theme. Then one day, rates and stocks will have gone up enough for this narrative to be dismissed entirely and we will be on to a new story. And, with any luck we will all live happily ever after.

May

16

S&P back of the envelope, from Duncan Coker

May 16, 2013 | 1 Comment

Some back of the envelope numbers on S&P500 futures daily changes last 10years for your perusal:

Year %up Max Min SDev 2003 55% 28 -29 10 2004 57% 18 -21 8 2005 54% 21 -21 8 2006 53% 26 -25 8 2007 52% 44 -57 14 2008 50% 127 -100 27 2009 56% 54 -42 14 2010 58% 48 -41 12 2011 51% 59 -85 18 2012 51% 42 -35 12 2013 65% 25 -38 11

Alex Castaldo ponders:

The standard deviation for a binomial is the famous sqrt(N p q) and the standard deviation for a proportion is sqrt(p q / N). Assume p=0.54 q=0.46 and N=252 days per year. Then sd= 3.1%. The proportions for 2003 through 2012 are within usual confidence intervals.

But for the year 2013 we have only N=95 trading days so far. In that case sd= 5.1%. So the observed 65% is about 2.16 standard deviations above the expected. Yes, it is statistically significant but not hugely so.

May

14

The Difference Between a Speculator and a Gambler, from Larry Williams

May 14, 2013 | Leave a Comment

I first saw the 'dead eyes' look of a poker player/loser when I was 13 or so. Still gives me restless nights and I know I cannot become that way.

I first saw the 'dead eyes' look of a poker player/loser when I was 13 or so. Still gives me restless nights and I know I cannot become that way.

My dad took me into the "stockman's bar" in Billings, Montana to impress upon me what degenerate, greedy people turn into.

Probably another sleepless tonight tormented by that devil.

Gary Rogan asks:

What is the real difference between gambling and speculation (if you take drinking out of the equation)? Is it having a theory about the odds being better than even and avoiding ruin along the way?

Tim Melvin writes:

I will leave the math side of that answer to those better qualified than I, but one real variable is the lifestyle and people with whom one associates. A speculator can choose his associates. If you have ever been a guest of the Chair you know he surrounds himself with intelligent cultured people from whom he can learn and whom he can teach. There is good music, old books, chess and fresh fruit. The same holds true for many specs I have been fortunate to know.

Contrast that to the casinos and racetracks where your companions out of necessity are drunks, desperates, pimps, thieves, shylocks, charlatans and tourists from the suburbs. Even if you found a way to beat the big, the world of a professional gambler just is not a pleasant place.

Gibbons Burke writes:

Here is something I posted here before on this distinction…

Here is something I posted here before on this distinction…

Being called a gambler shouldn't bother a speculator one iota. He is not a gambler; being so called merely establishes the ignorance of the caller. A gambler is one who willingly places his capital at risk in a game where the odds are ineluctably, mathematically or mechanically, set against the player by his counter-party, known as the 'house'. The house sets the odds to its own advantage, and, if, by some wrinkle of skill or fate the gambler wins consistently, the house will summarily eject him from the game as a cheat.

The payoff for gamblers is not necessarily the win, because they inevitably lose, but the play - the rush of the occasional win, the diversion, the community of like minded others. For some, it is a desire to dispose of money in a socially acceptable way without incurring the obligations and responsibilities incurred by giving the money away to others. For some, having some "skin in the game" increases their enjoyment of the event. Sadly, for many, the variable reward on a variable schedule is a form of operant conditioning which reinforces a compulsive addiction to the game.

That said, there are many 'gamblers' who are really speculators, because they participate in games where they develop real edges based on skill, or inside knowledge, and they are not booted for winning. I would include in this number blackjack counters who get away with it, or poker games, where the pot is returned to the players in full, minus a fee to the house for its hospitality*.

Speculators risk their capital in bets with other speculators in a marketplace. The odds are not foreordained by formula or design—for the most part the speculator is in full control of his own destiny, and takes full responsibility for the inevitable losses and misfortunes which he may incur. Speculators pay a 'vig' to the market; real work always involves friction. Someone must pay the light bill. However the market, unlike the casino, does not, often, kick him out of the game for winning, though others may attempt to adapt to or adopt his winning strategies, and the game may change over time requiring the speculator to suss out new rules and regimes.

That said, there are many who are engaged in the pursuit of speculative profits who, by their own lack of skill are really gambling; they are knowingly trading without an identifiable edge. Like gamblers, their utility function is not necessarily to based on growth of their capital. They willingly lose their capital for many reasons, among them: they enjoy the diversion of trading, or the society of other traders, or perhaps they have a psychological need to get rid of lucre obtained by disreputable means.

Reduced to the bare elements: Gamblers are willing losers who occasionally win; speculators are willing winners who occasionally lose.

There is no shame in being called a gambler, either, unless one has succumbed to the play as a compulsion which becomes a destructive vice. Gambling serves a worthwhile function in society: it provides an efficient means to separate valuable capital from those who have no desire to steward it into the hands of those who do, and it often provides the player excellent entertainment and fun in exchange. It's a fair and voluntary trade.

Kim Zussman writes:

One gambles that Ralph and/or Rocky will comment.

Leo Jia adds:

From the perspective of entering trades, I wonder if one should think in this way:

speculators are willing losers who often win; gamblers are willing winners who often lose.

David Hillman adds:

It is rare to find a successful drug lord who is also a junkie.

Craig Mee writes:

One possible definition might be "a gambler chases fast fixed returns based on luck, while a speculator has time on his side to let the market decide how much his edge is worth."

Bill Rafter comments:

Perhaps the true Speculator — one who is on the front lines day after day — knows that to win big for his backers, he HAS to gamble. His only advantage is that he can choose when to play.

Anton Johnson writes:

Anton Johnson writes:

A speculator strives to be professional, honorable, intellectual, serious, analytical, calm, selective and focused.

Whereas the gambler is corrupt, distracted, moody, impulsive, excitable, desperate and superstitious.

Jeff Watson writes:

I know quite a few gamblers who took their losses like men, gambled in a controlled (but net losing manner), paid their gambling debts before anything else, were first rate sports, family guys, and all around good characters. They just had a monkey on their back. One cannot paint with a broad brush because I have run into some sleazy speculators who make the degenerates that frequent the Jai-Alai Frontons, Dog Tracks, OTB's, etc look like choir boys.

anonymous writes:

Guys — this is serious, not platitudinous, and I can say it from having suffered the tragic outcomes of compulsive gambling of another — the difference between gambling and speculating is not the game, the company kept, the location, the desperation or the amounts. The only difference is that a gambler, when asked of his criterion, when asked why he is doing this, will respond with "To make money."

That's how a compulsive gambler responds.

Proper money management, at its foundation, requires the question of criteria be answered appropriately, and in doing so, a plan, a road map to achieving that criteria can be approached.

Anton Johnson writes:

It's not the market that defines whether a participant is a Gambler or a Speculator, it's his behavior.

Gibbons Burke writes:

That's the essence of my distinction:

"gamblers are willing losers who occasionally win"

That is, gamblers risk their capital on propositions where the odds are either:

- unknown to them

- cannot be known

- which actual experience has shown to have negative expectation

- or which they know with mathematical precision to be negative

They are rewarded for doing so on a random schedule and a random reward size, which is a pattern of stimulus-response which behavioral scientists have established as one which induces the subject to engage in the behavior the longest without a reward, and creates superstitious as well as compulsive behavior patterns. Because they have traded reason for emotion, they tend not to follow reasonable and disciplined approach to sizing their bets, and often over bet, leading to ruin.

"speculators are willing winners who occasionally lose." That is, speculators risk their capital on propositions where the odds are:

- known to have positive expectation, from (in increasing order of significance) theory, empirical testing, or actual trading experience

They occasionally get unlucky, and have losing streaks, but these players incorporate that risk into the determination of the expectation. Because their approach is reason-based rather than driven by emotion, they usually have disciplined programs for sizing their bets to get the maximum geometric growth of their capital given the characteristics of the return stream, their tolerance for drawdown.

If a player has positive expected value on a bet, then it is not a gamble at all. The house does not gamble. It builds positive expectation into its games. It is a willing winner, although it occasionally loses.

There are positive aspects of gambling, which I have pointed out earlier in the thread and won't belabor. To say that "all gambling is bad" is to take the narrowest view. Gamblers who are willing losers (by my definition all are) provide the opportunities for willing winners (i.e., speculators) to relieve gamblers of the burden of capital they clearly have no desire to hold onto, or are willing to trade in a fair exchange for the excitement of the play, to enable their alcoholic habit, to pass the time, to relieve their boredom, to indulge delusions of grandeur at the hoped-for big win, after which they will quit playing, or combinations of all of the above.

Duncan Coker writes:

I found Trading & Exchanges by Larry Harris a good book on this topic and he defines all the participants in the exchanges and both gambler and speculators have a role to play. Here is something taken from page 6 that make sense to me: "Gamblers trade to entertain". Speculators to "trade to profit from information they have about future prices."

He divides speculators into those that are well informed versus those that are not. One profits at the expense of the other. Investors "use the markets to move money from the present into the future". Borrowers do the opposite.

Apr

19

Cork Technology, from Duncan Coker

April 19, 2013 | Leave a Comment

New and old technology can coexist well together. For example, I had a ground water monitor installed recently which has a wireless feature that seamlessly deactivates a related irrigation system. Sounds complex, but the key element in the system is cork. When the cork in the device expands due to rain it triggers the cutoff. Cork is very useful in other areas too. The modern fishing reels use exotic metals and arbor designs to get the best performance. But cork is still used for the drags. This sets the tension on the line when fighting a fish which is the main purpose of a reel. In wine cork is preferred sealer especially for the purpose of aging. In trading the older methods of going against the panics and the crowds can coexist and profit in the post HFT world.

New and old technology can coexist well together. For example, I had a ground water monitor installed recently which has a wireless feature that seamlessly deactivates a related irrigation system. Sounds complex, but the key element in the system is cork. When the cork in the device expands due to rain it triggers the cutoff. Cork is very useful in other areas too. The modern fishing reels use exotic metals and arbor designs to get the best performance. But cork is still used for the drags. This sets the tension on the line when fighting a fish which is the main purpose of a reel. In wine cork is preferred sealer especially for the purpose of aging. In trading the older methods of going against the panics and the crowds can coexist and profit in the post HFT world.

Apr

11

Get the Drift, from Duncan Coker

April 11, 2013 | Leave a Comment

I used drift adjusted time series data, but I realize when one is trading against the drift (never a good idea) drift adjusted data will inflate the trade expectation. For example, using the difference method of subtracting the average move over the time series, X expectation will become X-drift. In a rising market, X-drift will be more negative than X, given a higher expectation to go against the drift. X are real points one might have made or lost; X-drift, I suppose, is for statistical significance test reasons. In a rising market if you are trading with the drift, using drift adjusted data gives you more conservative results, which is probably a good thing. But what about trading against the drift? Any comments appreciated to help me get the drift.

Apr

10

Scorecasting, from Duncan Coker

April 10, 2013 | 1 Comment

In reading Scorecasting, well reviewed and recommended by the chair, I came across a point that hits home when looking for statistical causal relationships. When x variable appears to be related to y variable, it is very possible that an undiscovered variable z has a much larger effect, perhaps on both variables. There are examples of this in the book, mostly thoroughly explained in the home field advantage. This is empirically shown to be true across, time, cultures and sports, running at an advantage of 55% to 70% in favor of the home team. Controlling for other things, crowd size does correlate very highly with the home team advantage. But changes is crowd size are shown to have no effect on players performance. Rather crowd size influences officials, but it is secondary affect. The primary affect is officials themselves who have a in bias (most likely unknown to themselves prior to this book) to favor home teams regardless of the fans. Crowd size amplifies or dims this already existing bias. Had the authors not researched deeper this point would have been lost.

In reading Scorecasting, well reviewed and recommended by the chair, I came across a point that hits home when looking for statistical causal relationships. When x variable appears to be related to y variable, it is very possible that an undiscovered variable z has a much larger effect, perhaps on both variables. There are examples of this in the book, mostly thoroughly explained in the home field advantage. This is empirically shown to be true across, time, cultures and sports, running at an advantage of 55% to 70% in favor of the home team. Controlling for other things, crowd size does correlate very highly with the home team advantage. But changes is crowd size are shown to have no effect on players performance. Rather crowd size influences officials, but it is secondary affect. The primary affect is officials themselves who have a in bias (most likely unknown to themselves prior to this book) to favor home teams regardless of the fans. Crowd size amplifies or dims this already existing bias. Had the authors not researched deeper this point would have been lost.

Pitt T. Maner III writes:

It is interesting that there are sites that keep statistics on the refs now too.

The held ball call near the end of the Louisville-Wichita St. Final 4 game by Karl Hess appeared particularly bad but you wonder what the factors and influences are that might have led to it. The game finish would have been much more enjoyable if the Shockers had had at least one last attempt at a 3-pointer to tie the game.

Was it the nearby presence of the Louisville coach Rick Pitino? An ego issue where the ref felt the need to decide the contest? Crowd influence? TV audience thoughts? Subconscious need to end the game and prevent possibility of overtime (desire to get off the court,)? Something a player said (need to payback for perceived questioning of previous call)? A whistle blown by mistake in a hurry with no means to take back (I never make a bad call in an important contest). Lots of possibilities.

Russ Sears writes:

When watching a game, I have often thought that the bias in the ref could be spotted by whether or not they avenge a bad or close call on one side by giving the next close call to the opposing team. After a moment of reflection, the ref probably realizes he blew the whistle too soon or did not blow the whistle when he should have. However, it appears to me that the avenged even handed blown calls are often one sided. Yet when watching a game, my own biases would prevent me from "counting" this fair.

Perhaps the broadcasters in a national game could be counted on, but it appears to me they have a vested interest to give the losing team something to complain about. If I recall correctly, the tie-up was initially called a great defensive play by Louisville, but then changed to blown call.

Apr

4

Carry Trade, from Duncan Coker

April 4, 2013 | Leave a Comment

Back in the pre crisis era (before negative real rates) hardly a day went by when the carry trade wasn't mentioned in some form or another. If the carry boys are still around they must be enjoying the BOJ policy. For example, AUD up 17% versus yen plus a 3% rate kicker, without leverage. It is roughly the same for NZD. I was told they never hedge the currency risk and put on at maximum leverage so returns could be many multiples higher, but I may be misinformed on that part.

Anatoly Veltman writes:

Of course, a funny BOJ announcement comes out right after your query– which may pretty soon invert the carry trade! Yen may soon become the highest yielding G-7 currency.

Mar

18

Market Scales, from Duncan Coker

March 18, 2013 | Leave a Comment

I played guitar for many years, but recently I've been taking to practicing scales which in my younger days I rejected as too boring. Now, far from tedious, I find it relaxing, challenging, helpful to develop dexterity skills and better timing. Musical theorists will know that every major scale has a relative minor scale (I just learned this, so never too late). The notes are exactly the same, the scale simply starts from a different root note. But that root note makes all the difference since the tonality of the scales are like day and night. The concept of a relative minor should have a place in the markets, the darker side of the optimistic (major) equity markets with the same notes, just played in a different order.

I played guitar for many years, but recently I've been taking to practicing scales which in my younger days I rejected as too boring. Now, far from tedious, I find it relaxing, challenging, helpful to develop dexterity skills and better timing. Musical theorists will know that every major scale has a relative minor scale (I just learned this, so never too late). The notes are exactly the same, the scale simply starts from a different root note. But that root note makes all the difference since the tonality of the scales are like day and night. The concept of a relative minor should have a place in the markets, the darker side of the optimistic (major) equity markets with the same notes, just played in a different order.

Mar

15

HFT, from Duncan Coker

March 15, 2013 | Leave a Comment

Despite what I have read I am not convinced the HFT in aggregate are profitable. Buying High, Selling low, and making it up on volume just does not seem like a good business model to me. The research on HFT seems unadjusted for survival bias. They study the biggest and most profitable firms to see how big and profitable they are. I personally know an HFT firm that made money 3 years in a row, then after 4 months of bad performance they realized their edge was gone and they closed shop. I am sure they were never included in HFT research. I use limit order so I suppose HFT is taking the other side and the jury is still out.

Jim Lackey writes:

Of course, Dunc, it should be like all things sports MX. Top 10 sleep in the Hilton and ride in the Factory rig and the next 10 best in the world sleep in their trailer in the pits 20-99 are part timers and lose money racing.

Feb

22

Next Month, from Duncan Coker

February 22, 2013 | 1 Comment

No doubt that any cuts next month will be targeted to inconvenience the public most directly like travel, preferably during school breaks. After all if no one noticed what's to stop them from making, horrors, additional cuts.

Feb

8

Richard III, from Duncan Coker

February 8, 2013 | Leave a Comment

It is remarkable they found remains

It is remarkable they found remains

Of Richard Three, the King that none could tame.

The discovery of the body of Richard III this week could be a hoax. However, I think not given the carbon dating, the matching historical features of the body, and the evidence of DNA linked to known descendants. It is history and legend transported to the present. Richard is made famous by Shakespeare who depicted him as one of history's greatest tyrants. True or not, I believe the Bard was most concerned with universal truths ahead of historical accuracy.

Along those lines, I am reading an interesting book on the forms of poetry. All the Fun's in How You Say a Thing, by Timothy Steele. Poetry of 14th and 15th century England was evolving from Old English to a newer form. Word accent, syllable-count, and rhyming pattern were the essential features. Most popular was an alternating accent (iambic), with 5 segments or feet per line (pentameter). The works of Chaucer, Shakespeare, Milton, Johnson and Pope were written in iambic pentameter. Modern poets like Robert Frost use it as well. Close to me, I can recall my Grandfather teaching me poems. He kept his favorite works by Samuel Johnson and Walt Whitman near at all times. It is relevant still, and learning the forms of verse makes poetry more meaningful.

I think of rhythm when generalizing about prosody, as I do in sports, music and even markets. The early markets in England were developing along with the Great Poets and perhaps there were mutual influences. The patterns in verse are made interesting by exceptions and variation, not unlike markets. On this stormy Northeast weekend, dust off the books of poems from university days.

It's true that time's well spent with poetry.

For snowy days and children full with glee.

Jan

28

Range Bound Skiing, from Chris Tucker

January 28, 2013 | 1 Comment

I was skiing in Vermont recently and as is usual for skiing in the northeast, the slopes weren't as deeply covered with snow as one would wish. When one attacks a steep run in these conditions, it is guaranteed that the center of the trail will be bereft of snow — thin cover is the term we use euphemistically to indicate ice and rocks — mostly ice though. When this happens, there can usually be found some snow piled on the edges of the trail, it having been pushed there by previous skiers who made all their turns in the center, their scraping edges clearing it away off of the underlying hardpack and pushing it to the sidelines.

Skiing in such conditions can be done, but not without incurring greater than normal risk. And it is usually not as satisfying as skiing using the entire available path whose deeper, more sweeping turns are somehow more satisfying and which provide greater control. But under these conditions, staying in the center is deadly so advanced skiers will stick to the edges of the trail, making all of their turns in rapid succession on what is in effect a trail only two or three feet wide. This means that turns must be small in degree and therefore must happen very quickly so as not to allow the tips to remain pointed straight down the hill and therefore incurring excessive speed. This kind of skiing requires conditioning, linking extremely rapid turns is exhausting and one must not attempt this when fatigued as the resulting inability to really push hard and dig can be catastrophic. It also requires some nerve, for one, keeping near the edge puts one in dangerous proximity to the treeline (or the edge of the abyss -as the case may be) and one slip at high speed and it's all over. And it means high speed, even while carving one edge after another in succession, the lack of available surface on which to gain traction means keeping the tips pointed perilously close to straight down the fall line. Mistakes at these speeds tend to have greater than normal undesirable consequences.

As I enjoy the speed, I will make one or two runs in these conditions just for the thrill of it, but this kind of tight skiing in a narrow and steep path requires tremendous concentration and loses it's appeal rather quickly. I will spend the majority of my time on tamer runs with more snow, even though they may be more crowded, so I can make the more gratifying, longer, carving turns that I prefer.

Jeff Watons writes:

That's just like surfing big waves vs small waves.I am not comfortable in the brutal conditions Mr Sogi San surfs on an every day basis. In those conditions, I will look for the rip current to get outside, paddle and make a bottom turn, and ride it in. Like typical Sunset. I don't stay out very long as I did when I was younger when it is big. But if the waves are 2-3' overhead, I'm good all day long. I'll still find the rip to make paddling out easier, but I'll attack the wave harder. But some of the very best days are those waist-chest high waves where you cruise on a long board, and catch the glide. However, during calm conditions I have suffered the greatest traumas while surfing. Broken vertebra, herniated discs, tendon and ligament damage, broken nose, etc. Somehow, being relaxed while it's calm is more dangerous then when it's big. Or maybe I'm more careless when the waves are small, and a bit reckless thrown in for good measure. Carelessness happens in the markets also. You start taking your profits for granted. It's humming along nicely with all your positions in the green, then wham, the Mistress gets a little PMS(no sexism intended) and throws the whole system off balance or upsets the cart, and your account suddenly needs a tourniquet. The lesson here is to keep your guard up at all times.

Jim Sogi writes:

Just back from backcountry skiing in the Eastern Sierras. The conditions were snow that was about a week old, with very cold temperatures, and no wind. The sun made a crust where solar energy hit, so the powder stashes were hidden on north facing aspects where there were old growth trees. The cold had dried out the snow making it sparkle and soft and creamy sugar which was excellent for skiing.. Though it had not snowed for over a week, in the shade, on the north facing slopes shaded by old growth pine where the sun did not affect the snow there was beautiful sugary soft powder. It took some doing finding these niches and some hiking to get there and fighting some pesky brush at lower elevations. No one else seems to have discovered these hidden stashes of nice powder. This reminds me so much of the markets, when even in less than optimal conditions, there are hidden stashes of unridden goods. It takes understanding of the underlying processes that create and destroy snow, the equipment and will to get there, and the ability to ride those conditions. Its surprising in such a huge mountain range that only in such limited conditions would there exist such fine skiing. The last day, new wet snow came and turned everything into the famous Sierra cement.

Just back from backcountry skiing in the Eastern Sierras. The conditions were snow that was about a week old, with very cold temperatures, and no wind. The sun made a crust where solar energy hit, so the powder stashes were hidden on north facing aspects where there were old growth trees. The cold had dried out the snow making it sparkle and soft and creamy sugar which was excellent for skiing.. Though it had not snowed for over a week, in the shade, on the north facing slopes shaded by old growth pine where the sun did not affect the snow there was beautiful sugary soft powder. It took some doing finding these niches and some hiking to get there and fighting some pesky brush at lower elevations. No one else seems to have discovered these hidden stashes of nice powder. This reminds me so much of the markets, when even in less than optimal conditions, there are hidden stashes of unridden goods. It takes understanding of the underlying processes that create and destroy snow, the equipment and will to get there, and the ability to ride those conditions. Its surprising in such a huge mountain range that only in such limited conditions would there exist such fine skiing. The last day, new wet snow came and turned everything into the famous Sierra cement.

Laurel Kenner writes:

I took Aubrey to our favorite ski place, Telluride, a couple of weeks ago. A drought was on and the mountain was brown, but the resort's snow-making machines had been at work since November and most runs were open. A few patches of grass were visible in some popular places — enough to send a skier head over heels in the old days. The new equipment was somehow able to ride it out, although caution was still warranted. That strikes me as like the market; if you're well-equipped enough with margin and numbers to ride out the rough patches, you can still do well in adverse conditions.

Steve Ellison writes:

I ski 10-15 times per year and encounter a wide variety of conditions. Light is an important factor. An overcast sky causes what skiers call "flat light". I slow down in flat light because the lack of shadows makes it hard to spot irregularities on the surface until one is nearly upon them. Dense fog is even worse. I have been in fogs in which I could not see the trees on either side and momentarily lost track of which way was down.

I like fresh snow, but there can be too much of a good thing. One day right after a 2-foot snowstorm, I started down my first run and fell on the very first turn when my outer ski caught some snow. I pushed off my hand to get up, but my arm sank into the snow all the way to my shoulder. It took a few minutes of wiggling and maneuvering to get back on my feet.

Wind is another factor. The Sierras sometimes have very high winds, which blow loose snow off exposed areas. The result is alternating ice and soft powder (in the spots in which blown snow settles). Going too fast at the transition point can result in a fall. On one traverse I often ski, I use moderate wind to my advantage by letting the wind slow me down as I ski into it with no effort on my part.

Duncan Coker writes:

When backcountry skiing which Mr. Sogi describes another key element is the approach. There are no lifts, so you hike uphill for every turn you will make downhill. It can be exhausting, but also very rewarding and you get to know the terrain including snow pack, the location of rocks, couloirs, tree wells, cliffs and the grade. After enjoying the view at the top you can descend focusing mainly on execution, making some nice turns. Skiing the steeper, untouched terrain has more dangers but is more rewarding.